Good morning!

Leaving it there for now, thank you. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Legal & General (LON:LGEN) (£15bn | SR30) | Core Operating Profit up 6% to £1,623m, core EPS up 9% to 20.93p. Profit rose in Institutional Retirement and Retail units and was flat in Asset Management. Dividend lifted 2%, new £1.2bn share buyback launched. 2026 outlook: expect core EPS growth to be at top end of 6%-9% 3yr target range. | AMBER ↓ (Roland - I hold) Today’s results have missed consensus expectations, which the company suggests is mainly due to a reappraisal of certain legacy assets whose performance has disappointed. I’d also point to mixed new business performance in some areas, including net outflows from asset management. While I think the 9% dividend yield could represent an attractive entry point for an income investment, I’ve decided to move my view down by one notch to neutral to reflect today’s miss versus expectations and the opacity of this business. | |

Harbour Energy (LON:HBR) (£4.5bn | SR99) | SP -9% to 257p Secondary placing: an entity controlled by EIG Management Company (7.55% shareholder) has sold 60m shares (3.8%) at 255p per share, raising gross proceeds of c.£153m. | AMBER = (Roland) [no section below] EIG was one of the original backers of Harbour Energy in 2014 as a private vehicle for oil and gas investment. Following the merger of North Sea producer Chrysaor with Premier Oil in 2021, EIG had a 36% shareholding in the combined group (renamed Harbour Energy). Since then, EIG’s stake had already fallen to 7.55% through distributions, sales and dilution from subsequent corporate transactions Harbour has undertaken. This latest disposal reduces EIG’s holding to c.3.5% of HBR. It looks like an opportunistic sale to me; EIG is presumably betting that the current disruption to shipping and oil and gas production in the Middle East will not last for too much longer, allowing oil and gas prices to return to more stable levels. Time will tell if this view is correct, but I think the big picture here is simply that EIG is continuing to exit a (presumably) successful investment. After this morning’s drop, Harbour is trading on c.8-9x FY26E earnings with a c.5% dividend yield. This valuation looks about right to me for a large commodity producer with a collection of (mostly) quite mature assets. I was neutral on Harbour in December when it announced the acquisition of LLOG and don’t see any reason to change that view today. | |

Hochschild Mining (LON:HOC) (£3.6bn | SR70) | Revenue up 25%, pre-tax profit up 110% to $373m. Production down 10% to 311,509 gold equiv oz. AISC up 27% to $2,138 per GE oz. Mara Rosa turnaround progressing “in line with expectations”. 2026 outlook: production 300-328k GE oz. | ||

Balfour Beatty (LON:BBY) (£3.4bn | SR69) | Revenue up 8%, driven by UK power transmission and US buildings demand. Underlying profit from operations from earnings-based businesses up 16% to £293m. £200m buyback and dividend +12%. Outlook: continued growth supported by a record £22.7bn order book (+23% YoY). | AMBER/GREEN (Roland) Like Costain yesterday, Balfour Beatty appears to be in a fairly good position at the moment. The construction group has reported both revenue growth and an overall improvement in operating margins for 2025, despite some localised problems in its US business. However, while the overall situation seems positive, the extra complexity and lower profitability of this business makes it a little less attractive for me than Costain. With Balfour Beatty shares already trading on 14x 2026 forecast earnings, I also feel the valuation is up with events. To reflect these concerns, I have opted for an AMBER/GREEN view today. | |

Drax (LON:DRX) (£2.9bn | SR98) | Drax has provisionally secured agreements to provide a total of 434MW of capacity (de-rated 399MW), principally from its pumped storage and hydro assets. For delivery from Oct 2029 - Sept 2030 at a provisional clearing price of £27kW/year, generating income of around £11m. | ||

Canal+ SA (LON:CAN) (£2.9bn | SR83) | 2025 guidance “achieved or exceeded”. Revenue +0.9% organic, adjusted EBIT up 5% to €527m. Tax issues resolved, debt refinanced and MultiChoice acquisition completed. 2026 outlook: expect adj EBIT to rise to €735m, with “at least €250m” of adjusted free cash flow. Medium-term target for “over €500m” of free cash flow. | ||

