Good morning!

It's unusually quiet for updates this Wednesday

1pm: all done for now, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Barratt Redrow (LON:BTRW) (£6.3bn) | Interim Results | Completions up 10.9% to 6,846, adj PBT up 6.4%. FY adj PBT to be at upper end of exps. | AMBER (Roland) |

Pan African Resources (LON:PAF) (£763m) | Interim Results | H1 -3.3% to 84,705oz, profit +10% to $44.6m. FY guidance for c.215koz (+16% YoY) unchanged. | AMBER (Roland) |

Close Brothers (LON:CBG) (£549m) | Update in relation to motor commissions | Close plans £165m provision in H1 FY25 results. CET1 falls to 12.0%. H1 adj op profit exp c.£75m. | GREEN (Graham) I think the risks are priced in here given CBG's enormous tangible NAV and very high capital ratios. This view does require the provision announced today to have at least some degree of accuracy. |

Cohort (LON:CHRT) (£503m) | Contract win | MASS subsidiary awarded 2-year UK JCAST contract worth “in excess of £17.5m”. | AMBER/GREEN (Roland) [no section below] Today’s contract doesn’t look likely to move forecasts, but is further evidence of Cohort’s strong momentum. If this continues, the shares may not be too expensive at this level. |

Iqe (LON:IQE) (£168m) | Convertible Loan Note Financing | Seeks to issue Convertible Note to raise £18m. Note to be convertible at 15p (latest SP 17.3p). | RED (Graham) Desperate terms with a very high implied interest rate and a generous conversion option. Possible dilution of up to 16%. |

Aoti (LON:AOTI) (£122m) | TU | Rev +32% to $58m. Adj. EBITDA margin rises to 13.8% (prev: 3.9%). Higher margin segments. | |

MTI Wireless Edge (LON:MWE) (£42m) | Significant contract win | Repeat manufacturing order for Antenna division. Value $4m, delivered until June 2026. | AMBER/GREEN (Roland) |

Goldplat (LON:GDP) (£13m) | Q2 operating results | H1 adj. op profit £2.5m, PBT £834k. Ghana: “outside mob” disrupted the gold export manager. |

Graham's Section

Close Brothers (LON:CBG)

Up 6% to 388p (£585m) - Update in relation to motor commissions - Graham - GREEN

Close Brothers Group plc ("the group" or "Close Brothers") today issues an update in relation to motor commissions and the group's financial performance in the six months to 31 January 2025.

After discussing S&U in yesterday’s report, it’s topical that we hear the latest view from Close Brothers.

It’s big news: CBG are putting a number on the estimated provision required for its legal and regulatory vulnerabilities.

The number is £165m.

Financial Strength

To put the provision in context, CBG’s last balance sheet (July 2024) had net assets of £1.8bn, of which c. £1.6bn was tangible.

Since that balance sheet was measured, the company has agreed to sell its asset management business (CBAM) for up to £200m. Based on the figures published for that deal, I think that it should boost tangible NAV by c. £130m.

Dividends are not being paid until the current uncertainty has been resolved, another factor that is helping to boost tangible NAV.

Of course a large capital base is a regulatory requirement, but CBG is carrying well in excess of its requirement: its CET1 ratio (Common Equity Tier 1 ratio) was 12.8% as of July 2024, vs. a regulatory requirement of 9.7%. This ratio is the main safety measure for banks.

CET1 has improved further to 13.5% as of Dec 2024.

The £165m provision will knock it back to 12%.

But then the impending sale of CBAM will take it back up to 13%.

That’s a very strong ratio considering that it is after taking what they believe is a reasonable provision for the legal/regulatory risks they face.

In summary, the company says they are “well placed to absorb the impact of the estimated provision”. Although they acknowledge that the ultimate cost could be “materially higher or lower” than this estimate. £165m is just their first guess, based on a range of possible outcomes that have been weighted according to their probability.

Trading Update

H1 saw a “robust performance”.

In Banking, the adj. operating profit is c. £104m.

Market-maker Winterflood will see a small operating loss.

