Good morning!

1pm: wrapping this up for now. See you tomorrow!

Explanatory notes

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day. We usually avoid the smallest, and most speculative companies, although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We have a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Add your own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing. Links:

Daily Stock Market Report: records from 5/11/2024 (format: Google Sheet).

Companies Reporting

Name/Mkt Cap | RNS | Status/ brief comment | Our view (Author) |

Ashtead (LON:AHT) (£27bn) | Final Results & US listing | Profit warning due to US weakness. FY rev growth exps cut from 5%-8% to 3%-5%. | AMBER (Roland) Previewed in The Week Ahead (MB). |

Centrica (LON:CNA) (£6.7bn) | TU | 2024 earnings expected to be “broadly in line”. | |

Games Workshop (LON:GAW) (£4.6bn) | Amazon agreement. | GAW has finalised its long-awaited deal with Amazon. | GREEN (Roland) |

Moonpig (LON:MOON) (£919m) | Half-year Results | In line. H1 adj PBT +9% to £27.3m, but £56m impairment relating to Experiences division. | |

NCC (LON:NCC) (£511m) | Final Results | There is a recent lengthening of sales cycles. Expecting flat to low single digit revenue growth. |

AMBER/RED (Graham) Down 18%. |

Boohoo (LON:BOO) (£492m) | Letter from the board | The board wants shareholders to vote against the GM resolutions. | |

Porvair (LON:PRV) (£305m) | TU | FY rev +9%, adj eps “marginally ahead” of exps. | |

Begbies Traynor (LON:BEG) (£150m) | Half-year Results | In line. Broker slightly increases revenue forecasts (FY25 & FY26) but adj. PBT forecasts are unch. | AMBER (Graham) |

hVIVO (LON:HVO) (£145m) | Contract win & TU | £11.5m contract to deliver in 25/26. FY24 EBITDA margins at “upper end” of exps. | AMBER (Megan) |

Springfield Properties (LON:SPR) (£106m) | TU | In line. | |

Solid State (LON:SOLI) (£68m) | Interim Results | Existing forecasts maintained by broker Cavendish, except for a reduced dividend. | AMBER (Roland) |

Naked Wines (LON:WINE) (£42m) | Half-year Results | In line. | |

Tortilla Mexican Grill (LON:MEX) (£19m) | TU | FY24 in line, but UK trading ahead. | |

Cambridge Cognition (LON:COG) (£12m) | Trading Update | Profit warning. 2024 revenue £10m (prev: £14m) and adj. EBITDA breakeven (prev: £0.5m). | |

Pennant International (LON:PEN) (£12m) | TU | In line. FY24 exps for rev of c.£14m and adj EBITA of c.£1.2m. |

* Market caps at previous trading day’s close

Summaries

Brave Bison (LON:BBSN) - down 3% to 2.1p (£27m) - Acquisition and Trading Update - Graham - AMBER/GREEN

I approve of this acquisition. Despite buying a loss-making company (even at the EBITDA level), BBSN has made the vast majority of the nearly £11m price conditional on the performance of the business after acquisition. Strategically the deal makes good sense to me and I remain impressed by BBSN’s financial performance.

Begbies Traynor (LON:BEG) - up 5% to 99.1p (£156m) - Half-year Results - Graham - AMBER

Another sturdy performance from BEG as it benefits from elevated levels of insolvency activity and good volumes in the non-residential property market. A small net debt position should cause no concern relative to ongoing profitability. I remain neutral as I think it’s fairly priced at a PER of about 10x for a professional services business.

Solid State (LON:SOLI) - up 6% to 127.5p (£73m) - Half-year Results - Roland - AMBER

Full-year expectations for this electronics supplier have been left unchanged, underwritten by an increase in the order book since 30 September. I remain positive on the long-term story and see this as a potential contrarian pick, but demand remains weak and recovery timing is uncertain.

Ashtead (LON:AHT) - down 12% to 5,522p (£24bn) - Half-year results & US listing - Roland - AMBER

This construction equipment hire group generates most of its profits in the US and has been hit by a slowdown in local construction in that market. The longer-term picture remains positive in my view, but I don’t see any need to rush in after today’s profit warning.