Hill & Smith (LON:HILS) (£1.78bn | SR88) | Revenue up 2%, adj pre-tax profit up 7% to £142.5m. Adj EPS +8% to 132.2p. “Strong US performance”. Outlook: strong US trading momentum expected to continue in 2026, “remain cautious about the degree of recovery in UK”. Expect increased H2 weighting to profits vs 2025. | ||

Bodycote (LON:BOY) (£1.22bn | SR84) | SP +8% Revenue down 4%, adj op profit down 11.4% to £114.3m. Adj EPS down 8.6% to 44.4p. Oil & Gas and Automotive & Industrial segments were challenging. 2026 outlook: expect underlying revenue growth and improved margins, confident in medium-term targets. New £80 million buyback. | AMBER/GREEN ↑ (Graham) [no section below] This High Flyer probably deserves an upgrade from us. EPS estimates were steadily downgraded throughout last year, but there are signs that this negative trend could potentially be at an end. Today's results are weak compared to 2025, but are nonetheless accompanied by a confident outlook statement and a fairly generous buyback announcement. Net debt has increased to £105m but the leverage multiple is still only 0.6x, which for most mature companies is reasonably conservative. They are essentially ploughing all of 2026's forecast profits into this buyback, while also paying a 3% dividend yield. The quality metrics at this heavy industrial business are average, as you might expect, but it strikes me as being quite a shareholder-friendly business. Without having huge conviction in this call, I'm happy to take a slighly more optimistic stance, consistent with the StockRank of 84. | |

Breedon (LON:BREE) (£1.12bn | SR51) | Revenue up 9%, adj pre-tax profit down 7% to £140.2m. Adj EPS down 8% to 31.8p. Leverage increased to 1.8x EBITDA following Lionmark acquisition. | ||

4imprint (LON:FOUR) (£1.09bn | SR87) | Revenue down 2%, pre-tax profit down 2% to $150.8m. EPS down 3% to 404.4c, in line. New customer orders down 12%, existing customer orders flat. 2026 outlook: YTD trading in line with expectations, “orders and revenue are slightly down compared to the same period in 2025”. | AMBER ↓ (Graham) I'm in two minds about this; I can see plenty of positives but also some clear negatives. On balance, I take us back to a neutral stance on the basis that the stock is still quite highly-rated given how fragile its earnings forecasts have proven to be, and the cautious tone of today's outlook statement (similar to last year). | |

Supermarket Income REIT (LON:SUPR) (£1.04bn | SR90) | EPRA EPS down 10% to 2.7p, reflecting asset transfer into JV. Dividend up 1% to 3.09p per share. Dividend cover 88% (2024: 99%). Annualised passing rent +11% to £132m, portfolio valuation +27% to £2,057m. EPRA NTA per share up 0.5% to 87.5p, LTV 45% (2024: 31%). Outlook: recent acquisitions expected to support sustainable dividend for FY27 onwards with minimum annual uplift of 2%. | AMBER/GREEN = (Roland - I hold) [no section below] Today’s results show a reduction in dividend cover to well below 1x. At first glance this is a potentially serious concern for a REIT. However, in this case I think that management’s explanation that this shortfall reflects the one-off movement of certain assets into a JV is fair. Having deployed the new capital associated with the JV, annualised passing rent of £132m is now significantly more than half the net rental income of £56.6m reported for H1. Today’s results reiterate guidance for a minimum dividend of 6.18p for FY26 (y/e June) and include new guidance for “minimum sustainable dividend uplift” of 2% per annum from FY27. SUPR stock remains at a modest discount to book value, with a forward yield of at least 7% based on today’s guidance. On balance I think this remains an attractive income play at a reasonable price, so I’m happy to retain our previous AMBER/GREEN view. | |

International Personal Finance (LON:IPF) (£546m | SR87) | Shareholder Janus Henderson (4.08% holding) is not able to vote in favour of the deal at today’s General Meeting with respect to shares representing 3.49% of IPF’s share count, as these shares are currently on loan. | PINK (Graham) [no section below] According to an RNS published after 3pm, the takeover (technically a "Scheme of Arrangement") has been approved. It was a fairly resounding victory, with close to 95% of votes in favour. And so the story of IPF as a listed company comes to an end. | |

ITM Power (LON:ITM) (£395m | SR21) | Confirm 20MW Notice to Proceed reported in February relates to MorGen Energy’s West Wales Hydrogen project, which has now reached Final Investment Decision. ITM has signed a 10yr service agreement with MorGen for the West Wales project. | ||

