Hello, it's Paul & Jack with the SCVR -

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda -

Castings (LON:CGS) - good H1 recovery but various headwinds mean the company is struggling to translate a strong pipeline as vehicle customers suffer from the semiconductor shortage. Castings looks like a sensibly run business with a strong balance sheet, so it should be able to navigate these conditions, but profitable growth has been lacking for some time.

Works Co Uk (LON:WRKS) - a better than expected revenue performance offsets rising freight costs, leaving the group on course to meet original expectations for FY22. There's a huge store estate here given the small market cap and a possible value opportunity given the valuation, but I'm unsure of the fundamental profitability of the business model.

Avon Protection (LON:AVON) - commiserations to holders after a brutal 40%+ share price drop this morning. The affected business area accounts for c12% of forecast FY22 revenue so there is a chance the reaction is overdone but shifts in sentiment like this can take a long time to undo, so I don't think there's any rush for onlookers to jump in. Final results now expected in December.

.

Jack’s section

Castings (LON:CGS)

Share price: 370p (+0.54%)

Shares in issue: 43,632,068

Market cap: £161.4m

This is an iron casting and machining group. It’s got a strong balance sheet and invests in its businesses plus, as we see today, management is admirably upfront about its challenges. Growth has been a bit of an issue, but it seems sensibly run so I can see why some longer term investors might gravitate towards it.

Highlights:

- Sales +67.1% to £69.8m,

- Gross profit +170.6% to £13.9m,

- Operating profit up from a loss of -£678k to +£5.4m,

- Diluted earnings per share up from a loss of -1.16p to +10.03p,

- Interim dividend of 3.66p.

These figures look like a strong recovery from Covid disruption but Castings says that, after a strong start to the period, supply chain disruption and the semiconductor shortage means that commercial vehicle customers are struggling to build enough heavy trucks to meet demand.

With the OEMs having to reduce truck build rates to below their order intake levels, group sales were reduced from the last two weeks of June and into the second quarter. This segment accounts for 70% of group revenue.

This dynamic became more evident in the last two weeks of June and into Q2. Castings says ‘Whilst forward demand schedules from our customers have remained high throughout the period, the conversion rate to actual sales has been significantly below what we would normally expect.’ While the group has increased inventory and production levels, it has been further hampered by labour recruitment difficulties.

In fact, Castings had to close the machining business for a week at the end of September.

Raw material prices have continued to rise throughout the period which, with the time lag in the associated sales price increase, has continued to put pressure on margins.

Foundry operations - output here was up 69% to 24,300 tonnes and revenue grew by 68% to £68.1m. Profit increased from £0.8m to £5.3m, although margins have been affected by fluctuating demand and rising raw material prices. Investment continues here.

Machining operations - CNC Speedwell revenue grew by 32% to £1.6m, and a profit of £0.1m is reported (H1 2020: -£2.1m). Significantly lower levels of demand in Q2 had a ‘particularly negative’ impact on results. Again, the company continues to invest here (£0.3m in the period).

Balance sheet - looks solid, with £34.6m of cash compared to current liabilities of £24.5m. Net tangible assets of £128.8m and no debt, so that’s a strong pass.

Conclusion

There are two separate points here. Number one, there has been a very encouraging recovery from Covid disruption. Number two, business is now being impacted by post-Covid disruption. Assuming these headwinds reduce at some point, then the strong balance sheet should see Castings through and the company and its sites appear well invested. How the share price reacts in the short term is another matter.

The group says raw materials prices have increased, impacting margins. Sales reduced in the last two weeks of June and into Q2 as vehicle customers struggle to source parts, the strong pipeline is currently difficult to convert, and labour scarcity means its machining business had to close for a week.

You can’t say this company doesn’t say it how it is. Putting those challenges to one side for a second, the H1 figures are actually very positive and margins improved in the period. How much impact the current dynamics have on those recovered margins remains to be seen, which makes the situation tricky to assess.

In the comments below, Yellowstone points to a webinar today at midday here. I’m sure management will give more colour at that point.

For now, the pipeline is busy and the balance sheet is strong, so the outlook could be worse for this particular company. It looks like it’s run sensibly and management pulls no punches. But it’s been struggling for growth for some time and this latest update suggests there are currently more attractive opportunities out there, in my view.

Perhaps if, in six months time, the share price has come down a bit and conditions begin to improve then there could be a good value trade here, but I’d want a cheaper price (and more visibility on the trading conditions) given that profits have been coming down for some time.

Works Co Uk (LON:WRKS)

Share price: 55p (-3.51%)

Shares in issue: 62,500,000

Market cap: £34.4m

Works is a multi-channel retailer of gifts, arts, crafts, and some other faddy things like fidget spinners. The group has a surprisingly large estate of more than 500 stores, which is obviously a lot for a £34m market cap company.

The shares have rerated and are of interest to the community, which perhaps senses a continued rerating as customers head back to shops.

The upcoming Christmas period is extremely important for retailers like Works, so a good performance over the next couple of months could make a big difference. Brokers rate it a strong buy, but Works has had a rough start to listed life and has disappointed in the past.

It has generated low margins in the past, so for all its revenue and store count, turning a profit appears to be a challenge. I think low margin businesses are particularly vulnerable with cost inflation and supply chain disruption running rampant.