Graham's Section

Brave Bison (LON:BBSN)

Down 3% yesterday to 2.1p (£27m) - Acquisition and Trading Update - Graham - AMBER/GREEN

This is a digital marketing agency that has in general been viewed positively in this report, due to sound financial health - see Paul’s review in September.

The company tried and failed to acquire TMG (Mission) this year.

Yesterday we learned that the company had found a new target: “Engage Digital Partners Limited”, “a global sports marketing company that works with the world’s largest sports brands and federations including Formula 1, ICC, Real Madrid and New Zealand Rugby”.

The rationale makes good sense to me:

Engage will combine with Brave Bison's existing network of channels, which already benefits from partners such as PGA Tour, Ryder Cup, US Open, Australian Open, CPLT20 and Le Mans. The combination will create an enlarged sports & entertainment division for Brave Bison partnering with channels across football, cricket, motorsports, tennis, golf, e-sports and rugby, and totalling £16 million in pro-forma turnover.

Cost: up to £10.6m, but only £2.1m is guaranteed.

For labour-intensive marketing work, it makes sense to me that a large part of the acquisition price would be conditional on performance after acquisition.

This is especially true as I note that Engage is expected to post an EBITDA loss on revenues of £6.9m for 2024. So Brave Bison are doing the right thing by protecting themselves against buying a dud: if Engage helps their performance to improve, they will pay handsomely, but if it doesn’t, they might have to pay very little.

There are two legs to the conditional payments: first up is “equity consideration of £2m”, taking the form of 66.7 million warrants over BBSN shares. The existing BBSN share count is 1.3 billion, so the potential dilution from these warrants is small.

The warrants can’t be exercised until 2028 and “will only vest if the mid-market price per Brave Bison ordinary share exceeds 3 pence [GN note: c. 40% above the current share price], and if the Group has met certain financial targets at the time of exercise.”

In addition there is “contingent consideration of up to £6.5m over three years subject to performance conditions”. BBSN would potentially have the cash to pay this even if they didn’t generate much operating cash flow over the next three years - more on that in a moment.

Overall, I’m going to give this deal a big thumbs up, as I like the way BBSN has protected itself from the risk that it fails to improve the performance of a negative-EBITDA marketing company.

Trading update: BBSN also published a brief trading update along with the acquisition announcement. It was short and sweet:

Trading in the second half of 2024 has been in-line with expectations and the Board anticipates that Brave Bison will meet current market forecasts for FY24 of approximately £3.6m of Adjusted EBIT.

Following the acquisition, the Company is now expected to report net cash of approximately £7.0m at the end of FY24.

The year-end cash forecast is slightly reduced, from £9m to £7m, but pleasingly that still leaves plenty of cash to pay the contingent consideration for Engage, even if the group doesn’t generate much operational cash.

Graham’s view

I’m glad that BBSN has found a more amenable acquisition target than The Mission Group. This deal sounds to me as if it is strategically sound, and I can’t possibly argue that they have overpaid, given how the purchase has been structured.

I’m happy to leave our AMBER/GREEN stance unchanged. While I do admire BBSN’s financial performance in recent years, I’m not convinced that the shares are a slam-dunk bargain at a current market cap of £27m, given just £3.6m of adj. EBIT (before the acquisition of Engage).

Begbies Traynor (LON:BEG)

Up 5% to 99.1p (£156m) - Half-year Results - Graham - AMBER

I’m impressed with the 16% revenue growth posted by Begbies today for H1 (to £76m). Organic growth is strong at 11%, while acquired growth contributes the remaining 5%.

There have been “increased year on year insolvency activity levels in higher value cases”.

More bluntly, the company says later in the statement that “UK insolvencies remain at elevated levels”.

But the “property advisory” segment is growing even faster than the “business recovery” (i.e. insolvency) segment.

In property advisory, asset sales have seen “strong growth driven by property auction volumes”.

In total, adj. EBITDA rises 20% to £15m. PBT rises 57% to £4.7m.

The company moves into net debt of £4m, as its acquisition strategy does require significant earn-out payments (£4m paid in H1).

Outlook: in line. The range of forecasts for adj. PBT is £23 - 24.3m (thanks to BEG for disclosing this).

H1 adj. PBT was £11.5m, so no growth is required in H2 to achieve the bottom of the forecast range.

