Good morning from Paul & Roland.

Agenda -

Paul's Section:

Essensys (LON:ESYS) - interim results yesterday triggered a 36% rise in share price. Interim figures look poor to me, with revenue growth almost stalled. However, the balance sheet is strong (for now anyway, it intends burning through the whole cash pile in the next 2 years). Outlook comments indicate growth is accelerating now people are returning to offices. However, forecasts show it needs to more than double revenues, and still won't reach breakeven. Hence this looks a high risk business model, and shares are just a punt at this stage.

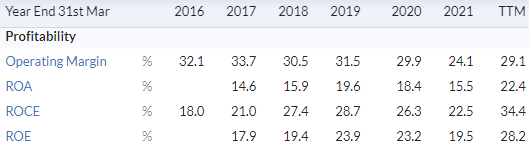

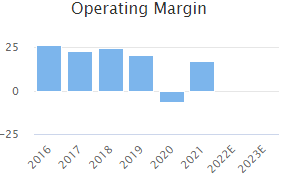

Solid State (LON:SOLI) - an impressive year end update, with the latest in a series of profit upgrades. Record order book gives comfort for the new year just started. Cost headwinds seem to be absorbed within increased revenues. 2 acquisitions have performed well. Valuation looks about right to me.

Procook (LON:PROC) - my first look at this recent IPO, which retails kitchenware online and in c.50 UK stores. I like what I see! Valuation probably still too high though.

Roland's Section:

Record (LON:REC) - this specialist currency management business saw a slowdown in AUME growth last year, but appears to be benefiting from rising interest rates. I can see some attractions, but I wonder if the business model may face tougher competition than in the past.

Ibstock (LON:IBST) - this FTSE 250 brickmaker upgraded its 2022 guidance yesterday following a strong Q1. The company seems to be on a sound footing and the stock looks reasonably valued, but I’m wary about cyclical risks and might prefer to focus on the top performers in this sector.

Brickability (LON:BRCK) - This fast-growing building materials group now expects to report FY22 EBITDA 19% ahead of previous guidance. I’m encouraged by the presence of owner management and this group’s strong progress since its 2019 IPO. Although I can see some cyclical risks, I have a favourable impression of the business.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Essensys (LON:ESYS)

Shares up 36% yesterday to 115p

Market cap £74m

For the 6 months ended 31 Jan 2022.

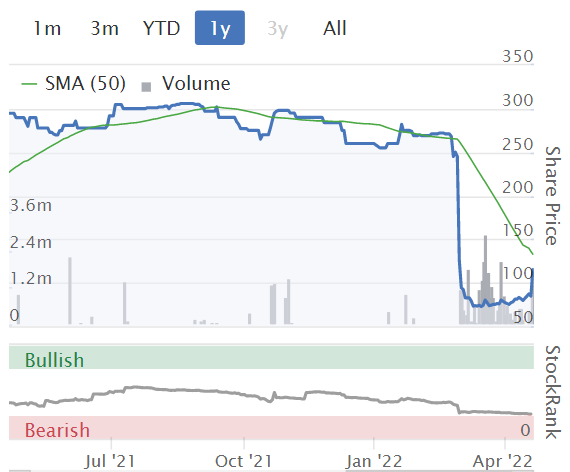

We had a deluge of company news yesterday, and this one slipped through the net. We try to report on big movers, so as there’s nothing of interest today, I’ll look back at a few big movers we missed yesterday, starting with this SaaS company focused on “delivering digitally enabled buildings and spaces”. It’s not at all clear to me from Essensys website what the company does, and how it’s better than other IT services.

Essensys floated on AIM in May 2019. I don’t seem to have looked at it before (although it looks vaguely familiar to me as a jam tomorrow, heavily loss-making company that is one of the worst places to invest at the moment, as these things have heavily de-rated), but Jack reviewed its FY 7/2021 trading update here in Aug 2021, and concluded the valuation “seems steep” at 315p. Good work Jack, as the share price has since collapsed, bottoming out recently at c.75p.

As you can see from the chart below, something awful happened on 1 March 2022 - a profit warning, saying that growth had slowed, a client was lost unexpectedly, and providing lowered FY 7/2022 guidance of £23.5m revenues, and a £(7)m EBITDA loss. No wonder the share price tanked! Although it also talked of a strong pipeline.

.

.

Interim Results

Published yesterday.

Revenue growth has stalled to low single digits, at only £10.9m for H1. It’s nearly all recurring revenue though.

H1 loss before tax of £(4.7)m - pretty awful.