Forterra (LON:FORT) (£350m | SR71) | Revenue +12.1%, EBITDA +18.5% (£61.6m). Outperformance vs. wider market. 2025 ended with subdued market conditions which have continued into early 2026, with exceptionally wet weather making it difficult to assess the strength of the underlying market. FORT currently anticipates demand in 2026 will be similar to 2025, although with current activity tracking behind 2025 levels, demand is expected to be weighted towards the second half. We currently expect our 2026 adjusted EBITDA to be slightly ahead of 2025. | BLACK? (AMBER/GREEN =) Graham) [no section below] I think 2026 was supposed to be better than a “slight” improvement over 2025. However, the share price for this brick manufacturer is unchanged today, so the market seems reasonably content with the news? I note that the share price already fell 30p in the last two weeks, so it's possible that any perceived weakness in the outlook may have already been priced in. The EPS forecasts on the StockReport are as follows: 12.1p for 2025, and 13.5p for 2026. The actual EPS result for 2025 in today's results is 12.6p, so that's at least some positive context to go with the warning that 2026 will be H2-weighted. Roland was AMBEER/GREEN on this last year at a slightly higher market cap. I'll leave that unchanged today. EPS forecasts have been very stable over the thast year, so it appears that little has changed. | |

Nichols (LON:NICL) (£333m | SR63) | SP +6% Revenue +1.3%, adjusted operating profit +9.9% (£31.7m), operating profit +27.1% (£27.3m). Trading so far during 2026 has been positive and in line with expectations. Reducing dividend cover to 1.5x due to “strong balance sheet, confidence in the outlook and good cash generation”. | GREEN ↑ (Graham) [no section below] I've been very stubbornly leaving this soft drinks company on my annual watchlist year-in, year-out, waiting for the share price to reflect my positive view of the stock. I note today that the share price is up by 6% despite the trading update only being "in line". I typically interpret this sort of price action to mean that the market became too pessimistic, expecting bad news, but that the bad news did not materialise. Not only is there no bad news in today's results, with profit margins picking up (something I've been patiently waiting to happen), but the company is also reducing dividend cover from 2x to 1.5x for 2026. This means paying out thirds of earnings in the form of dividends, rather than merely half. Meanwhile the adjusted PBT margin has improved from 18% to 19%. Exceptional items are down, too (from £7.4m to £4.4m), so the results are cleaner. I'm a bit of a broken record on this one, but I think it deserves more appreciation by the market. The QualityRank is 98 although it scores less well for Value and Momentum.. | |

GYM (LON:GYM) (£312m | SR64) | Revenue +8%, adjusted EBITDA +13% (£98.9m). Adjusted PBT +194% (£10.6m). Non-property net debt £59m. Trading momentum remained strong in our peak recruitment months of January and February; revenue after two months has grown by 9% year on year; like-for-like revenue up 3%. Group Adjusted EBITDA Less Normalised Rent for FY26 expected to be at the top end of the analysts' forecast range. | ||

B.P. Marsh & Partners (LON:BPM) (£236m | SR86) | B.P. Marsh invested in Sodalis in November 2025. On 10 March 2026 Sodalis announced the launch of Brecon, a new London-based wholesale insurance broker. Brecon has been created to provide specialist broking and risk advisory services to international independent brokers, as well as direct clients, with a focus on Cyber and Technology Errors & Omissions (E&O) risks globally. | ||

SRT Marine Systems (LON:SRT) (£225m | SR43) | The Philippine Courts have formally and fully cleared and dismissed as false and baseless all allegations, claims and media reports of conspiracy, graft and bidding irregularities made against Simon Tucker (CEO), SRT Marine Systems and other named persons. | ||

Mercia Asset Management (LON:MERC) (£119m | SR45) | The three Northern Venture Capital Trusts, which form part of Mercia's third-party funds under Management, have successfully completed their expanded fund raise totalling £80.0million of new capital, through share offers launched in September 2025. | ||

Berkeley Energia (LON:BKY) (£116m | SR17) | Cash reserves of $68,408,000. Cash outflows during the period totalling $3,709,000. Net assets $76,056,000. Berkeley continued to advance its ongoing exploration initiative targeting critical minerals at its Conchas Project. Salamanca project: ready and open to collaborate with the relevant Spanish authorities to find an amicable resolution to the permitting situation, remains hopeful discussions can take place in the near term. | ||

