Good morning! It's a busy day for updates.

All done for today, cheers!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

HSBC Holdings (LON:HSBA) (£222bn | SR86) | SP +5.5% Adjusted profit before tax decreased by $2.4bn to $29.9bn, due to more negative “notable items”. Excluding notable items, constant currency PBT increased by $2.4bn to $36.6bn. Outlook: targeting a RoTE of 17% or better for 2026, 2027 and 2028, excluding notable items. | [Graham] Previous ROTE target was “mid-teens or better” for 2025, 2026, 2027, so new guidance is an upgrade on that. | |

GSK (LON:GSK) (£90bn | SR91) | Acquisition includes HS235, “a potentially best-in-class activin signalling inhibitor in clinical development for treatment of cardiopulmonary diseases”. Price is $950 million, payable in cash. | ||

Diageo (LON:DGE) (£42bn | SR65) | Net sales down 4% (organic net sales down 2.8%). Operating profit down 1.2% (adjusted operating profit down 2.8%). Increased commitment to reduce leverage. Outlook: organic net sales down 2-3% given further weakness in the US. Organic operating profit growth to be flat to up low-single-digit. Dividend cut based on a 30-50% payout policy. | BLACK (AMBER/RED =) (Roland) CEO Dave Lewis has started his tenure by cutting full-year sales and profit guidance to reflect weak trading in North America and China. Lewis’s take is that consumer spending rather than weight-loss drugs is the main reason for US headwinds, but he acknowledges that there are some changes to consumption patterns. Lewis’s initial priorities appear to be focused on improving operational and commercial execution to ensure products are competitively positioned and do not suffer from any availability issues (Guinness). Beyond this, he says the group’s operating framework needs to be improved to deliver clarity, agility and efficiency – qualities that I assume may be missing from the current setup. I’ve left our moderately negative view unchanged to reflect today’s profit warning, which follows a previous cut to guidance in November. But I’d hope to be able to move back to neutral later this year if trading stabilises in line with today’s revised guidance. | |

HALEON (LON:HLN) (£36bn | SR70) | Revenue down 1.8%, organic revenue +3%. Adjusted operating profit +10.5% (£2.5bn). Leverage multiple 2.6x. Outlook: organic revenue growth 3-5%. High single digit adjusted operating profit growth at constant currency. | ||

Valterra Platinum (LON:VALT) (£19bn | SR65) | Revenue +7%, adjusted EBITDA +68% to ZAR 33.4 billion. "In 2025, we delivered on all our strategic priorities… We move into 2026 with momentum…” 2026 M&C and refined production guidance of 3.0 - 3.4 million PGM ounces remains unchanged. | ||

St Jamess Place (LON:STJ) (£6.6bn | SR61) | “Underlying cash result” up 3% year-on-year to £462m. FUM +16% to £220 billion. Profit after tax £531m (2024: £398m). An increased 70% payout ratio for ordinary shareholder returns for FY26 and beyond. | ||

Hiscox (LON:HSX) (£4.8bn | SR52) | Written premium $4,979m (2024: $4,704m). PBT $733m (2024: $685m). “...Firmly on track to deliver our strategic initiatives and the guidance set out at our Capital Markets Day in May 2025…” | ||

Lion Finance (LON:BGEO) (£4.5bn | SR81) | 4Q25 and FY25 Preliminary Results & GEL 53.5m extension to the share buyback programme | Profit before one-off items of GEL 2,192.8 million for the full year of 2025 (+20.9% y-o-y). Key targets for the medium term remain c. 15% annual growth of loan book, 20%+ return on average equity, 30-50% payout ratio. | |

| Shaftesbury Capital (LON:SHC) (£2.9bn | SR64) | Final Results | EPRA NTA +7.2% to 214.7p per share, total accounting return of 9.1%. Dividend +14.3% to 4.0p. Portfolio valuation +6.6% LFL to £5.4bn, with 6.2% increase in ERV to £270m. LTV reduced to 16.8% (FY24: 27.4%). | |

Morgan Sindall (LON:MGNS) (£2.6bn | SR86) | Adjusted PBT +35% to £233m. Outlook: “we remain positive for the year ahead and are on track to deliver an outcome for 2026 which is in line with revised expectations as set out in our Trading Update released on 12 February 2026". | AMBER/GREEN ↓ (Roland) These 2025 numbers are excellent, but more detailed disclosure of the order book suggests growth in the higher margin Fit Out division may be flattening out. Consensus forecasts also suggest earnings could edge lower over the next 12-24 months. While I continue to admire the quality and consistent execution of this well-managed business, I think it’s fair to moderate my view slightly today to reflect the lack of any new catalysts to support further upgrades. This situation may change as the year unfolds, but I think the valuation is probably at a fair level already based on current information. | |