Overall adj. operating profit for the group, after central expenses, is c. £75m.

Graham’s view

Most recently, I’ve been AMBER/GREEN on this one.

I was GREEN until the Court of Appeal’s ruling on motor finance commissions in October.

I must say that I’m tempted to go back to GREEN on this today. The Supreme Court might find reasons to take a "common-sense" approach, as we discussed yesterday.

As for the issue of potential redress in relation to discretionary commissions, there is still a large element of uncertainty, although hopefully it's reducing in size.

However, this is arguably priced in with a sub-£600m market cap, vs. tangible NAV that could be around £1.7bn.

I'm going to stick my neck out and call this GREEN, with a warning that there is still a great deal of regulatory risk. I think that the risks are likely to be priced in here, with an attractive risk:reward, but that's just my flawed opinion on the subject, based on my current understanding. If the £165m provision turns out to be grossly inaccurate, and too low, or if other regulatory risks materialise, then I can see that CBG shares might not be a bargain here.

Iqe (LON:IQE)

Down 2% to 16.9p (£164m) - Convertible Loan Note Financing - Graham - RED

I’ve been negative on IQE for a long time but must concede that the share price is up by 60% since I looked at it in November.

However, today’s update re: financing does not fill me with any confidence that the fundamentals have improved.

Today we learn that the company has come to an agreement around a convertible loan note with its existing investors, led by Lombard Odier (they own 15% of the company).

The details

IQE will receive £18m for these loan notes.

The loan notes have a face value of £21.2m and an initial term of 12 months. They do not pay interest, but if they are repaid in cash for £21.2m then the return will be nearly 18%.

IQE can extend the term by 6 months at a cost of 9%.

Importantly, the notes are subordinated to the company’s existing bank lender, HSBC.

On maturity (or whenever IQE seeks to repay the notes), the noteholders can instead convert to IQE shares at a conversion price of 15p. Last night’s close was 17.4p, so I would say that 15p is a generous price at which to offer conversion.

So in summary, IQE are borrowing at 18% from their existing investors, and also offering a discounted conversion price to these investors.

A conversion option is supposed to reduce the interest rate on a loan. So to borrow at 18% with a conversion option attached strikes me as a very desperate move.

What happens next

Shareholders have to approve the transaction at a general meeting.

They are given the following warning (emphasis added):

The directors of IQE independent of the Proposed Transaction, believe that successful completion of the Proposed Transaction is required to maintain sufficient short-term liquidity whilst the Company completes the ongoing strategic review.

So without this transaction or some other equivalent funding, I think it’s reasonable to assume that IQE will enter a state of financial distress.

Certain Directors are not considered independent. These include the Exec Chairman, who is taking part in the transaction, and the Lombard Odier representative.

Speaking of which, IQE has agreed to give Lombard Odier another slot on the Board, in recognition of their role in this transaction (assuming it goes ahead).

Graham’s view

These are terrible lending terms, and they provide further evidence for me that IQE is in a desperate situation.

As usual, I find myself disagreeing with what I’m reading from this company:

…the Company is undertaking a Strategic Review which the directors believe will unlock significant unrealised value within the IQE group. The Proposed Transaction is integral to the Strategic Review and the Company's ability to demonstrate financial resilience to both our customers and potential parties to the Strategic Review.

I’m afraid I don’t see how borrowing at 18% (plus a conversion option) does anything to demonstrate financial resilience.

To me, it only demonstrates that the company has again failed to generate enough cash to fund itself, and has had to turn to its existing investors to help it keep the lights on while it figures out what to do next.

Hopefully they will find a buyer for their Taiwan operations. But in the meantime, this proposed transaction threatens to create up to another 150 million IQE shares, with dilution of almost 16% for existing shareholders.

I’m staying RED on this.

Roland's Section

Barratt Redrow (LON:BTRW)

Up 5.1% to 459p (£6.7bn) - Interim Results - Roland - AMBER

Full year adjusted profit before tax [ … ] is now expected to be at the upper end of market expectations.

