Good morning!

It looks like we have a large collection of updates that do not include any profit warnings - only "in line" and "ahead of" updates.

It's a rare "good news only" day - let's enjoy it while it lasts!

1pm: wrapping this up for now, cheers.

Spreadsheet accompanying this report (updated to 17/1/2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Cranswick (LON:CWK) (£2.6bn) | Q3 TU | FY25 trading remains in line with market expectations. | |

Abrdn (LON:ABDN) (£2.6bn) | Q4 AUMA & TU | Net inflow of £1.2bn in Q4, AUMA up to £511bn. FY24 adj op profit in line with market exps. | GREEN (Graham) An in line update. Much improved flows. Cheap valuation. |

Qinetiq (LON:QQ.) (£2.4bn) | Q3 TU | FY expectations unchanged. FY revenue exps “high single digit organic” growth at stable margins. | AMBER (Roland) |

Premier Foods (LON:PFD) (£1.6bn) | TU | Q3 sales up 3.1%. FY adj profit at upper end of expectations. | |

4imprint (LON:FOUR) (£1.4bn) | TU | 2024 rev +3% to $1.37bn. PBT “not less than” $153m, above the upper end of forecast range. | |

Alpha International (LON:ALPH) (£944m) | TU | FY24 rev +23% to £135m, total income +18% to £221m. Adj PBT in line with exps. | |

Alphawave IP (LON:AWE) (£935m) | TU | FY24 adj EBITDA to “exceed $50m” with revenue at lower end of guidance ($310m-$330m). | |

Elementis (LON:ELM) (£862m) | TU | Strong Q4. FY adj op profit now expected to be $126-128m, ahead of expectations. | |

Marshalls (LON:MSLH) (£641m) | Full Year TU | Revenue -8% to £619m. Net debt reduced. FY adj PBT to be within range of exps. | |

Kier (LON:KIE) (£627m) | TU | Trading in line with expectations. H2 weighting expected, order book +2% to £11bn at 31 Dec 24. | |

Serica Energy (LON:SQZ) (£599m) | TU | 2024 rev -21% to $726m. Net debt $71m. “Significant” increase in production in 2025. | AMBER/GREEN (Roland - I hold) |

WAG Payment Solutions (LON:WPS) (£586m) | TU | FY24 revenue +13.8% to €256m. Results in line with guidance. | |

Essentra (LON:ESNT) (£351m) | TU | FY24 rev +0.3%. Trading mixed. Adj op profit expected to be in line with current exps. | |

XP Power (LON:XPP) (£313m) | TU | 2024 adj. op profit within the range of exps (£25.1 - 27.6m). 2025 likely to be H2-weighted. | |

Yu (LON:YU.) (£311m) | TU | FY24 rev +40%, EBITDA margin above exps. Confidence in delivering FY25 exps. | AMBER/GREEN (Roland - I hold) |

Marston's (LON:MARS) (£269m) | TU | Adj. PBT “within the range” of exps (£52-53.7m). Cautious outlook for 2025. | |

Gulf Marine Services (LON:GMS) (£159m) | Contract extension | 171-day extension to an existing contract. Backlog now $483m. | |

Epwin (LON:EPWN) (£128m) | TU | “Resilient”. Adj. op profit marginally ahead of exps. Confident outlook for 2025. | |

System1 (LON:SYS1) (£75m) | TU | Full-year revenue “at least in line” with exps, and adj. PBT £5m, “comfortably above” exps. | GREEN (Graham) |

Shoe Zone (LON:SHOE) (£46m) | Final Results | Rev falls to £161m, PBT to £10.1m. Store refits/relocations to complete by end-2026. | |

Argentex (LON:AGFX) (£44m) | TU | Full year revenues £50.3m ahead of market expectation, full year EBITDA margin in line. | AMBER/GREEN (Graham) Excellent revenue performance. Mkt cap not supported by profits yet but balance sheet worth c. £40m. |

Ilika (LON:IKA) (£34m) | Half-year Results | “Significant progress”. H1 revenue £1m, includes grant funding £0.9m. EBITDA loss £1.9m. | |

Gear4music (HOLDINGS) (LON:G4M) (£31m) | TU | FY25 EBITDA in line with consensus markets exps. | |

Mission (LON:TMG) (£29m) | Full Year TU | “Resilient” H2. Full-year revenue +2%. Headline operating profit in line with exps at £9 - 9.2m. | |

Christie (LON:CTG) (£27m) | Full Year TU | Full year adj. op profit £1.4m, ahead of the £1.0m upper range previously indicated |