By my calculations, revenues would need to rise by c.70%, just to reach breakeven! Broker research shows it's worse than that - even a doubling of current revenues to £42.3m in FY 7/2024 would still result in adj PBT of a £(6.1)m loss, and all the cash pile having been burned up.

Capitalised R&D of £1.5m in H1, so remember to deduct this cost from adj EBITDA of £(2.9)m, which ignores it.

It’s pleasing to see the software development moving to the UK -

As previously reported, the Group continues to invest heavily in product development. Increasingly these costs are borne in the UK following a decision to increase the UK based development team and reduce the size of the Group's outsourced offshore development centre.

Balance sheet - is strong (for now), as the company did a big £33m equity fundraise in July 2021, and is sitting on a £30.5m cash pile - although it’s burning through that cash due to ongoing losses, and increased overheads. So it's only expected to last for 2 years - a scary rate of cash burn that looks reckless to me.

Receivables look high, at £6.1m, compared with £10.9m revenues in H1, suggesting the customers are not in a rush to pay - which might indicate maybe some disputed invoices? It’s a question to ask management, if any readers speak to them.

So far, so bad. These H1 numbers definitely don’t justify any increase in share price, so it must be the outlook comments that excited people yesterday, to chase up the share price by 36%. Or just day traders playing around, which we're seeing a lot of at the moment - spikes up in price that often don't stick.

Outlook - says that growth is accelerating again.

Pipeline up 23% since Jan 2022.

Caution expressed over inflationary cost pressures.

Structural growth drivers returning, as workers come back into offices after covid.

Concluding -

The Group continues to expect to meet FY22 consensus market expectations and remains confident in the longer-term structural growth opportunity

Webinar today - There’s a webinar today at 11am on InvestorMeetCompany. I tend to watch the recordings over the weekend.

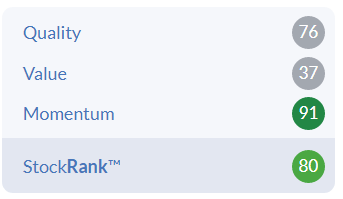

My opinion - the current £74m market cap seems a lot more realistic than when we last looked, at around £200m. Particularly as the company has 41% of its market cap sitting on the balance sheet in cash - hence fully funded to expand, although depleting its cash rapidly along the way, with continued heavy losses expected as overheads are cranked up (expanded sales teams, etc).

If you’re tempted to buy this share, do first have a look at Singers research notes, available on Research Tree. This shows continuing heavy losses, despite forecast revenues almost doubling by FY 7/2024, and the cash pile completely gone by the end of that year.

That looks a scary investment proposition to me! It looks as if Essensys has much too heavy overheads, which swallow up the strong revenue growth anticipated. It doesn’t even reach profitability with revenues almost doubling to £42.3m in FY 7/2024 - which requires a faster growth rate than has been achieved before.

Too risky for me. I think readers would need to properly research the software, compare it to the competition, talk to users of the software, etc, to be sure that the upside is strong enough to justify paying £74m for a heavily loss-making company, which intends burning through its cash pile over the next 2 years in an attempt to more than double in size, and still be loss-making at the end of it! That doesn’t strike me as a very good business model.

.

Solid State (LON:SOLI)

1110p (down c.3% at 09:43 today), up 13% yesterday

Market cap £84m

Solid State plc (AIM: SOLI), the specialist value added component supplier and design-in manufacturer of computing, power, and communications products, announces a trading update for the 12 months ended 31 March 2022 (the "Period" or "FY22").

This share caught my eye yesterday, with a decent move up +13% on a positive trading update. It’s slipping back a bit today, but on negligible volume reported so far (remember bigger trades are allowed delayed reporting, which is why prices often move in a way which seems strange to people following the reported trades - you’re only seeing a partial picture of small retail trades in real time. The bigger trades might be being worked in the background).

SOLI shares have held up very well in the last 6 months, a period when many small caps have relentlessly dropped due to macro concerns. Is SOLI a shining star, or an accident waiting to happen?

.

Trading update - this looks excellent! -

Following an exceptionally strong finish to the Period, the Company expects to announce record results with revenues for FY22 of approximately £85m (2021: £66.3m) up 28% over the prior year, and adjusted profit before tax for the Period of approximately £7.2m (2021: £5.4m) up 33%; both ahead of recently upgraded consensus expectations1.

The like for like open orderbook at 31 March 2022 is up 106% over the prior year at a record £85.5m (31 March 2021: £41.5m).

