Good morning from Paul!

All done for today, and the week. Podcast should be tomorrow morning.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

** New SCVR summary spreadsheet for calendar 2024 ** This is the live one! (updated 26/8/2024)

Archive - SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia.

Companies Reporting

Summaries

Gear4music (HOLDINGS) (LON:G4M) - 186p (pre-market) £39m - AGM Trading Update - Paul - AMBER/GREEN

An in line trading update, with a generally positive tone. Shares have had a good run, but still look reasonable value, given improving trend of profits (from a very low base though). Chinese direct to consumer competition is a big worry longer term. There could be a bit further to go in this current bull run in G4M shares, possibly?

Asos (LON:ASC) - up 18% y’day 434p (£518m) - Refinancing, Topshop JV, FY 8/2024 Trading Update - Paul - AMBER/RED

Interesting deals announced yesterday - selling its best brand to a JV (retaining 25% ownership) to raise £118m, but will hurt profitability of course. Refinances super cheap 2026 bonds with expensive 2028 junk bonds, in order to reduce net debt and buy time, but at a large increased annual finance cost. TU is ambiguously worded. I remain negative on the fundamentals, and think equity could end up at zero, but there could be speculative upside, who knows?

Next 15 (LON:NFG) - down 48% to 427p (£435m) - Trading Update [Profit Warning] - Paul - BLACK/ AMBER

A savage market reaction, with shares halving on a profit warning concerning the loss of a major contract, and continued weak spending by public sector and tech clients. I don't have enough information to form a clear view, so it's AMBER whilst we await more information.

XP Factory (LON:XPF) - 13.7p (£24m) - IFRS 16 treatment of leases - Paul - AMBER/GREEN

This is postscript to my review here on 2/9/2024 of XPF's 15-month results. I had a chat with the company, who told me that IFRS 16 has penalised their profit by £1.5m compared with the old lease accounting standards. This is apparently due to opening lots of new sites, where the rules are harsher under IFRS 16 in the early years, compared with the previous accounting method. I asked for a reconciliation, as I don't fully understand IFRS 16 workings, which was sent to me by XPF's finance department. This is clearly material to the profits, so I thought it was worth repeating here -for your consideration & possibly comments -

Paul’s Section:

Next 15 (LON:NFG)

Down 48% to 427p (£435m) - Trading Update [Profit Warning] - Paul - BLACK/ AMBER

A spectacular fall from grace here. A previous high-flyer, this share roughly 47-bagged from the 29p 2009 low, to 1,376p in April 2022. Down to 427p now, we’re back at 2017 price, and fairly near the 2020 pandemic lows.

What does NFG do? I’ve never really been sure, and had it down as a PR/marketing type group. Its website includes this in the “what we do” section -

“...combining growth consulting with marketing services, data and technology platforms and business transformation projects – for companies like Alphabet, Amazon, P&G, Johnson & Johnson, Toyota and many more.”

There was a sign of possible trouble on 27/6/2024, when its in line AGM TU mentioned trading being “resilient, despite a tough macro environment”, and “delays in some clients’ spending, notably relating to government contracts… Spending across the Group’s technology customers has remained soft”.

It said an improvement in trading in H2 was expected.

That triggered a c.15% share price fall over several days, and with hindsight the sellers in late June made the right decision, as things are now much worse.

This is today’s bombshell -

“Contract non-renewal and trading update

Next 15 has been notified that the contract with Mach49’s largest customer has not been renewed after its initial three-year term and will now end on 31 December 2024. This contract had been expected to contribute just over £80m of revenue in FY26. While we anticipate that the client will continue to use Mach49’s services in the future, we believe it is prudent to materially reduce forecasts for the financial year to 31 January 2026. This will in turn reduce the earnout obligation to Mach49’s shareholders due over the next three years.

While the Group has seen strong performances from a number of its consumer-facing businesses, it has continued to see an ongoing weakness in spend from its technology customers as well as a reduction in revenues from its public sector clients.

As a result of these factors and the contract ending which will impact the last month of the fiscal year, the Board now believes FY25 revenue will be lower than planned, and profits to be materially below management expectations."

It’s important to note that NFG’s year end is 31/1/2025. So this major contract loss will only give a glancing blow (one month) to FY 1/2025, but knocks out a huge £80m revenue hole in FY 1/2026.

