Morning all, it's just Paul here, with the SCVR for Friday.

Today's report is now finished.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to cover trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda -

Paul's Section:

Best Of The Best (LON:BOTB) (I hold) - Brutal profit warning, with profit guidance for FY 04/2022 lowered by 62% to c.53p. Expect a big fall in the share price today.

Mccoll's Retail (LON:MCLS) (I will hold - applied for placing) - equity fundraising at 20p announced last night, with interim results. This is a special situation - financially distressed and high risk. However, I like the turnaround plan, to re-brand stores as Morrisons Daily, which has worked well in early trials.

Venture Life (LON:VLG) - profit warning, and broker forecasts reduced. Chinese distribution deal sounds like it could be dead in the water. Too much uncertainty & too many moving parts for my liking.

Paul’s Section

Best Of The Best (LON:BOTB)

(I hold)

1525p (pre market open) - market cap £146m

I’ll rush to get this out before 8am, as this share is widely held by readers (and by me!)

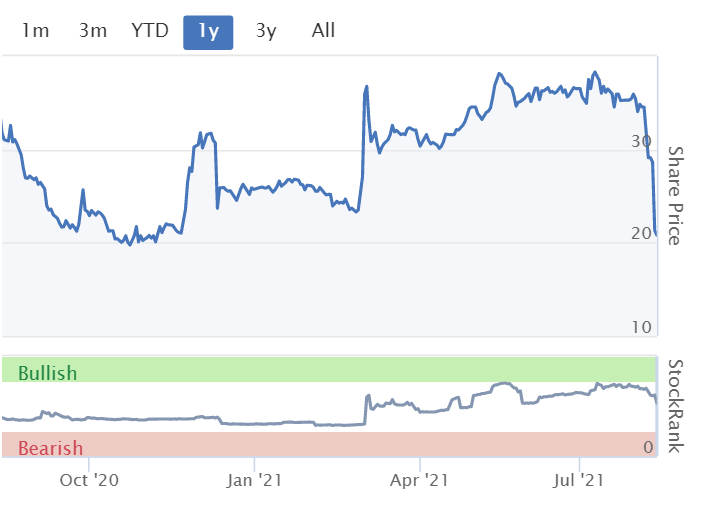

Background - briefly is that this supercars competition company went entirely online (it started in UK airports), and started delivering stellar growth. The shares were a big multibagger. However, more recently the gloss came off BOTB shares when management sold about £60m of shares in a secondary placing at £24 per share, after a lengthy period when the company was up for sale. About 2 months later, a disappointing trading update hit the share price, which had settled around £15.

Trading Update (profit warning) - today

Best of the Best PLC (LSE: BOTB), the online organiser of weekly competitions to win cars and other lifestyle prizes, provides the following trading update for the 15 weeks ended 8 August 2021.

This is the start of FY 04/ 2022.

The company had previously (on 16 June 2021) said that trading had softened, since lockdown ended on 12 April 2021.

Guidance slashed - a lengthy explanation is given, but the key point, and it’s horrible, is that profit for FY 04/2022 is now expected to be 57% down on FY 04/2021.

Actual EPS last year (FY 04/2021) - 122.5p

New guidance for this year (FY 04/2022) - 52.7p

Finncap’s last note was forecasting 142.4p EPS for this year. The RNS says new guidance is 62% below market forecasts (there’s only one forecast, I think), which arrives at 54.1p, very close to the 52.7p figure above.

EDIT: revised forecasts have just come through from Finncap, as follows;

This year 53.3p

Next year 64.1p

Its revised target price is 1400p - which is certainly not realistic in the short term, but could come about if trading recovers in due course, who knows? It seems that BOTB is a lot more unpredictable than we realised.

What PER to use? I'm leaning towards 15-20, implying a valuation of 800-1066p, that's what I think it's now worth for the time being. Longer term, who knows, that depends on whether trading recovers or not.

PatrickL makes a very good point in the comments below, that revenue is forecast to only drop from £45.7m to £40.0m (still more than double pre-covid level), but it's the operational gearing that's the killer here. that leads to a forecast 57% drop in profitability.

End of edit.

Cash balances - over £6m at 12 August 2021, so no issues with solvency or liquidity.

What’s gone wrong? A lengthy explanation is given, but it boils down to reduced customer demand (people spending money on other things since lockdown ended), and higher marketing rates resulting in lower marketing activity.

My opinion - this is a stinker, much worse than I was expecting.

Unfortunately, I think the share price probably halves today, to £7-8 (am writing this at 07:38). I've already decided there's no point in trying to sell, because there won't be any buyers until it's found a level much lower, this share tends to be very illiquid.

