Good morning! The newswire has now officially come back to life.

1pm: this report is finished! I'll hopefully get something from the backlog covered for tomorrow.

Analyst Roundtable: last night's webinar with Ed, Megan and me is available on replay here.

Spreadsheet accompanying this report (updated to 3/1/2025).

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Tesco (LON:TSCO) (£24.8bn) | Q3 & Christmas TU | ‘Biggest ever Christmas’ and largest market share since 2016. Sales +3.1% over Q3 + Christmas. | AMBER/GREEN (Graham) |

Marks and Spencer (LON:MKS) (£7.6bn) | Christmas TU | “Another good Christmas”. LfL rev +8.9% (food), +1.9% (clothing). Confident of further progress. | AMBER/GREEN (Megan) |

Unite (LON:UTG) (£3.9bn) | Q4 TU | Strong demand and increased rental for 2025/26 academic year. Guidance confirmed. | |

B&M European Value Retail SA (LON:BME) (£3.5bn) | Q3 TU | Narrows adj. EBITDA guidance to £620m-650m (prev: £620m-660m). | AMBER (Graham) |

Greggs (LON:GRG) (£2.7bn) | Q4 TU | Slower Q4 sales, but full year revenue and profits in line with board expectations. | AMBER/GREEN (Megan) |

Assura (LON:AGR) (£1.2bn) | Q3 TU | Rent roll slightly down, but disposal programme on track with net proceeds of £48.4m. | |

Hilton Food (LON:HFG) (£804m) | TU | 2024 results in line with expectations. Confident for 2025. FX rates an area of focus. | |

IP (LON:IPO) (£481m) | Share buyback programme update | Launches £25m buyback extension, bringing it up to £70m. | |

Boohoo (LON:BOO) (£433m) | Letter from the Board | Again urging shareholders to reject proposals by Frasers. Resolution seeks to remove Mahmud Kamani. | |

Foresight group (LON:FSG) (£423m) | TU | AUM down 2% over 3 months. Fundraising in line. On track to double core profitability by FY29. | |

Mears (LON:MER) (£317m) | TU | FY24 marginally ahead of exps. Company increasingly confident of delivering exps for FY 25. | |

Impax Asset Management (LON:IPX) (£310m) | Q1 AUM Update | AUM falls 8.3% to £34.1bn. Termination of large mandate with STJ takes effect in Feb 2025. | GREEN (Graham holds) |

SIG (LON:SHI) (£176m) | 2024 Full Year TU | LfL rev -4%. Adj. op profit c. £25m, in line. Continued market softness at least in H1 2025 is expected. | |

H & T (LON:HAT) (£150m) | TU | Pledge book ahead of expectations. Comment on higher NI costs which management will attempt to mitigate. | GREEN (Graham) |

Ground Rents Income Fund (LON:GRIO) (£31m) | Response to possible offer | BoD believes the offer undervalues the company. BoD is now receiving feedback from shareholders. | |

Cirata (LON:CRTA) (£27m) | Q4 TU | Q4 cash burn $3.2m. Cash $9.7m. Does not anticipate FY25 fundraise for working capital. |

Summaries

H & T (LON:HAT) - up 2% to 341.9p (£150m) - Trading Update - Graham - GREEN

A good update from this pawnbroking group with the pledge book continuing to grow at a very impressive rate for a mature business, up over 25% in a year although that is boosted by a small acquisition. Higher-value secured loans to people who may use the funds for business purposes are becoming increasingly important. Looking ahead, estimates for FY25 are unchanged for now at the company’s broker Canaccord, as it is thought that the higher-than expected growth in the pledge book will help to offset the c. £2m expense from higher national insurance contributions.

Greggs (LON:GRG) - down 9.5% to 2376p (£2.7bn) - trading update - Megan - AMBER/GREEN

Final quarter sales suffered amid lower than anticipated high street footfall meaning like-for-like sales for the full year are lower than many investors would have liked. The store estate continues to be bolstered by new openings, which helped Greggs report its first annual revenue of more than £2bn. Cost inflation thanks to rising national insurance contributions is likely to kick in in April, although management insists this won’t hurt the company’s value proposition.

Marks and Spencer (LON:MKS) - down 6% to 353p (£7.7bn) - Christmas trading update - Megan - AMBER/GREEN

Continued very strong sales growth in the food division (64% of total sales) was offset slightly by a weaker than expected non-food performance. Overall the company reported a 5.6% increase in sales to £4bn over the 13 weeks to 28 December. The challenge for the company (which has been a phenomenal turnaround story over the last couple of years) will be where the next level of growth comes from.