Comment by Ric Traynor:

Since 2014 we have tripled the size of the business with a six-fold increase in adjusted profit before tax. Building on this track record, we are making good progress towards our medium-term revenue target of £200m.

Market conditions remain supportive for the group's service lines which is reflected in our current activity levels and positive momentum across the business. This, together with our financial performance in the first six months, leaves the board confident of delivering current market expectations for the full year, which will extend our longstanding track record of strong, profitable growth.

Dividend: the interim dividend increases by 0.1p to 1.4p.

Headcount (measured in full-time equivalents) has crossed 1,100, up from 1,050 a year ago.

Adjustments: in H1 there are £6.8m of “non-underlying items”, which create the large gap between adjusted PBT (£11.5m) and actual PBT (£4.7m).

There are two components involved here: amortisation of intangible assets (£1.9m) and payments for acquisitions that are deemed to be remuneration, as they require the sellers to stay employed within BEG (£4.9m).

We’ve been over this before. I’m fine with taking these adjustments at face value, but with conditions.

Firstly, if we are willing to ignore the amortisation of intangible assets, then we should be willing to write down the value of all of BEG’s intangible assets to zero. If we do that, the BEG’s balance sheet equity is £6m, not £76m!

Secondly, if we are willing to add back in the cost of acquisitions that are deemed to be remuneration, then we need to remain mindful of the fact that BEG’s success depends on the input of certain individuals, i.e. we need to value this as a “people business” with a lower earnings multiple than we’d give to businesses that do not depend on the input of key individuals.

Estimates: many thanks to Equity Development for publishing a detailed note this morning. I have not read it in its entirety yet, but I note that it includes an adj. PBT forecast of £23.3m for FY April 2026, with adj. EPS of 10.4p, and the company having “free cashflow to fund both acquisitions and dividends”.

They see "scope for a significant rerating” to a PER of 14x, with fair value of 145p.

Graham’s view

I’ve been neutral on this one, as I’m a fan of this business and its management, but I view it as correctly priced (see coverage in November at the half-year trading update).

For the reasons explained above, I’m happy to use BEG's adjusted earnings numbers but I wouldn’t want to pay an above-average or even average multiple for them, and I would also want to treat the balance sheet with caution.

Therefore, to me, a PER of about 10x on adjusted numbers makes good sense. That’s roughly where the stock is currently trading (share price 99p vs adj. EPS forecast of 10.4p). So I’m staying neutral on it. Perhaps when I read the Equity Development note later on, I'll be convinced that it's worth a bit more!

NCC (LON:NCC)

Down 18% to 133.8p (£422m) - Preliminary Audited Results - Graham - AMBER/RED

NCC Group plc (LSE: NCC, "NCC Group" or "the Group"), a people-powered, tech-enabled global cyber security and software escrow business, reports its 16 months to 30 September 2024 ("2024", "the 16-month period"), following a change to the Group's financial year end.

I don’t usually cover this one and my initial question relates to the change in the accounting year-end.

It has taken me a little while to find the answer but in January 2024, NCC said:

The Board has changed the year end of the Group from 31 May to 30 September, this is to drive greater efficiency in our corporate reporting and audit process.

I have no idea how a September year-end would drive greater efficiency than May - perhaps it has something to do with summer holidays?

Back in September 2023, I see that KPMG requested additional time to complete the audit for FY May 2023. NCC would go on to change its auditor in 2024.

Perhaps I am focusing too much on this issue, but it’s remarkable to me how often a change in accounting year-end is associated with some hidden or not-so-hidden problem.

Let’s move on and look at these 16-month results to Sep 2024, which are really 4-month results for the period from June to Sep, as unaudited 12-month results were already published.

In the 4-month period, revenue is up 6.6% (at constant currency) to £105.1m.

Adj. EBITDA has quintupled from £1.9m to £9.5m, and the company posts an operating profit of £2.3m (vs. a loss of £7.7m in the corresponding 4-month period).

Unfortunately finance costs eat all of this operating profit, so the bottom line result is around breakeven.

CEO comment:

"We have made great progress over the past 18 months, transforming the business by focusing on client needs while building the Group's resilience. Our more focused Cyber Security business returned to growth in the second half to May 2024, with improved sources of recurring revenue with Managed Services performing well, and our Escode business building a track record of growth. We are pleased to see this strategic progress coming through in improved gross margin and Adjusted EBITDA - a key priority for the Group.

