Good morning, it's Paul & Jack here with the SCVR for Friday.

Timing - early today, as I have my first city lunch of the year, on a breezy terrace next to Tower Bridge. I'm so excited, I feel like a convict (I imagine) might feel on being released from prison heading straight for the nearest Harvester! Today's report is now finished.

Agenda -

Paul:

Pci- Pal (LON:PCIP) (I hold) - I review its small placing, to raise funds for expansion into new territories. I'm all for small caps strengthening their balance sheets, after big rises in share price - that's the ideal time to do it, not in a crisis. Under 10% dilution is fine by me, in return for a much stronger balance sheet. Although this does likely push out breakeven further into the future, which some may not like.

Card Factory (LON:CARD) - the usual end of month bank waiver is granted. However, the better news is that a longer-term bank refinancing looks to have been agreed, but not yet documented. The balance sheet is shot to bits, so a big equity fundraising is likely to follow, or be part of the bank refinancing. Re-opening of the shops is said to have been better than expected, but no numbers given. High risk, but so far, so good.

Fireangel Safety Technology (LON:FA.) - awful 2020 results are out. Another equity fundraising to raise £9.0m at 18p per share is announced, so at least the company's finances are now shored up. It's too accident-prone for me, but good luck to holders - who knows, it might be a turnaround in the making, if you're an optimist.

Jack:

Up Global Sourcing Holdings (LON:UPGS) - another upside surprise from this owner and manager of small domestic appliances.

Sylvania Platinum (LON:SLP) - a couple of operational issues in Q3 at the platinum group metals (PGM) producer, but strong basket prices are driving eye-catching quarter-on-quarter growth.

Eleco (LON:ELCO) - in line Q1 update from architectural SaaS business that, while pricey, looks deserving of its 99 Q Rank.

Paul’s Section

Pci- Pal (LON:PCIP)

(I hold)

104.5p - mkt cap £62m

Proposed Placing to raise £5.5m

I last reviewed PCIP here on 8 March 2021, on publication of its interim results. My view at the time was that the cash position looked adequate, but that given the big rise in share price, a small placing of say 10% dilution, would not concern me.

My crystal ball was working well on that day, because such a small placing has just been announced.

I like to scrutinise fundraisings for companies of interest, to inspect the terms, and make sure they’re OK. Also, these announcements often provide useful information about strategy, and current trading.

PCI-PAL PLC (AIM: PCIP), the global cloud provider of secure payment solutions for business communications, today announces its intention to conduct a fundraising to raise gross proceeds of up to approximately £5.5 million through a placing to new and existing institutional investors ...

Main points -

- Quantity - 5.79m new shares to be issued, a 9.7% expansion of the share count - modest dilution

- Price - 95p, a 9% discount, slightly disappointing

- Amount raised - c.£5.5m before fees, so maybe £5.2m after fees?

- Method - accelerated book build, as is usual. When the ABB is announced, it’s usually already a done deal

- No EGM needed, as the company has existing authorities

- Finncap arranged the deal

- No open offer unfortunately - I feel that, where a discount is offered, then existing shareholders should also get the opportunity to participate, and not just a fig leaf tiny open offer, but maybe the same amount again, as any placing

- Purpose - expansion into new territories - mainland Europe, Canada, and Australia

My opinion - when a share has roared upwards, as many have, this is the ideal time to strengthen the finances with an equity fundraising. I wish more companies would follow suit. Look at how many companies ran their balance sheets too thin, then had to raise money near the bottom in April 2020, causing often large & unnecessary dilution. If only they had fixed the roof when the sun was shining. The future is always uncertain, hence why having some cash reserves is good.

PCIP is generating tremendous organic growth, in a niche where it has an enviable position. Therefore it makes sense to maximise the opportunity by expanding faster.

The downside is that extra up-front costs are needed for expansion, so this pushes out the timing of breakeven. Does that matter? Probably not in a bull market, as investors are likely to prefer faster growth, and grabbing the opportunity that PCIP has before it.

The historic figures look bad, but if you watch PCIP's investor presentations on InvestorMeetCompany, the upside case is explained very well - in a nutshell, it’s all about rapidly growing, high margin, sticky, recurring revenues. Providing growth continues, then profitability is easy to forecast.

The shares have had a great run recently, so I imagine it might need time to consolidate. This one is a coffee can share for me, so I don’t really care about the short term share price. It’s rare to find such strong organic growth, at high margins, which then leads to a leveraged positive boost to the bottom line. This is one of the best small cap software companies out there, in my opinion, because customers are lining up to use its product, with the USA being its prime market. Maybe a takeover target too?

