Good morning from Paul! In case you missed it, I added some extra sections to yesterday's report in the afternoon/evening, and we're off to a flying start this morning with 5 backlog sections.

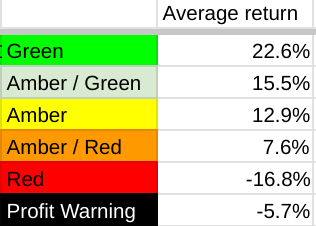

I'm finishing promptly today, to meet Phil Hanson for lunch, as a thank you for his excellent spreadsheet which measured the performance of our traffic lights system here in the SCVR. It clearly shows that GREENs do best, with AMBER/GREEN and AMBER not far behind (so do look at all 3), whilst considerable under-performance is shown in particular by REDs. Whereas AMBER/REDs also under-perform, but within it, there are some big winners - so that category is a bit of a lucky dip, where every now and then a poor/risky company suddenly shoots up when it sorts itself out, eg McBride (LON:MCB) . So there are opportunities throughout, but statistically you skew the odds more in your favour with GREENs - which is what we hoped would happen, so it's great to have data from Phil which proves it works!

Latest figures as of last night -

It would be interesting to see if combining our traffic lights with the StockRanks produces a better result still.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia.

Companies Reporting

Summaries

Keller (LON:KLR) - 1,582p (£1.16bn) - Interim Results - Paul - AMBER/GREEN

Superb H1 results, and FY estimates raised. Looks a remarkable turnaround in the last year which we've flagged here before, several times. Still looks good value on a fwd PER of c.8x, despite shares having doubled. Is this improved performance sustainable though?

Seeing Machines (LON:SEE) - Up 3% to 4.82p y’day (£200m) - Q4 KPIs - Paul - AMBER/GREEN

Strong growth, driven by EU legislation requiring fitment on new cars. However, this update drops the Q3 wording of reassuring on FY 6/2024 performance, which arouses suspicion. No broker notes available. I like the story, but am a little wary given the changed wording of this Q4 TU.

Paul's Section:

Firstly some interesting movers from yesterday (with news)

Beazley (LON:BEZ) - up 11% to 706p (£4.56bn) - Results FY 6/2024 - Paul - AMBER/GREEN

A striking 11% rise in share price yesterday, in a positive reaction to record H1 profits, up 99% to $729m.

Strong NTAV/share of 483p ($4bn).

Positive comments & outlook, eg -

“When faced with the world's largest ever IT outage, Beazley's approach to underwriting cyber risk was tested and proved to be highly resilient. We see opportunities in the remainder of the year and are confident in delivering on our high single digit growth guidance. We are also pleased to confirm that we have improved our undiscounted combined ratio guidance for the full year to around 80%."

High StockRank of 89. Strikingly cheap fwd PER of 6.0x.

Looks interesting - worth a closer look.

Deliveroo (LON:ROO) - up 10% to 141p (£2.42bn) - H1 Results - Paul - AMBER

Positive market reaction rising 10%, on positive H1 results & outlook.

I reviewed this here on 18/4/2024, coming away pleasantly surprised.

It’s a turnaround year, but the H1 profits are tiny for a £2.4bn market cap company -

Net cash of £662m.

Outlook sounds positive -

Paul’s view - very difficult to value, as it’s only really trading around breakeven. Who knows what the future holds? Strong balance sheet with surplus cash, of which £150m is ear-marked for further buybacks.

Hikma Pharmaceuticals (LON:HIK) - up 8% to 1,992p (£4.42bn) - Half-year Report - Paul - AMBER/GREEN

Underlying H1 results show flat operating profit vs H1 LY at $402m.

Good outlook -

“The outlook for 2024 remains strong and we are pleased to upgrade Group revenue and profit guidance:

Group core operating profit of $700 million to $730 million, up from $660 million to $700 million”

Has almost $1bn net financial debt.

NTAV $1.2bn.

Paul’s view - valuation metrics look quite attractive, so shares look worthy of a closer inspection.

Main Sections:

Keller (LON:KLR)

1,582p (£1.16bn) - Interim Results - Paul - AMBER/GREEN

This is an interesting one! It’s done some big moves over the last 20 years, but in an overall sideways move until Oct 2023 - where I’ve cut off the chart -

Now look what’s happened in the last year - it’s doubled!

I’m pleased to say we did spot something interesting happening here, as follows -

23/10/2023 - AMBER - Keller - up 15% to 771p - TU materially ahead. Graham thinks it's low quality, but cheap. Paul is more positive on Keller.

17/01/2024 - AMBER/GREEN - up 3% to 853p - ahead exps. Very low PER, and 5% yield. Balance sheet just about OK, but fair bit of debt. Interesting!

05/03/2024 - AMBER/GREEN - up 7% to 935p - FY 12/2023 Results - good numbers - underlying dil EPS up 53% to 154p (PER 6.1x). Net bank debt down 33% to £146m. Total divis for year up 20% to 45.2p (yield 4.8%). Confident outlook. Modest pension deficit payments to end in Aug 2024. Balance sheet NTAV c.£400m, looks OK overall, although gross bank debt seems higher than I would like. Paul’s view - I like it.