Overall, taking into account the stronger than expected trading during H1 FY22 and the higher freight costs and, assuming that our strategies to ensure the availability of stock to customers in the lead up to Christmas continue to be successful, the Board anticipates that the full year result for FY22 will be in line with its original expectations.

Trading has been stronger than expected, with a two-year LFL sales up 14.5% and total two-year sales growth of 17.9%. Online sales were close to double those in the comparable FY20 period. The board consequently expects full year results to be in line with original expectations, despite higher freight costs.

Net cash (excluding leases) improved by £17m to £17.8m ahead of the peak trading period. This improvement includes favourable timing differences of approximately £10, which should unwind. The group has managed its supply chain issues and expects to have adequate stock levels heading into Christmas.

The new strategy outlined in July 2021 includes de-emphasising new store openings and focusing on profitable digital growth and driving improvements through the existing store estate. The product range has been improved, as has stock management and space management in stores.

Three new stores were opened, five were closed, and four were relocated. That leaves the group trading from some 526 stores at the end of H1 FY22.

Consumer demand has also been strong, perhaps due to staycations and a strong 'back to school' performance. There are also signs that customers are shopping early for Christmas and, ‘whilst the impact of this on H1 FY22 was small, we hope it is a positive indicator that strong demand will continue into the peak Christmas trading period.’

Conclusion

Online sales have doubled but no actual numbers are given. Two-year like-for-likes are up by 14.5%, which is encouraging. The company was struggling before Covid though, and I’m not sure about the longer term prospects for this concept. The margins have just been too low in the past.

The shares still remain well below the IPO level.

With a single digit forecast PER and a trailing twelve month price to free cash flow multiple of just 1.3x, there does seem to be value here. But I’m just not sure about the economics of the enterprise.

There’s not enough information here to sway me one way or the other, although if consensus forecasts are met, then there is a value case to be made. Perhaps a continued rerating if the backdrop remains favourable, but longer term I’m not so sure of the prospects. The poor historical operating margins put me off.

Avon Protection (LON:AVON)

Share price: 1,094.27p (-42.62%)

Shares in issue: 31,023,292

Market cap: £339.5m

I’m surprised to see this one so firmly back in SCVR territory. Not long ago, Avon was touted as a particularly high quality growth company and it had the valuation premium to match. Towards the end of last year the shares were trading at c4,600p, making for a market cap of £1.4bn.

Today, less than a year later, they are some 76% down on that level. It just goes to show how quickly perceptions can change. Commiserations to holders. We all end up seeing something like this at some point, unless you’re disciplined with your stop losses.

Avon retains its high Quality Rank (currently 87) but there has been a slightly alarming deterioration in margins.

The shares are down by more than 40% this morning so I’m curious about this announcement.

Following the contract awards for the U.S. Defense Logistics Agency ("DLA") Enhanced Small Arms Protective Inserts ("ESAPI") and U.S. Army Vital Torso Protection ("VTP") ESAPI body armor plates, we have been engaged with our customers to complete the necessary product approval processes. Disappointingly, the VTP ESAPI plates have encountered a failure in First Article Testing which will significantly delay the likely approval timetable for this product.

Separately, we have experienced further delays in obtaining final product approvals for the DLA ESAPI body armor plates, with approvals for this product now expected in the second quarter of our financial year ending 30 September 2022 ("FY22").

This has led to a strategic review of the recently acquired body armour business.

The FY22 revenue guidance included approximately $40m of body armor revenue but clearly this is no longer the case. Body armour revenue ‘in FY22 and beyond’ will be significantly reduced.

Avon’s respiratory protection and helmet product portfolios are unaffected.

This also leads to a delay in FY21 results ‘to allow for a review of the carrying value of the assets related to the body armor business and the additional audit work arising from this post balance sheet event.’ The revised results date is expected to be in December.

Conclusion

FY22 revenue was expected to be £239m, so the affected $40m represents about 12% of that. It’s a brutal reaction today and it pays, if possible, to analyse the developments objectively as such reactions can overshoot. Still, such severe drops can weigh on sentiment for some time, so I don’t think there’s any rush to come to a conclusion on the revised prospects.

The group had been ramping up production of its body armour products, so it feels like this failed test has come quite late on in the process. Unfortunately, that raises some questions around testing rigour and due diligence on the products of the acquired business.

BlackRock and two directors were buying reasonable amounts of stock as recently as 24th September, and the most recent broker research note is subtitled ‘Confirming the growth path’, so it looks like the severity of these events has taken everyone by surprise.

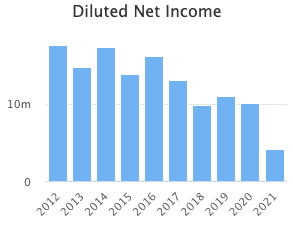

This is a useful case study in what can go wrong with High Flyers when the business prospects begin to diverge from market sentiment. We can see that diluted normalised EPS has been struggling to push on as far back as FY18 even though the share price went from strength to strength in that period.

With the benefit of hindsight, problems have been growing ever since 3M was acquired in early 2020 and it seems like the bad news has leaked out over quite a long period of time. That makes me wary, especially when coupled with a lack of meaningful growth over the past few years.

On the one hand, the fall could be overdone but on the other, selling the old milk business and committing to what now looks to be faulty product lines could prove to be a drastic strategic misstep. As such, I’m not going near the shares right now until we have more detail in the delayed final results.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.