Speedy Hire (LON:SDY) (£106m | SR56) | The CFO succession process is concluding more quickly than anticipated. New CFO appointment begins 1st July 2026. Most recently she was CFO of Ricardo plc. | ||

Amcomri (LON:AMCO) (£80 million | SR47) | FY25 revenues up 22%, adjusted EBITDA +17% (>£9m), significantly ahead of market expectations. Two acquisitions during the year. FY26 has started well across both the Embedded Engineering and B2B Manufacturing divisions and the Group is trading in line with expectations. | ||

Robert Walters (LON:RWA) (£75m | SR73) | Revenue -14% (cc). Operating loss £14.9m (2024: profit £5.2m). 2026 will see further meaningful reduction in the cost base. “Trading over the first two months of 2026 has been in line with the Board's expectations, albeit in a seasonally lighter part of the year.” | ||

ECO Animal Health (LON:EAH) (£65m | SR93) | The United States Department of Agriculture (USDA) has delivered a favourable safety assessment of ECOVAXXIN® MG, the Company's live poultry vaccine targeting Mycoplasma gallisepticum. | ||

Batm Advanced Communications (LON:BVC) (£51m | SR65) | Comparable revenue +9% ($123.2m). Adj. operating profit $14.7m (2024: $3.8m). Sold four businesses during the year and a fifth post year end. Entered the new financial year with increasing momentum; confident of delivering strong underlying growth for 2026 and significant, sustainable growth in the medium-term. | ||

Ariana Resources (LON:AAU) (£50m | SR29) | Further positive assay results from its 2025-2026 RC drill programme at the Dokwe Gold Project in Zimbabwe. “These results confirm that the Dokwe North mineralised system continues beyond the limits of the current resource model towards the north-east.” | ||

Zenith Energy (LON:ZEN) (£24m | SR48) | Application for annulment of the ICC-2 Arbitration. The Republic of Tunisia failed to submit its response to the Annulment Application within the required procedural timeframe set out by the Swiss Court and has instead sent a submission to the Swiss Court contesting its jurisdiction. The Republic of Tunisia says that the application should be adjudicated by a Court of Appeal seated within the Republic of Tunisia. | ||

Cambridge Cognition Holdings (LON:COG) (£19m | SR16) | Monument Therapeutics Limited, in which COG has a 20% shareholding, has announced the dosing of the first patient in its clinical trial with MT1988, to treat patients at clinical high risk for psychosis. | ||

Vulcan Two (LON:VUL) (£15m | SR20) | Five-year license agreement with a leading provider for the implementation of a central enterprise resource planning system. This follows the conditional raising of £40m to acquire three companies in the ePharmacy sector. Annual subscription fee £80-100k, plus consultancy fees £765k. | ||

Light Science Technologies Holdings (LON:LST) (£10m | SR29) | Buying 100% of RLUK Injection Ltd and remaining 10% minority interest in UK Circuits and Electronics Solutions for £5.37m. Placing and retail offer to raise up to £6.6m at 1p per share. Last night’s close: 2.9p. Trading update: operating loss £0.6m, cash position £0.7m. | (Graham) This is a deeply discounted placing that is partly designed to strengthen the balance sheet, in addition to making these acquisitions possible. |

Graham's Section

4imprint (LON:FOUR)

Down 9.5% to £34.98 (£984m) - Final Results - Graham - AMBER ↓

4imprint Group plc (the "Group"), a direct marketer of promotional products, today announces its final results for the 52 weeks ended 27 December 2025.

A fairly weak outlook statement for 2026 has soured the mood here.

Before getting into that, the 2025 results show everything down by 2%:

It was a “resilient performance amidst a volatile macroeconomic environment”.

The number of orders declined 3%, while the average order value increased 1% - resulting in an overall 2% revenue decline.

Gross margin is flat at 32%. The company previously thought it would achieve something closer to 33%.

Roland observed these trends at the January trading update.

At that update, 2025 PBT guidance was raised from >$142m to >$149m. We see today that the actual result was $150.8m.

Stockopedia’s EPS forecast trends show that the market did get overly pessimistic about the 2025 result. However, there has not yet been any recovery in the 2026 forecast, which remains gloomy (the light blue line below):

Cash is down year-on-year but remains solid at $133m.