The StockReport shows forecast revenue for FY 1/2026 at £644m, so losing an £80m contract is losing over 12% of forecast revenue. Operational gearing means the impact on its profit could be much larger than 12%. It does raise the question of client concentration - often something that’s difficult to find out, unless you’re an insider - and a good question to ask all companies in their webinar Q&As. We should probably scrutinise the notes in annual reports more closely, and the risk warnings for signs of excessive client concentration risk, but how many of us have the time to do that in reality for the hundreds of companies we look at?

Results FY 1/2024 look very good - eg revenue £578m, adj operating profit £121m (a high 21% operating margin), and 81.6p adj EPS. There are some funnies in finance income & finance costs, relating to deferred consideration liabilities (earn-outs on acquisitions).

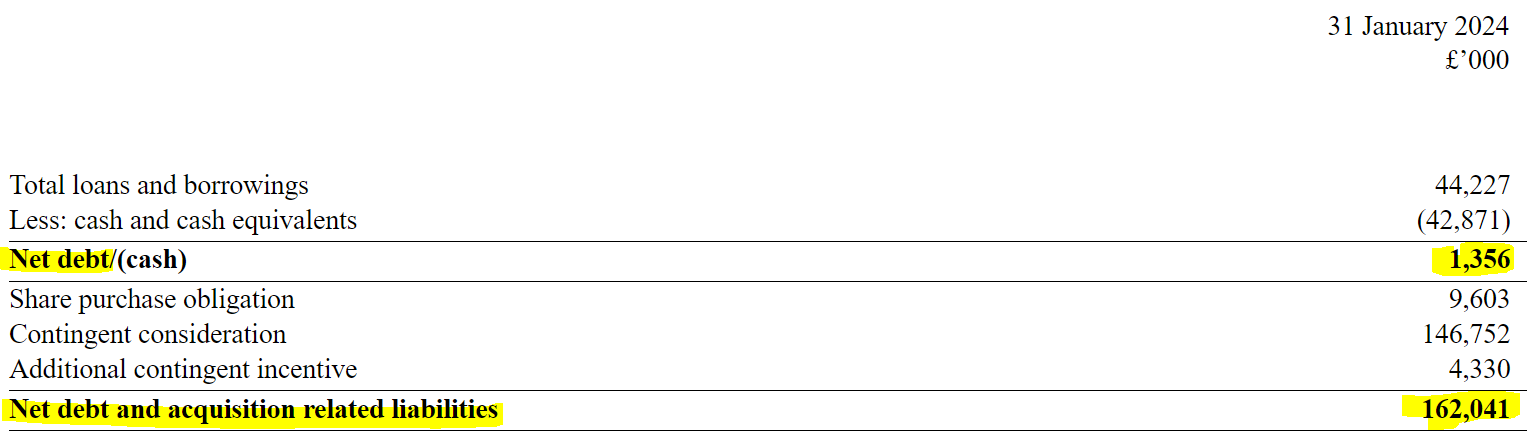

Balance sheet is goodwill heavy, with £279m intangible assets from previous acquisitions. That means NAV of £156m becomes a negative NTAV £(123)m. This also includes a deferred tax asset (unusual) of £62m, less deferred tax liabilities of £6m, gives net deferred tax asset of £56m. I tend to remove deferred tax, so that takes NTAV down to a concerningly bad £(179)m. So when NFG says it has a strong balance sheet, they’re certainly not looking at the numbers in a prudent way. They might be referring to liquidity, as its 31/1/2024 year end net cash was almost neutral: £42.9m cash, less £44.2m “loans & borrowings”, so only £1.3m of net bank debt. That means tons of headroom on the £150m+£50m HSBC facility.

However, there’s a sting in the tail. The balance sheet also contains substantial deferred consideration liabilities (earn outs). These are big numbers - let note 9 do the talking -

Although note the profit warning today indicates that the earn-outs will reduce, but we need to know by how much.

Broker updates - nothing available. We can’t possibly judge this without sight of revised FY 1/2026 forecasts. Losing 12% of revenue, which could be high margin work (we don’t know, but it’s a high margin group, so that stands to reason) could have a devastating impact on next year’s profit. Hence it’s not possible to value this share without the revised forecasts.

Key other information is by how much the earn-out liabilities are going to reduce? As they stand, paying those liabilities recorded at 31/1/2024 would theoretically use all of the available bank facilities. That probably won’t happen, because the amounts payable should now reduce after Mach49 lost this major contract, and the earn-outs are spread over several years, but we need an updated figure.