Impax Asset Management (LON:IPX) - down 4% to 233.7p (£310m) - Q1 AUM Update - Graham holds - GREEN

It’s a poor AUM update but I find a few reasons to look on the bright side. Equity Development have left their profit forecasts virtually unchanged, and a large chunk of the outflow this quarter is attributable to the loss of one of the St. James’s Place mandates, with the loss of these mandates striking me as a one-off event. Valuation is in the dumps compared to Impax’s history; I think that risk:reward is positive from this level, but the trend in terms of flows and share price momentum is against me.

B&M European Value Retail SA (LON:BME) - down 12% to 305.7p (£3.1bn) - 3rd Quarter Trading Update - Graham - AMBER

There is only a slight narrowing of the range of profit expectations by BME, along with confident commentary from management, but the market is unimpressed - even with the announcement of a £150m dividend. Perhaps investors think that management should be more careful, given net debt (before leases) of nearly £800m?

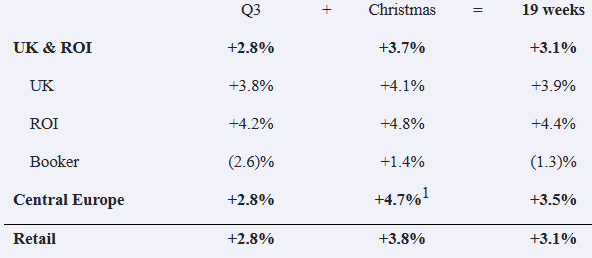

Tesco (LON:TSCO) - down 1% to 366p (£24.5bn) - Q3 & Christmas Trading Statement - Graham - AMBER/GREEN

This update confirms guidance for adj. operating profit of £2.9 billion this year, and also reaffirms guidance for retail free cash flow of £1.4 - 1.8 billion. Like-for-like sales numbers are up by 3.1% with strength in UK/ROI offset by a little weakness at wholesale distributor Booker. I’m happy to take a mildly positive stance given the robust performance and moderate PER of 13x.

Graham's Section

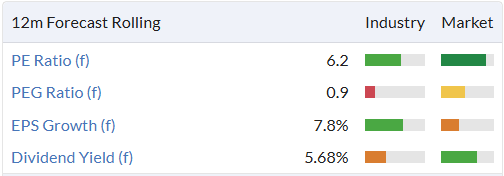

H & T (LON:HAT)

Up 2% to 341.9p (£150m) - Trading Update - Graham - GREEN

This update is in line with expectations. Key points:

Pledge book grows ahead of management expectations to £127m as of the end of December (Dec 2023: £101m). Includes £6m pledge book at the acquired company Maxcroft.

18% of the pledge book now consists of loans for over £5k, often used for business purposes (Dec 2023: 13%).

Back in August, a big topic for H&T was the increased seasonality of pawnbroking demand. There was a pattern of high redemptions (i.e. customers repaying loans and taking back their items) in March and April, “to wear them at religious and family celebrations”.

The company is even changing its accounting year-end in response to this, apparently to get a more even split between H1 and H2.

That’s the context in which H&T says:

The Group's current planning assumption is that there will be lower pledge book growth in the spring, due to increased levels of redemptions, followed by a period of stronger growth in later months. This is consistent with the way the pledge book developed in 2024. As such, we do not anticipate material pledge book growth in the first or second calendar quarters of 2025, with growth expected to return in the third and fourth calendar quarters of the year.

Their accounting year-end will change to September, so that H1 will not include the two weakest calendar quarters (Jan-March and April-June).

Other points: retail sales in the peak trading period met expectations. The pre-owned watch market has stabilised. Foreign exchange revenues also in line.

National insurance: employment costs to increase by c. £2m p.a. They are “reviewing options to mitigate the impact where possible”. However, I can’t imagine what direct options they have when it comes to mitigation, other than hiring fewer part-time staff.

Estimates: Canaccord say that they are still confident in their FY25 forecasts, thinking that revenues from the higher-than-expected pawnbroking pledge book should largely offset higher national insurance costs.

H&T is fortunate that its current profitability gives it a cushion to deal with higher NICs. Adj. PBT is expected to come in at £29m for FY24, £32.2m for FY25, and £34.8m for FY25.

The EPS estimates are 49.2p (FY24), 54.6p (FY25), and 59p (FY26).

Graham’s view

I’ve been a fan of this one for many years and I was GREEN on it in August despite a little frustration with what I perceived as a covert profit warning.