The Outlook from the Chairman is worth pasting in full:

Trading results in the first two months of 2026 have been in line with the Board's expectations. Orders and revenue are slightly down compared to the same period in 2025, reflecting continued uncertainty in the market. As anticipated, tariff-related costs are being phased in by suppliers and tariff policy continues to evolve. Whilst these factors may influence revenue and margins in 2026, the business will continue to be managed to deliver solid financial results in the near term, and best position us to take advantage of opportunities that will present themselves as economic and market conditions improve.

Despite a challenging environment, our view of the prospects of the business is unchanged. The Board is confident in the Group's strategy, competitive position, and long-term growth opportunity.

If you made it through all of that, I think that the message is pretty clear: the business is going to be under pressure in 2026.

Estimates: Edison have published on this today (many thanks to them for that). They say they have “made no material changes to our FY26 forecasts”.

Cross-checking against their prior note, I observe the following changes for FY26::

Revenue of $1,322m has been reduced by only $1m.

Operating profit of $116m is up by $1m.

Adjusted EPS of 324.6c is lower by only 2 cents.

So they are totally correct: the changes to FY26 are indeed minimal.

Of greater significance are their new FY27 forecasts:

Revenue of $1,341m

Operating profit of $123m

Adjusted EPS of 341.6c

It’s worth mentioning that, as a mid-cap, many brokers cover this stock in addition to Edison.

And when I check these new Edison forecasts against what is currently in the market, these new forecasts are really not that bad - revenue is a little lower, but operating profit and EPS are a little higher.

I’m therefore not going to interpret today’s release as a profit warning, despite the share price falling 10% and the weak-sounding outlook statement from the company.

Graham’s view

My best interpretation of today’s fall in the FOUR share price is that it’s primarily a consequence of the uncertainty in this statement: “tariff-related costs are being phased in by suppliers and tariff policy continues to evolve. Whilst these factors may influence revenue and margins in 2026, the business will continue to be managed to deliver solid financial results in the near term.”

This simply doesn’t inspire confidence - even if broker estimates are unchanged.

The stock hasn’t recovered yet from the weakness in early 2025:

It’s interesting if we go back to last year’s full-year results announcement, in March 2025.

That was just before Trump’s official introduction of tariffs. The stock slid sharply after those full-year results, and then continued to fall before eventually reaching a bottom after “Liberation Day”.

This is the outlook statement a year ago:

In the first two months of 2025 revenue at the order intake level was slightly down compared to the same period in 2024, reflecting continued uncertainty in the market. It is possible that market conditions, including potential tariff impacts, may continue to influence demand in 2025. From our experience, however, as business sentiment improves, demand for promotional products increases as does our ability to gain market share.

Despite a challenging near-term environment, our view of the prospects of the business remains unchanged. The Board is confident in the Group's strategy, competitive position and growth opportunity.

If we change a few of the numbers, this could have just as easily been written in 2026.

So actually, a vague and cautious outlook statement has become normal for 4imprint.

And considering how EPS forecasts have evolved, they have been right to be cautious.

Roland was AMBER/GREEN on this in January, at a market cap of £1.2 billion.

I’m in two minds about this. Some positives:

Strong cash position.

Excellent quality metrics. QualityRank 93.

Very limited downgrades to forecasts today.

Passes some of my favourite bullish stock screens (Greenblatt’s Magic Formula, Ben Graham Deep Value).

But there are also some clear negatives:

Limited growth even if it hits forecasts.

A weak start to 2025 requires improvement later in the year to hit those forecasts.

Consensus EPS forecasts have been unstable.

Tariff-related uncertainty (not just policy itself, but policy effects over time as price rises feed through the system).

What is the long-term competitive advantage? I get that its commercials have raised 4imprint’s brand awareness, but why will customers still be choosing 4imprint in five or ten years? I’m not sure.

On balance, this is more of an AMBER for me. If I had to explain this downgrade in one sentence, I would say simply that the stock is too expensive given the fragility of its earnings forecasts:

Legal & General (LON:LGEN)

Down 5.6% at 242p (£13.8bn) - Full Year Results 2025 - Roland - AMBER ↓

(At the time of publication, Roland had a long position in LGEN)

Investors have taken a dim view of today’s results from Legal & General, after the UK’s largest investor (with over £1trn under management) missed consensus estimates on a number of key measures.