Jet2 (LON:JET2) (£2.5bn | SR72) | Currently expect to report Operating profit in line with current market expectations (£439m). Broker downgrade for FY27: Operating profit estimate at Canaccord cut by 5%, EPS estimate cut by 4%. | BLACK (GREEN =) (Graham) Despite my view that today's news is technically a profit warning, I think I can stay GREEN on this with reasonable justification. The company is likely to need to keep prices low in order to improve its load factor while also growing capacity. But the cut to the FY27 profit forecast is mild and FY28 forecasts have not been cut at all. And even more importantly than that, the shares are trading at less than 7x forecast earnings. In my view, companies at this sort of rating are not expected or required to hit their forecasts perfectly. | |

Hammerson (LON:HMSO) (£1.86bn | SR65) | Total net rental income +23%, portfolio value +33%. Like-for-like net rental income +3%. EPRA net tangible assets per share +6% to 394p. Profit £232m including net revaluation gain of £120m. FY26 outlook: total net rental income growth of c.20%; EPRA earnings growth of c.15%, EPRA EPS growth c.10% | ||

Trainline (LON:TRN) (£790m | SR74) | The CEO intends to step down after more than six years with the company. He is thanked. Formal search process for his successor commences. The Company reconfirms its previously-upgraded market guidance for FY2026. | ||

Aston Martin Lagonda Global Holdings (LON:AML)(£576m | SR48) | SP -2% Revenue -21% to £1,258m, wholesale volumes -10% to 5,448 units. Pre-tax loss up 26% to £363.9m, Net debt up 19% to £1,380m. Expects “material improvement in financial performance” for FY26. | RED = (Graham) [no section below] The increase in net debt to £1.38 billion (from £1.16 billion) is the standout feature of these results to me. As noted by Roland, net debt is now higher than annual revenues. Furthermore, the company is heavily loss-making (£189m) even at the adjusted EBIT level. Even with a "material improvement" expected next year, it's not clear to me how the equity here continues to command a market cap of over £500m, given the lack of profitability for so many years. It only really makes sense to me if someone like Mercedes-Benz (who are on the shareholder register) might eventually pay a large premium for the marque, taking over both the debt and equity to do so. The leverage multiple is now nearly 13x which is far beyond anything that might be considered reasonable, and the company's credit rating was downgraded by Fitch in November to CCC+. Referring to the largest shareholder, Fitch said that "Yew Tree Consortium support remains key to funding additional cash shortfalls". My view is that I would vigorously avoid investing in these shares. | |

ME International (LON:MEGP) (£554m | SR78) | Auditor needs more time to complete FY25 audit. Company is “naturally displeased” but not aware of any material audit issues. Reconfirms FY25 guidance from 7 Nov: revenue £311-318m, pre-tax profit of £76-79m. Expects shares to be suspended from 2 March until audit is concluded, which is expected to be no later than 13 March 26. FY26 YTD trading in line with exps. | AMBER ↓ (Roland) I think it’s disappointing that a FTSE 250 company is struggling to meet the FCA’s regulatory requirement to report its annual results within four months of the year end. In my view, it shouldn’t have come down to the wire like this. I speculate that the disruption caused by a failed sale attempt, November’s profit warning and the partial transfer of leadership to a Deputy CEO might have contributed to this situation. While I remain a fan of this high quality and cash-generative business, I’m going to adopt a neutral view until the results are published. | |

International Personal Finance (LON:IPF) (£516m | SR95) | 2025 Final Results and Accounts & Final* Recommended Cash Acquisition | SP +7% | PINK (Graham) [no section below] |

Amaroq (LON:AMRQ) (£514m | SR24) | 2026 Production and Financial Guidance and Exploration Update | FY26 gold production from Nalunaq to be 25-35k oz, depending on startup timings. Production expected to be H2 weighted with H1 production of 7-10k oz. Targeting FY26 cash costs of $44-47m. | |

Foresight Environmental Infrastructure (LON:FGEN) (£421m | SR50) | NAV stable at 104.7p per share, quarterly dividend of 1.99p in line with FY26 target. On track to deliver dividend cover of 1.2-1.3x. Gearing stable at 30.9%. | ||

Capital (LON:CAPD) (£320m | SR90) | Awarded waste stripping contract at Sukari, 5yr grade control drilling contract with Montage Gold (Cote d’Ivoire) and 5yr MSALABS contract with Equinox Gold in Newfoundland. Will update guidance w/ FY results on 19 March. | ||

Victorian Plumbing (LON:VIC) (£277m | SR86) | AGM Trading Update, Acquisition & Results Notice & CEO Succession | Positive momentum continued into Q2. Revenue for first 21 weeks of FY26 +9% driven by order volume growth and stable margins. Confident of delivering FY26 revenue and adj PBT in line with expectations. Recently acquired transport business for £3.4m to bring haulage in house. Founder/CEO Mark Radcliffe will become NED from 31 March. Group MD will be promoted to CEO. | |

