Good morning. Apologies, I didn't get round to further updating yesterday's report in the afternoon/evening, because it took over 5 hours to get back to Hove from London - a derailed train just outside Brighton station brought everything to a standstill. Then I had to spend the evening doing the monthly accounts for my local share club.

RWS Holdings (LON:RWS)

Share price: 136p (down 10.7% today)

No. shares: 211.6m

Market Cap: £287.8m

Trading update - for the

half year ended 31 Mar 2015. This is a firm which provides specialist services (e.g. translation) to patent attorneys and direct to corporates, and other patent-related

services. I've not reported on this company for a long time, as the shares

looked too expensive. They've come down quite a bit lately, hence

it's worth me running the slide rule over the figures, as from a value

perspective we want to be buying low, and selling high, not the other way

around!

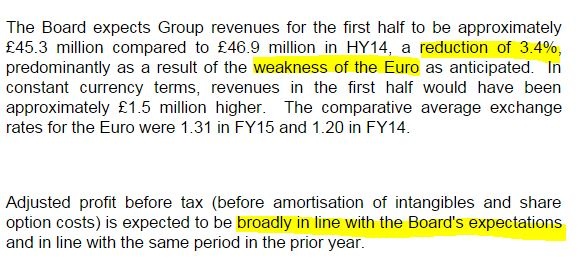

The first bit of today's statement is saying that turnover was flat in constant currency terms, but down 3.4% due to the weak Euro. Profit is slightly below expectations, and flat against last year;

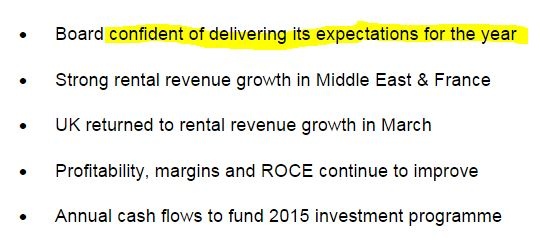

Outlook - the Directorspeak sounds confident;

However, to my mind

the optimism in this paragraph doesn't seem consistent with the

more cautious comments also made today in this update about competitive

pressures, client wins being slow to convert into sales, and subdued trading

conditions.

Net cash - is reported at £21m as at 31 Mar 2015, so a very comfortable position there, and gives them scope to finance more bolt on acquisitions from existing resources. Note that the company has expanded over the last six years without issuing any significant quantity of new shares - always good to see companies which can self-fund their expansion.

Dividends - nothing is mentioned today, but Stockopedia shows the forecast

yield last night at 3.36%, so adjusting for today's share price fall that

should now be c.3.7% - not bad considering the divi rises about 14% each year.

I prefer a solid divi yield that is consistently rising, and reasonably well

covered, rather than chasing often unsustainably higher yields of 5%+.

My opinion - broker forecasts are for 8.0p this year, which might be a struggle to achieve, reading between the lines of today's update. So at 136p it hardly looks a bargain - that's a PER of 17.0.

I think a price of about 100p would be the right sort of entry price for me, so am happy to pass on this for the time being.

Lavendon (LON:LVD)

Share price: 171p

No. shares: 169.0m

Market Cap: £289.0m

Trading update - covering Q1 of the current calendar year. This is a rental company, of powered access equipment, with around half its business coming from the UK, and the balance from Europe and the Middle East.

The summary bullet points today say;

The UK was soft, with rental revenues down 3% in Q1, although this improved throughout, so a soft Jan-Feb, with a better Mar (up 1%). The M.East and France doing well has probably raised a few eyebrows in surprise.

Net debt - is reported as having risen to £98m, which is due to a heavy capex programme to expand the rental fleet.

My opinion - I quite like this share, but am a little reluctant to invest in equipment hire companies, since they are currently benefiting from very low interest rates. I've had a look through the 2014 Annual Report, and didn't notice any details about interest rate caps, so I assume borrowing costs are at floating rates, so a rise in interest rates would eat into profitability.

The divis are alright, but nothing to write home about at a forecast yield of about 2.9%.

Overall it comes close to, but doesn't quite float my boat.

Epwin (LON:EPWN)

Share price: 107p

No. shares: 135.0m

Market Cap: £144.5m

(at the time of writing I hold a long position in this share)

Final results - for calendar 2014. This is the first time I've written here about this group of building supplies companies. Looking at their website, the main product lines seem to be: patio doors, double glazing, window cills, fascia boards, cladding, guttering, drainage, conservatories, etc. They seem to operate through a wide variety of individual brands.