Core (adjusted) profits were slightly lower than expected, as was the group’s Solvency II coverage ratio, a regulatory measure of the group’s capital buffer.

One reason for the drop in the coverage ratio was that the company has cut its valuation estimates for a number of assets – something newish CEO António Simões is describing as addressing “legacy complexities”.

While the miss wasn’t large, it’s perhaps unexpected for such a large and well-followed business. The market has wiped more than £800m from the group’s market cap this morning:

As several of you have already commented, Legal & General is an extremely complex business that relies on a vast balance sheet and a slither of equity. This capital-light business model is not without risk and relies heavily on accurate long-term projections and modelling, skilled use of reinsurance and the maximisation of opportunities presented by regulations (and regulatory changes).

I guess the real fear behind today’s market reaction might be that downward valuations to asset values become a recurring problem, rather than a neatly-contained legacy issue.

2025 results summary

I am not an expert in life insurance or pensions, so I tend to confine my analysis of Legal & General to considering a few key numbers and understanding the general direction of travel of the group’s three main divisions.

While I’d usually aim for a higher level of understanding of a business that forms 5% of my main personal portfolio, in this case I choose to rely on the company’s scale, reputation and 190-year heritage to underwrite the quality of my investment.

Let’s see whether today’s results alter my comfort level with this approach.

Headline profit figures look broadly positive, but as mentioned above these figures are below company-compiled consensus estimates of £1,649m and 21.17p, respectively:

Core Operating profit up 6% to £1,623m

Core Operating Earnings Per Share up 9% to 20.93p

Dividend up 2% to 21.79p per share

New £1.2bn buyback (including £1bn relating to Meiji Yasuada transaction)

Personally, I place more emphasis on the group’s surplus cash generation, which underpins support for the £1.2bn dividend and any buybacks.

This surplus generation is governed by regulatory Solvency II rules. Legal & General reports a number of key measures:

Operational Surplus Generation up 5% to £1,530m (+8% to 26.78p per share due to buybacks)

Net Surplus Generation up 5% to £1,264m (operational surplus less capital required to support new business)

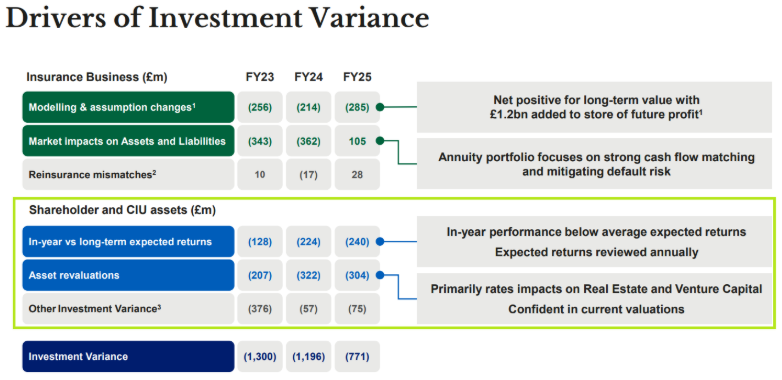

Solvency II Surplus down 23% to £6,913m

Pro Forma Solvency II Coverage Ratio: 210% (2024: 232%)

The City was expecting a Solvency II coverage ratio of 219%, so it seems that Legal & General has drained its surplus to a greater extent than expected over the last year.

A number of factors contributed to this and it does appear to be part of Simões’ strategy to reduce the coverage ratio to 160%-190%. However, it seems the main reason for last year’s fall was lower in-year returns and subsequent revaluations of some property and other assets:

Source: LGEN FY25 presentation

What strikes me is that the level of asset revaluations last year was very similar to that seen in each of the previous two years. This may reflect changing interest rates and other factors over the last few years, but I can’t help wondering if it’s a trend.

Divisional results: I’ll look at each of these very briefly.

Institutional Retirement (operating profit up 6% to £1,168m): this business is a market leader in pension risk transfer (PRT). In 2025, the unit wrote £11.8bn of new PRT business (2024: £10.3bn). International volumes were lower, however, at £1.4bn (2024: £1.9bn). Management notes “the pricing environment has been challenging”, presumably reflecting much-increased competition in this market.

