Good morning! I have a backlog section on CRST to kick us off today.

Event tonight! At 5pm (London time), Megan and Ed are hosting a webinar on how to navigate reporting season. Here's the signup page.

13:15pm: we've run out of time again, thanks everyone.

Spreadsheet accompanying this report (last updated to: 23rd Jan 2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£57bn) | Final Results | 2024 rev +3% to £31.4bn, adj op profit +11% to £9.2bn. £1.8bn Zantac charge. 2025 outlook 3%-5% rev growth. | AMBER/GREEN (Roland) |

SSE (LON:SSE) (£17.8bn) | TU | FY25 adj eps exp 154p-163p (vs 158.5 in FY24). Business unit op profit exps unchanged. | AMBER (Roland) |

DCC (LON:DCC) (£5.4bn) | TU | Q3 adj op profit “broadly in line with prior year”. FX headwinds. FY25 op profit growth expected. | |

JTC (LON:JTC) (£1.6bn) | FY TU | FY results to be in line with market exps. Organic rev +10%, adj EBITDA margin 33%-38%. | |

Grainger (LON:GRI) (£1.6bn) | TU | 15% growth in net rental income. Occupancy 96%, in line with exps. Outlook “exceptionally supportive” | |

Future (LON:FUTR) (£1.0bn) | TU | YTD “on track to achieve market exps” in FY25. US ad market YoY growth, UK more challenging. | AMBER/GREEN (Roland) |

Target Healthcare Reit (LON:THRL) (£527m) | TU | 1.47p quarterly divi fully covered. Net tangible assets +0.9% to 112.7p, LfL valuation uplift. | |

Ferrexpo (LON:FXPO) (£478m) | Legal case | This Ukraine miner has received a claim for nearly $4bn in damages relating to alleged illegal mining. | RED (Graham) I have no insights into Ukrainian politics or their legal system, but can only assume there is a risk of shareholder wipeout arising from this lawsuit. |

Custodian Property Income Reit (LON:CREI) (£336m) | TU | 1.5p quarterly divi fully covered. C. 8% yield. Valuations stable, 0.5% LfL increase. | |

Aptitude Software (LON:APTD) (£178m) | FY TU | 2024 in line. ARR +2% to £52m total revenue fell as anticipated. Net funds £20m. 2025 started well. | |

James Fisher And Sons (LON:FSJ) (£154m) | FY TU | “Solid” H2. Underlying op profit c. £29m, ahead of exps. Net debt within target range 1.0 - 1.5x. | AMBER (Graham) An excellent transformation, including some disposals, has seen this get back into a reasonable financial position. Oil, gas and renewable energies are providing nice tailwinds as it proceeds. Perhaps it's trading at fair value here? |

Made Tech (LON:MTEC) (£41m) | Half-Year Results | H1 revenue +14%, adj. EBITDA +29%. Both now expected to be ahead of upgraded exps. | AMBER (Graham) Excellent momentum in terms of earnings upgrades, a healthy net cash position, and opportunities to benefit from government spending plans. But I wonder if it's still quite expensive for what it is. |

Tandem (LON:TND) (£9m) | TU | Rev +11% to £24.6m, adj. PBT in line. Early indicators in Jan 2025 align with management exps. | AMBER/GREEN (Graham) A new senior management team and a new NED. A meaningful discount to net tangible assets. I have run out of patience waiting for this to generate meaningful, sustainable profitability. In the short-term, prospects look decent. |

Backlog

Crest Nicholson Holdings (LON:CRST)

Down 7% yesterday to 163p (£419m) - Final Results - Graham - AMBER/RED

CRST’s track record as an accident-prone housebuilder continued yesterday with a £144m loss and a “going concern” warning that spooked the market.

Their full-year results (to October 2024) were “in line with guidance” officially, with an adjusted PBT of £22m.

Investigating the difference between the £22m adjusted PBT and the £144m statutory loss, it turns out that the main reason is a “combustible materials charge” of £132m.

This includes a £98.5m provision for estimated remedial costs for buildings that have not yet been surveyed, £15m of estimated remedial costs for buildings that have been surveyed, and an £18m increase in remedial costs for buildings where a provision had already been recognised.

So all of these items amount to pretty much the same thing, but it’s worrying that the actual cost appears so uncertain.

Net debt: £8.5m as of October 2024 (down from net cash of £65m a year prior).

Average net debt in the year was £50m, which I think is a more useful number.

Going concern warning: the market hated this disclosure, for good reason.