AdvancedAdvT (LON:ADVT) (£206m | SR33) | Strong performance in H2. Revenue to be c.£53m, adj EBITDA “not less than £14.4m” - ahead of exps (previous consensus £52.5m and £13.7m). Recurring revenue 80% of total revenue. | ||

Avingtrans (LON:AVG) (£188m | SR75) | H1 revenue flat at £78.1m, adj EBITDA +10.4% to £9.6m, in line with exps. Adj PBT +27.1% to £5.7m. Strong performance by Hayward Tyler driven by increased global energy demand due to data centre growth and electrification of transport. | ||

AFC Energy (LON:AFC) (£149m | SR18) | SP -3% Revenue £125k (FY24: £4m), pre-tax loss increased to £25.5m (FY24: LBT £19.3m). Warns company will need a significant increase in revenue or additional funding to be able to trade beyond the second half of 2027. Recently launched new LC30 30kW fuel cell generator, seeing “inbound commercial interest”. | RED = (Graham) [no section below] Heavy cash burn and limited revenues have been the main features of this one. FY25 highlights show the company raising £27.5m of new equity and finishing the year with a cash balance of only £25.3m. As Mark noted at the last trading update, this signals heavy burn during the year (they started it with £15.4m). The cash balance has further reduced to £20.4m as of January 2026, i.e. a £5m burn in three months. The commentary says there has been a "strategic reset" with a "significant focus on commercial viability", but I can't get past the numbers. There is no going concern warning for the short-term (until February 2027). Beyond that, however, "the business will require a sizable increase in revenue... or additional funding through debt or a further fundraise in order to be able to continue to trade in the medium term (second half of calendar year 2027)." | |

| Augmentum Fintech (LON:AUGM) (£146m | SR64) | Recommended cash offer for Augmentum Fintech plc | SP +24% Recommended cash acquisition at 110p. 27% premium to yesterday’s close. £185.7m valuation. | PINK (Graham) The stock market's unwillingness to put a reasonable valuation on this fund is leading to its likely departure. I don't personally understand why it has traded at a 45% discount to NAV, or why shareholders might agree to a takeover at a 31% discount to last-published NAV. There is clearly very little appetite for this type of investment and/or low trust in the calculations which lead to NAV figures for portfolios of investments in private businesses. |

Tracsis (LON:TRCS) (£95m | SR59) | Trading in line with FY expectations. H1 revenue to be c.£39m (H1 25: £36.3m) with adj EBITDA c.£5.0m (H1 25: £3.9m). Net cash £25.8m. New multi-year Train Dispatch contract win with a freight railroad in North America. | AMBER = (Roland) [no section below] Growth in the North American business is encouraging, but this region only generated 5.6% of revenue last year, so growth is from a low base. What’s more important is the outlook for the group’s UK rail operations – which account for the majority of group revenue. Today’s update warns that UK conditions remain unchanged with “hardware volumes continuing to run below historic levels” and “protracted” procurement timelines. While the Government’s 2025 Railways Bill is expected to support long-term growth, there’s no visibility on timelines. I would argue that Tracsis remains exposed to regulatory and political influences that are hard to predict. Financially, year-end net cash accounted for over 25% of the market cap and the forward P/E of 12 looks undemanding. But profitability has fallen to low levels in recent years and today’s update is only in line with guidance. For these reasons, I am going to maintain my previous neutral view today. | |

Strategic Minerals (LON:SML) (£91m | SR33) | Redmoor: positive drill results from underexplored western portion of SVS. Multiple higher-grade intervals identified. | ||

Fairview International (LON:FIL) (£40m | SR8) | Revenue +7% to £3.0m due to higher fees and ancillary income. Gross profit +13% to £1.59m. Student numbers +2% to 723. | ||

Predator Oil & Gas Holdings (LON:PRD) (£26m | SR11) | SC-3 pre-drill report conclusions: targeting unrisked P50 prospective resources of 8.73 MM bbl with net back of US$32.6/bbl at WTI $60/bbl. Would generate $2.044m operating profit. Progress continues at Bonasse and Goudron. | ||

Star Energy (LON:STAR) (£18m | SR89) | 2025 net production 1,886 boe/d, below expectations. Made £2m cost savings and reduced geothermal expenditure. Net debt of £4.3m excl. restricted cash. 2026: targeting c.2,000 boe/d. |

Graham's Section

Augmentum Fintech (LON:AUGM)

Up 25% to 109p (£181.5m) - Recommended cash offer for Augmentum Fintech plc - Graham - PINK

This is “Europe’s leading listed fintech fund”.

We generally don’t cover it in the DSMR/SCVR, as it’s a fund, but today’s dramatic announcement is worth a mention.

There is a recommended offer from funds managed by Verdane Fund Manager AB.