Assume the brace position.

What a grim chart. I'm astonished that it has unravelled so quickly. All the numbers looked so good just a few months ago.

.

Mccoll's Retail (LON:MCLS)

(I’ve applied for a small amount in the placing)

Share price: 20.75p

No. shares: 115.3m now, 290.3m after placing/open offer (assuming full take up)

Market cap: £24m before, £60m after fundraise

Fundraising - many thanks to my friend William who flagged up this fundraising to me last night, which was announced at 15:50. So after winding down for the day, I cranked back up again and spent yesterday evening going through the numbers.

Here are my notes -

- Placing to raise £30m, 150m new shares - book build successful, announced this morning.

- Priced at 20p - a deep discount to the share price of c.35p before news leaked

- Open Offer for up to 25m new shares to existing holders

- Share count will rise by 152% to 290.m - so a highly dilutive fundraise

- Purpose - reduce gearing, and fund rollout of site re-branding to Morrisons Daily

- CEO putting in £3m, a serious amount of money, which I like a lot

Interim results - not good, the balance sheet looks really weak, hideous actually, with negative NTAV of £(144)m. Although supermarkets do have favourable working capital - i.e. receiving customers cash before having to pay the suppliers. This £35m fundraise will only eliminate about a quarter of the balance sheet NTAV deficit, so further balance sheet repair is needed. Net debt is £111m (excl. leases) which is too high. Covenants are tight. So this fundraise is from a position of financial distress.

Like for like sales are positive +1.0% for H1, on top of +8.3% in the prior year, so some signs of life there.

Supply chain disruption sounds like a growing problem, shortage of drivers, could derail H2 trading, the company says.

Margins fell, but have since partially recovered.

Morrisons deal - this is the interesting bit. It’s a very odd situation, but McColl’s has started re-branding some of its sites to Morrisons Daily, and it’s working well. This is what makes this share potentially interesting. Each rebranded site costs about £60k + £30k for more fridges, which enables the format to move away from newsagent/booze& fags led, and become fresh food-led, with prices not much more than supermarket. These are local, convenience stores, which are being turned into mini Morrisons. What’s the betting then, that Morrisons might buy MCLS at some point? That seems the logical end game.

Wholesale supply agreement with Morrisons runs until Jan 2027.

Rebranded sites are generating a good uplift in sales & profits, with a fairly good 2-3 year payback - so this strategy looks worth pursuing.

My opinion - this probably won’t be the last fundraising - MCLS says more funds will be needed, and the balance sheet looks awful to me.

I went through the interim results, also published last night, and they’re not good. EBITDA gets swallowed up by heavy finance charges, and £1.8m p.a. pension deficit recovery payments. Plus of course business rates will be kicking back in again, which saved £5.8m just in H1, a material additional cost coming back in. So the company is facing cost headwinds.

I see this as a high risk, special situation. However, the upside from converting stores to Morrisons Daily is fairly clear. The banks have relaxed a bit, as part of this deal, so potential insolvency looks less of a risk.

In my view, there’s potential upside here to maybe 40-60p if the bull case plays out, that’s my target, based on analyst forecast of profitability once the sites are refitted to become Morrisons Daily. The strategy looks sensible to me, with proven uplifts in performance from converted shops. The CEO putting in £3m personally is another big sign of confidence in the strategy (mgt already owns 10.5% before the fundraise).

Overall, I like the occasional punt, where there’s a logical turnaround plan. Hence I rather impulsively rang my broker last night after the market had closed, asking him to see if he could get me into the 20p placing, not really expecting anything to come of it. Anyway, this morning I got a message to say I’d received 70% of my order. So in a couple of weeks, I’ll end up being a MCLS shareholder - hence why that needs to be disclosed here, even though I don’t technically actually own any yet.

Quite an interesting special situation, but now its funding position is somewhat improved, and the share price has plunged, I think it’s a more attractive investment idea than before. Definitely not for widows and orphans though.

As we saw with Revolution Bars (LON:RBG) (I hold), small caps that need to raise cash from a position of weakness, can result in brutal dilution & losses for existing holders. Hence why it’s usually best to avoid these type of stressed situations until after the new funds have been raised and hence risk reduced.

There are lots more companies out there which obviously have overly indebted balance sheets and need to raise fresh funding. They’re very high risk, and people need to wake up to how risky some of the shares in your portfolios might be. It only takes a previously co-operative bank manager to have a fit, and demand an immediate fundraise, and before you know it, the share price goes into freefall.