FTSE 100 housebuilder Barratt Redrow bulked up last year with the acquisition of its smaller rival Redrow. Today’s results cover the six months to 29 December 2024 and reveal a slowdown in trading.

However, the company has seen an improvement in reservation rates and now expects full-year adjusted per-tax profit to be at the upper end of market expectations. Helpfully, the company has provided the information we need to evaluate this guidance:

Bloomberg consensus for FY25 adjusted profit before tax on 11 February 2025 was £542m with a range of £506m to £588m, excluding the impact of purchase price adjustments.

Let’s take a closer look.

Half-year results summary: these accounts are significantly more complicated than usual due to the accounting adjustments required to reflect the completion of the Redrow deal on 21 August 2024.

The main figures that seem useful for comparison and align with consensus forecasts are:

Home completions fell by 12% to 6,846 (HY24 pro forma: 7,777)

Adjusted pre-tax profit (pre PPA) fell by 12.6% to £217.5m

H1 adjusted earnings per share (pre PPA) of 12.0p

Interim dividend: 5.5p per share (HY24: 4.4p)

Net cash: £459m (HY24: £753m)

Tangible net asset value per share down 2.9% to 438p (HY24: 451p)

PPA (purchase price allocation) adjustments totalled c.£50m in H1. They are being made to simulate what Barratt’s results would have been if Redrow’s assets and liabilities were held at their historic carrying values, rather than the fair value required by IFRS 3 business combination accounting rules. I think it’s safe to ignore this as it’s a one-off factor that will gradually unwind and does not affect cash generation.

Operating metrics: after a difficult period, sales performance appears to be improving.

H1 net private weekly reservation rate up 33% to 0.60 (Barratt/Redrow comp: 0.45)

2025 YTD reservation rate unchanged at 0.60

The improved sales rate has not yet translated into a larger order book, but the proportion of private sale homes is increasing again, resulting in higher average selling prices:

Forward sales at 3 Feb 25 were 10,903 homes (4 Feb 24: 11,460)

Order book value at 3 Feb 25 £3,350.3m (4 Feb 24: £3,135.2m)

Order book ASP Feb 25: £307,282 (Feb 24: £273,578)

FY25 guidance & strategic update: full-year performance will depend on the important spring selling season. But Barratt Redrow now expects to complete between 16,800 and 17,200 homes in FY25, implying a significant step up in completions from H1 (6,846).

Given the updated profit guidance this morning, I guess consensus earnings estimates may edge up slightly, but I don’t expect a big upgrade.

Prior to today, analysts were expecting adjusted earnings of 27.5p per share, supporting a 15.9p dividend.

Dividend & Buybacks: one other update that may be of interest to investors is a change in the company’s capital allocation policy.

Target dividend cover is going to be increased from 1.75x to 2.0x, with additional surplus cash directed into share buybacks.

The company is targeting buybacks of £100m each year and today has announced a £50m buyback for the second half of FY25.

I am not a fan of redirecting dividends into buybacks. But it’s certainly the fashion at the moment and might generate a reasonable return on investment at current levels, based on adjusted profit estimates.

Roland’s view

There are a lot of moving parts in today’s results. Far more than usual for a housebuilder, due to the integration of Redrow. This is expected to generate £100m of cost savings over time, through measures such as the closure of regional offices.

However, administrative cost savings in FY25 are only expected to total £10m, while the costs associated with the acquisition and integration now total £49.9m. My view remains that this deal is unobjectionable, but is unlikely to result in a significant increase in profitability for the combined group.

Reassuringly, there are no new remediation provisions in today’s results. However, Barratt had £798.1m of existing fire safety provisions at the end of 2024, plus £87.1m of provisions relating to reinforced concrete frames. That’s £885m in total. As with Bellway yesterday, I wonder if these provisions are likely to remain a drag on free cash flow for some years yet.

Are Barratt Redrow shares attractively priced? The Redrow acquisition was an all-share deal that increased Barratt’s share count by nearly 50% to 1.45bn.

Today’s results show net tangible assets per share of 438p at the end of December 2024, 3% lower than the 452p reported at the end of June 2024 (before Redrow was included).