“Escode” (external link) is the “software escrow” side of the business, which is essentially a software depository.

Market economics - this section includes some negative commentary on the state of the industry, although it does say “notwithstanding macroeconomic factors outside of our control, we remain confident in delivering our medium-term financial goals.” The company’s office in Manila “has enabled us to expand our global capability and offer more options to our clients”.

Let’s bullet point the negative factors at play:

Clients looking for higher levels of assurance during their procurement processes.

Higher value, longer term contracts have a longer buying cycle.

Security leaders are competing for budget with other spending priorities in their organisations, and cyber security is not immune from the cost pressures experienced by other departments.

Cooling of buying activity in the UK re: Budget.

North America tech sector spending has not returned to levels seen during or immediately after Covid-19.

It’s a lot of negativity and this feeds through to an uninspiring outlook statement.

The Group has a strong pipeline of opportunities, and management is pleased with the foundations put in place through strategic actions taken in the period. In line with the wider market, the Group has recently seen a lengthening of sales cycles, in particular across the Cyber business, compared to H2 to May 2024 and also the four-month period to September 2024. In spite of this, management expects to deliver profitable growth across both businesses in the current financial year to 30 September 2025, with flat to low single digit revenue growth and modest Group Adjusted EBITDA gains…

Estimates: Zeus have left their forecasts unchanged.

Net debt has reduced by a few million pounds to £45m.

Graham’s view

I’m not seeing a lot to like here, despite the strong growth in adj. EBITDA. The balance sheet has a negative tangible asset value of minus £40m, and retained earnings (more like cumulative losses) of minus £89m.

Combine that with limited revenue growth forecast by management, finance costs devouring the company’s operating profit, and an IT sector (managed services) that I would ordinarily want to put on a low multiple, and it’s creating a picture of a stock that I’d want to steer away from.

I’ll tentatively put this on AMBER/RED for now. I think it’s trading on a current-year PER (using adjusted EPS) of 21x, falling to 16x for next year. This is significantly higher than I’d want to pay for it.

Megan's Section

hVIVO (LON:HVO)

Up 4% to 22p (£150m) - Contract win - Megan - AMBER

There are positives and negatives in this morning’s announcement from hVIVO (LON:HVO).

On the one hand, the company confirms it has signed a new £11.5m contract with a large pharma company (an existing customer) to test its new antiviral medicine in humans. This should provide reassurance to those who were a little disappointed by the company’s £71m order book announced in September.

On the other hand, the trading update confirms that the company is still set to deliver £62m of revenue in the 2024 financial year, which means that the pace of delivery in the first half has not been maintained. In H1 the company ran through its order book at a rate which meant it delivered 57% of its forecast annual revenues. With no additional orders set to deliver revenue in the second half, the company is still set to report just £26.4m of revenue in H2. That is down on the £28m of revenue generated in the second half of 2023.

And herein lies the problem with Hvivo’s business model: it is very reliant on the pace of innovation at large pharmaceutical companies which rely on its testing facilities to evaluate new drugs.

The company has done what it can to counter that. Earlier this year it expanded into a new facility in Canary Wharf, which means it now runs the largest human challenge trial site in the world. This means that the company will be able to test multiple drug candidates at the same time. The new site, which was financed largely by the company’s existing clients, also comes with a larger laboratory space, which could help it expand its pre-clinical trial offering.

Financially, there are also positives and negatives to be found.

The company receives a good chunk of revenue upfront and booked £21.6m of deferred revenue in the first half of the financial year - a lot of that relating to orders that were to be satisfied throughout the duration of the year. But on the other hand, Hvivo has quite high debtor days and on average it takes 145 days to receive payment from its customers for work delivered.

Megan’s view

I like the ‘picks and shovels’ approach to investing in small cap pharma. The risks associated with a company which provides services to the industry are significantly lower, compared to one that is looking for a groundbreaking new treatment.

Hvivo clearly has a strong position in the market it operates in, but its capacity for growth is somewhat limited by where its clients chose to invest.

