Good morning, it's just Paul here today, with the SCVR for Friday.

Timing - I'm still plugging away, so intend finishing about 4pm today. Update at 15:39 - all done for today!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to cover trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research) - don't blame us if you buy something that doesn't work out. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda -

Paul's Section:

Tungsten (LON:TUNG) (I hold) - I review in line results for FY 04/2021. What interests me here is that cash burn has been almost eliminated, and this software company has big name clients, and 93% repeating revenues. Cheap compared with other software companies, and could attract a takeover bid in my view.

Pendragon (LON:PDG) - another car dealer chain reporting a trading bonanza. Although it's a one-off benefit, from a spike upwards in used car prices, which is bound to reverse at some point. Mentions similar uncertainties for H2 as Vertu did yesterday. The whole sector looks very cheap at the moment, even allowing for profits falling when this current bonanza ends.

Lookers (LON:LOOK) - to complete the hat-trick of strong trading updates from car dealers this week.

Getbusy (LON:GETB) - a quick look at interim results from this small, niche software company. It stays on my watchlist as potentially interesting, but there's nothing in the figures or commentary that gets my pulse racing.

Epwin (LON:EPWN) - a positive trading update from Weds. Looks good!

Tungsten (LON:TUNG)

(I hold)

38p (last night’s close) - mkt cap £48m

Tungsten Corporation plc (AIM: TUNG), a leading provider of digital financial management products and software solutions, announces results for the year ended 30 April 2021

Preamble - I last looked at this software company here on 4 June 2021, when it issued an in line with expectations trading update for FY 04/2021.

Several things have changed for the better at Tungsten - cost-cutting to eliminate cash burn, big name contract win with NTT (Europe), and new CEO who came from NTT (so must have been impressed with the software from a client perspective).

On the downside, TUNG has previously announced that a major client (5% of revenues) has given notice to terminate its contract in FY 04/2023, so a negative hit to profitability is in the pipeline.

Today’s results - for FY 04/2021 look as expected.

Revenues £36.1m (down 2%) - I see this as a resilient performance in a year dominated by the pandemic, and it shows the benefit of having 93% of revenues recurring or repeating.

Adj EBITDA is £3.6m (up 33%) - but this is a fantasy number due to capitalised development spend of £2.4m

Huge loss before tax of £34.6m, mainly caused by impairments (non-cash) totaling £27.9m, and a £3.3m forex loss, and £2.1m exceptional costs. So underlying profits close to breakeven.

Net cash of £2.1m (down by £1.1m in a year) - cash burn now largely eliminated. Also note that, being a software business, its costs are quite flexible, being salaries mostly. This is noted in the going concern section, which says that even in a severe downside scenario, it could cut costs accordingly.

Balance sheet - is weak. I would like to see a top-up fundraising. NAV of £56.2m becomes negative NTAV of £(10.3)m. Working capital looks weak, but bear in mind the company receives cash up-front from customers, like a lot of software companies, so it can operate normally with a weak balance sheet.

Cashflow statement - always useful where the P&L is confusing, and there are lots of adjustments. To sumamrise it, operating cashflow is £2.5m, less £2.6m capitalised development spend, less £1.1m in lease payments. So cashflow as I see (i.e. all the important items) is negative £(1.2)m. That’s not great, but it’s vastly better than in the massive cash burning days of old.

Tax losses - don’t seem to be recognised on the balance sheet. But note the accumulated losses are £164.1m, so if TUNG does become profitable, it shouldn’t be paying any tax on those profits.

Outlook - talks mainly about plans to develop its software, and improve the way the business is run. I can’t see anything specific about financial guidance. Existing consensus forecast shows a rise in revenue to £39.0m this year FY 04/2022, and a move into a small profit.

Bear in mind there’s a headwind coming as previously announced loss of a major customer generating 5% of TUNG’s revenues will be phased out. I’d like to know the reason why the major client is withdrawing.

My opinion - software companies seem to be valued on multiples of sales, which I don’t agree with, but that’s what the market is doing right now, so it doesn’t matter what I think!

Recurring/repeating revenues are highly valued, but not in this case.

The £48m market cap seems strikingly low compared with other similar-sized software companies. TUNG also stands out for having very big name clients, which could be of interest to an acquirer. Therefore my main reason for holding a small speculative position personally is that I reckon it could attract a bid at the current valuation. Proactis took me by surprise in that regard - it was practically insolvent, performing poorly, badly managed, but it attracted a bid at a large premium.

.

Pendragon (LON:PDG)

18.4p (unchanged at 10:12) - mkt cap £257m

Preamble - we looked at Vertu Motors (LON:VTU) (I hold) yesterday, which issued a remarkably large upgrade to profit guidance for the half year, and full year. It seems that car dealers are having an absolute bonanza at the moment, due to arguably one-off factors like supply shortages causing a rise in prices (hence also profit margins), particularly for used cars.