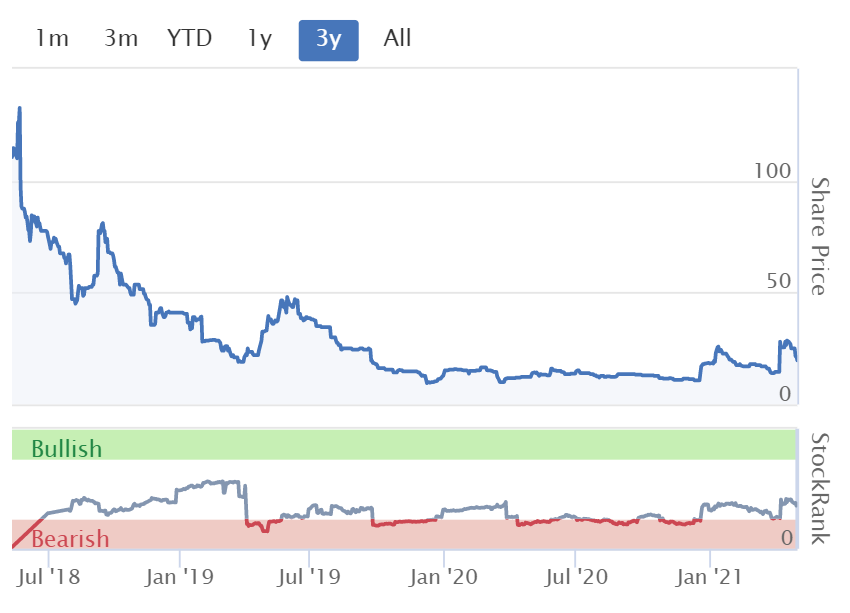

As you can see below, the StockRank system doesn't like it at all ... yet! It will, in a couple of years' time, when the profits are flowing hopefully.

.

.

Card Factory (LON:CARD)

83.8p (up 7%, at 09:25) - mkt cap £287m

It’s the last day of the month, so as usual this is when we get an update from CARD, saying that its banks have given it another month's stay of execution on its banking covenants.

Sure enough, the usual wording appears today, about another month’s grace -

... the banking syndicate has extended waivers in respect of anticipated covenant breaches to 31 May 2021, taking account of the Company's cash flow projections, subject to certain conditions.

However, today’s update also contains much more positive news about a refinancing deal having been agreed with its banks, this is new & positive information -

The Company has agreed headline terms for refinancing of the Group with its current syndicate of commercial lending banks and will issue a further update, over the coming weeks, once terms are documented.

That’s excellent news for shareholders, who were/are taking a helluva risk on this one - solvency risk, and equity dilution risk (which still exists - the balance sheet will need to be repaired with a placing, and debt reduced).

Trading following re-opening - good, but no figures provided -

The Company is pleased to report that its performance following the reopening of stores in England and Wales from 12 April 2021 has exceeded its expectations.

The only other update I can think of, following the recent re-opening, was from Fulham Shore (LON:FUL) which also said things have gone well. The big difference now (compared with last year’s summer re-opening) is that so many people have been vaccinated. Hence I would expect the public to be more confident about returning to something nearer to normal.

Although, anecdotally, a lot of people I know have expressed caution, even fear, of going out again - there seems a degree of inertia, even agoraphobia, with some people, so this is a complex situation where the public seem to be in clear categories about their attitude to re-opening. I think we’ll need to see what happens over time. The direction of travel (getting back to normal) seems fairly clear to me, but I don’t know how long it’s likely to take. The risk of setbacks has to be taken into account also. Nobody knows for sure what the future holds, hence why I recoil when people talk with false certainty, saying this “will” happen. They’re often/usually wrong, so why don’t people moderate it to “might”, or “could”?

My opinion - the market cap of £287m, for a retailer which went into the crisis with a balance sheet already groaning with debt, and which must by now look atrocious, doesn’t make any sense to me.

However, bulls obviously see things differently, so good luck to them.

.

.

Fireangel Safety Technology (LON:FA.)

20p (down 11%, at 10:02) - mkt cap £25m

Results FY 2020 -

I’ve quickly reviewed the figures, and rapidly lost interest - FireAngel had a really poor year - an underlying loss before tax of £(5.7)m.

Capitalised development spend was £2.5m.