Graham's Section

System1 (LON:SYS1)

Up 3% to 605p (£77m) - Trading Update - Graham - GREEN

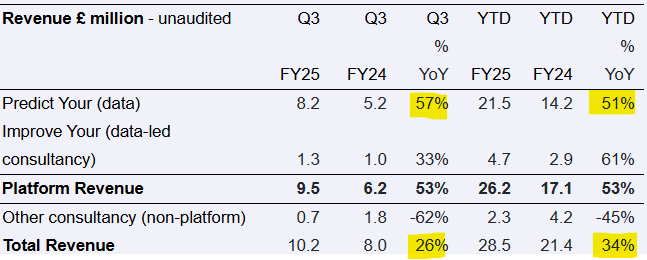

This provider of a “marketing decision-making platform” (helping companies to test their ads) provides an update for Q3 (Oct-Dec).

The main data-oriented products are enjoying a burst of growth as can be seen in the top row of the above table.

I think it’s a little bit more complicated when it comes to interpreting SYS1’s consultancy-based income streams. Yes, their “data-led” consultancy is up, but in my mind it’s just replacing the “other consultancy” income stream that has been abandoned.

So personally I would either focus on the performance of the data-oriented products (top row) or the growth of the total revenue figure (bottom row).

Q3’s strong performance reflected “growth in ad testing together with completion of a large project for a US-based client in December 2024” - we might still need to be careful that particular projects and clients can have a big impact on results in the short-term.

Clients: 120 new clients in Q3 contributed over a quarter of SYS’s “Platform Revenue” during that quarter. Tiktok is named as one of the new clients.

Outlook:

System1 enters the final three months of this financial year on the back of a record third quarter achieved while facing some economic headwinds in Europe and the UK. The Board now believes that the Group is well placed to achieve full-year revenue at least in line with current market expectations and deliver a full-year adjusted profit before taxation of approximately £5m, comfortably above current market expectations (FY24: £3.1m).

Existing market expectations for FY March 2025 are helpfully provided: revenue of £37m and adj. PBT £4.4m. So an additional £600k of adj. PBT is on the cards..

Estimates: Canaccord have updated both their FY March 2025 and FY March 2026 figures in response to this.

For next year (FY March 2026), they are now expecting revenues of £45.1m (prev: £44m), converting to adj. PBT of £5.9m (prev: £5.6m). This upgrade to next year’s profit forecast reverses the downgrade I mentioned in December.

Graham’s view

In December, I left this one fully GREEN despite having some concerns around valuation. On the back of this positive update, I’m happy to leave that stance unchanged.

There is little doubt in my mind that the shares are expensive:

But what we’re getting for this price is a company that’s offering genuine organic growth: hundreds of new blue-chip clients signing up in a very short period of time (230 in the first nine months of the current financial year).

We don’t see this sort of organic growth very often and when we do, I think it’s important to recognise it and celebrate it. While SYS1’s clients already include many of the world’s largest advertisers, I would be surprised if they started to run out of prospective new customers too soon. There’s also the potential for continued revenue growth from existing clients - the net retention rate for Platform Revenue was 120% in H1.

So yes, there is a chance that this stock is overvalued, but I’d like to let this winner run a little longer.

Argentex (LON:AGFX)

Up 10% to 39.8p (£48m) - Trading Update - Graham - AMBER/GREEN

It’s a nice little full-year update from this “global specialist in currency risk management and alternative banking”.

Key points:

Full-year revenues of £50.3m, ahead of market expectations and slightly ahead of 2023..

Full-year EBITDA margin in line with expectation, in the low single digits.

Australia and Dubai regions are now fully operational. These “significantly increase our addressable market”.

Some commentary on how the year panned out:

Whilst the adverse market conditions experienced during 2023 in the core FX business continued into the first quarter of 2024, trading momentum improved subsequently, with the business returning to year on year growth in the second half and revenues in H2 exceeding those generated in H1.

Besides the geographic diversification, there is product diversification into “the broader payments and alternative banking markets”, which according to the company will improve customer retention.

CEO comment excerpt:

It has been a busy year and I am delighted with the progress made. We have invested for growth in 2024 and have made major changes to the business. With a strong team now in place, and a clear roadmap for the future, I am excited about the prospects for 2025 as multiple new profit generating revenue streams commence.

Estimates: thanks to Singers for updating on their client today.

They had previously expected just £43.4m of revenues for 2024, so the new guidance of £50.3m is a very substantial beat.

The previous EBITDA forecast was just £0.7m; this now doubles to £1.5m.