Vertu warned of several key uncertainties in H2 - supply shortages of new & used cars, pandemic disruption, higher salaries. Hence it’s guiding for hardly any profit in the seasonally quieter H2, probably lining things up for another upgrade later this year, is my guess.

It looks as if the market has already done the read-across to sector peers, because Pendragon’s share price had bounced by a similar amount before today’s positive update. See how closely correlated the shares of Pendragon and Vertu have been over the last year -

.

Today’s update -

Pendragon PLC (the "Group") today provides a trading update and increases underlying profit before tax guidance for the full year to 31 December 2021 to a range of approximately £55m to £60m.

That’s a lot of profit for a company with a market cap of £257m.

Other points -

- Strong close to June

- Continued momentum in used cars in July

- Supply constraints led to “exceptional gross profits per unit”

- “Good levels of demand”

- Achieved good levels of used car stock availability, from broad range of sourcing channels

- Net debt of £46.0m a year ago has been eliminated, with net cash of £9.5m at 30 June 2021

- Outlook - mirrors what Vertu said yesterday - uncertainty on supply constraints, pandemic, and when (not if) profit margins on used cars return to normal

- Guidance - Full year 12/2021 expected to be £55-60m u/l profit before tax.

Valuation - I haven’t seen any new broker updates today. Working on a note from Zeus on 1 July, it was forecasting £46.9m FY 12/2021 u/l PBT. So today’s £55-60m range is an increase of 17-28% - a big uplift.

Zeus EPS forecast was 2.5p, so I’ll increase that by the same percentage, arriving at 2.93p to 3.2p EPS.

At today’s 18.4p share price, the current year PER is 5.8 to 6.3 - dirt cheap in other words, but we are using the 2021 unusual, one-off spike in earnings, which is not really a valid way to value a company.

My opinion - I think the listed car dealers are very similar in most regards. The reason I prefer Vertu to the others, is its stronger balance sheet. VTU trades at around NTAV = 1, so you’re effectively buying the net assets, and getting the business in for free, so it doesn't really matter what happens to profit, as you'll always be protected with the asset backing. Whereas PDG has negative NTAV at the last year end, which is a major difference.

.

Lookers (LON:LOOK)

70p - mkt cap £273m

Another car dealership chain, which reported yesterday.

Lookers plc ("Lookers" or the "Group"), one of the leading UK motor retail and aftersales service groups, today provides a trading update covering the six month period ended 30 June 2021 ("H1" or the "Period") and an increase in the Board's expectations for underlying profit before tax for the full year.

Factors mentioned for the “excellent” H1 performance -

- Continued outperformance of the UK new retail car market - this sounds ambiguous to me, is Lookers saying that it out-performed the market, or that the market out-performed (what? overseas markets?)

- Strong used vehicle volumes and margins

- “Improved hybrid, omni-channel customer experience”, so it claims, for a sector-wide period of strong trading

- Resilient aftersales performance

- Material cost reductions

Guidance - revised upwards to £50m u/l PBT, just for H1. No specific guidance for the full year.

Of this £50m profit, £13m has come from taxpayer support measures. The company really should pay that money back, given its bumper H1 profits, in my opinion. Although you could argue the Govt will get some of it back from higher corporation tax, and other taxes from buoyant trading (e.g. payroll, VAT). Tricky one.

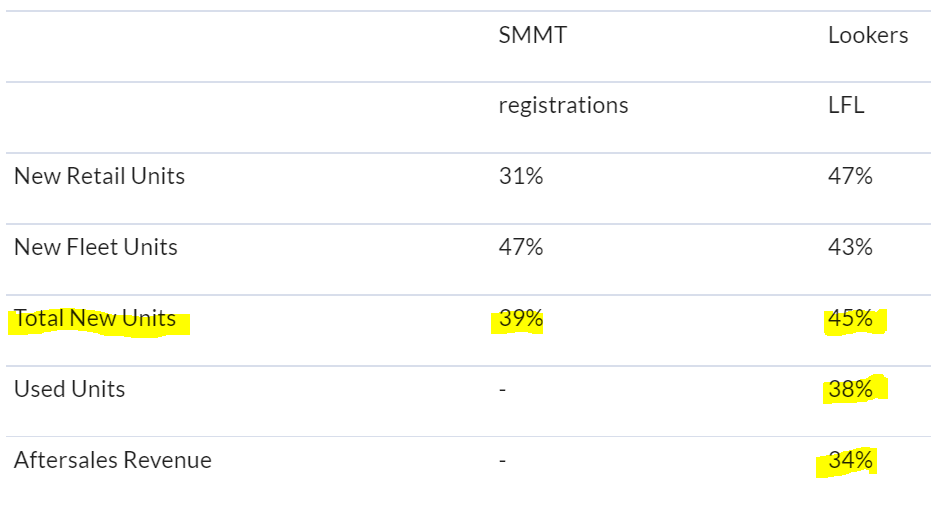

Table below showing out-performance against industry average (“SMMT”). Although comparisons with last year are bound to look good, since that was lockdown 1 a year ago. Still, 45% for new cars uplift, is better than +39% industry average. Vertu and Pendragon didn’t give us this information in their updates this week.

