Good morning! I'm looking forward to Ed's next webinar here, at 12:30 today, explaining more about StockRanks - a proprietary Stockopedia system which I am growing in confidence about, as it has already established a very good track record. It tends to favour stocks which fit many of my criteria too (a lot of my bigger holdings seem to have high StockRanks), although personally I like to apply additional filtering to exclude companies with weak balance sheets. I'm very happy that StockRanks provide an excellent starting point for a shortlist anyway, so it is not only steering us away from shares that are likely to underperform, but also saves a lot of time. I'll be out of a job here if StockRanks gets too good!!

Entu (UK) (LON:ENTU)

Share price: 121.5p

No. shares: 65.6m

Market Cap: £79.7m

Final results - for the year ended 31 Oct 2014. These are maiden results as a listed group, since Entu floated on 30 Oct 2014. It is a group of home improvement companies - e.g. replacement windows, conservatories, boilers, solar panels, etc.

I flagged up this company here on 15 Dec 2014 when it issued a positive trading update, so results this morning were expected to be good, and they are. Very good actually.

Trading - turnover is up 24.6% to £119m, and pre-exceptional operating profit up a tremendous 69.5% to £10.3m. Note 4 to today's results (segmental analysis) shows some dramatic shifts in profitability by division. So the home improvements division (which is nearly 71% of turnover, at £84.3m) generated a relatively modest operating margin of 4.5%, with operating profit of £3.8m (up 6.3% against prior year).

The energy generation & saving division saw operating profit shoot up from £0.2m to £1.8m. A similar strong rise in profits occurred at the Insulation division, where profit shot up from £0.4m to £2.7m.

I have put a call in to the company, to get a bit more flavour on what has driven these strong increases in profit at two of the smaller divisions, so will report back later if there is anything interesting to convey.

Valuation - adjusted EPS came in at 12.3p (up 57.7%), which is ahead of broker consensus, which was for 11.97p. Therefore the shares are only rated on 10 times historic earnings now, which seems a very reasonable price for a business that is performing well.

Broker forecast is for 13.26p for the current year (ending 31 Oct 2015), although I wouldn't be surprised if the forecasts are increased as the year goes on. Personally I'm thinking in terms of 14-15 EPS for this year. If I'm right, and assuming a more fair PER of say 12, then that gets me to a personal price target of 168-180p. That's 38-48% upside on the current share price, so very much worth sitting tight on my existing shares.

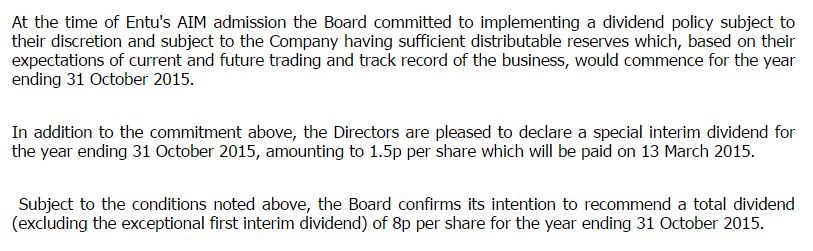

Dividends - better still, Entu is committed to paying shareholders handsomely for waiting. One of the reasons I bought these shares shortly after the IPO, was that the admission document stated the company's intention is to pay an 8% dividend yield (based on the IPO price of 100p per share).

That commitment has been reiterated today, and the company has also paid a 1.5p starter dividend, which is on top of the intention to pay 8p divis for the y/e 31 Oct 2015;

So whilst there is wiggle room in that statement, it's pretty clear that the company wants to, and intends to pay generous divis.

Balance sheet - the company generated strong cashflow in the year, and ended with net cash of £5.8m. Overall the balance sheet is surprisingly thin, with only £0.9m net assets, and minus £0.8m net tangible assets. Normally that would be a red flag for me, but in this case the company's business model cleverly outsources production. So the suppliers provide nearly all the capital needed. That leaves Entu sitting in the middle between customers & suppliers as a sales & project management operation.

Not only is this model capital light, but it is also flexible - so the company can downsize in a recession fairly easily & without onerous costs. I like this business model, as it seems to eliminate much of the risk for shareholders.

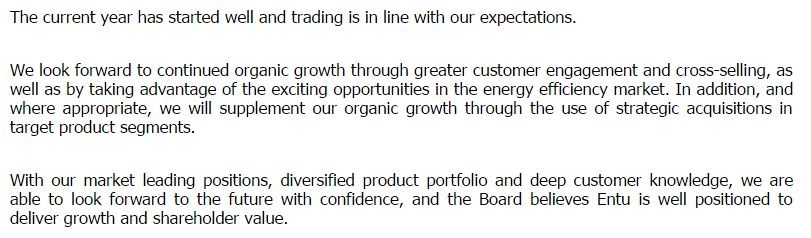

Outlook - this sounds positive to me, and I like the emphasis on more organic growth. A bank facility exists for bolt-on acquisitions too;

My opinion - as you've probably gathered by now, I like this share! It's just a classic value share in my view, with a low PER and an attractive dividend yield, and a capital-light business model, with net cash in the bank.