The share price in August was over 400p and at c. 340p now, I think I have to remain positive on it today. The main news since August is the national insurance, and while that’s a blow, I’m not sure that it’s enough on its own to justify the 15% decline in the share price since then.

So I’m happy to stay positive on this one as a value play: its ValueRank is 94 and the company remains the market leader by far in UK pawnbroking, with a legacy going back well over 100 years:

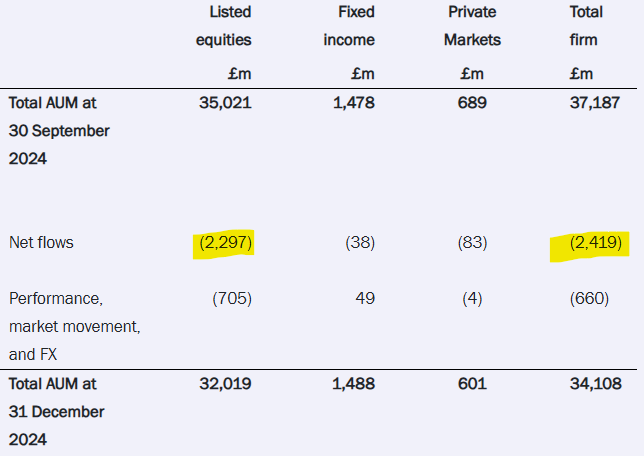

Impax Asset Management (LON:IPX)

Down 4% to 233.7p (£310m) - Q1 AUM Update - Graham - GREEN

(At the time of publication, Graham has a long position in IPX.)

This ESG-focused fund manager provides an assets under management update that makes for grim reading:

We have a £2.3 billion outflow from listed equities, creating a £2.4 billion outflow across the group.

Market movements didn’t help either; the overall result is an 8.3% decline in AuM in a single 3-month period.

The CEO comment now emphasises the need for efficiency and cost management:

"This quarter we saw relatively high outflows, notably the closure of our smaller mandate with St. James's Place and redemptions driven by industry consolidation in our institutional channel in the Asia-Pacific region. More positively, we have continued to see a slow-down in outflows from our largest European distribution partner, BNP Paribas Asset Management, and from our US mutual funds…

…we continue to pay close attention to the efficiency of the business and the management of costs in the context of providing an excellent service to clients.

The larger mandate with St James’s Place, worth £5bn, will be lost in February.

Graham’s view

You can find my most recent writeup of Impax here, in the 12 Stocks of Christmas series.

I initiated a position here, after the announcement of the loss of the larger STJ mandate, as I thought the valuation had reached such an extreme level that it would be difficult for the stock to offer much better value than this.

Unfortunately, things have gotten a little worse with the continuation of the trend of outflows, as announced today. Let’s review flows over the past year:

Q1 FY24: net flows minus £1.0 billion

Q2 FY24: net flows minus £1.7 billion

Q3 FY24: net flows minus £1.9 billion

Q4 FY24: net flows minus £1.2 billion

Q1 FY25 (announced today): net flows minus £2.4 billion.

The only consolation I can find is that this very poor outflow figure announced today includes a one-off event in the form of the loss of one of the STJ mandates. I think that mandate was possibly worth c. £750m. So if it was not for that loss, IPX’s outflows in Q1 FY25 would have been similar in size to some of the previous quarterly outflows.

How long can this trend of outflows last - indefinitely? As I said in yesterday’s webinar, some people will take the stance that conventional fund management is dead. Personally I don’t believe that, but I do agree that it needs to change. The industry needs to work harder to make its fees competitive and to make its offerings as relevant and as specialised as possible.

I think that Impax still has a great deal of credibility as an ESG investor. However, it’s proven now that it’s not immune to the general wave of pessimism around UK fund managers.

Is all of the bad news priced in here? Personally I believe that it is, but that’s just my opinion:

Estimates: Equity Development have cut their AUM forecast but other forecasts are virtually unchanged, e.g. they still expected 23.9p of EPS in FY Sep 2025 (previous forecast: 24p).

B&M European Value Retail SA (LON:BME)

Down 12% to 305.7p (£3.1bn) - 3rd Quarter Trading Update - Graham - AMBER

BME hasn’t been covered much in this report historically, as it’s been considered too big.

I see that Paul briefly mentioned it in June, when the share price was over 500p.