Whilst the Group forecasts to meet all its covenants in the base case scenario, the cumulative impact of the assumptions and mitigations in the SBP [severe but plausible] downside case indicates that the Group would not meet its interest cover covenant during the going concern period, with the first measurement date in April 2025.

I’m surprised that the Board have proposed a 1.2p final dividend in these circumstances.

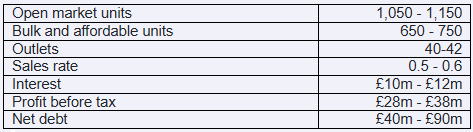

Guidance for 2025 suggests an increase in open market units and higher adj. PBT, although net debt is also forecast to increase:

Graham’s view

Readers may know that I tend to value housebuilders relative to NAV first of all, before other considerations.

Today’s results from CRST show one of the dangers with this approach: NAV can be volatile. CRST’s NAV has fallen from £856m to £729m, as a result of the large reported loss in these results.

At least this £729m is still a tangible number, mostly - there are only £29m of intangible assets on the balance sheet.

Therefore, for a £419m market cap, there is a lot of “value” on offer, if we can assume that another large set of provisions doesn’t come along in the current year to wipe out this value.

I also note that Bellway (BWY) were willing to offer around 262p per share for the business last year.

However, I must be disciplined. When there is a going concern warning, I always take a negative stance, due to the risk of dilution (or worse). So I’m going to take an AMBER/RED stance on this today. I would be fully RED except that I do think CRST shares offer some speculative value.

For example, it passes the Ben Graham NCAV Screen - but would Ben Graham invest in a share that had a going concern warning, even as part of a diversified portfolio? I'm not sure.

Graham's Section

Ferrexpo (LON:FXPO)

Down 23% yesterday to 80p, now at 73.7p (£442m) - Update regarding Ukrainian subsidiary - Graham - RED

I’ve never commented on this before as it’s an iron ore miner based in Ukraine.

Keelan covered it in an article about opportunities in base metals here.

Yesterday’s RNS concerned a police investigation that Ferrexpo had previously mentioned in an update on 16th January.

The January update noted that the Prosecutor General’s Office of Ukraine had made accusations against senior Ferrexpo managers relating to “the alleged illegal mining and sale of waste products that are produced normally as a result of the mining and processing of iron ore”.

The case had been sent to court, awaiting a first hearing date.

Yesterday we had an update as follows:

FPM [Ferrexpo Poltava Mining] has now received information that a civil claim was filed seeking joint liability of FPM and its General Director for damages amounting to UAH 157 billion (approximately US$3.76 billion) in favour of the Ukrainian state.

Initial accusations on the illegal sale of waste products have transformed into accusations that FPM is illegally mining and selling subsoil (minerals other than iron ore), which is said to have caused damage to the environment. FPM rejects these allegations in their entirety on the basis that there was no illegal extraction of the subsoil.

Graham’s view

This is a geographic problem, first and foremost. Who can understand the motives of the Ukrainian police and prosecutor’s office? Not me, that’s for sure.

One of the reasons that I stay away from the resource sector is that many listed resource companies are based in geographies, such as the Ukraine, where I do not understand local politics and where political matters can and often do interfere with business. Perhaps locally-owned businesses might do a little better, but London-listed companies with foreign shareholders rarely seem to attract much sympathy from the authorities who govern many resource-rich locations.

FXPO’s homepage loudly blasts that they are “standing with Ukraine” and have been involved in providing a great deal of humanitarian assistance in the country. But apparently that is not enough to insulate them from these charges (to be clear, I don’t have a view on whether or not these charges have any merit.)

I’m going to go RED on this as a claim for $3.76bn of damages poses an extreme risk to FXPO’s Ukrainian subsidiary and I have no way of knowing the probabilities around the outcome of this claim. Perhaps it will go away and the company will carry on as normal, but how are we to know?

Made Tech (LON:MTEC)

Up 12.5% to 31.2p (£47m) - Half Year Results - Graham - AMBER

Made Tech Group Plc, a leading provider of digital, data, and technology services to the UK public sector, is pleased to announce its unaudited half year results for the six months ended 30 November 2024

I had a brief look at this in November, on the day of its AGM.

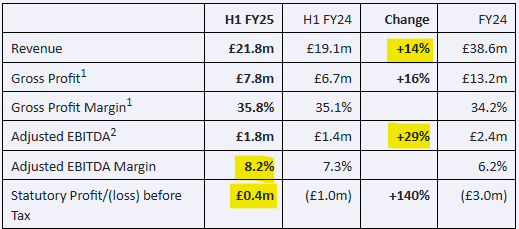

Today we have interims; here’s an excerpt from the table.