Here’s the very clear footnote below - why can’t all companies provide these, it makes life so much easier for investors, and the clarity makes us more likely to want to buy the shares.

1 Analysts from brokers WH Ireland Limited, finnCap Limited, and Edison Investment Research Limited, provide equity research on Solid State, and the Company considers the average of their research forecasts to represent market expectations, being, for Solid State's 2021/22 financial year, revenue of £80m, and adjusted profit before tax* of £6.5m.

Note that 28%revenue growth is 8% organic, the rest from acquisitions.

That’s a 6.3% beat vs expectations on revenues, and a 10.8% beat on adj PBT. Hence yesterday’s +13% share price rise looks logical.

To beat estimates at the end of the financial year is impressive indeed, especially when the context is a series of upgrades to estimates earlier in the year -

.

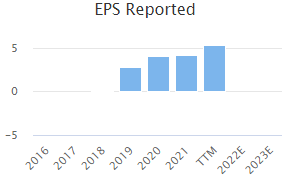

Broker updates - Edison (which is effectively from SOLI, as it’s commissioned research) estimates EPS of 71.2p for FY 3/2022, and similar for next year - which assumes that £5.0m higher revenues are mainly absorbed by cost increases.

That gives a current PER of 15.6 - which doesn’t strike me as cheap in a very cautious small caps market. Priced about right, perhaps? (assuming that performance can be maintained).

Cyanconnode Holdings (LON:CYAN) is mentioned as a major customer, which makes me nervous because it has a history of being loss-making, and repeatedly raising cash. Checking its last accounts, CYAN is small, still loss-making, with a weak balance sheet (unusually high debtors looks a problem), and recently did a £2m placing. So a blue chip customer, it is definitely not! Hence I hope SOLI’s CFO is insisting on pro forma invoicing only (i.e. payment up-front), or trade credit insurance, as that could be a higher risk receivable otherwise.

All sales are a gift, until they’re paid for, remember!

Acquisitions - SOLI seems to be good at making acquisitions, with “notable contributions” from Willow Technologies and Active Silicon, and both “performed ahead of management’s expectations since their acquisition in March 2021”.

Supply chain & inflation - this partially reassures, but I’ve heard from IT companies that lead times on electronic components are currently getting worse, so problems in supply chains is still a considerable risk I’d say -

As previously reported, Solid State has navigated the long-term supply chain challenges associated with semiconductor shortages through careful inventory management and pro-active engagement with customers to manage order scheduling.

Given the success of this experience, the Group is taking a similar approach to the management of input cost pressures and inflationary effects of recent global events, continuing to manage the ongoing supply challenges and help mitigate potential margin erosion risks. This is enabling the Group to share the risk with its customers and pass on some of the cost increases.

Only some, not all of the cost increases passed on.

Inventories have been increased, which is a sensible approach.

Outlook - there are various comments scattered through the commentary, but this is the concluding paragraph -

Solid State continues to deliver on its organic growth strategy through the targeting of structural growth markets and remains focused on complementary acquisition opportunities. The record open order book and trading momentum underpin the near-term prospects and give the Directors optimism for the future.

My opinion - this is an impressive update. The share price looks about right to me. A PER of 15.6 would have seemed cheap a year ago, but with all the current macro worries, it’s difficult to justify why I would want to pay any more than that right now.

A strong order book, good acquisitions, and seemingly having the supply chain under control, would probably give me enough confidence to continue holding, if I were an existing shareholder.

.

Procook (LON:PROC)

121p

Market cap £132m

This company floated on the UK main market in Nov 2021, at 145p, for a £158m market cap.

It’s only down 17% since then, quite good for a recent IPO!

Existing family shareholders cashed out £39.7m at the IPO.

Here is the Prospectus, which I’m having a quick initial look through now (it only takes a few minutes so skim read the key sections, and ignore everything else at first)

Here’s a 5 minute video introduction from ProCook, which sells kitchen products, pots & pans, knives, and other kitchen products, online and from about 50 UK stores.

Shareholder structure is striking - it’s controlled by the O’Neill family, with a tiny free float. They owned 100% pre-IPO.

Pre-pandemic, it was growing fast, but only operating just above breakeven.

Profit before tax ballooned to £8.4m in FY 3/2021, clearly a major beneficiary from the pandemic, which immediately raises the big question whether this was an opportunistic float based on unsustainably high profits from the pandemic?

Net assets look modest.

Interim results for H1 of FY 3/2022 showed a decent rise in revenues to £32.1m (up 34%), but a drop in profits - underlying PBT of £3.6m (down 11% from previous year).