The buyer: Verdane is a “leading European mid-market growth equity investor”, having offices in Oslo, London, Copenhagen, etc.

The offer price: 110p (implied valuation £185.7m). It’s a 27% premium which is around the minimum level where I have found that shareholders are often agreeable to a takeover.

Rationale:

Verdane and BidCo believe that Augmentum will be better able to achieve its growth and valuation aspirations with better access to capital under BidCo's ownership. Verdane and BidCo believe that under private ownership there will be greater flexibility to execute and accelerate the investment strategy with a supportive owner which can help unlock the potential of the Portfolio.

It’s pretty common for companies going private to make statements like this which imply that stock market ownership isn’t conducive to getting the support they need to grow properly. And there may be a grain of truth to this - we tend to be a rather impatient bunch!

If we ignore the underlying value in the fund, the price chart for Augmentum says that it hasn’t been particularly successful. No dividends have been paid and the shares have been trading below their 2018 issue price of 100p:

Irrevocable undertakings/letters of intent: shareholders representing about 9% of the company have said that they support the takeover. Normally I’d want to see a larger number than this to ensure that a takeover gets over the line, but it’s always difficult to judge. I note that the share price today is only 1p below the offer price. Maybe there’s an outside chance of an increased offer?

Timetable: expected to go through in the second quarter of 2026.

Augmentum Chairman comment:

Since our IPO in 2018, Augmentum has been at the heart of the UK and European fintech sectors, backing high-growth companies such as Tide, Zopa, Iwoca, Cushon and Interactive Investor. However, we recognise that for our shareholders, this portfolio's potential has not been reflected in Augmentum's market valuation.

Over several years, we have faced a persistent and widening discount to Net Asset Value, compounded by low levels of liquidity. This has made it difficult for shareholders to realise the true value of their holdings or for Augmentum to raise the capital necessary to support our ambitions.

To address this, the Augmentum Board has run a process to consider a range of strategic options. We are now recommending the Verdane offer, the best we received.

Graham’s view

I note that as of September 2025, Augmentum’s NAV per share was said to be 159.5p. The discount to NAV was a remarkable 45%.

The portfolio was heavily concentrated, which must count against it, although a 45% discount is really punishing:

Tide (24% of net assets)

Zopa Bank (14%)

Iwoca (7%)

BullionVault (6%)

Volt (6%)

Personally, I would be unable to accept selling an investment fund at a big discount to NAV, unless there were really serious problems/uncertainties with the NAV calculations.

The 110p offer from Verdane is at a 31% discount to the September 2025 NAV.

Unless the values of some top holdings have collapsed since September, I can't see why I would agree to this if I was an Augmentum shareholder.

The most recent major story relating to Tide, Augmentum's largest holding, is a fundraising in September 2025 that raised its value to $1.5 billion.

Even if that was a very rich price that massively overvalued Tide, I still wouldn’t be in a rush to sell Augmentum at a 31% discount to NAV. Tide itself was still only 24% of NAV.

Personally, therefore, I can’t understand the logic of agreeing to a takeover at 110p. As someone who hasn’t followed the story closely, I may have missed something. But the only explanation I can see is that stock market investors have had enough of waiting for Augmentum's share price to increase - which I guess would serve to justify Augmentum’s statement that private ownership might be more supportive.

Or in other words:

The prolonged duration and substantial size of the discount, which the Augmentum Directors believe indicates insufficient demand for Augmentum Shares, has made it clear to the Augmentum Directors that continuing with business as usual is unlikely to reduce the discount or deliver the returns to Augmentum Shareholders that they wish to see within a reasonable timeframe. Put simply, the Augmentum Directors believe that an Investment Company structure such as Augmentum's is unfortunately no longer a competitive owner for the Portfolio, and that other pools of capital may be willing to put a significantly higher valuation on the Portfolio.

Jet2 (LON:JET2)

Down 2% to £12.61 (£2.5 billion) - Trading Update - Graham - BLACK (GREEN =)

Jet2, the UK's leading provider of package holidays and third largest airline, provides the following update on trading.

Thank you to a perceptive reader who noticed that this appears to be a “hidden” profit warning.

FY March 2026 is in line, but what should be much more important at this stage is FY March 2027, which starts in one month.

One of Jet2’s joint brokers Canaccord has cut the FY 2027 operating profit forecast by 5%. I’m not sure at this stage what the company’s other brokers have been saying.

But before getting into the reasons for that, here is what’s in the RNS.

Key points:

New Gatwick base to start flying in late March.

Winter seat capacity +7.4% year-on-year

Average pricing has followed a similar trend to summer 2025.

Result: “we currently expect to report Operating profit in line with current market expectations” (£439m), which includes a £10m spend on Gatwick start up cost.

FY March 2027: the company provides helpful detail on operations, but they shy away from providing a profit forecast.

