Good morning!

Spaceandpeople (LON:SAL)

Share price: 57p (up 27% today)

No. shares: 19.5m

Market Cap: £11.1m

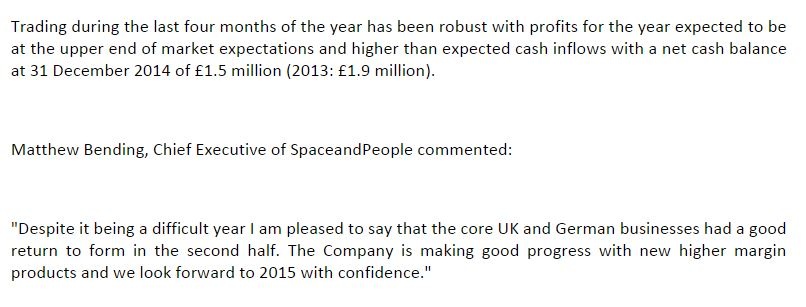

Trading update - this niche marketing company, which manages retail & promotional space in shopping malls & other open spaces (e.g. railway stations) in the UK & Germany mainly, certainly had an annus horribilis in 2014, with two profit warnings, and a severe drop in the share price. I covered it extensively here in the past, click here for my previous articles.

Looking at the chart, the shares have been bottoming out since Sep 2014, having lost two thirds of their value from the peak in early 2014 (when profit expectations were much higher).

Things sound a lot more positive today, with the update saying;

"Upper end of market expectations" is the key phrase above. Although obviously market expectations are now much lower than they were a year ago. The range is, I believe, £0.8m to £1.0m forecast profit for 2014, pre-exceptionals (some redundancy costs mainly).

Net cash - reported at £1.5m - whilst probably a seasonal peak, it's not bad for a profitable, dividend paying company that is only capitalised at £11.1m, and that's factoring in today's share price rise.

I understand there was never any issue with solvency here, which is one of the good things about screening for adequate financial strength - you don't have to worry about companies going bust, even if something goes wrong with trading.

Forecasting - the company has learned from its experiences in 2014, when a series of problems with contracts - not renewing, being delayed, etc, lead to the original profit forecast turning out to be far too optimistic. This was a new issue for the company, as in the past it had won the business it expected to win.

Going forwards therefore, the company now has a policy of guiding the market to a base case scenario for profits, on existing levels of business. The pipeline of new business is now treated as icing on the cake. Therefore, we should from now on receive very conservative profit forecasts, and see those gradually edge upwards as the year goes on.

Strategy - as part of the recovery process from its problems in 2014, SAL had a refresh of the board, bringing in new Non-Execs who have relevant (and considerable) experience. This has helped refocus strategy on the core businesses in UK/Europe, and in particular on generating new, higher margin revenues.

New promotional kiosks have been designed and trialed, which considerably broaden SAL's appeal to its shopping mall landlord clients. Instead of just offering kiosks for third parties to sell things like mobile phone covers, jewellery, etc., SAL will soon be offering promotional kiosks that are rented out on a weekly basis to companies wishing a professional-looking stand in a very high footfall area. So think charities, utility companies, any company that wants interaction with the public on a short term basis.

The trial has gone well, and it's now a roll-out over the next two years. Edison have put out a note today with more detail - it's on their website. I think this additional, high margin business, augurs well for future profitability. It's good to see SAL's business model evolve, and the company is innovative in outlook.

My opinion - I don't believe in adopting a standard policy for profit warnings. Some people do, and they immediately ditch shares which disappoint. That works for some people, and it's a strategy I respect, but it's not for me. It's important not to let the emotional pain of a loss from a profit warning cloud your judgment. I try to get over the emotional response as quickly as possible (within a few minutes), and not dwell on it. Draw a line under it mentally, and then look at the current position with a cool head.

I see every profit warning as being a unique situation which needs properly investigating. So it's a question of crunching the numbers, untangling the Directorspeak, and forming a view on essentially whether the company is a good company that has run into temporary problems and can recover, or whether it's a bad company that is permanently on the wane.

My view, after doing a lot of digging, was that SAL would almost certainly recover from the problems in 2014. That it would take a bit of time, but it would have been a mistake to throw out the shares when sentiment was negative, and the valuation extremely low.

I'm looking forward to seeing management again after the results are published in Mar 2015. In my opinion, they've got their mojo back, and are looking forwards to growing the business, rather than firefighting problems (which have now been resolved).

We might well see a headwind on the share price from stale bulls wanting to exit, so it wouldn't surprise me to see the shares give back some of today's big rise, but the negative trend is now clearly over, and I am looking forward to hopefully getting my money back here, with a timescale of c.1 year.

Robinson (LON:RBN)

Share price: 150p (down 13% today)

No. shares: 17.7m

Market Cap: £26.6m

Trading update - sounds fine for 2014, with profits in line, but a wobbly outlook;

The words "much more challenging outlook" have rattled me, as that doesn't sound like a temporary issue.

Valuation - broker consensus is 12.8p EPS for 2014, so that looks in the bag, for a PER of 11.7. The outlook isn't good, but note the last sentence says that EPS should still rise in 2015, but not by how much.

Bear in mind also that this company has surplus property assets, so there's hidden value in the balance sheet from that, although I don't recall the figures. Update: I've just checked the 2013 Annual Report, and note 10 says that the market value of surplus property is est. £2.7m, so not particularly material, and less than the company's net debt.

I did more detail on the figures after the interims, in my report here of 20 Aug 2014.

My opinion - I did have a small position in this share, but have decided to ditch it today. Packaging is surely an area where margins are going to come under increasing pressure, as the supermarkets squeeze harder & harder? With an uncertain outlook, I'd say the risk of another profit warning is high. Looking at Robinson's Annual Report, most of the pictures of their products are food packaging. So I think they will be mercilessly squeezed on price by their customers, in a supermarket price war situation that is likely to continue permanently.

This is an extremely illiquid share too, and I've only been able to trade 1,000 shares at a time, so £1.5k, which makes it pointless getting involved really, with a nasty 10p bid/offer spread at most times too. I might revisit it once the level of sustainable trading has become more clear, but it's not a sector that appeals.

updating, pls refresh page periodically

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.