Estimates: The company is now tracking ahead of expectations for FY May 2025 and they helpfully inform us that prior expectations were for revenues of £38m and adj. EBITDA of £2.8m.

It looks like 57% of the full-year revenue estimate was achieved in H1, and 64% of the full-year EBITDA estimate.

It’s great to see EBITDA profits growing faster (at 29%) than revenues (at 14%).

Although I must point out that the EBITDA margin of 8.2% is still quite low, compared to what you might see from businesses in higher-quality sectors. MTEC is a consultant providing IT transformation services to the UK public sector.

Singers have helpfully provided fresh numbers today: they are now looking for adj. EBITDA of £3.0m this year, rising to £3.4m next year (FY May 2026). They also suggest that further upgrades are possible, and they believe the company is heading towards an adj. EBITDA margin of 10%.

Adjustments: In November, I suggested MTEC had a poor track record when it came to converting adj. EBITDA into real profits.

The table I posted at the start of this section highlights the problem, as while the company did generate a small pre-tax profit in this six-month period (£0.4m), that’s only a fraction of its adj. EBITDA (£1.8m).

When I investigate this, I find that the biggest reason for this discrepancy in H1 was £1m of share-based payments, i.e. management remuneration. This is not an adjustment that shareholders should be ignoring, in my view. And it’s a significant number in the context of a sub-£50m market cap.

Net cash: £9m, so the enterprise value is £47m minus £9m = £38m.

Current trading and outlook:

Strong trading performance expected for FY25 underpinned by £80.8m Contracted Backlog, with the Group on track to achieve double-digit percentage annual revenue growth for FY25 and free cash flow positive for the year

A strong sales pipeline, active bids, and Government stated priorities indicate a positive outlook for FY26 and beyond

The CEO echoes the above, saying “the business is in great shape to benefit from new public sector digitalisation programmes, which are expected to be announced in the UK Government Spending Review in the Spring.”

Graham’s view

Probably my favourite aspect of this stock is that it’s a likely beneficiary of the new government’s tax/spending policies, rather than a victim.

Top-line growth is good, and margins are improving.

But I really want to see this convert into meaningful profits. Latest forecasts suggest adj. PBT of £2.1m in the current year, and then £2.4m in FY26.

Write that down by 25% and we have adjusted after-tax net income of £1.6m and then £1.8m.

Whichever way you cut it, the P/E is well over 20x.

I still don’t think I can give this anything more bullish than AMBER. It can grow into this valuation, but it’s not there yet.

James Fisher And Sons (LON:FSJ)

Up 9% to 334.7p (£169m) - Full Year Trading Update - Graham - AMBER

James Fisher and Sons plc (FSJ.L) ('James Fisher', 'the Group'), a leading marine services company providing innovative solutions across energy, defence and maritime service, today provides an update on trading for the year ended 31 December 2024

Excellent news as we learn that underlying operating profit will be c. £29m, ahead of expectations.

For a small company, this enjoys plenty of broker coverage, four brokers in total. Although none of them have posted up on Research Tree about it recently.

I think the estimate for underlying operating profit was c. £25m. It looks like we have a significant beat against that number, but we should bear in mind that it includes “a contribution from several specific non-recurring items”.

Exposure to the cyclically strong energy sector has been a boon to performance (oil, gas and wind).

FSJ’s defence division has also done well, so the only weak point at the moment is the “maritime transport” division, which has seen weaker demand for ship-to-ship LNG transfers.

Net debt: within the target range of 1.0-1.5x, sounds fine. The company has a recently refinanced £95m facility.

CEO comment:

We ended the year in a stronger position having continued to execute on our turnaround strategy, including undertaking disposals and refinancing our debt facilities. As a result, we are now beginning to see the benefits of our transformation programme coming through.

The company has had a very poor run, explaining the need for transformation:

I’m encouraged to see no increase in the share count in recent years, despite the poor financial performance. Disposals of non-core businesses have been key to achieving that.

Outlook: trading in the new year has been in line with expectations, so I think we need to underline that the earnings beat for 2024 was the result of non-recurring items.

Whilst conditions in key end markets are expected to remain supportive in 2025, underpinned by structural drivers, the Group remains mindful of the continued near term political and economic uncertainty.