However, they leave their EBITDA forecasts for subsequent years unchanged, “for the moment”. So their 2025 EBITDA forecast remains at £1.7m (on flat revenues) and then in 2026 they continue to expect a step-change to £8.1m of EBITDA.

They acknowledge that this is a “cautious” estimate for 2025..

Graham’s view

There were some interesting comments in a recent thread around the FX space including Wise (LON:WISE) and Revolut.

With smaller players such as AGFX, we may have to look a little harder for their unique selling proposition: why pick Argentex over anyone else who can provide a currency service?

With Argentex I get the impression that there’s a great deal of emphasis on customer service and bespoke solutions, so for me this goes in the category of traditional FX brokers where there is a lot of human-to-human interaction (rather than something like Revolut, where if you need help you have to talk to their AI bot first!)

Paul put this at AMBER/GREEN in July (share price at the time: 29p) on the basis that it seemed to be stabilising under new management, after it had a torrid 2023. He was right and the shares are up by nearly 40% since then.

The interim balance sheet published since then shows net assets (tangible only) worth about £40m.

If I was valuing this purely on earnings I’d move to AMBER, because even if EBITDA does see a step change next year, I would not wish to pay a very high multiple for a traditional FX broker.

However, given the balance sheet strength which supports most of the market cap, I’m happy to leave it at AMBER/GREEN for now.

Hopefully there is plenty of recovery left in this one:

Abrdn (LON:ABDN)

Up 5% to 148.1p (£2.7bn) - Q4 Update - Graham - GREEN

Thanks to Ken Mitchell in the comments for bringing this one up.

I tend to follow the smaller fund managers in detail but why not check in on this giant? Even if I still don’t accept the name change that it went through in 2021.

The company’s new CEO has been forced to defend it again this morning, saying “The name is the name and we will be continuing with it.”

They should just change it back to Aberdeen, shouldn’t they? I wonder how many millions the branding agency was paid for this.

Anyway, let’s check out the contents of today’s Q4 update.

I think these are the key points. Firstly, an improvement in flows against last year:

Q4 positive net flows £1.2 billion (vs. last year: negative net flows £5.7bn).

Full-year negative net flows £1.1 billion (vs. last year: negative net flows much worse at £17.6 billion).

Assets under management and administration (AUMA) are up 3% for the year as a whole (to £210bn) and are also up slightly during Q4.

At Interactive Investor, there was a strong inflow of £5.7bn for the year, with AUMA up 17% to £77.5bn. It looks like it was responsible for most of ABDN’s AUMA growth in 2024.

It now has 81,000 SIPP customers, up 29% in a year.

Group P&L: £100m of annualised cost savings have been achieved, with £150m targeted by the end of 2025.

Operating expenses: in line.

Adjusted operating profit for the year: in line.

CEO comment:

We made significant progress in 2024, exceeding our cost transformation targets and also laying the foundations for the new management team to achieve growth and efficiency as we enter 2025…

Outflows in Adviser are being addressed, with an absolute focus on an improved service and value proposition for our clients.

Graham’s view

I don’t think I can be anything except GREEN on this, given my stance on (nearly) all other fund managers.

The picture of flows presented today is not all that bad, and yet here is the valuation on offer:

It’s more of a multi-faceted picture than the other fund managers I cover, as it includes not just traditional fund management but also Interactive Investor and the “Adviser” business.

Arguably this boosts the appeal, given the state of the fund management industry. Interactive Investor appears to be a high-quality business, and the Adviser segment provides another type of diversification.

It's staggering to think that £1.5bn was paid for Interactive Investor, and now the entire group is valued at £2.7bn.

I’m happy to take a GREEN stance.

But they really do need to change their name back.

Roland's Section

Yu (LON:YU.)

Down 7% to 1,729p (£288m) - Y/E Trading Update - Roland (I hold) - AMBER/GREEN

Business energy supplier Yu Group is a holding in the SIF portfolio and a stock I hold personally. Today’s year-end trading update tells us that growth slowed during the second half of last year, leaving full-year revenue below expectations.

However, profit margins are higher than expected and the company’s broker has upgraded its earnings forecasts today, so I don’t think this update is too disappointing (my emphasis below):

FY24 revenues grew c.40% and are expected to be approaching £650m (FY23: £460m).

Delivery of FY24 EBITDA margin forecasted above expectations driven by strong contract profitability in H2 24, robust hedging policy and tightly managed bad debt.

Net cash position of £80.2m (FY23: £32.1m).

For context, the consensus revenue forecast prior to today was £674m, so today’s guidance is perhaps 4% below expectations.