There’s also a striking drop in u/l operating profit margin from 19.0% to 10.4%.

That sets the scene, on to the most recent news, yesterday -

FY 3/2022 revenues of £69.2m, up 30% on LY, and up 78% on 2 years ago

Strikingly high gross margin, of 67.2% (down from 68.6% LY, due to higher marine freight costs)

Profit guidance -

We anticipate full year adjusted PBT will be broadly in line with market expectations5.

5 Latest analyst expectations reflect adjusted PBT of £10.0m for FY22

Outlook -

Trading conditions have become more challenging over the last quarter with a number of well-documented pressures impacting consumer shopping habits and operational costs. Despite a tougher consumer and macro environment, we continue to attract new customers to the brand, are outperforming the market, and remain confident in our value-for-money, specialist offer.

Returns rate? Not provided in the update, but would be interesting to find out the online customers returns - likely to be low, I would imagine.

My opinion - this is only my first look at ProCook, but have to say, I like what I see. This looks a decent business.

Bull points -

- Specialist niche, with very high gross margins

- Huge skin in the game, from founding family, which still owns most of the business

- Reasonably good Q3 & Q4 trading updates, showing that bumper pandemic profits were not a flash in the pan [!!], and are being maintained

Bear points -

- Main one is valuation. The whole sector has been smashed to pieces in the last 6 months, so PROC is now looking too expensive.

- Balance sheet is adequate, but not strong, with £10.7m NAV

Roland's Section:

Record (LON:REC)

Share price: 66p (pre-open)

Shares in issue: 199m

Market cap: £133m

“Net inflows of $2.4 billion during the financial year”

Specialist currency and derivatives management firm Record (LON:REC) has released a fourth-quarter update today. Record’s core products are dynamic and passive hedging strategies used by institutional clients to manage their currency exposure. The company is also diversifying into asset management with a number of debt and FX strategies.

Record put on a growth spurt after CEO Leslie Hill took charge in February 2020 and reported net inflows of $9.7bn for the year ending 31 March 2021. But today’s update suggests to me that this early momentum may be slowing.

Despite this, Record scores highly for quality and offers a tempting 6%+ dividend yield. I think it’s worth a closer look.

Financial highlights: Record reports its activities in fund manager language, disclosing net inflows, assets under management equivalent (AUME) and performance fees. This emphasises the ongoing nature of the company’s services, as opposed to the transaction-based services provided by some rivals.

For example, an institutional client might sign up to maintain a specified level of hedging to protect its overseas assets from currency volatility.

Today’s update covers the fourth quarter and full year ending 31 March 2022. Record appears to have achieved modest growth in FY22, despite a poor fourth quarter:

- AUME +3.7% to $83.1bn in FY22

- Net inflows of $2.4bn in FY22

- Q4 AUME -2.7% (-$2.3bn) due to market disruption caused by the war in Ukraine.

- Performance fees of £0.5m earned in Q4 and FY22

- Further $1bn inflow into dynamic hedging after the period end. A further $1bn is expected during H1, as a major client expands its mandate

Profitability: Record has always been highly profitable. But like many asset managers, it has suffered from pressure on fee margins in recent years. In today’s update, the company says that fee rates were “broadly unchanged” during the fourth quarter. Similar wording was used in the Q3 and H1 reports.

I’d guess this means that there’s been some slight pressure on fee rates, due to the use of the word “broadly”.

Management warns that the ongoing fee rate for Dynamic Hedging is now expected to fall, due to the recent increase in mandate size from an existing client.

It’s not easy to be sure of the exact fee rates charged by Record. This information isn’t disclosed. But I think the operating margin trend gives us an idea of the underlying fee margin trend:

Performance fees: These charts from the FY21 results presentation show that management fees have increased relative to revenue since 2019. This seems to imply that Record may not be generating as much income from performance fees as in the past.

However, CEO Ms Hill said today that the £0.5m performance fee earned during Q4 (when AUME fell!) was linked to opportunities arising from recent interest rate rises. If rates continue to rise, I wonder whether we might see further performance fees in 2022. That could have a significant impact on profits.

Source: Record FY21 presentation

Outlook: No new guidance was issued today. The company will announce its full-year results for the year ending 31 March on 21 June.

My view: Record was founded by Neil Record in 1983 and claims to have offered the world’s “first standalone currency hedge in 1985”. It’s always appeared to me to be a clever if slightly niche business. But Record has struggled to deliver consistent growth in recent years and I’m starting to wonder if the market environment has changed.