.

Liquidity - ample, and a similar move from net debt into net cash as we saw at Pendragon -

The Board retains its focus on cash management and liquidity. At 30 June 2021, the Group had a net cash balance of approximately £30m compared to net debt of £11.0m last year and £40.7m at 31 December 2020.

Property portfolio is worth £300m it says.

Dividends - intend to resume them.

Outlook - expects FY 12/2021 to exceed previous expectations, but doesn’t provide any numbers on the full year guidance.

Some uncertainty & challenges.

H1 profit weighting expected to be greater this year than previously.

Valuation - many thanks to Zeus for providing an update note today. It’s raised FY 12/2021 profit by 19%, which translates to 12.5p EPS - a PER of just 5.6

That drops to 10.9p in 2022 & 2023, raising the PER to a still very cheap 6.4

I feel Lookers should have a discount to peers, as its shares were suspended for a while, due to accounting problems. Personally I’m not very forgiving about that sort of thing, and prefer to hold a similarly cheap competitor which has not had accounting problems.

My opinion - see what I mean about the listed car dealerships being very similar?

I suppose you could argue that this year’s out-performance is next year’s tough comps.

Overall I find this sector very attractive for the value investing segment of my portfolio, especially now divis are coming back, and balance sheets have been bolstered by the bumper profits this year.

Who would have thought that industry supply problems would send profits soaring?!

.

Getbusy (LON:GETB)

84p - mkt cap £41m

This small group of software companies peaked at about 110p in March, and has fallen back almost 25% from the top - like so many other companies, it amazes me how charts look so similar over the last year.

There’s a half year results presentation on IMC at 11am on Monday (2 August), so I’ll tune in to that, as this company does intrigue me. It’s got some older software (Virtual Cabinet) that is a cash cow, and it’s using the cash from that to develop some new things (Smart Vault).

Smart Vault saw +17% revenue growth (+28% at constant currency) - not bad.

Virtual Cabinet saw flat revenues, and decent profits of £2.1m, up 6%, although I recall they classify a lot of costs as central, which helps the divisional profitability look better.

Overall, the group is still loss-making, at £(949)k in H1.

Balance sheet - quite weak, with negative NTAV and a not very good working capital position.

Outlook - sounds confident -

We continue to see a significant scaling opportunity for our document management business through SmartVault, on which we intend to capitalise. We expect continued strong growth in recurring subscription revenue in that business during H2 and, as we invest in the scale-up, we see an opportunity for the growth rate to potentially increase over the next few years. We look to the future with increasing confidence.

My opinion - I’m keeping this one my watch list, as it’s an interesting niche business. I’m looking for signs that its newer software might reach an inflection point where it begins to rapidly sell. There’s not really any sign of that yet.

.

.

Epwin (LON:EPWN)

109.5p - mkt cap £159m

Epwin Group Plc (AIM: EPWN) ("Epwin" or the "Group"), the leading manufacturer of low maintenance building products, supplying the Repair, Maintenance and Improvement ("RMI"), new build and social housing sectors, announces its half-year trading update in respect of the year ended 31 December 2021.

This update came out on Weds this week, but slipped through the net here on the day. I’ve come back to it, because it looks positive -

Strong trading continues, ahead of previous expectations

- H1 revenues are £157.8m, up 13% on pre-pandemic trading in 2019 (and up 69% on lockdown 1 impacted 2020)

- Supply chain issues continue - raw materials prices continued to rise.

- Selling prices being raised, but lags increased input prices (implying pressure on margins in the short term)

- Net debt of £15.9m at 30 June 2021, a modest 0.6x EBITDA, and £60m headroom - looks fine to me

- Diary date - 15 Sept 2021, for interims to 30 June.

- Outlook - “continues to be favourable” despite supply chain issues

Guidance raised, but no numbers provided -

Assuming that the Group does not experience material supply chain or COVID-19 related impacts in H2, the Board now expects adjusted profit before tax for the full year to be materially ahead of its previous expectations.

Broker update - many thanks to Shore Capital for making its research available to us on Research Tree, that’s extremely helpful.

They have 7.8p EPS this year, and 9.5p next year, giving a PER of 14.0, falling to 11.5 - which looks good value.

My opinion - neutral, as I’m not really up to speed on my research of the company, but the low PER, and positive trading/outlook make this look quite interesting for value/GARP investors.

.

.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.