The increase in the year-end net cash position isn’t as impressive as it seems, either. Yu moved to a new trading facility with Shell last year, which resulted in c.£50m of cash being released from its previous counterparty. Stripping this out, year-end net cash appears to be broadly unchanged from 2023.

Energy supply: headline operational growth in the core energy supply business was strong last year, but today’s numbers reveal a slowdown in H2:

Meter points supplied: FY24 +65% to 88k (H1: +35%, H2: +22%)

Avg monthly new bookings: FY24 £42.6m (H1: £46.9m, H2: £38.3m), partly due to lower energy prices

Volume of energy supplied: FY24 +c.78%

Smart meters: Yu is building a smart meter business that is expected to provide an annuity-like revenue stream over time.

Income from this operation is described as Index-linked annualised recurring revenue (ILARR) - this rose to £1.3m last year from 27.2k meters owned.

Dividend: a progressive dividend policy is being maintained, targeting 3x earnings cover.

Outlook: organic growth in 2025 is expected to reflect “more normalised” energy prices. At the end of 2024, contracted revenue for the year ahead was £566m, an increase of 9% on the end of 2023.

Broker Panmure Liberum has updated its forecasts today, cutting its 2024 revenue estimate to £645m but increasing its 2024 eps estimate by 5% to 198.4p.

The company says it is confident of delivering FY25 expectations and Panmure’s earnings estimates for 2025 are unchanged at 213p per share.

Incidentally, the Panmure note (available on Research Tree) provides lots of detail on the business and is worth a read for anyone interested in Yu.

Roland’s view

While I’m slightly disappointed to see growth (apparently) fall below expectations in H2, I don’t think today’s update is too bad. The business is still adding new meter points at double-digit rates and is doing so with improved profitability.

Revenue is closely linked to energy prices and so may be more volatile than we’re used to seeing with other types of business.

CEO Bobby Kalar owns 51.6% of the stock, so his interests are well aligned with those of other shareholders. This gives me confidence that he will continue to manage the business to provide consistent profitability and cash generation.

Today’s update has left the shares trading on a 2024 forecast P/E of 8.6 with a 3.3% yield. While this isn’t a business I’d buy on a high rating, I think this looks reasonable given YU’s growth prospects and improving profitability. AMBER/GREEN

Serica Energy (LON:SQZ)

Up 3% to 157p (£618m) - Trading and operations update - Roland (I hold) - AMBER/GREEN

I last covered Serica just two weeks ago, when the company warned 2024 production would fall below expectations.

Today’s update covers the full year and the outlook for 2025. The company takes a positive tone, but as I’ll explain shortly, I think today’s guidance may be slightly weaker than originally expected.

The outlook for 2025 is promising, with ongoing work to increase asset reliability and further positive results from the Triton drilling programme expected to boost production and help deliver material free cash flow.

CEO Chris Cox says he expects to “continue delivering material direct returns to our shareholders” in 2025, which seems to suggest Serica’s existing generous dividend may remain sustainable. Based on last year’s 23p per share distribution, the yield is currently over 14%.

Financial summary:

2024 production of 34,600 boepd (2023 pro forma: 40,100 boepd)

2024 revenue of $726m (2023 pro forma: $920m)

Avg Brent oil price $81/bbl (2023: $81/bbl)

Avg NBP gas price of 83p/therm (2023: 99p/therm)

Dividends of $114m (23p/share) and $19m buyback

Free cash outflow of $1m

Net debt of $71m at 31 Dec 24, improved cash generation expected in 2025

Operationally, recent work appears to be paying dividends:

Triton production ramping up after the recent restart and is being boosted by the new Gannet GE05 well. This is producing at 6,000 bopd, “well ahead of expectations”

Additional wells are being drilled and expected to add to production over the coming year

The Triton compressor fix is expected to be completed by the end of March 2025

Outlook:

2025 production is expected to rise by c.15% to around 40,000 boepd, evenly split between oil and gas

Spending will be similar to 2024, improved cash flows are expected to support further shareholder returns

Preparatory work underway regarding a move from AIM to the Main Market in 2025.

Company remains active in screening for M&A opportunities in the North Sea and elsewhere

The company doesn’t mention whether the 2025 outlook is in line with expectations. I think it may actually be slightly below previous forecasts.

In my last review, I speculated that Serica’s ageing assets may require more regular maintenance than some others.