Net debt £3.7m, and a weak balance sheet once you write off the intangible assets.

Fundraising of £6.1m in April 2020. That money’s effectively gone, so they’re coming back for more.

Placing of £9.0m announced today, looks a done deal, at a 20% discount, 18p.

There’s a decent-sized Open Offer too, 10 for 33 shares, which seems to be done on a clawback from the placing shares, which I like a lot, that does respect pre-emption rights, unlike many other placings without a proper open offer.

Current trading - says 2021 has started well.

My opinion - it’s been so accident prone in the last few years, and performed so badly, that I personally wouldn’t believe any assurances that things have been turned around.

Good luck to more optimistic investors, if you do decide to give the company the benefit of the doubt. The institutions are clearly prepared to give it another chance, with the £9.0m placing today, so there must be a decent story attached to the new products being developed, and management must retain some credibility. Either that, or the brokers maybe pulled in some favours to get this fundraising away?

With a decent fundraising now done, the risk of insolvency looks to have gone away, so this share is a much safer proposition today, than it was yesterday, having been refinanced. A lot more shares in issue though, so the upside % is diminishing with each fundraise.

We’re in a bull market, so who knows, this could be a nice little speculative trade? Too speculative for me though, and my view is tainted by past serial disappointments. I’d want to see a decisive turnaround in the future numbers, before being willing to have a punt on this.

.

.

Jack’s section

UP Global Sourcing (LON:UPGS)

Share price: 160.6.5p (+2.6%)

Shares in issue: 82,169,600

Market cap: £128.6m

Up Global Sourcing Holdings (LON:UPGS) is a distributor of its own and licensed value-focused consumer household goods brands. Licences include Russell Hobbs and Slater.

It sources parts and products from China (it also has a showroom in Guangzhou) and is headquartered in Oldham.

This kind of model is often afforded a lower valuation multiple, but UPGS looks like it is well run with able management, and its share price has performed very well over the past few months in particular. It seems the market has revised its perception of this company.

Trading at 14.6x forecast earnings, UPGS is not as obviously cheap as it has been in the past, but it’s earning returns on capital employed of some 55.9% and has built up double-digit compound annual growth rates (CAGRs) over time.

Some might think the easy money has been made here but the fact remains that UPGS stacks up very well in terms of Ranks and it qualifies for two Guru Screens (O’Shaughnessy Cornerstone Growth and Lakonishok Momentum), so it is still getting flagged across a range of data points.

Others might argue that the business model is prone to shocks, but we’ve just had the mother of all exogenous shocks and UPGS has managed to navigate its way through, so I’m sure it's looking to the future with confidence.

I don’t see why the company can’t continue to grow from here, ably led as it is by ambitious management.

A strong performance with favourable long-term consumer trends

The outlook statement is found quite far through the update but is worth quoting here for emphasis:

The Board anticipates that its performance in FY 21 will be ahead of current expectations, with revenues forecast to be in excess of £135 m (FY 20 - £115.7 m). While the Group has seen an increase in shipping rates, as noted above, the Board nevertheless currently expects that underlying EBITDA for FY 21 will be in excess of £13.0 m (FY 20 - £10.4 m) with underlying profit before tax in excess of £10.8 m (FY 20 - £8.2 m).

Interim highlights:

- Revenue +11.4% to £75.4m; online platforms revenue +53.6% to 15.6% of total,

- International revenue +0.5% to £23.6m,

- Underlying EBITDA +20.8% to £8.8m,

- Underlying profit before tax (PBT) +24.4% to £7.7m; PBT +18.9% to £7.2m,

- Interim dividend +45.7% to 1.69p.

This looks like continued good execution from a company that is building up a fine track record. FY21 PBT of £10.8m is a notable upgrade and, frankly, the valuation still looks reasonable given the growth.

UPGS has made a purchase post-period: Petra, the Germany electrical kitchen brand. This stock is well followed by Equity Development so you can find a note on that acquisition here (in fact, I’ve just seen that there’s one out already for today’s results here).

International - revenue was ahead of last year by 0.5 % (£0.1 m) to £23.6 m, with Germany performing particularly well, +25.7 % (£1.5 m). This is where UPGS’s most recent acquisition is presumably focused and Germany is ‘a particularly exciting opportunity.’

Supermarkets - good performance in both the UK and, increasingly, in Europe. H1 FY 21 revenue +27.6 % to £20.4 m thanks to its Beldray, Salter and Russell Hobbs brands. The supermarket segment accounted for 27.1 % of revenue in the period (H1 FY 20 - 23.7 %).