Seat capacity for Summer 2026 is up 8% year-on-year, rising faster than the UK market (growth of only 5.5%).

There are hints that profits might be a little lighter than expected:

To ensure more holidaymakers can experience Jet2's outstanding end-to-end customer service, we are investing in load factor and remain committed to pricing that is attractive and represents real value to our Customers. These actions will ensure that Jet2 has the right foundations to thrive in an increasingly competitive market. Our booked to date passengers are up by 7.9% which includes positive growth at our established bases and over 0.26m passengers at London Gatwick, with healthy demand for both our leisure travel products.

“Investing in load factor” is corporate-speak for keeping prices low to ensure that planes are reasonably full.

Fuel: 75% of FY27 fuel needs have been hedged, which sounds sensible.

CEO comment doesn’t add too much:

We are very pleased with how the 2026 financial year is concluding, and are excited about the commencement of operations at London Gatwick. For Summer 2026, we are satisfied with our bookings to date and remain committed to pricing that is attractive and represents real value to our Customers.

Estimates

Many thanks to Canaccord for publishing and making their note available on Research Tree today.

Among many other things, they make interesting comments on FY27. In particular:

The company is planning market share growth in FY27 (which makes sense if capacity is growing faster than the wider market).

They want their load factor back around 90% (it has been 88% recently).

The combination of higher capacity and a higher load factor will require something like 11% passenger growth, implying some price effect.

It’s great news for consumers, but it’s likely to mean slightly softer profits than previously anticipated.

The 2027 adj. PBT forecast gets cut by 4% to £455.8m. The adjusted EPS forecast gets a similar cut to 187.7p.

Reassuringly, the FY March 2028 forecasts are not cut and are even increased slightly.

Graham’s view

While I’m calling this a BLACK (a profit warning), it strikes me as a mild one.

Firstly, while it is in a sense “hidden”, there are some clues in the RNS to let readers know that profits might be under some pressure in FY27. It’s very far from the transparency that I’d like to see, but it’s also not the worst I’ve seen.

Secondly, the company’s joint broker has raised FY28 forecasts, suggesting that the strategy in FY27 is expected to have positive effects in future years.

Thirdly, the extent of the cut to FY26 profit forecast is mild at only c. 4%.

And finally, I don’t think we need to be too upset about profitable, thriving companies which experience some growing pains. FY25 revenue at Jet2 was only £7.2 billion. It’s now expected to generate nearly £8.5 billion in FY27, rising to £9.2 billion in FY28. There are plenty of things that shareholders in public companies can reasonably get animated about, but a slight reduction in the short-term profit forecast at a growing business like this isn’t really one of them, in my view.

We were GREEN on this at a market cap of £3.8 billion last year. The market cap is only £2.5 billion today.

EPS forecasts have been variable but have generally held up ok:

And in my view, a P/E multiple of less than 7x already prices in plenty of uncertainty over short-term earnings. In general, companies at this sort of rating are not expected or required to hit their forecasts perfectly, compared to companies trading at 20x or more.

Based on the latest EPS forecast for FY27 and the current share price, Jet2 shares are now trading at 6.7x FY27 earnings.

Therefore, it might be a little risky, but I think I can keep us GREEN on this, despite interpreting today’s news as technically being a profit warning.

Roland's Section

ME International (LON:MEGP)

Down 15.5% at 124p (£462m) - Delay in FY25 Audited Financial Statements - Roland - AMBER ↓

The market has taken a dim view of today’s news that the company’s auditor, Forvis Mazars LLP, has requested more time to complete its audit of ME Group’s FY25 accounts.

This delay means that ME Group’s results are expected to be delayed until “no later than 13 March 2026” and that its shares are likely to be suspended next week.

At this stage it’s impossible to know if there’s anything to worry about or not.

The company has reiterated previous guidance today and says that as of today, it’s “not been told of any material audit issues affecting the Group’s consolidated financial statements”.

This rather narrow statement does not seem to entirely rule out the risk that some issues may come to light, but it does seem to suggest that nothing serious is wrong.

ME Group’s financial year ends in October, so if the results are not published this week the company will breach the FCA’s requirement for Main Market companies to issue results within four months of their year end. This is why the shares are expected to be suspended from next week.

Trading update

Management reiterate November’s FY25 guidance today:

Revenue of between £311m and £318m;

Pre-tax profit of between £76m and £79m.

FY26 trading is said to be in line with expectations so far this year, with consensus forecasts suggesting a c.4% rise in EPS.

We are of course nearly four months into the current financial year, so this seems broadly reassuring following November’s profit warning:

Share buyback

ME Group also advises investors today that it expects to be able to implement a share buyback programme of £15-20m “shortly following publication of its FY25 results”.

If the results are published without any issues, then I’d imagine this might trigger a share price rebound – perhaps its intention.