The Epwin name might be familiar, as it was previously listed, but was taken over in a cash bid, and de-listed in Dec 1999.

Zeus Capital floated Epwin again in Jul 2014, and the company is closely linked to another share I hold, Entu (UK) (LON:ENTU) which is the direct selling part, and sources a lot of its products from manufacturer Epwin. On balance I prefer the business model of Entu, as it seems to carry less inherent risk from a downturn - since it outsources production & stock holding to Epwin. Therefore Entu is just a cash machine, and is using that cash to pay out generous divis.

That said, I'm impressed with the figures from Epwin today too.

You have to bear in mind that both these businesses are cyclical, but we seem to be at the right point in the cycle where they are trading very well.

Turnover rose slightly to £259.5m for 2014, and underlying operating profit rose strongly from £13.3m in 2013 to £18.3m in 2014.

Basic EPS is reported at 11.76p for continuing operations. Although I think this benefits from a £3.5m one-off gain from a business closure & releasing provisions for onerous leases, by the looks of it (the descriptions given are a big vague).

Valuation - by my back of the envelope calculations, adjusting out the one-off gain, I get to an adjusted (by me) EPS figure of about 10p per share. That's in the same sort of ballpark as the broker consensus for 2014 shown on Stockopedia of 10.7p.

Therefore at 107p per share, we can see that the PER is between 10-11, which looks reasonably attractive in my opinion. Although arguably this type of business should never command a high PER, as barriers to entry are limited, there's plenty of competition, and it's operating in a very cyclical sector.

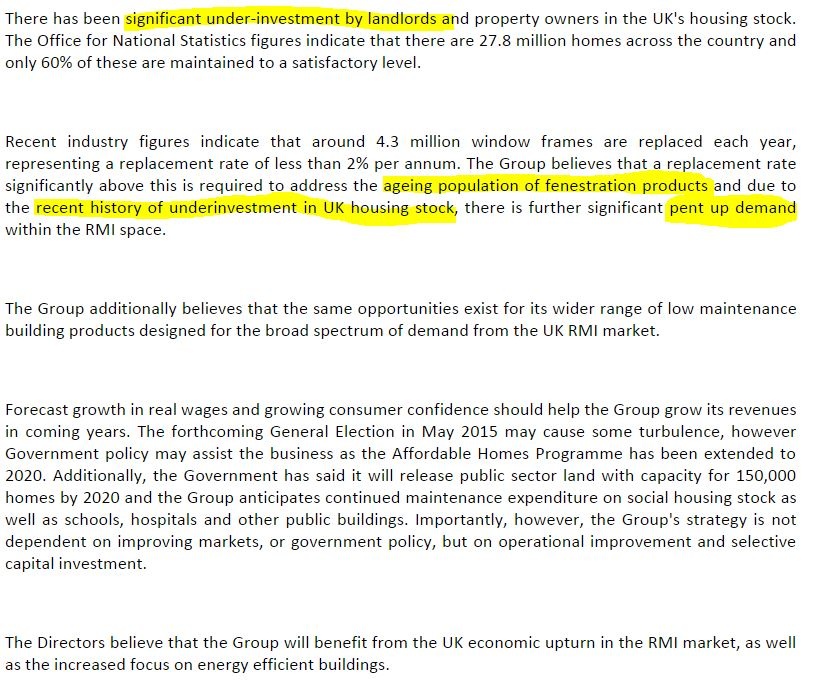

Outlook - this is a huge copy/paste below, but it's all interesting, so worth repeating here:

My opinion - I only highlighted "ageing population of fenestration products" above because it's such a fabulous phrase!!

I buy into the optimistic outlook above, and this suggests to me that there could be a number of good years ahead of companies like Epwin & Entu. For that reason, I think the shares look quite attractive at relatively modest PER, and with generous divis too (Epwin is forecast to pay out over 6% in divis in 2015).

On the other hand, with cyclical companies one has to keep a close eye on the exit - when the next Recession does occur, then cyclical companies can easily lurch from big profits to big losses. In theory Entu should be less vulnerable, as its salesforce is outsourced, and its production is outsourced - therefore it should be able to scale up & down with little in the way of one-off costs. Epwin should be the more cyclical, and hence more vulnerable to downside risks. Anyway we'll see.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.