Paul’s opinion - all of this leaves the question as to whether NFG’s super profit margins depended on one big contract? How will the business look afterwards now it's ended?

Reduced spending by tech customers is also a worry, and reminds me of the point some are saying that massive spending on AI might be sucking cash away from other budgets at IT companies? YouGov (LON:YOU) delivered a similar devastating profit warning earlier this year, and is slashing overheads to rebuild margins. It looks like NFG will also need to slash its own overheads, which means redundancies seem likely unfortunately.

Without any updated forecasts, it’s impossible for me to assess whether this share is cheap after today’s 50% fall, or whether the fall is justified.

I don’t see any immediate risk of financial crisis, due to the neutral net bank debt position and plentiful facilities available. However, a lot depends on how much, and when the next earn-out payments will be, which could significantly increase bank debt.

Hence it all looks impossible to judge right now, due to lack of key information. So I’ll stick it in my “don’t know, awaiting further facts/figures/forecasts, but no insolvency risk for now” tray, so AMBER.

My profit warning data clearly showed that in the last year, the larger small-mid cap companies (c.£100m-1bn) which have savage profit warnings do tend to recover, at least somewhat. Whereas it's the sub-£100m profit warnings which usually continue falling. So I think there's a chance both Next 15 (LON:NFG) and YouGov (LON:YOU) could be interesting potential trades, worth doing some further research on.

Asos (LON:ASC)

Up 18% y’day 434p (£518m) - Refinancing, Topshop JV, FY 8/2024 Trading Update - Paul - AMBER/RED

Trading Update -

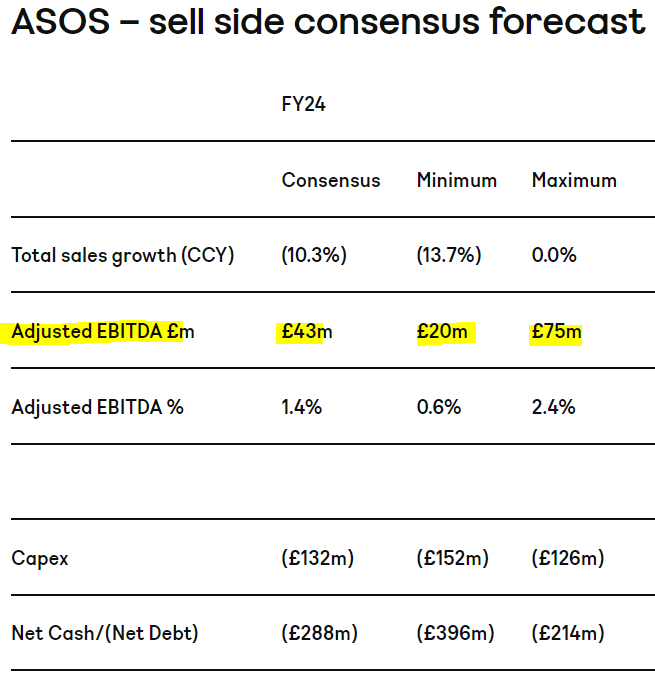

“ASOS expects FY24 adjusted EBITDA at the top end of consensus estimates2, sales slightly below guidance, and all other guidance as set at FY23 year end remains unchanged.

2 Company-compiled consensus, as available on ASOS Investor Relations website.

Extract from Asos website -

I’m not clear what the phrase “at the top end of consensus estimates” actually means. Is it referring to the £43m consensus figure above? Or the range from £20-75m? That form of wording could mean either. "Consensus" is the average, it’s not a range, so how can you be at the high end of a specific figure? All of the above numbers turn into PBT losses anyway, so it's arguably splitting hairs.

There are no broker notes on Research Tree to help me here.

The StockReport’s EPS analyst consensus data has updated overnight, which shows a slight improvement in FY 8/2024 EPS loss from -116.2p to -112.7p. Note that the nonsense EBITDA figures at Asos turn into losses before (and after) tax. So this is not a healthy, profitable business, it’s loss-making and has a weak balance sheet, as I’ve flagged before.

Sales are shrinking, as the consensus is -10.3% fall in sales, and it says “sales slightly below guidance” - so what maybe -12, -13%? Why can’t they just give the number instead of making us guess? Probably because they haven’t reconciled the year end numbers yet, which isn’t unreasonable given it’s only 6 days after the year end cut-off. Although sales really should be a very simple number to produce.