Against this backdrop, the focus remains on delivering against the turnaround plan, with the next phase of initiatives now underway. The Board sees opportunities to build on progress made to date and drive the business further towards its medium-term target of 10% underlying operating profit margin.

Graham’s view

I think today's gain in the share price is a little optimistic, as the earnings beat is due to non-recurring factors and the 2025 outlook is merely in line. Nothing wrong with that, but does it justify a nearly 10% increase in the valuation?

More broadly, I was negative when I looked at this a year ago. Paul was neutral in more recent times, thinking that it could be interesting once disposals completed.

With a refinancing out of the way and a reasonable leverage multiple, I’m happy to be neutral on this now.

It doesn’t stand out to me as being particularly cheap, but it’s no longer in a financial emergency.

Well done to FSJ for getting through a very difficult period. Hopefully better days lie ahead!

Tandem (LON:TND)

up 20% to 191.5p (£10m) - Trading Update - Graham - AMBER/GREEN

This is now eligible for coverage, as its market cap has reached back up to £10m!

I used to own a lot of TND stock, relative to the size of my portfolio. I eventually got out and didn’t look back, as I got sick of the endless problems at this company.

It has been listed for decades and the fact that it is still worth just £10m tells the story.

But today’s update is quite encouraging.

2024 revenue is up 11% to £24.6m.

Adjusted PBT will be in line with expectations, although no word in this RNS about what those expectations are. It looks like about £0.5m was forecast.

For a company as old as this, operating in mature industries, a pre-tax profit of £0.5m doesn’t impress me too much, but at least it’s no longer loss-making, as it was in the previous year.

Toys, Sports & Leisure: revenue up 20%.

Bicycles: revenue up 11%. Within this, Squish bike sales were up 69%.

Golf: up 13%. Home & Garden: down 22% due to bad weather.

Outlook: “early indicators in January align with management expectations”.

Graham’s view

I’m planning to never own this share again, as I didn’t enjoy owning it the first time. It wasn’t good for my sleep! Although that’s probably got something to do with the fact that I owned too much of it.

The new management team is supposed to be more shareholder-friendly than the previous team, who seemed to view external shareholders as a nuisance.

17% shareholder Simon Bragg has been on the board as NED since October 2024. They also have a new Chief Commercial Officer on the board as of January.

Checking the most recent interim report, I see net assets of £23.3m, although £5.5m of this is intangibles. Let’s call it c. £18m of tangible assets.

As of Dec 2023, the last date for which we have an annual report, the company claimed to have £14.3m of freehold land and buildings included within PPE, more than the market cap.

So I’m guessing there is probably still some deep value available at TND. I don’t have any faith in the long-term profit profile, so personally I’m going to pass. But the stock can move when it wants to - up 20% today - and may have further to run. AMBER/GREEN.

Roland's Section

Future (LON:FUTR)

Up 2% to 953p (£1.1bn) - Trading Update - Roland - AMBER/GREEN

Future plc (LSE: FUTR; "Future" or "the Group"), the global platform for specialist media, today announces a trading update covering the four-month period ended 31 January 2025.

I remember buying cycling magazines published by Future Publishing when I was a teenager. Today the company has a broader UK/US offering, primarily online, and is also the owner of the Go.Compare price comparison website.

FY25 outlook: this morning’s trading update appears to be broadly positive. Departing CEO Jon Steinberg has left expectations for the year to 30 September 2025 unchanged:

Overall Group performance in the first four months has been as expected with the Group on track to achieve market expectations for FY 2025.

Future has helpfully provided figures indicating its view of consensus forecasts:

FY25 revenue: £776.9m (range £758.5m to £785.4m)

FY25 adj operating profit: £217.8m (range £197.3m to £223.0m)

These figures are slightly below the equivalent figures for FY24 of £788.2m and £222.2m. Future expects a return to revenue growth from FY26.

Current forecasts appear to support a forward P/E of 7 for the current year – potentially interesting value if the business does return to growth. Cash generation has been strong, historically.

Trading summary: Future generates revenue from advertising, ecommerce affiliate sales and traditional subscriptions and newsstand sales. The company was hit hard by the post-pandemic advertising slump, but is now showing signs of recovery.

Looking at the detail of today’s update, my impression is that performance remains mixed, albeit without any major concerns.

B2C: this division includes all the consumer publishing online and in print. B2C generated 66% of revenue last year. Progress during over the last four months appears to have been stronger in the US than the UK:

Improvement in US digital advertising and ecommerce “has continued”

UK advertising “continues to be challenging”

Magazines (i.e. printed) have been “more resilient, led by premium titles”

The UK remains the largest market for Future, generating over 60% of revenue. The US generates the remainder. So slower conditions in the UK could potentially continue to hold back the performance of the wider group.