In the 12 years since its IPO, Hvivo hasn’t really delivered an awful lot for its investors. I’m finding it hard to get excited by the potential upside, except perhaps as a takeover target. AMBER

Roland's Section

Games Workshop (LON:GAW)

Up 2% to 14,165p (£4.7bn) - Amazon agreement - Roland - GREEN

Games Workshop’s long-awaited film and television production deal with Amazon has been finalised:

Games Workshop has granted exclusive rights to Amazon in relation to films and television series set within the Warhammer 40,000 universe, together with an option for Amazon to license equivalent rights in the Warhammer Fantasy universe following the release of any initial Warhammer 40,000 production.

Today’s statement comes exactly on schedule. When the Amazon agreement was originally announced on 18 December 2023, the company said they would work with Amazon for 12 months “to agree creative guidelines”.

No financial details have been included in today’s RNS and management warns that this could remain a slow burner:

Production processes in respect of films and television series may take a number of years.

Outlook: forecasts for the current year (ending 1 June 2025) are unchanged, following November’s upgrade, which Megan covered here.

Roland’s view

At this point, it’s impossible for us to know what potential impact this agreement could have on Games Workshop’s financial results in the future.

If production goes ahead and is successful, I would imagine this could add materially to the company’s existing licensing revenue. Licensing contributed revenue of £31m and operating profit of £27m last year – exceptionally high margin.

However, as far as I can tell there’s no obligation on Amazon to actually produce any Warhammer films or series. Nor are there any timescales or fixed plans yet.

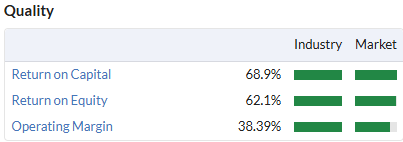

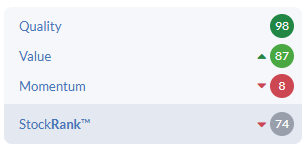

Games Workshop was promoted to the FTSE 100 last week – an incredible result for a niche hobby business. I think this remains a truly excellent company, with outstanding quality metrics:

The company upgraded its guidance for the current financial year in November. Brokers also took the opportunity to upgrade FY26 estimates as well.

The shares don’t look obviously cheap on a forward P/E of 28. But Games Workshop’s StockRank remains high, at 85, with strong momentum.

After reviewing November’s trading update, Megan concluded that this stock continues to deserve a GREEN rating. I’ll leave that unchanged today.

Solid State (LON:SOLI)

Up 6% to 127p (£74m) - Interim Results - Roland - AMBER

“The Group order book at 30 November 2024 of £85.5m provides confidence that current earnings guidance for this year and next is deliverable, with potential to outperform, especially in view of spending on individually large programmes that are currently in abeyance.”

Today’s interim results mark the third update from this electronic components supplier in just over a month. Unfortunately the previous update – on 14 November – was a profit warning that wiped 48% off the share price on the day.

Things appear to be looking up slightly today. The company has left full-year expectations unchanged and suggests that the cyclical outlook for demand may be starting to improve:

There are tentative signs of cyclical improvement in the leading indicators for the industry, and this is reflected in order intake in recent weeks.

Let’s take a look at the main points from Solid State’s results.

Half-year results summary: today’s results cover the six months to 30 September 2024.

Solid State’s revenue fell by 30% to £61.8m during the period, while pre-tax profit dropped 80% to just £1.2m. Even the more favourable measure of adjusted pre-tax profit was 66% lower, at £2.5m.

Encouragingly, gross margin improved marginally to 31.1% (H1 24: 31%) suggesting the company’s pricing power has remained stable. However, the drop in volumes caused negative operational gearing and left the group’s operating margin for the half year at just 3%, compared to 7.9% in H1 last year.

Solid State’s management is keen to highlight that the H1 profit slump was made worse by the early delivery of a large order representing £10m of revenue and £3m of profit. This was expected during the first half of the current year, but actually fell into the second half of last year.

Moving this revenue into H1 would have lessened the scale of today’s profit drop, but H1 profits would still have been lower due to the delay in a big defence order discussed in November’s profit warning (see here).

Bonus share issue/eps calculations: a subscriber has flagged up the potential for confusion relating to Solid State’s bonus share issue on 2 October 2024. This saw the company create four new shares for each existing share. The effect is the same as a five-for-one stock split.