Roland’s view

We could argue that a £500m FTSE 250 business ought to be able to publish audited results comfortably within four months if its financial controls and reporting are up to scratch. Personally, I think it’s a little disappointing that it’s come down to the wire in this way.

Without wanting to sound like a conspiracy theorist, I think it’s also worth remembering that this delay comes in the wake of:

A failed attempt to sell the company last year;

November’s profit warning;

The recent appointment of Vladimir Crasneanscki as Deputy CEO. He is the son of 83-year-old CEO Serge Crasnianski.

I wonder if these various events have disrupted normal business processes or contributed to some unforeseen financial complexity. Alternatively, the fault may lie with the auditors – perhaps they did not allocate sufficient resources to this job.

We don’t know what – if anything – lies behind this delay. But investors have already been voting with their feet over the last 12 months. ME the shares are now down by nearly 50% from their June 2025 highs:

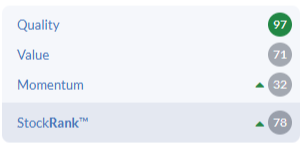

As a result, ME has earned a Contrarian styling from the StockRanks, with high quality and value scores but low momentum:

I can see this argument and might normally be tempted to consider investing at current levels. ME Group has a long track record of generous dividends (a common characteristic of owner management) and extremely strong quality metrics:

However, I’m not sure that I’m brave enough to buy into a dip caused by an audit delay where a FTSE 250 company is struggling to meet FCA reporting deadlines. I’m going to move our view down by one notch to neutral until this situation is resolved.

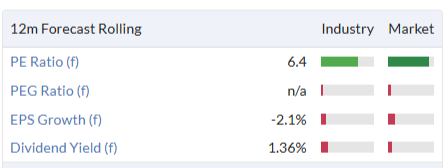

Diageo (LON:DGE)

Down 6.6% at 1,750p (£39.0bn) - Interim Results - Roland - BLACK (AMBER/RED =)

I’m relieved to see Mark downgraded the global drinks group to AMBER/RED in November, following a previous profit warning.

New CEO Sir Dave Lewis has opened his account today with another profit warning and a 50% dividend cut to help cut leverage.

Let’s take a look at the main points from today’s half-year results and – perhaps more importantly – Lewis’s initial comments on the business.

H1 results summary

Today’s headline numbers aren’t very encouraging, but a regional view on results presents a more nuanced picture.

Net sales down 4% to $10,460m (organic net sales -2.8%)

Operating profit down 1.2% to $3,116m

Adjusted earnings per share down 2.5% to 95.3c

Free cash flow down 9.7% to $1,532m

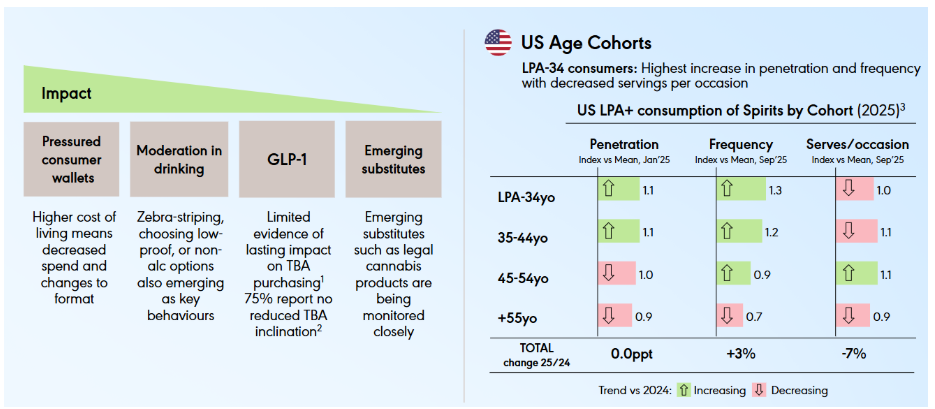

A regional breakdown shows that organic net sales (excluding disposals) rose in Europe, LatAm and Africa, only falling in North America and Asia Pacific. However, volumes were lower in all markets except Africa:

North America: softer spirit sales, especially Tequila, are said to be mainly due to pressure on consumer spending. A breakdown by spirit type shows tequila volumes fell by 17% in H1, with US whiskey volumes down 6%.

Weight loss drugs and moderating drinking habits are only seen as secondary factors:

(LPA = Legal Purchase Age)

Asia-Pacific (China): Diageo’s problems in the APAC region are mostly due to a slowdown in the consumption of Chinese White Spirits (CWS) such as baijiu. These are typically consumed at celebrations or formal events.

Net sales in Greater China fell by 42.3% due to a 50.4% decline in CWS that was blamed on “market policy changes” and shipment phasing due to the later timing of Chinese New Year.