15/05/2024 - AMBER/GREEN - up 16% to £13.18 (£958m) - AGM TU - excellent update says 2024 will be materially ahead of the Board’s previous expectations. Balance sheet also appears to be strong with a very low leverage multiple.

Keller Group plc ('Keller' or the 'Group'), the world's largest geotechnical specialist contractor, announces its results for the half year ended 30 June 2024.

Things are going well -

“Outstanding H1 performance; expectations for FY 2024 materially increased”

Some really impressive highlights numbers here, in particular a big improvement in operating margin, and a large reduction in debt -

Outlook -

“Board's expectations for full year 2024 materially increased, underpinned by our record order book of £1.6bn”

“We maintained our focus on sustainable markets and attractive projects and the results reflect both the strength of the Group's presence in the buoyant North American market and our continuous groupwide emphasis on improving project execution and delivery.

The current macroeconomic environment presents opportunities, particularly in North America, albeit there are challenges in some of our other markets. The strength of the Group's performance, together with the quality of our record £1.6bn order book, provides us with increased confidence in the outlook for the rest of this year. As a consequence, the Board now anticipates that the Group's performance for the full year will be materially ahead of current market expectations1. This performance will have a modest weighting towards the first half given beneficial tailwinds in the period."

1 Analyst consensus underlying operating profit for FY 2024: £178m; range: £176m - £179m.”

Broker update - there’s a really helpful detailed note from Panmure Liberum, which significantly raises estimates, as follows -

FY 12/2024 adj fully diluted EPS, old: 156p, new: 186p

FY 12/2025 adj fully diluted EPS, old: 161p, new: 191p.

Those are big increases, and PL hints there could be more upside on these raised numbers.

If it’s heading towards say 200p EPS, then the current PER is only about 8x 2025 estimates.

As you can see, nearly all the H1 profit came from the high margin N.American business -

Balance sheet - looks fairly strong, although I note receivables are extremely high at £797m - something to query with management if they do a webinar.

Cashflow statement - all looks good to me.

Paul’s opinion - we’ve been moderately positive on Keller since autumn 2023.

These H1 numbers and outlook show a remarkable improvement in performance, driven by its higher margin N.American business. How sustainable is this, and how has a transformational improvement in performance occurred?

Based on these numbers, and a forward PER of only 8x, I suspect this share’s bull run could continue.

It’s already risen a lot, so I’m happy sticking with a positive view at AMBER/GREEN.

Seeing Machines (LON:SEE)

Up 3% to 4.82p y’day (£200m) - Q4 KPIs - Paul - AMBER/GREEN

Seeing Machines Limited (AIM: SEE, "Seeing Machines" or the "Company"), the advanced computer vision technology company that designs AI-powered operator monitoring systems to improve transport safety, publishes its quarterly Key Performance Indicators ("KPIs") for the quarter ended 30 June 2024.

I better understand the investment story here, after having a briefing with management earlier this year. This eye-tracking technology has been around for years, with SEE being a leading provider of just a handful of competitors globally. Uptake is now rapidly growing because of EU legislation requiring this being fitted to new cars. SEE doesn’t make the products itself now, it’s just an IP business, charging a relatively modest per unit royalty. Rapid growth means it should move into profit & cash generation quite soon, after years of losses. Mgt seem confident they can reach profits without needing any more equity raises.

Recent quarters show a strongly improving growth trend -

It recently received a $16.5m licence fee from Caterpillar.

The above seems good, but it doesn’t say how trading is going versus expectations.

Outlook -

“Paul McGlone, CEO of Seeing Machines, said: "We have maintained growth of over 100% in the number of cars on road featuring our technology from 12 months ago, despite the quarter-on-quarter volatility experienced during the year. Regulations are now in place so we are confident that these figures will continue to grow for existing Automotive programs and as new programs start production.

"Similarly in Aftermarket, the new regulation in Europe will require more commercial vehicle OEMs to seek After Manufacture fitment for our Guardian technology, underpinned by successful homologation (regulatory approval) with our Northern Ireland customer, Wrightbus, as announced on 30 July 2024. With Guardian Generation 2 stock sold we are now focused on Guardian Generation 3, initially with European commercial vehicle OEMs, then all customers across existing markets in Europe, The Americas and Asia Pacific."

Paul’s opinion - I don’t have enough information as to whether these KPIs are as expected, or above or below, since SEE doesn’t directly tell us, and I don’t have any broker notes available. This looks a bit suspicious, as the previous Q3 update did specifically say that SEE was on track to meet FY 6/2024 expectations. That wording has been dropped from this latest Q4 update, which is bound to make investors suspicious that performance might have fallen short of expectations for FY 6/2024.

I’ve been AMBER/GREEN here twice previously in 2024, so will stick at that level, although I’m a little nervous, so will probably hold back on buying any shares personally until we have more clarity on how 2024 has panned out. There does seem a good growth opportunity here, driven by legislation requiring the use of this safety technology. Shares are currently tricky to value, as it is still loss-making, so the valuation depends entirely on future growth and profitability, which is tricky to estimate at this stage.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.