Sure it's cyclical, but I think with interest rates low, and consumers having more discretionary spending & confidence, this is the right time in the cycle to be looking at companies like this. There might also be something of a backlog of home improvement work possibly? i.e. if consumers have felt nervous over the last few years, now that they can finally see incomes rising ahead of inflation again, then they are more likely to decide to have new windows, or a conservatory, which they might have been putting off for the last few years perhaps?

Not all IPOs are over-priced flops. It's good to see that Entu seems to have been priced sensibly, even cheaply, as it has risen since the IPO;

Agreement with Flow Group - we were discussing Flowgroup (LON:FLOW) yesterday funnily enough, and today Entu has announced that it will be an authorised installer of these new boilers. So in a way perhaps Entu is a picks & shovels type of investment, whereas Flow is the more speculative (higher risk, but higher potential reward) share. It seems a good fit with Entu's existing product offerings, which have a theme of environmental benefits.

Entu already has the sales teams out there, and the installation teams, so adding another product onto that infrastructure should be positive for both companies, I imagine. It might also provide useful intelligence about how well (or not) Flow products are selling. So if Entu announce that they are selling like hot cakes, then that could be my cue to buy back into Flow shares, with a bit more comfort that commercialisation is working. For the moment though, I'm watching and waiting re Flow.

UPDATE - I've had a useful telecon with the CFO of Entu, and comment as follows;

Bank facilities at the moment are modest, and not utilised. However, the bank is receptive to providing finance for possible acquisitions. The company would limit any future borrowing to under 2 times EBITDA, which sounds fine to me. Lots of potential acquisitions in this space. Being a Listed company has raised their profile.

Divisional profit - the warranties business looks highly profitable, but it shares the overheads (free) of other divisions. So would be much less profitable if costs were allocated.

Improved performance from smaller divisions is expected to continue.

Flexible cost basis means the group can adapt easily & quickly to market changes. They like having a portfolio approach, so if demand weakens in one area, they can make it up elsewhere.

Related party transactions - these were over-reported, to be completely open. Due to changes in shareholdings, there won't be related party transactions in future. A lot relates to Epwin, which has itself now Listed.

Flow group - Entu really likes their product, and think it has huge potential. So hoping for a big future from this new product line.

Hornby (LON:HRN)

Trading update - it sounds as if things are stabilising at the previously troubled toy models maker. The company today says that sales & profits for the year to date (y/e 31 Mar 2015) are in line with expectations.

Net debt has come down a bit, to £7.9m at end Dec 2014, although I assume that might be a seasonally positive cash position after Xmas sales are in the bag?

The company is relocating from its outdated Margate site, to a modern office in Sandwich. Note that the Margate site is freehold, so one would need to find out how much that is worth. Probably not much, given that it's in Margate, but who knows?!

Outlook - positive noises are made about reaction to new ranges, at toy fairs, etc.

My opinion - it seems to me that the shares are already pricing in a significant recovery in earnings, which hasn't happened yet. It's priced at 26 times this year's earnings, which seems way too high to me. That is basically asking you to pay up-front for a doubling of profit in future, when there's no guarantee such a doubling will happen.

The price looks much too warm to me. I suppose people are hoping it can get back to 10-12p EPS levels that it achieved prior to the supply chain problems. However, there are no dividends, and if you want a cheap toy company, then it seems to me Character (LON:CCT) is a vastly better value proposition right now. It's trading well, is cheap, and pays divis. Whereas Hornby is expensive, doesn't pay divis, and has too much debt. It's a very easy choice for me - I'm long Character Group.

Simigon (LON:SIM)

A positive trading update today has propelled these shares up 19% to 25p today.

It's based in Israel, and as regulars know, I rarely touch any overseas companies listed on AIM. The company is also very small. It has high cash balances for the size of company, and has started paying divis too - although I believe there can be a problem of withholding taxes when it comes to divis from Israeli companies, so that needs checking.

All in all, might be worth a look for the more daring of you!

All done for today!

Do check out the new "Ranks" tab at the top of the Stockopedia black menu. Ed explained the new features very well today, although it amused me how he chose Rank (LON:RNK) to explain the Ranks! So it got slightly confusing lol!

See you in the morning.

Regards, Paul.

(of the companies mentioned today, Paul has a long position in ENTU, and no short positions. A fund management firm with which Paul is associated may also hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.