Asset Management (operating profit flat at £402m): total assets under management rose by 5% to £1,197bn, reflecting market movements – the business saw overall net outflows of £28bn during the year. Costs edged higher, accounting for 75% of income (2024: 74%). The average fee margin rose to 9.1 basis points (0.091%), up from 8.8bps in 2024. This does rather highlight the large volume of low-margin products under management – presumably index trackers and similar.

Retail (operating profit up 4% to £447m): profits rose due to “higher CSM release and investment margin” – in effect, annuities written in the past have been more profitable than originally expected. However, margins on new business tightened, falling to 5.9% (2024: 7.5%). Flows into Workplace DC pension schemes rose by 3% to £6.2bn during the year, but retail annuity sales fell by 14% to £1.8bn. Management continues to expect both the Workplace DC and retail annuity markets to double in size by 2034.

Outlook

Management reports a “healthy pipeline” of new PRT opportunities, with £17bn of transactions actively being priced on. An “increase in large transactions” is expected relative to 2025.

In asset management, the company expects revenue growth to outpace cost growth as the business sees the full benefit of new business written last year. The shift to higher-margin products is expected to continue.

Further growth is expected in retail, also.

Overall, the business is said to be on track to meet all of its medium-term targets.

Broker consensus prior to today suggested an increase in earnings to 24.3p per share in 2026. That puts Legal & General on a forward P/E of 10, with a potential 9% dividend yield.

Roland’s view

On the face of it, a P/E of 10 and 9% yield may represent a very attractive entry point to this share. If guidance for 2% annual dividend growth is maintained, the stock could offer a theoretical expected return of 11% annually (dividend yield + growth). That’s not bad for what remains a high quality, blue chip business.

I hold the shares for income and am unlikely to sell following today’s results.

That said, I have to admit my comfort level with my holding is slightly lower than it was prior to today’s figures.

The problem is that I don’t have any way of truly understanding whether this year’s miss is genuinely a one-off caused by legacy assets, or if there’s an underlying trend.

In my view, it’s not too hard to imagine that some of Legal & General’s investments in illiquid assets such as property and renewable energy are turning out to be less profitable than originally projected in different market conditions. We’ve seen this when looking at investment trusts specialising in assets in these kinds of markets.

While Legal & General does have deep collective experience of long-term modelling, the last decade has seen some unusual changes.

To reflect the black box nature of this business for outside investors, limited divisional growth and the market’s disappointment at today’s miss, I am going to move down one notch to take a neutral view – consistent with the StockRank.

Balfour Beatty (LON:BBY)

Up 6% at 743p (£3.6m) - 2025 Full Year Results - Roland - AMBER/GREEN

Like Costain yesterday, Balfour Beatty appears to be in a fairly good position at the moment. Its share price has risen by more than 70% over the last year:

Today, this FTSE 250 construction group has reported both revenue growth and an overall improvement in operating margins, to 2.9% for “earnings-based businesses” (2024: 2.7%):

Revenue up 8% due to “UK power transmission and US buildings demand”

Underlying profit from earnings-based businesses up 16% to £293m

Underlying earnings per share up 9% to 47.6p

Dividend up 12% to 14.0p

Order book up 23% to £22.7bn

Average monthly net cash up 58% to £1,212m

One uncomfortable exception to last year’s good news was the group’s US Construction business, where margins fell from 1.1% to 0.6%. This drop was caused by cost overruns on a highway project in Texas, which offset improved profitability in the US Buildings business. Management says cost recoveries are being pursued, but this is exactly the kind of issue that periodically causes trouble for large construction groups.

Fortunately, Balfour Beatty’s broad business and UK scale were enough to dilute the impact of this issue, supporting an overall increase in profit last year.

As with Costain, net cash also improved last year leaving the group with average monthly net cash of £1,212m (2024: £766m).

Outlook

A 23% increase in the order book to £22.7bn gives confidence in the outlook for 2026 – assuming no further cost overruns afflict the business.

On balance, I don’t think this is quite as attractive as Costain. Margins are lower, as are returns on capital employed, at just 11% for 2025 (Costain: 16%).

The complexity of having US and UK businesses and an actively-managed £1.1bn investment portfolio is also less attractive to me than Costain’s tighter focus on UK infrastructure.

While I can see some good qualities here, I think there’s also a little more risk. With Balfour Beatty already trading on 14x 2026 forecast earnings, I am going to opt for an AMBER/GREEN view today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.