Topshop JV - selling the family silver? This is a cash raising exercise. Asos bought Topshop (including TopMan, plus Miss Selfridge and HIIT) from the administrators of Arcadia in Feb 2021 for £265m cash - overpaying, in hindsight, at the peak of the pandemic boom in online sales.

Topshop brands have now been sold to a new JV at a £180m valuation. Asos will own 25% of the JV, with HEARTLAND owning 75%. So it looks as if Asos will receive cash of £135m, which after fees and other, will net to £118m net cash for Asos - helping its balance sheet, but of course reducing future profits from selling a profitable brand and instead having to pay a royalty to use it.

HEARTLAND is connected to Bestseller, which is Asos’s largest and longstanding shareholder, currently at 27.1%, which on paper has lost billions on this share. I think it’s worrying that the biggest shareholder wants to secure for itself the best brand asset - that’s the sort of thing you see happen when a company’s long-term survival is in doubt.

JV financial impact? - this is confusing -

“The Joint Venture will grant ASOS certain design and distribution rights for the TSTM brands in return for a royalty fee to enable it to continue marketing and selling the TSTM brands online. For FY25, the Transaction is expected to have a £10-20m negative impact on EBITDA and to be increasingly EBITDA accretive over time.”

The way I interpret that, is this deal will hit Asos’s profits by £10-20m pa. What the last bit means, who knows? Since it’s harming profit, how can it be “increasingly EBITDA accretive over time”? That doesn’t make sense. My best guess is that they’re trying to say the financial impact will lessen over time, but who knows? This announcement looks like it’s been heavily edited by the PR people to confuse with positive spin.

Timing - expected to complete in Q4 2024, which must mean calendar 2024, as FY 8/2024 Q4 has already passed.

Asos’s strategy is -

“to turn ASOS into a company that delivers sustainable, profitable growth.”

A nice aspiration, as currently it’s not profitable, and isn’t growing either.

Refinancing - this relates to bond financing, which is key for Asos’s balance sheet. It has benefitted from insanely cheap interest rate bonds issued during the zero interest rate period. That was a time bomb though, as finance costs would shoot up when the bonds expired, and that’s assuming Asos would even be able to refinance the bonds. Worst case scenario, bondholders would end up owning the company, with equity wiped out.

“ASOS today launches a refinancing, which will include (i) an offering of approximately £250m Convertible Bonds due 2028 and (ii) a concurrent partial cash repurchase of the outstanding £500m 0.75% Convertible Bonds due 2026 issued by Cornwall (Jersey), with full details included in a separate RNS.”

Two separate announcements yesterday on the refinancing. I’ll concentrate on the later, outcome RNS called “Successful placement of Convertible Bonds due 2028…”

The rationale is to buy back (at a discount to par) the existing April 2026 bonds, using the £118m proceeds from the Topshop JV disposal, and a new issue of longer-dated 2028 convertible bonds. That reduces net debt, and extends the maturity. Although it will of course greatly increase the cash outflows for paying interest on the bonds, something it doesn’t mention in the rationale bit!

New bonds - carry a coupon of 11%, and are issued at par. That’s a huge hike in interest cost from just 0.75% on the old bonds. I’m not a bonds specialist, but google tells me that 11% coupon is into junk bond territory - higher risk, higher reward.

Conversion (into ordinary shares) price is the same as the old bonds, at an absurd £79.65/share. So forget the convertible element of the bonds, they won’t convert unless there’s a miracle, given the current share price is just £4.34.

Sept 2028 redemption date buys Asos more time to sort itself out.

Redemption price is 120% of par, so that’s another hefty but deferred cost. This takes the yield to maturity up from 11% to 14.84% pa - very much a junk bond.

Old bonds - Asos offered to buy back the 2026 bonds at 85p in the pound, so a useful benefit to its balance sheet by eliminating some of its net debt, but at substantial additional costs from the very expensive new bonds.

£173.4m have been bought back for cancellation, announced last night.

It says £73.6m of the old bonds remain outstanding.

This deal looks very bad to me, and is all about survival, rather than good economics. Financing cash outflows are now going to shoot up, due to taking on expensive new bonds, in order to buy time to try and move from trading losses into profits.

Paul’s opinion - I’m astonished Asos shares shot up yesterday, as the bond deal means its finance costs will soar - and reinforces that this is a financially distressed business, having to issue a junk bond on poor terms.