However, the balance sheet date for today’s results was 30 September, which was before the bonus issue. As a result, today’s eps numbers do not reflect the share split. Restated figures will be provided with the FY results. Alternatively, we can just divide by five to get the relevant numbers today:

H1 24 adj earnings per share: -62.6% to 17.5p

H1 24 eps restarted: 3.5p

Dividend cut: Reflecting weaker trading, the interim dividend has been cut by 40.7% to 0.83p per share. Confusingly, this has been adjusted for the bonus issue in the headline numbers.

Trading commentary & order book: Solid State has already flagged up the risk that the UK Defence Review will continue to delay new defence orders.

Defence remains a core market for Solid State, but the company is working to diversify into markets such as industrial computing, communications and medical electronics. Management believes the medical sector in particular has similar attractions to defence, in that there are high barriers to entry, long design cycles and tough certification requirements.

Over time, I imagine this strategy may help to reduce Solid State’s cyclical exposure, which the company highlights in its commentary today:

The global electronics market has continued to normalise, with orderbooks adjusting to reflect shorter lead times and unwinding of overstocking. Political and economic uncertainty has affected some sectors, with certain customers delaying orders in response to shorter lead times combined with slower demand.

To put this in context, Solid State’s order book was £76.6m on 30 Sept 24, down from £99.7m one year earlier – that’s a reduction of 23%.

However, order intake in H2 appears more promising. The company says the orderbook had risen by £8.9m to £85.5m on 30 November.

Outlook: the increased orderbook “gives the Directors confidence in meeting revised full year consensus analyst expectations”. Helpfully these have been included in today’s results:

Brokers Zeus and Cavendish (many thanks) have both left their FY25 forecasts unchanged today, at 5.3p and 5.5p per share respectively (adjusted for the bonus issue).

Both figures imply that H2 eps will be around 45% below the restated figure of 3.5p I’ve calculated above. Clearly, earnings are expected to be sequentially weaker during the remainder of the year, despite the more positive tone to today’s update.

Roland’s view

I suspect Solid State will always be somewhat dependent on large and lumpy contracts. But I don’t see anything in today’s results to suggest the company’s core appeal has changed.

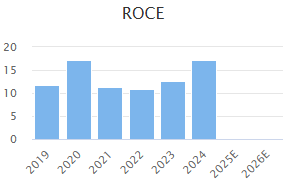

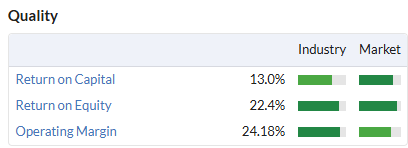

Historically, the business has generated a return on capital employed in the mid-teens. This suggests it benefits from some durable competitive advantages and has been able to invest capital at attractive returns as it’s grown.

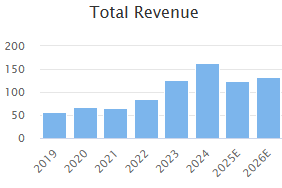

The two charts below show a combination I like to see – rising revenue and stable ROCE, demonstrating growth at attractive profitability:

Profitability will be poor this year and today’s results put the stock on a FY25 forecast P/E of 22. However, with the shares trading close to book value, I think any recovery in profitability to historic levels could support a substantial share price recovery.

The StockRanks view the shares as a potential contrarian play, with high quality and value scores and poor momentum.

I share this view and don’t see any reason why the long-term growth story should not remain intact for this business, which has been listed on AIM since 1996.

On balance, I think Solid State could reward more in-depth research. However, after this brief review, I can’t ignore the uncertain timing of any recovery. I would not rule out the risk of a further cut to expectations.

For these reasons, I’m going to take a neutral view and upgrade our stance slightly to AMBER.

Ashtead (LON:AHT)

Down 12% to 5,522p (£24bn) - Half-year results & US listing - Roland - AMBER

FTSE 100 construction equipment hire group Ashtead issued two RNS statements this morning. Unfortunately one of them included a profit warning (my bold):

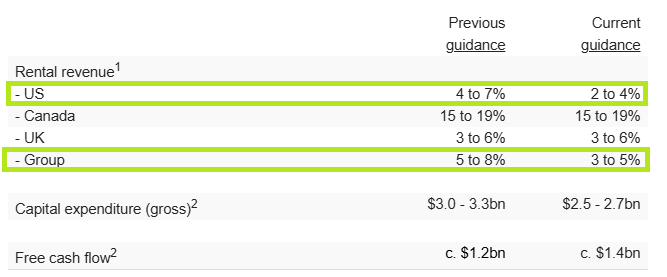

Principally as a result of local commercial construction market dynamics in the US, we now guide to Group rental revenue growth for the full year in the range of 3-5% and hence, full year profit lower than our previous expectations.