Institutions don’t seem as willing to support fundraises now, and if it’s a challenging situation like this one, then they demand a deep discount as the price for their support. Existing holders then have a permanent loss, unlikely to be recouped, unless you greatly increase your position size at the new lows, which you may not want to. These things are very tricky, but can be easily avoided by just focusing on the balance sheet position, and avoiding companies with a funding need.

.

.

Venture Life (LON:VLG)

74.7p (down 25%, at 10:44) - mkt cap £94m

Trading Update and Progress on Recent Acquisitions (profit warning)

Oh crumbs, another profit warning, bad luck to holders here. You can’t avoid all profit warnings, because the future is inherently unpredictable, so there’s no point in getting emotional about it. Accept this as part of the process - some investments do well, others disappoint. We have to take it all in our stride, and crucially learn from each mistake, and try to spot similar things in advance in future. Easier said than done, I know!

Venture Life (AIM: VLG), a leader in developing, manufacturing and commercialising products for the self-care market, provides an update on trading and the acquisitions of BBI Healthcare Limited ("BBI") announced on 7 June 2021 and the Helsinn Integrative Care Portfolio ("HICP") announced on 6 August 2021.

H1 revenues (Jan-June 2021) expected to be £13.8m, down 18% on H1 2020

Reasons? “Much lower sales of hand sanitising gel”, and reduced sales to Chinese partner

Everything else showed overall growth of +9%

Covid had an impact in H1, but “encouraging signs” of recovery, esp in UK retail

Acquisition of BBI added £1.1m to H1 sales, despite only being c.1 month from acquisition - sounds like this will be material to full year results then, if we annualise it to c.£13m revenues. This was a big acquisition, costing up to £36m, so should materially boost future performance I imagine. VLG says the acquisition is “progressing well”, cost synergies extended.

HSG - sales dropped to almost nothing in H1, and “unlikely to be anywhere near the 2020 levels in the future”

Dentyl sales to Chinese partner also negligible, at just £0.2m in H1 (see below)

There’s more detail in the trading update, which I won’t get into, because I've already lost interest in this share.

Chinese partner - this sounds pretty bad to me - it might be wise to remove any contribution from this sales channel from forecasts, to be on the safe side -

In addition, whilst we have also seen some sales to our partner for Dentyl in China during the first half of 2021 (£0.2 million vs £2.3 million in H1 2020) as well as the continued paying down of a significant part of their debtor balance, sales out to this partner so far this year have not picked up as we had expected. The partner is still suffering from the effects of the Covid impact in 2020, and is not yet taking new product at the rate anticipated when the agreement with them was signed in 2020 or indeed in line with their communication earlier in 2021, which has likely been exacerbated by the significantly increased shipping cost to China now being seen.

Whilst we expect more sales to this partner in 2021, and are hopeful that sales this year can at least match the full year 2020 revenues to this partner, we are exploring all options to maximise the value of these assets in China, where demand for the product has been good historically.

Order book -

The order book for the business (excluding any orders for the China partner and the acquired BBI business) is higher than at the same time last year, indicating good growth in the core business during another extended period of lockdown across many markets.

Outlook -

The second half will have a more meaningful contribution from the new acquisitions and the business is well placed to benefit from the confidence that can be seen as the UK and global economies recover from the impact of Covid. The Board is excited by the growth opportunities available to the Group and looks forward to reporting further delivery on its strategy…

The two recent acquisitions meaningfully increase our expected profitability and cash generation in 2021, where we will receive the benefit of the two new acquisitions in the second half year. 2022 will see us receive the full year benefit of the new acquisitions and, along with the continued growth of our existing business, enables us to look forward to significant growth in revenues and profitability next year. At the same time, we have the resources to pursue additional earnings enhancing acquisitions to accelerate this growth and the Board looks forward to the future with confidence."

My opinion - too many moving parts here, for me to be able to form a view. The recent acquisitions are very material to the overall size of the group, so a lot hinges on how they perform.

As mentioned before, I didn’t like management disposing of about £7m-worth of shares at 90p, at the same time as raising fresh capital in Dec 2020.

Historically VLG has made very little profit, and the one year it did (2020) seems to have been boosted by some one-offs, e.g. hand gel. Therefore the valuation now rests largely on the recent acquisitions, and broker forecasts, which have been reduced today a fair bit. 2021 fc EPS comes down from 4.5p to 2.5p, then a big jump to 4.6p in 2022 - how likely is that to be achieved? No idea!

Overall then, I’m neutral, because there's too much guesswork involved in predicting future profitability.

Overall the shares have gone sideways for the last year, so not a disaster by any means.

.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.