A broadly flat result seems to suggest that the acquisition of Redrow was probably fairly priced, as I’d expect given the element of founder ownership at Redrow.

However, today’s share price gains have lifted the BTRW share price to 463p at the time of writing, slightly above tangible book value.

Barratt Redrow says its targeting an operating margin of 15% and return on capital employed of c.20% over the medium term. This is based on a target of c.22,000 completions per year.

If this can be achieved sustainably, then I think a premium to book value may be justified.

However, we’re not there yet. Today’s half-year results show ROCE of 8.1% and my sums suggest underlying free cash flow (before working capital movements) of just £51m. This is much closer to the company’s reported net profit of £75m than it is to any of the adjusted numbers.

Consensus forecasts seem to suggest free cash flow will normalise at around £300m in FY26. That’s equivalent to a free cash flow yield of under 5% at current levels.

On balance I can see the potential for further progress. But I think there are more compelling choices elsewhere in this sector and will maintain our view at AMBER.

MTI Wireless Edge (LON:MWE)

Up 8% to 52.5p (£45m) - Significant Contract Win - Roland - AMBER/GREEN

Israeli group MTI Wireless Edge specialises in antennas and related radio communications systems. It operates in the defence, remote irrigation and telecoms sectors.

MTI has announced a number of contract wins over the last year or so, in addition to its quarterly trading updates. Today we have news of a $4m deal repeat order for military antennas:

[The] Antenna division has received a significant repeat order from a system house in Israel for the manufacture of military antennas worth a total of approximately US$4m, which are expected to be delivered up until 30 June 2026.

CEO Moni Borovitz says the order is an example of the company’s market-leading technology:

The order entails the supply of state-of-the-art antennas and is integral to an end use which is considered to be one of the most advanced systems of its kind in the world. The antennas are designed to deliver unmatched accuracy and robust communication, leveraging our sophisticated and complex production technology.

Estimates: house broker Shore Capital has issued an updated note today but has left its forecasts for FY25 and FY26 unchanged ahead of MTI’s full-year results in March.

The broker notes that “if further significant orders are secured then there is upside potential in FY25F and FY26F, in due course.”

Shore’s current forecasts suggest earnings of 4.7 cents per share for 2025, rising to 4.9 cents in 2026. That prices the stock on around 13 times forecast earnings:

Roland’s view

MTI Wireless has been a superb multibagger for long-term investors, five-bagging over the last 10 years:

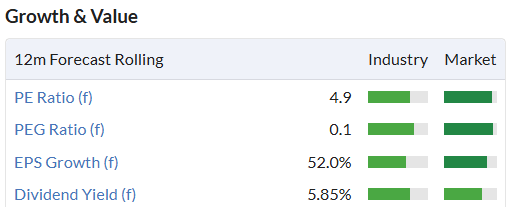

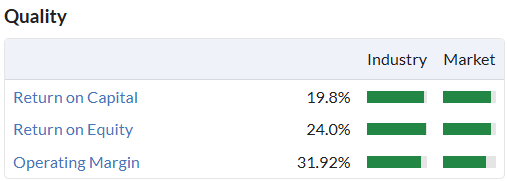

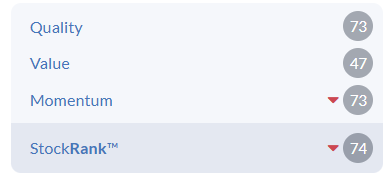

The company pays reliable, cash-backed dividends and has above-average quality metrics:

However, investors must offset this against the additional uncertainty and risk that comes with investing in a small, AIM-listed overseas firm. While there are some UK institutions on the shareholder register, MTI is effectively controlled by its two largest shareholders, who own 42% of the stock.

The StockRanks have a favourable view of MTI and this stock is also a member of Ed’s 2025 NAPS portfolio.

I’m going to go AMBER/GREEN today, ahead of a more detailed update on the business when the 2024 results are published in March.