The 1-year chart shows it making progress towards small-cap territory:

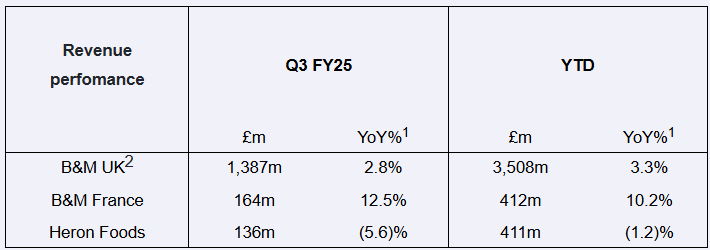

Let’s investigate today’s Q3 update (Oct-Dec, as financial year-end is March). Highlights table:

Unfortunately the numbers in this table are not like-for-like, as store openings are growing total revenue.

The like-for-like revenue figure for B&M UK in Q3 was actually minus 2.8%. However, the performance sounds fine apart from that:

B&M UK gross margin and profit performance was strong in the quarter, with a clean inventory exit position. January seasonal transition is well on track and availability is very strong

Further confidence is seen in the announcement of a special dividend of 15p per share, or £151m.

The company’s leverage multiple was 1.2x at the interim results, a modest level but I think in physical retailing, where store leases create additional leverage, we need to be particularly careful about debt. BME’s net debt figure was £788m.

CEO comment: he narrows the adj. EBITDA guidance slightly to £620-650m (previously: £620-660m).

Our performance across the Golden Quarter reflects disciplined operational execution across our businesses, driving volume and in turn profit growth. The business remains undistracted by the current economic headlines. Our operating model is well set up to give customers exceptional value when they need it most. Pricing, availability, store standards and a disciplined opening programme will underpin positive volume growth across our ranges…

Graham’s view

The 12% fall in the share price seems a little over-dramatic to me, given that there has been such a small downward revision to the profit guidance.

However, value retailers are out of favour these days and so I suppose any slight disappointment can be a reason to sell. The negative like-for-like sales figure in the main UK segment is an easy excuse to hit the sell button, even if many investors were already expecting a poor number.

I also think that the company’s ambitious growth plans (73 new stores in FY25, and dozens more in FY26), along with the announcement of a special dividend, seem inconsistent with a business where like-for-likes are negative and where profits have been struggling to tread water in recent years. Perhaps the sell-off could also reflect nervousness that management are taking on too much risk?

I am extremely selective in this sector and B&M doesn’t stand out to me as a particularly good candidate for investment in it. I’m happy to take a neutral stance on it while its profits are holding up, but I wouldn't sleep soundly owning it.

Tesco (LON:TSCO)

Down 1% to 366p (£24.5bn) - Q3 & Christmas Trading Statement - Graham - AMBER/GREEN

Let’s briefly check in on Tesco: like-for-like retail sales are up 3.1% in UK/ROI, with the Christmas period slightly stronger than the Q3 period that preceded it:

The CEO has nothing but praise for the result:

Our strong performance reflects the investments we have made, positioning Tesco as the UK's cheapest full-line grocer for over two years, improving quality across all our ranges, with more than half of this year's Christmas range new or improved, and providing the best experience for our customers in-store and online, supported by an extra 28,000 colleagues over the Christmas period.

TSCO’s share price has been very strong over the last couple of years:

It is hard to criticise the company’s achievements, such as 19 consecutive periods of market share gains with share taken from competitors at both the higher and lower end of the price spectrum.

Outlook: in line with previous guidance.

The ongoing investments in our customer offer continue to drive volume momentum and set us up well to deliver long-term growth. As a result, we continue to expect to deliver retail adjusted operating profit for the 2024/25 financial year of around £2.9bn, in line with the upgraded guidance we gave at our Interim Results.

In addition, we continue to expect retail free cash flow within our medium-term guidance range of £1.4bn-£1.8bn and adjusted operating profit contribution from the retained Tesco Bank business of around £120m.

Graham’s view: I have no criticism to make of Tesco whatsoever but from an investment point of view, it’s virtually the definition of a mature business in a below-average sector. Even at a StockRank of 90, I’d struggle to get very excited about this one. However, as I gave BME an AMBER today, I think I should make this AMBER/GREEN to differentiate it.

Megan's Section

Greggs (LON:GRG)

Down 9.5% to 2376p (£2.7bn) - Trading Update - Megan - AMBER/GREEN

For the second time in as many updates, Greggs’ management has managed to avoid using the dreaded term ‘below expectations’ thanks to previous vagueness on what those expectations might be.

In the first half of 2024, like-for-like sales (which takes into account revenue generated at the company’s own managed stores) rose 7.4%. In Q3 that had fallen to 5% and in these numbers (for the three months to December) like-for-like sales growth was just 2.5%. Management blames that performance on the “well-publised” lower consumer confidence in the UK in the last few months, which impacted high street footfall over Christmas.