Let’s take a closer look at today’s news from this high-flyer, which has been a five-bagger over the last decade:

Megan covered this stock in the Week Ahead and warned that any earnings weakness could cause a correction. Unfortunately, that’s what’s happened.

Ashtead’s Q2 revenue growth of 2% was unchanged from the first quarter, leaving half-year revenue up 2% at $5,695m. However, pre-tax profit for the period fell by 4% to $1,197m, which the company says was mainly due to lower used equipment sales and an increase in depreciation and interest costs.

The company’s own measure of return on investment for the half year fell to 15% (2023: 18%) due to lower utilisation of a larger fleet.

Free cash flow was positive at $420m, benefiting from a reduction in capital expenditure during the period. Net debt excluding leases remained broadly unchanged at c.$8.2bn, representing 1.7x EBITDA. While this is a little higher than I’d choose, I don’t see it as a big problem.

2024 results below expectations: Ashtead CEO Brendan Horgan says that US conditions have diverged. While “mega projects and hurricane response efforts” continue to drive demand, local commercial construction has slowed.

Mr Horgan says this is linked to “the prolonged higher interest rate environment”. Underlying demand is said to remain “strong” and Ashtead expects to see a recovery as interest rates stabilise.

However, as a result of this situation, Ashtead has cut its US revenue growth guidance for this year, resulting in an overall downgrade:

I’m encouraged to see that Ashtead expects to be able to increase free cash generation this year simply by scaling back capex.

The numbers above imply a full-year free cash flow yield of over 4.6% at today’s share price. That’s not a value rating, but it’s not necessarily unreasonable for a faster-growing business, as Ashtead has been (until recently).

Outlook: This business generates more than 90% of its profit in the US, so any drop in revenue in this market has an immediate impact on profit.

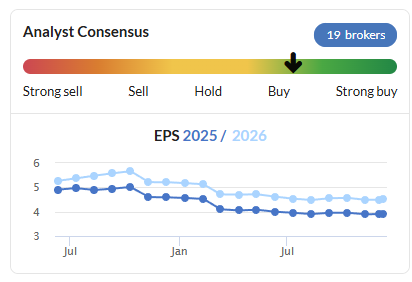

I don’t have access to any updated broker notes today. But prior to today, analysts were expecting Ashtead to deliver broadly flat adjusted earnings this year, before recovering in FY26:

FY24 earnings: $3.86 per share

Stockopedia FY25 consensus: $3.90 per share

Stockopedia FY26 consensus: $4.51 per share

Expectations have already been slipping lower this year:

Today’s 12% share price drop suggests to me that the market may be pricing in a further 5%-10% cut to earnings forecasts.

My sums suggest a revised figure of perhaps $3.60 per share (c.285p). That would place the stock on an unchanged FY25e P/E of 19, after today’s drop.

Move to a US primary listing: Ashtead generates over 90% of its profits in the US and reports in US dollars. It’s no surprise to me that the company has decided to move its primary listing to the US.

Today’s statement indicates that Ashtead will retain a secondary listing in the UK, so shareholders won’t be forced to sell or hold overseas stocks.

The decision will be put to a shareholder vote before being implemented, with completion expected “over the next 12-18 months”.

Roland’s view

Today’s profit warning from Ashtead isn’t a complete surprise, in my view. Other companies, such as Somero Enterprises (disclosure: I hold) have also noted the impact of higher interest rates on local construction projects.

I think Ashtead remains an attractive long-term business, but I also think there’s a risk that interest rates will remain higher for longer than expected. If I’m right, the time needed for property markets to adjust might also be slightly longer than expected.

I generally avoid buying shares directly after an initial profit warning. Stockopedia’s research indicates that stocks often continue to underperform following an initial downgrade.

Ashtead’s shares are not obviously cheap, either, in my view, despite strong quality metrics.

However, this business does have a strong track record and is the second-largest hire operator in the US, with further growth opportunities. I don’t see any reason to take a negative stance at this point, so I’m going neutral with an AMBER view today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.