Pan African Resources (LON:PAF)

Down 1.6% to 37p (£752m) - Interim Results - Roland - AMBER

This South African gold miner has released half-year results today, covering the six months to 31 December 2024.

The headline figures seem somewhat mixed to me, with rising profits driven as much by the higher gold price as by any underlying growth:

H1 gold production down 13% to 84,705oz vs H1 24 (-3.3% sequentially from H2 24)

H1 All-in Sustaining Costs (AISC) up 29% to $1,675/oz, due to a variety of issues

Revenue down 1% to $189.3m

Pre-tax profit down 2% to $56.1m

Earnings per share up 10.3% to 2.35 cents per share, due to lower tax

Dividend of 1.2 cents per share ($23.7m) paid in December

As a result of construction projects and an acquisition, net debt rose to $228.5m (H1 24: $64.3m).

Outlook & Guidance: The company is maintaining its guidance for full-year gold production of 215,000oz. That would be a 16% increase from FY24, but relies on a 54% increase in production in H2 versus H1.

I assume this outlook is supported by the completion of a hoisting shaft project at the Evander mine and the commencement of production from the MTR mine, which is now said to be “fully ramped up ahead of schedule”.

FY26 guidance has also been provided. Pan African expects to achieve gold production of between 270k and 308k ounces next year, suggesting further significant growth from FY25.

Hedging impact: one point worth noting is that Pan African has not been fully benefiting from higher gold prices. A hedging agreement locked the company into a lower price of $2,359/oz during this half-year reporting period, resulting in an “opportunity cost of $17.4m”.

The final settlement under this hedging contract will be in February 2025, after which Pan African will have unhedged exposure to the gold price. Assuming the price stays at current levels, this should have a favourable impact on profits.

Management expects the resulting cash flow to allow the group to repay all of its debt over the next 12-18 months, potentially opening the door for more generous shareholder returns.

Roland’s view

Pan African Resources has been a remarkable performer over the last couple of years, rising by 150%:

Of course, the company’s performance has been aided by the rising gold price, which is up by 57% over the same period to nearly $2,900/oz.

I think it’s interesting to compare the PAF share price with the price of a listed physical gold trust over the last 20 years.

This illustrates the way that commodity producers can be a leveraged play on the underlying commodity price. PAF shareholders have suffered huge volatility relative to more modest movements in the price of gold:

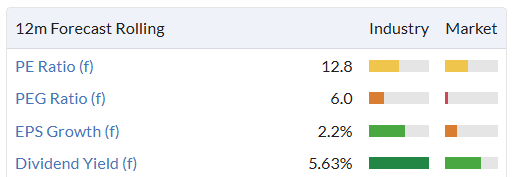

Despite recent gains, Pan African Resources currently trades on seemingly attractive valuation metrics, relative to earnings and the dividend:

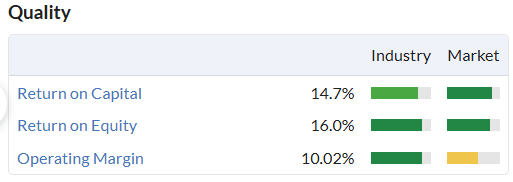

Quality metrics are impressive, too:

Do the shares still offer value? It all depends on what happens to the gold price. Pan African doesn’t appear to be a particularly low cost producer, with AISC for the full year seemingly likely to exceed $1,500/oz.

However, with gold at $2,800/oz it’s clear the company should be able to throw off plenty of cash.

Personally, I think it’s also worth considering the complexity and age profile of some of the company’s deep mines – and their location (mostly) in South Africa. This market carries a mix of operational, political and currency risks. The past 15 years have seen plenty of examples of how this can impact UK-listed precious metal miners.

Pan African’s StockRank has fallen steadily over the last year (highlighted on chart above) and Stockopedia’s algorithms now take a fairly neutral view of this business:

Personally, I think the easy money is probably already in the price here.

I would take the view that Pan African’s low price-to-earnings ratio reflects cyclically strong earnings and the company/location risks I’ve outlined above, including higher debt levels. I’m going to stay neutral for now. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.