Today the company advised that production will be H1 weighted, largely because of two planned outages this year, including a 45-day outage on the Triton FPSO:

Production weighted to H1, with annual maintenance programmes at the Bruce Hub and Triton FPSO expected to take production offline in Q3 for 12 and 45 days respectively

An updated note from broker Auctus Advisors is available on Research Tree today. Comparing this with the previous Auctus note on 7 Jan shows they have cut their 2025 production estimate from 41.4k to 40.1k boepd to reflect lower expected oil production, presumably because of this new planned outage.

Auctus’s 2025 eps estimate has been cut by 25% from $0.56 to $0.42 since 7 Jan.

This is only one estimate and other brokers covering Serica may take a different view – Stockopedia’s data suggests 4 brokers cover the shares.

Roland’s view

My impression is that earnings (and free cash flow) expectations for 2025 have been trimmed in today’s update.

However, the guidance laid out today still suggests to me that Serica’s current dividend will be comfortably supported by free cash flow in 2025. If so, then the shares could still offer a 14% dividend yield.

There are no free lunches in investing though, and I think it’s sensible to remember the risks here. Serica’s main assets are mature and increasingly appear to be relatively high maintenance.

Regular additional drilling is needed to maintain or expand production. Current broker forecasts suggest production may peak in 2027 before starting to fall quite sharply – hence management’s focus on M&A opportunities.

I remain positive at the current valuation and continue to hold the shares. But I plan to continue to view this business as something of a special situation, requiring regular monitoring and (perhaps) decisive action at some point. AMBER/GREEN.

Qinetiq (LON:QQ.)

Down 11% to 372p (£2.1bn) - Third Quarter Trading Update - Roland - AMBER

Today’s update from defence contractor QinetiQ is headlined as being in line with expectations, and this was my first impression when quickly skimming the RNS feed at 7am.

Closer inspection reveals that it turns out that UK order intake has been “slower than expected”, prompting an 11% share price drop at the time of writing.

Let’s take a look.

QinetiQ has a 31 March year end, so today’s update covers fiscal Q3, the three months to 31 Dec 24.

Trading summary: the company has seen growth in its EMEA Services business (75% of revenue). “Good visibility” is said to be supported by a strong opportunity set from several major programmes.

However, within EMEA Services, the UK Intelligence business has suffered a sufficiently large slowdown to justify some restructuring activity:

Short-term order intake in the UK has been slower than expected due to the fiscal environment and we have taken proactive action to resize some of our capabilities in our UK Intelligence business.

UK Intelligence generated 29% of EMEA Services revenue in H1. So the affected business has previously generated more than 20% of total group revenue.

Fortunately, the far larger UK Defence business (59% of EMEA Services) is said to be unaffected by this slowdown. The company says it has greater exposure to long duration contracts which are unaffected by short-term spending decisions.

QinetiQ’s other operating segment is Global Solutions. Revenue is said to be stable in this business “despite headwinds in the contracting environment in the US”.

Order intake: year-to-date order intake is £1.3bn, slightly below last year’s figure of £1.35bn.

FY & mid-term expectations unchanged: CEO Steve Wadey does not seem to expect the shortfall in UK orders to affect full-year results:

Our expectations for the full year remain unchanged

Outlook: the company expects to report “high single digit organic revenue growth at stable underlying operating margin” this year. This is the same wording that was used in November’s interim results.

I don’t have access to broker notes for QinetiQ, but this comment seems consistent with consensus forecasts on Stockopedia for FY25 revenue growth of 7% and an implied adjusted net profit margin of 8.8% (FY24: 8.9%).

Over the medium term, QinetiQ is maintaining its target of achieving £2.4bn of annual revenue at c.12% margin by 2027.

Assuming forecasts remain unchanged, today’s fall leaves the stock trading on a FY25e P/E of 12, with a 2.3% yield.

Roland’s view

Today’s update stops short of giving us any idea of the scale of the shortfall in orders in UK Intelligence. So it’s hard to estimate the real severity of this issue. It may be minor and temporary, but the company’s decision to “resize some of our capabilities” suggests to me that it could be more severe.

I wonder if we might see a profit warning at some point in the coming months. The double-digit share price drop we’ve seen today (for a £2bn mid cap held by institutions) suggests to me that some brokers covering the stock may have trimmed their FY25 estimates following today’s news.

As always, there’s not a level playing field here. Institutional investors will have received updated broker notes this morning, but we’ll have to wait for updated consensus estimates to filter through.

Despite these concerns, today’s update doesn’t sound like a calamity to me. The current valuation suggests to me that a reasonably cautious outlook may now be priced in.

I’m going to take a neutral view ahead of the company’s usual year-end update in April. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.