I have written before about my penchant for a Greggs baguette and Q4 2024 was no different. I visited seven different Greggs stores in the period under review (four of them on local high streets) and each one was just as full as I have ever seen it. The most significant queue was at the Cherwell service station on the M40, when I gave up and went to Burger King instead.

Now my survey of one is not as reliable as the very real trading statement, which does show that the company as a whole is struggling to maintain growth across its existing store estate. But the demand in certain locations, especially in the south of England demonstrates how there should still be optimism for the roll-out programme.

In 2024, Greggs opened a record 226 new shops, closing the year with 2618 stores in total. That is now more than the number of UK McDonald’s, KFC and Burger King restaurants put together. Greggs’ management have plans to add at least another 140 stores in 2025.

Adding new stores has been key to the Greggs growth journey. In 2024, total revenues rose 11%, passing the £2bn mark for the first time. In the last five years, sales have risen at a compound annual rate of 12%.

Price inflation concerns?

In 2023, Greggs employed an average of just over 30,000 staff, 25,400 of whom worked on the shop floor and are likely to be part-time or lower paid. In other words, the kind of staff who are most likely to be caught up by higher national insurance bills, due to come into effect in April. Greggs’ total wage bill in 2023 was £519m, equivalent to roughly 60% of the company’s selling costs.

Management says that higher employment costs will impact the company’s overall cost base in 2025, but seems unconcerned about the potential impact on margins:

“Greggs has demonstrated its ability to mitigate cost inflation in recent years whilst retaining its value leadership, and we are confident we can continue to do so.”

There is likely room for some inflation in a Greggs meal. Compared to its peers, the company’s food offering is phenomenally cheap. But being cheap is part of the demand, so Greggs will want to ensure it maintains its position.

There are other ways of mitigating rising staff costs and that is through increased automation. Many of the company’s larger, American peers are already using self-service machines in their stores and there could be scope for Greggs to decrease the number of in-store staff, especially in some of its newer locations.

Megan’s view:

A price to earnings ratio of 18x is a more enticing valuation than Greggs has had for some time and likely reflects some of the fears around price inflation. This is a high quality company which reports decent operating margins and a very strong return on capital (ROCE has averaged 21% in the last five years, adjusting for the loss-making period during the pandemic).

But to justify that sort of PE ratio, the company must keep growing and an expansion of a store estate, which at some point is surely going to start saturating the UK market, feels like quite a tall order.

I really would like to be fully positive about Greggs, because I think it is a fantastic business, but I am hedging my bets and waiting for more clarity on the cost inflation in the annual results. AMBER/GREEN

Marks and Spencer (LON:MKS)

Down 6% to 353p (£7.7bn) - Christmas trading update - Megan - AMBER/GREEN

Marks & Spencer seems to have swerved the cost of living crisis. More customers than ever ticked off their whole shopping list at M&S according to the company’s Christmas trading update, with like-for-like food sales up 8.9%. Food contributed just over two thirds of overall revenue in the period, with the remainder coming from the far slower growth clothing business and the insignificant international division.

Food has been central to the turnaround at MKS, which has enjoyed an uninterrupted growth trajectory since the middle of 2022 when the share price fell below 100p. Now at 353p investors who backed the turnaround have made a handsome profit.

But where next?

In this trading update, Stuart Machin, chief executive commented:

“Transforming M&S is a marathon, not a sprint, and we go into 2025 shifting up a gear and raring to go as we accelerate the scale and pace of change.”

That change is expected to come from continued improvements in the supply chain, which will help improve the volume of goods that can be delivered, especially in some of the company's smaller food stores. In clothing, home and beauty there remains scope for greater use of digital channels. In the first half, online sales contributed a third of the division’s overall revenue after reporting 11% growth. Management hasn’t given an exact update on the online growth in these numbers, but did say online sales grew strongly.

Megan’s view:

The turnaround at MKS has been fantastic, but growth in the food division alone is no longer going to cut it, shareholders seem to have been spooked today by the slowdown in non-food growth, which was only 1.9% on a like-for-like basis.

Ongoing economic jitters also create some level of concern for a company which is known for its more premium price point (although that didn’t seem to have much of an effect in 2024).

In November, Graham downgraded Paul’s GREEN rating as the easy share price gains seemed to have all been achieved. Now trading on 12 times forecast earnings, the company will need to step up a gear. And while management has promised some acceleration, the disappointing non-food sales don’t instill as much confidence as I would like. AMBER/GREEN .

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.