Go.Compare: this UK price comparison website enjoyed “a standout” FY24, thanks to a surge in car insurance switching. However, performance has now moderated, “reflecting the expected slow-down in the car insurance switching market”.

Go.Compare is continuing to diversify into markets such as home insurance “which are delivering good growth”.

B2B: this business provides content marketing solutions for corporate customers. Performance “remains mixed” so far this year.

Share buyback: a £55m buyback is ongoing, with just under £10m repurchased to date.

New CEO: Jon Steinberg will be replaced by Kevin Li Ying at the end of March. Ying has been at Future for over 20 years and is currently head of B2C, the company’s largest division.

Roland’s view

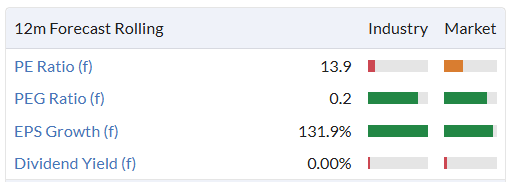

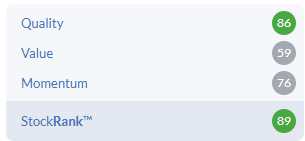

Stockopedia’s algorithms style Future as a Super Stock with a StockRank of 89. My view on the business is broadly positive at the current valuation, too.

One point I would make is that the company is a heavy adjuster of profits. In FY24, for example, adjusted operating profit of £222m translated into reported operating profit of £134m.

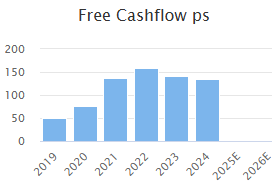

My test in these scenarios is to look at the company’s free cash flow. I calculate Future’s FY24 free cash flow to have been £156m, excluding acquisitions.

This compares very well with the current £1bn market cap, implying a free cash flow yield of c.15%.

So while I’d prefer to see fewer adjustments, in this case I don’t see it as a concern, given the company’s strong cash generation and modest valuation.

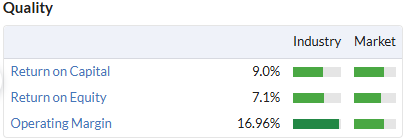

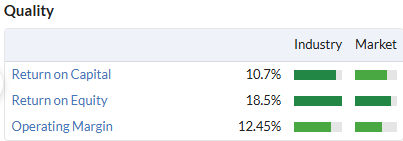

The other point I’d make is that while Future’s margins are quite high, return on capital employed and equity are more average. I think this is largely a reflection of hefty past spending on acquisitions, some of them perhaps quite fully priced:

Graham took an AMBER/GREEN view on Future in December. I don’t see any reason to change this today.

GSK (LON:GSK)

Up 5% to 1,458p (£60bn) - Final Results - Roland - AMBER/GREEN

Pharma group GSK is one of the first UK companies to publish full year results for 2024. Five weeks from the year end seems an impressive turnaround for a global business that handled £31.4bn in sales last year.

Megan covered GSK more broadly in a recent article here. Let’s take a look at some highlights of today’s results, which have been well received by the market:

Total sales up 7% to £31.4bn at constant currency

Core (adjusted) operating profit up 11% to £9.2bn

Core EPS up 10% to 159.3p at constant currency

Dividend up 5% to 61p per share

£2bn share buyback programme

Net debt down £1.9bn to £13.1bn

Trading commentary: last year’s growth was driven by the company’s specialty medicines portfolio, where sales rose by 19% to £11.8bn. This includes cancer, respiratory/immunology and HIV treatments.

This strength offset a weaker performance in vaccines, where sales were down 4% at £9.1bn. Vaccines have historically been a key strength for GSK, but in today’s results CEO Emma Walmsley suggests the group’s focus may be shifting slightly:

In particular, we are increasing and prioritising R&D investment to promising new long-acting and specialty medicines in Respiratory, Immunology & Inflammation, Oncology and HIV.

One reason for this, of course, may be the possibility that the political support for vaccines in the US is about to weaken. Sales of flagship vaccines for shingles, RSV and flu all fell last year, while the company’s Established Vaccines portfolio only managed to eke out a modest gain.

This compares to double digit sales growth for HIV and respiratory/immunology medicines, together with a near-doubling of sales in oncology, aided by recent acquisitions.