Debt & Dividend

Today’s results show net debt of $21.7bn, largely unchanged from $21.9bn at the end of FY25. This gives Diagoe an unchanged leverage multiple of 3.4x adjusted EBITDA. For a business like Diageo, I would describe this as manageable but too high, from an equity investing perspective.

The new CEO seems to agree, as he has cut the dividend by c.50%. The new payout policy will target:

A 30% to 50% payout ratio

“A minimum floor” of 50 cents per annum

For context, last year’s full-year payout was 103.48 cents.

At current prices, a 50 cent full-year payout implies a forward dividend yield of c.2.1%.

It’s worth noting the recent disposal of East African Breweries and the group’s Kenyan spirits business will raise $2.3bn and is expected to reduce leverage by 0.25x.

Outlook & Updated Guidance

Unfortunately today’s guidance amounts to another profit warning:

Organic net sales to be down by 2% to 3% (previously “flat to slightly down”);

Organic operating profit to be “flat to up low-single-digit” (previously up by “low to mid single digit”);

Free cash flow of $3bn (unchanged) - aided by a c.$450m saving on the interim dividend vs last year.

To help support the group’s finances, spending is also being cut. Capital expenditure is expected to be at the lower end of the $1.2-$1.3bn guidance range, down from $1.5bn in FY25.

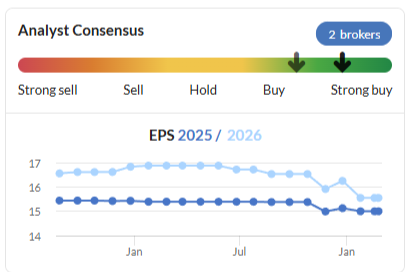

Diageo shares are down by c.5% this morning and I would guess that this is a reasonable indicator of the likely cut to FY26 EPS estimates. This would continue a long run of estimate erosion over the last 18 months:

CEO comments: early thoughts from ex-Tesco boss ‘Drastic Dave’ Lewis suggest that he is not planning any major disposals, but is focusing instead on improving Diageo’s operational and commercial executions. Areas highlighted include:

Improving customer service for distributors, seen as below standard;

Addressing supply limitations for Guinness and Guinness 0.0 which are resulting in lost sales;

Repositioning some brands to gain share in value segments;

Improve the “clarity”, “agility” and cost-efficiency of the group’s operations and capital deployment.

In The Week Ahead, I quoted an FT article in which an insider suggested Lewis thought Diageo had become “fat and happy”. His initial priorities seem to support this view, in my opinion.

Roland’s view

As he did at Tesco, I suspect Dave Lewis is planning to shake-up Diageo’s central functions and introduce new discipline and focus to its operations.

Whether this will be enough to return the group’s core brands to volume growth remains to be seen.

Assuming my view on EPS estimates is correct, I reckon Diageo shares are trading on a FY26E P/E of perhaps 15.5x at current levels, with a c.2.1% dividend yield.

For a business with this quality, scale and market leadership, this could be cheap. These results show an operating margin of 29.8%, in line with the underlying results from last year. Underlying return on capital employed was almost 15% last year.

Assuming volumes stabilise, I would hope ROCE might edge higher as Dave Lewis’s plans take shape.

Mark was AMBER/RED on Diageo in November. While my inclination is to take a neutral view today, I’m going to leave Mark’s view unchanged to reflect today’s profit warning. I would hope to be able to return to AMBER if May’s Q3 trading update is in line with guidance.

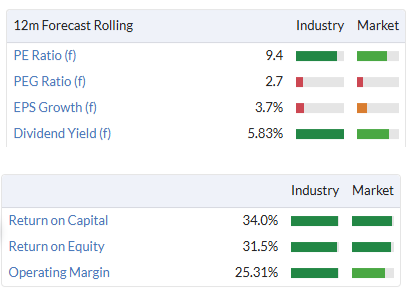

Morgan Sindall (LON:MGNS)

Down 2.8% at 5,180p (£2.5bn) - Results for year ended 31 Dec 25 - Roland - AMBER/GREEN ↓

I covered Morgan Sindall’s year-end trading update (and upgrade to FY26 guidance) less than two weeks ago, when the company upgraded its outlook for FY26. Despite this, I think today’s results provide some additional insight to add to our understanding of the business and the current outlook for 2026.

For this reason, I think it’s useful to consider today’s 2025 numbers and check if any change is needed to my previous GREEN view on this business.