Online - grew substantially, with revenue +53.6 % to £11.8 m and 15.6 % of overall revenue (against a newly increased long-term target of over 30%).

The group notes that:

COVID‑19 lockdowns are likely to have accelerated the consumer switch to online shopping by several years. We believe that this changed behaviour is here to stay and have seen particularly strong sales in kitchen electrical, cookware, cleaning and laundry products. In only a few years, online has gone from a start-up to a substantial contributor to overall revenue and a key driver of growth.

Group operating margins declined year-on-year from 23.6% to 22.8% as a result of online marketing spend increasing by £0.2m.

Discounters - sales +0.6 % to £28.4m after a decline in FY20 caused by lockdowns. So this should bounce back in the months and years ahead.

Net cash from operations for the period was level at £6.8m. Net bank debt is down from £11.2m in January 2020 and £3.8m in July 2020 as a result of strong profitability, reduced stock levels, improved supplier terms, and online demand.

This takes the net bank debt/underlying EBITDA ratio to just 0.1x.

Conclusion

UPGS is good at what it does (in fact, it’s probably best-in-class). I wonder if, even now, we are sleeping on the potential here? Increased home working could prove to be a longer term tailwind, and the company is investing in its Head Office.

This investment is ‘an important step in the curation of our talent, providing a workplace that will promote training, collaboration and the interchange of ideas between colleagues.’

There may prove to be a natural ceiling for this kind of business model but for now it seems as though UPGS is making the required investments to become a bigger business in time. There is organic and acquisitive growth potential, along with a clear strategy.

UPGS 'intends to develop its portfolio of brands for mass-market, value-led, consumer goods for the home focused on international retailers, supermarkets, online platforms, and discounters' - given the track record, I’m not about to bet against it.

Sylvania Platinum (LON:SLP)

Share price: 116.8p (-2.67%)

Shares in issue: 272,570,115

Market cap: £318.4m

(I hold)

Sylvania Platinum (LON:SLP) is a producer of PGM metals. One of the main drivers of demand here is from the car industry for catalytic converters, where these metals can help clean up emissions. It’s a Stockopedia Investment Club holding - in fact one of it’s best performers so far - and you can read a much more detailed Pitch on the company here.

Rhodium in particular is expected to remain in deficit for a couple of years but the outlook for all of these metals looks promising at the moment and basket prices at the likes of SLP have been steadily rising.

SLP is not actually a miner - the Sylvania Dump Operations (SDO) comprises six chrome beneficiation and PGM processing plants focusing on the retreatment of PGM-rich chrome tailings materials from mines in the Bushveld Igneous Complex. It’s the largest PGM producer from chrome tailings re-treatment in the industry.

Aside from that, Sylvania also holds mining rights for PGM projects and a chrome prospect in the Northern Limb of the Bushveld Complex, along with some other exploration assets.

Highlights:

- SDO delivered 17,420 4E PGM ounces in Q3 (Q2: 18,363 ounces),

- SDO Q3 net revenue of $74.2m net revenue (Q2: $43.7m),

- EBITDA of $58.7m (Q2: $29.1m),

- Net profit of $41.3m (Q2: $20.3m),

- Cash balance of $102.1m (Q2: $67.1m). Post period end, SLP paid a one-off Windfall Dividend of $14.3m.

The group is experiencing a couple of operational challenges. It’s seeing a higher degree of oxidation in current feed sources, resulting in lower than anticipated PGM recovery efficiencies. Also an inconsistent supply of RoM material to the Lannex milling plant has impacted processing efficiencies and operating costs.

But SLP also notes opportunities:

- Mooinooi chrome proprietary processing modifications and optimisation project should be completed during Q4,

- Lesedi MF2 project on track and commissioning estimated to commence towards the end of Q2 FY2022, and

- Strong cash reserves and no debt means the company can fund further optimisation and exploration projects.

The company’s operations are in South Africa (as is the majority of global PGM production). Covid is still an issue here, and SLP unfortunately lost an employee during the country’s second wave. South Africa remains at a further revised Level-3 status as of the beginning of March 2021, so it’s a live situation.

The mineral royalty tax (calculated as a percentage of PGM revenue) remains a significant cost arising from the higher PGM basket prices.

Conclusion

SLP is always fairly upfront about operational challenges and Q3 is historically a lower production quarter. The group says it remains on track to produce c70k ounces for the current year.