Zantac litigation: GSK appears to have (almost) resolved the litigation relating to the heartburn treatment Zantac. Today’s results include details of a £1.8bn charge related to settlement costs.

Outlook: GSK tends to provide quite clear guidance. Today we have numbers for 2025:

2025 revenue growth of 3% to 5%, versus analyst expectations of c.3.5%

2025 core EPS up 6% to 8%, aided by a £2bn share buyback

2025 dividend is expected to be 64p, giving a 4.4% yield

We also have upgraded guidance for the period to 2031:

2031 sales outlook: revenue target increased to “more than £40 billion”, from £38bn previously.

This upgrade reflects “late stage pipeline progress” with “significant phase III” trial progress since last year and “multiple launch opportunities” over the next five years.

Roland’s view

As an investor I tend to lean towards relying on quantitative metrics. GSK is always an interesting study in this way.

Quality metrics are quite strong, although not outstanding (and weaker than some peers):

However, the gaping chasm between core and reported profits always causes me some concern.

For example, today’s 2024 results show a core operating margin of 29.2% (£9.1bn), but a reported operating profit margin of just 12.8% (£4.0bn). Adjusting out the £1.8bn Zantac settlement improves this to 18.4% (£5.8bn).

When faced with big adjustments I generally turn to the cash flow statement to understand what’s actually happening.

My sums suggest GSK generated free cash flow of £4.2bn last year (2023: £4.1bn).

Using this as a guide suggests the stock is currently trading with a free cash flow yield of around 7%. That seems like reasonable value to me, and comfortably covers the £2.5bn dividend.

I’m torn between whether to go AMBER or AMBER/GREEN with GSK today. The company’s indifferent performance over the past decade suggests some caution may be warranted. The shares first traded at current levels in 2011:

However, today’s results and upgraded outlook seem broadly positive to me and the stock’s forward P/E of nine doesn’t seem too demanding.

With the Zantac issue now (hopefully) fading into the past and the prospect of improved cash generation, I am going to take a chance with an AMBER/GREEN view.

SSE (LON:SSE)

Up 1% to 1,630p (£18.0bn) - Q3 Trading Statement - Roland - AMBER

Today’s update from this FTSE 100 utility group provides earnings per share guidance for the 25/26 financial year, which ends on 31 March 2025:

2024/25 full year adjusted earnings per share expected to be between 154 - 163 pence

The consensus shown in Stockopedia prior to today was 163p, so today’s guidance range is perhaps towards the lower end of expectations.

The market does not seem concerned though, which may be because CFO Barry O’Regan has confirmed that the group remains on track to deliver material growth in earnings in the 2026/27 financial year:

Looking further ahead, our resilient and balanced business mix continues to give us confidence in achieving targeted adjusted earnings per share of between 175 - 200p in 2026/27.

SSE is one of the UK’s largest renewable generators and reports that its renewable output rose by 26% to 9,253GWh over the nine months to 31 December 24. This increase was driven by a mix of new capacity and favourable (i.e. windy) weather – about three quarters of SSE’s renewable output is from wind.

Interestingly, gas generation remains more significant in terms of volume and has also risen. Output from SSE’s thermal power stations rose by 15% to 12,459GWh during the nine months to 31 December.

The outlook for the final part of the year remains somewhat uncertain, with “variable weather conditions” seen in January. Presumably this is reflected in the range of earnings estimates for the full year.

SSE’s transmission networks business (in Scotland) is said to have delivered a “strong operational performance” to date.

Roland’s view

SSE’s share price has pulled back substantially since September:

The share price decline seems to have reflected a series of earnings downgrades for the 25/26 financial year since last summer:

Exposure to weather-related variability and lower future prices are possible risks, but my main concern when I look at big UK utilities is usually the level of capex and debt involved.

SSE plans to invest at least £22bn in grid infrastructure by 2031 and potentially up to £32bn. The group’s net debt was just under £9bn at the end of June 2024 and will presumably be higher by 2031.

While borrowing is linked to regulated asset values (i.e. regulated income), the numbers involved are staggering and I would guess that there’s at least some risk the dividend could come under pressure again at some point.

However, SSE cut its payout a few years ago and now has earnings cover >2x. I think this should provide some level of safety unless the premise for payouts is altered.

On balance, my feeling is that the shares are probably fairly valued at current levels. The 4% dividend yield should be covered and my sums suggest investors could see a return on cost of equity of 10%-12% from buying at current levels.

I’m going to take a neutral view ahead of the company’s year end. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.