A number of outsourced currency management businesses have been launched in London and elsewhere over the last 15 years. Alpha Fx (LON:AFX) and Argentex (LON:AGFX) come to mind, but there are others. I wonder if the technology and data that are widely available today (but weren’t in the 80s/90s) may mean that Record’s hedging strategies no longer have the edge they once did.

I should stress this is speculation on my part. Record remains highly profitable and cash generative and today’s update seems reassuring enough to me.

It’s also worth noting that broker forecasts remain bullish and suggest a return to growth over the next two years:

The balance sheet looks bulletproof to me, with substantial net cash. Record is also highly profitable. Margins are high and return on equity has averaged 21% since 2016.

Record’s share price has pulled back from last year’s high.

The stock now looks quite reasonably priced to me, on a rolling forecast P/E of 14, with a prospective yield of 6.7%.

I think Record could be attractively valued at current levels. It might be worth further research. I’ll certainly be watching with interest, to see how the business performs over the coming year.

Ibstock (LON:IBST)

Share price: 179p (-1% at 09.00)

Shares in issue: 409.6m

Market cap: £681m

AGM trading update (from Thurs 21/4)

I’m circling back to look at updates from yesterday from two brickmakers. I’ll start with FTSE 250 firm Ibstock (LON:IBST) which is now at the upper end of our market cap range.

Ibstock closed up 8% yesterday after issuing a strong update and upgrading its guidance for 2022.

- Q1 performance ahead of expectations thanks to stronger brick volumes and “resilient margin performance”

- FY22 guidance now “modestly ahead of previous expectations”

- £30m share buyback programme announced as part of value creation strategy

- Cost inflation a concern, but energy requirements for FY22 are now largely locked in, with one-third purchased for 2023.

- The group is committed to take action to protect margins

Demand in both the new build and RMI (repair, maintenance and improvement) markets is said to remain robust. Ibstock says it’s taking an active approach to managing cost inflation.

My view: Brickmakers including Ibstock have enjoyed good trading conditions in recent years, thanks to strong demand from housebuilders and economics which favour UK production.

But Ibstock’s performance since its 2015 IPO has been underwhelming, in my view. The firm doesn’t seem to have been able to protect its margins or deliver consistent growth:

Ibstock shares are trading below their 2015 IPO levels and have lagged key rivals substantially over the last five years:

In fairness, Ibstock does seem to be on a sounder footing now. Debt levels have been reduced and the dividend looks more sustainable to me. At first glance, the valuation appears quite reasonable:

However, I’m wary of cyclical risks at this point, given the sharp increase in energy costs and the likelihood of rising interest rates.

Ibstock looks reasonably valued and the outlook for trading seems strong. But I’d want to do more research before deciding whether to choose this company over its better-performing rivals.

Brickability (LON:BRCK)

Share price: 100p (-0.5% at 09.30)

Shares in issue: 298.5m

Market cap: £293m

Pre-Close trading update (from Thurs 21/4)

Results for the year ending 31 March 2022 ahead of expectations

AIM stock Brickability (LON:BRCK) supplies building materials rather than producing them. The group’s roots are in bricks and building materials, but Brickability has expanded through regular acquisitions, and now offers a wider range of products and services.

Trading update: Results for the year ended 31 March 2022 are expected to be ahead of previous guidance.

- Revenue of £520m (+11% vs previous consensus of £470m)

- Adjusted EBITDA of at least £38m (+19% vs previous guidance of £32m)

The company says it remains confident that underlying demand for UK housing will be robust, as will construction activity generally.

Management are confident of further organic growth and say the “acquisition pipeline remains strong”.

My view: Brickability floated on AIM in 2019 and has been highly acquisitive since then. Since August 2021 alone, the group has announced three acquisitions and one joint venture.

Buy-and-build businesses can sometimes implode, but when done successfully they can create significant value for shareholders. Brickability’s management are highly experienced and at least some of them remain invested in the business.

The company’s track record as a listed company is still short and we have not yet seen how Brickability will perform during a construction or housing downturn. However, progress so far seems encouraging to me and acquisitions have been achieved without diluting shareholders.

Broker forecasts have already been upgraded on several occasions over the last 12 months.

After yesterday’s update, house broker Cenkos has increased its FY23 earnings forecast by 4% to 9.9p per share (updated note available on Research Tree). This values the stock at 10 times forecast earnings, with a prospective yield of around 2.4%.

As with Ibstock, I’m a little wary about investing in this sector at the moment. But I would be more inclined to consider Brickability than Ibstock, given the group’s entrepreneurial management and strong recent track record.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.