The real driver at the moment is the strong PGM basket price, boosted by the high rhodium price, as well as the recent performance of both iridium and ruthenium.

On that note, the financial results are striking: net revenue up 70%, EBITDA up 105%, net profit up 103% (with a net profit margin of 56%), and net cash reserves up 52%. And these are all quarter-on-quarter growth rates, not year-on-year.

SLP says this is a historically quiet quarter, but if you annualise that net profit figure you come to a run rate of c$165m or £119m. Compared to a market cap of £318.4m, shares still look attractive even after the strong performance. There is always commodity price risk here though. Profits could fall just as fast if the basket price declines.

That aside, these results would make for about 44p of run rate earnings and a PE ratio of just 2.7x (but note that the basket price has been increasing throughout the year and so the actual FY results will likely be less than this).

If you knock off the $102.1m (£73.5m) of net cash you have an enterprise value of £244.9m. Annualised EBITDA of $234.8m (£169m) suggests a potential EV/EBITDA ratio of just 1.45x. So if anything, the share price performance has lagged the basket price performance.

Clearly the market remains skeptical as to the sustainability of these earnings, so as ever we come back to whether or not the PGM prices are in a bubble that will quickly pop. At some point the market fundamentals may change but for now, all the indicators suggest current prices are broadly sustainable for at least 1-2 years and likely longer.

Eleco (LON:ELCO)

Share price: 125.84p (+8.48%)

Shares in issue: 83,079,650

Market cap: £105.4m

Eleco (LON:ELCO) is an AIM-listed specialist international provider of software and related services to the Architectural, Engineering, Construction and Owner/Operator (AECO) industries and interior furnishing industries.

Its market-leading Elecosoft software solutions are developed by teams in the United Kingdom, Sweden and Germany, and include project management, estimating, timber engineering, CAD and visualisation, asset and facility management and cloud-based digital marketing solutions.

These software solutions are sold directly in ELCO’s core markets of the UK, Sweden, Germany, the Netherlands and USA, and indirectly through its international reseller partner channel.

There are more pricey SaaS-based, recurring revenue software stocks than you can shake a stick at these days. What’s immediately a little more interesting about Eleco is that it was actually founded in 1895 and listed on the London Stock Exchange in 1939.

Obviously it wasn’t a SaaS stock at the time, but it sounds like Eleco is building on some real heritage and evolving its model with the times, having originally been called the Engineering and Lighting Equipment Company.

What’s more, Eleco’s valuation is not quite as expensive as other tech stocks (it’s still not cheap though):

Its divisions are:

Building Lifecycle - Comprised of Eleco’s Project Management, Estimating, Property Management and Maintenance Management products. These solutions complement each other and can be adopted into core customer segments. The market for these solutions is c£8bn with an 8-15% CAGR.

CAD and Visualisation - Includes niche products with minimal synergies between customer segments of the Building Lifecycle portfolio. Eleco’s ESIGN and Active Online products are key players in a £450m market.

The group’s growth trends over time look quite promising, so this company is actually starting to tick a few boxes. See the diluted normalised EPS:

Highlights:

- Revenue +9% year-on-year to £7m; recurring revenue up 9% to £3.7m,

- Profit before tax +21%,

- Net cash up from £6.2m to £7.9m

It looks like a solid start to the new financial year. This is just a Q1 update so there’s not much to go on just yet but trading is in line.

Eleco notes a ‘compelling’ market opportunity and a new, focussed growth strategy, which is probably worth looking at in more detail in the most recent annual report, or any investor presentations if they can be tracked down.

Conclusion

This looks quite good actually, and I’ll probably do some more work into it.

You have to be wary of valuation when it comes to SaaS recurring revenue tech stocks. Some of these current ‘nosebleed’ valuations will prove in time to have been cheap. Others may struggle to generate the requisite organic growth.

Regarding Eleco specifically, the stock is not quite as pricey as some other software plays and the outlook for the construction and built environment sector is looking positive at present. A recent report from Glenigan anticipates a sustained recovery over the coming years.

Alongside that, rising material costs and increased regulation are anticipated to squeeze the industry’s margins, making Eleco’s technologies, which use automation and data to improve margins, ever more critical to potential customers.

Margins, returns on capital, and free cash flow per share are all increasing steadily, and the Quality Rank is 99, so I do think this is worth spending some more time on. Early days though, and we could always find something in the due diligence that puts us off.

It looks like broker forecasts were recently revised down - and we do want to see good forecast growth given the valuation - so that’s something to check.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.