Also the current trading statement is ambiguous, and means Asos remains loss-making at the PBT level.

Its last balance sheet showed negative NTAV of £(72)m, and remember that’s getting worse every 6 months due to ongoing trading losses.

This share could easily end up a zero in my view.

So why is it worth £518m market cap? There could be strategic value given Asos has >£3bn pa revenues, and a very well known brand and repeat customers. Mike Ashley’s scattergun approach of buying retailer stakes includes Asos, where his Frasers (LON:FRAS) empire holds 22.4% of Asos. The 3 big holders (Bestseller, Frasers, and Camelot Capital Partners) control 64% together, so there might be a tussle for control.

Turnaround potential is intriguing, as with over £3bn revenues, each 1% improvement in the profit margin is over £30m additional profit (or reduced losses more accurately at this stage).

Hence this share is best seen as a special situation, where anything could happen.

From my point of view, after following since the start, it looks very much like we’re witnessing a business that originally had stellar growth, but has made negligible profits (only £228m retained earnings since day 1), has never paid any divis, and now seems to be in serious trouble.

Hence I’m keeping my AMBER/RED negative view, based on the interim results, which I explained here on 17/4/2024. The deals announced yesterday are not positive in my view. They buy it more time, but at considerable cost - selling its best brand, and agreeing to very expensive new junk bonds which will increase its cash outflows.

Anything could happen though, Asos may have strategic value to an acquirer, or it might pull off a trading turnaround, who knows? Refinancing the bonds means it has time on its side, hence you could argue a speculative positive case too.

Cradle to grave? -

I'd be surprised if yesterday's spike up in price sticks -

Gear4music (HOLDINGS) (LON:G4M)

186p (pre-market) £39m - AGM Trading Update - Paul - AMBER/GREEN

Gear4music (Holdings) plc, ('Gear4music' or 'the Group') (LSE: G4M), the UK's largest retailer of musical instruments and music equipment…

Reassuring comments today for FY 3/2025 -

"We are pleased to report that trading during the financial year to date has been in line with the Board's expectations.

Having successfully reduced our net debt and operating costs during FY24, during the early stages of FY25 we have focused on implementing the growth strategy outlined in June and expect this to start delivering results in the second half of this year.

We are well prepared operationally for the upcoming seasonal peak trading period, and the Board remains confident of the delivery of our medium and longer-term profitable growth strategy.”

Broker update - thanks to Singers for its note this morning. It talks about EBITDA, but of course that’s not a reliable number in this case, as explained here before. However the real profit figures look quite good too, with adj PBT forecast to rise from £1.1m in FY 3/2024 actual, to £2.7m in FY 3/2025 forecast. That’s adj EPS of 9.4p, rising further to 14.6p in FY 3/2026. PERs are 19.8x and 12.7x - perfectly reasonable I’d say.

Paul’s opinion - I upped us from amber to AMBER/GREEN at 147p on 25/6/2024, on improving fundamentals - notably improving profits from restructuring, and a balance sheet gearing problem resolved. Revenues are now in a modestly rising trend. I’m not convinced the acquisitions previously have added much value, maybe it should stick to its knitting rather than buying more brands?

Shares are up nicely this year to 186p, but don’t look stretched yet in valuation terms, and it wouldn’t surprise me to see a continuing bull trend up to maybe 200-250p at a guess? Quite good, but not madly exciting. This is after all a highly competitive, and low margin market. Also the growing threat from Chinese direct to consumer websites puts me off buying any shares in companies that have products made in China and sell them in the UK. I’ll cover this in more detail in my forthcoming weekend podcast. A quick search on TEMU shows it is already supplying cheap musical instruments & accessories (although quality can be very hit & miss with TEMU, so I suspect many people wanting musical instruments might prefer to stick with a trusted UK brand).

On balance, AMBER/GREEN still feels about right.

An interesting rollercoaster since G4M floated in 2015. Note that it floated with 20.2m shares in issue, and now has a barely changed 21.0m - clearly showing the watchful eye of its owner-manager Andy Wass in eschewing dilution. That also means in theory there's nothing to stop the share price regaining previous highs, if the market gets into another speculative frenzy over growth.

Brexit restrictions on trade might have helped impede sector leader, Germany's Thomann possibly? I've heard previously that UK customers prefer the rapid delivery times that G4M can offer domestically in the UK.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.