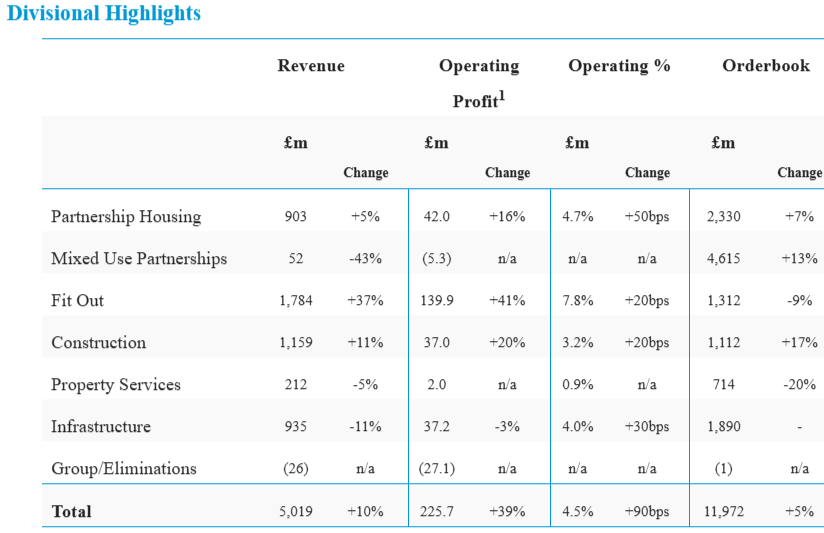

2025 results summary

Revenue up 10% to £5,019m

Pre-tax profit up 35% to £231.8m

Adjusted earnings up 33% to 370p per share

Dividend up 20% to 158p per share

Year-end net cash up £39m to £531m

Average daily net cash of £368m (FY24: £374m)

These are excellent figures by any standards and actually appear to be slightly ahead of the consensus forecasts on the StockReport for EPS of 355p and a 152p dividend.

My sums suggest an operating margin of 4.5% and a return on capital employed for the year of 27%, super figures that are comfortably ahead of last year’s 3.6% and 22%, respectively.

These high returns on capital help support strong cash generation and dividends. This is highlighted by the strong average daily net cash position – the gold standard of balance sheet quality in this sector. My impression is that cash generation is aided by very tight financial controls, disciplined bidding and careful project selection, all under the long-term leadership of co-founder and 6.8% shareholder John Morgan.

Trading commentary & Order Book: Looking at the segmental breakdown of last year’s results shows us that this growth was achieved despite weakness in partnership housing (widely reported elsewhere) and Infrastructure:

The Fit Out division was the standout performer in the business, generating 35% of sales at a much higher operating margin (7.8%) than any other part of the business. As a result, this division contributed 62% of last year’s operating profit.

This balance could shift over time, though, as it has done in the past. Interestingly, today’s commentary flags up changes to medium-term targets for two of last year’s weaker performing divisions:

Mixed Use Partnerships: return on capital up up towards 30% (previously 25%);

Infrastructure: Revenue up towards £1.5bn, operating margin of 3.75% to 4.25% (previously £1.0bn, no change to op margin);

Medium-term targets for all other divisions are unchanged today.

CEO John Morgan says these upgrades are supported by “the quality of returns within the work secured, market position held together with future prospects”.

The order book for the current year seems to support a positive view:

Secured order book up 5% to £12.0bn, with preferred bidder work increasing to £7.1bn

Partnerships up 29% to £11.5bn (Partnership Housing & Mixed Use Partnerships)

Fit Out down 2% to £1.8bn

Construction up 4% to £5.8bn (Construction & Infrastructure)

This seems to add some useful context to both FY26 forecasts and the guidance update earlier in February.

As Fit Out is the highest-margin part of the group, any slowdown here could have a larger impact on profits. Although the order book is multi-year and we don’t know exactly what work is earmarked for 2026, I wonder if this might help to explain why earnings are expected to fall slightly this year, even after this month’s upgrade:

Outlook

As I’d expect, FY26 guidance is unchanged today from the update earlier this month:

Looking ahead, and despite some of the current headwinds in the housing market, the Group remains positive for the year ahead and is on track to deliver an outcome for 2026 which is in line with its revised expectations set out in its Trading Update released on 12 February 2026.

Consensus estimates on the StockReport are for earnings of 328p per share this year, pricing the stock at just under 16x forecast earnings with a c.3% dividend yield.

Roland’s view

These are a lovely clean set of accounts, with minimal adjustments. There’s not really anything I can fault about last year’s performance, but I do feel that the slight weakness in the order book for Fit Out may be worth noting.

While I don’t want to overreact to what might simply be a shorter-cycle workload (i.e. bookings are not made so far in advance), any weakness in this division could have a more significant impact on profits due to its higher margins.

I’d also note that while it’s still early in the year, consensus forecasts I can see for both FY26 and FY27 suggest profits could flatten or fall slightly over the next couple of years.

While Morgan Sindall still looks very reasonably priced on an EV/EBIT multiple of about 10, I do think that a mid-teens P/E is probably high enough for a business in this sector.

In the absence of any catalysts for further upgrades today, I am going to moderate my view on this business slightly today and move down to AMBER/GREEN. This may prove to be over-cautious, given Morgan Sindall’s track record of beating expectations. But I think it’s a fair choice at this time, based on the information available today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.