Good morning from Paul!

Today's report is now finished.

I was very impressed with Megan's webinar earlier this week. If you missed it, this is well worth a listen over the weekend - some useful insights, with high quality stocks tending to perform better in market downturns. (Note: it's silent at the start, then starts properly at about 3m 25s)

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk.

Quick Comments

To round off the week -

S4 Capital (LON:SFOR) - down 5% to 123p (£708m) - AGM TU - Paul - RED

Sir Martin Sorrell’s rapidly growing digital marketing group. I reviewed it here on 11 May 2023, concluding that the weak, greared balance sheet, and huge adjustments to turn a statutory loss into a profit, put me off.

It’s difficult to work out what this waffly update, full of buzzwords, is actually saying today. The market doesn’t like it anyway, with shares down 5%.

Paul’s opinion - same as last time - the accounts look horrible, and the style of today’s update puts me off further. I wouldn’t bet against Sir Martin, given his amazing track record.

Costain (LON:COST) - up 3% to 48.7p (£134m) - Update re A66 Project - Paul - AMBER

I’ve read this 3 times, and am still struggling. Costain’s involvement in a road project, the A66, is coming to an end, but no details are provided as to why. It denies that this will hit the order book, as press reports have apparently claimed. The most important bit says -

The Board remains confident of delivering full year results in line with its expectations.

Paul’s opinion - not a sector I invest in (low margin contractors). But the value metrics are looking superb now, a fwd PER of only 4.3x, 5% dividend yield, and a strong balance sheet, with shares at a discount to NTAV. See SCVR from 11 May 2023 for a review, where I concluded positively about this share. It’s dropped about 20% on the rumours/news about this problem project, so might be worth a fresh look, if you do invest in this sector. Although clearly the A66 news is bound to unsettle investors, as often we see that an initial problem can escalate into a series of profit warnings. For that reason, I think it’s best if I play it safe and await developments, so AMBER for now.

WANdisco (LON:WAND) - suspended - update - Paul (I hold) - RED

This jam tomorrow company turned out to be a giant fraud, at least the order book & supposed contract wins were. So I've mentally written off my investment here. However, an update today gives a glimmer of hope - shares should come back from suspension on 30 June - likely to gap down maybe 80-90%, I imagine. A little more detail on the false orders, which were with 8 supposed customers. Trying to raise $30m, which looks like it's been well supported by shareholders, although no indication on what price new money will be raised at. Change of name planned, probably a good idea in the circumstances!

Backlog items -

Midwich (LON:MIDW)

Up 3% to 465p yesterday

Market cap £480m (based on 103.3m enlarged share capital)

This growing distributor of audio-visual equipment caught my eye here on 9 May 2023, with an in line, confident AGM statement combined with quite modest valuation, drew me to view the share positively at 446p.

Earlier this week it announced a £50m placing, to fund acquisitions and reduce debt (rather confusingly worded, I felt).

The placing has now been done, at 425p, which is only a 5.6% discount. This has been well received by the market, with the price closing yesterday up 3% to 465p, a healthy premium for those who participated in the placing, and also a small PrimaryBid retail offer, which raised £1.25m.

Paul’s opinion - I’m mentioning this fundraise because it says to me that decent companies which are raising money for sensible expansion plans, not to avoid bankruptcy, are able to get a deal done on sensible terms. A 5.6% discount is fine, if the money is going to be used for good quality, reasonably priced acquisitions. Midwich says there are 6 more possible acquisitions currently in due diligence (i.e. detailed, confidential inspection of the business & accounts, where an outline deal has already been informally agreed).

The main acquisition target, is a Canadian company called SFM. The price being paid is 7x adj EBIT (operating profit) for 2022, but with 2023 revenues expected to be “materially ahead”.

This sounds impressive -

The Acquisition and M&A Pipeline combined is expected to be materially earnings accretive in the first full year of ownership, including the impact of the Fundraise and before synergies

There’s obviously execution risk with doing lots of acquisitions, but as far as I can tell, Midwich seems to be growing strongly with an acquisitive strategy that doesn’t seem to involve excessive dilution, relative to the growth being achieved. It had 80m shares in issue in 2017, which will have risen to 103.3m after this latest fund raise. Yet EPS has more than doubled over that period - demonstrating that (so far anyway) the acquisitions have added value. Dilution is good, if it’s used to buy good companies at a lower rating than the acquirer's own shares, and where there are synergies on top of that.

Midwich is looking like an increasingly interesting company, which might be worth you taking a closer look at. I’ve not done any detailed work on it, as always, because I have to cover hundreds of companies here. Potentially interesting is my conclusion, so I’ll remain GREEN on it.

ME International (LON:MEGP)

158p

Market cap £599m

We’ve been raving here about MEGP shares for some time. Checking the archive, I did a thorough review of the FY 10/2022 results here on 1 March 2023, concluding that I liked everything about this share, giving it a firm thumbs up.

Previously on 7 June 2022, I concluded that it was a highly attractive buying opportunity at 70.6p. It’s more than doubled since then - very impressive in a nasty bear market for small caps.

Management tried to take it private in Jan 2022 for 75p cash per share, which was declined by outside shareholders, but it was a clear message that management saw good times ahead.

That’s the background, so I’m starting off with a very positive impression of this share. Let’s see if that stands up to scrutiny of the latest update for H1, which was published a week ago, on 1 June 2023.

ME Group International plc (LON: MEGP), the instant-service equipment group, announces an update on the Group's trading for the six months ended 30 April 2023 (the "Period").

Company’s headline says -

Strong H1 performance across all business areas and operating markets, with increased full year outlook for 2023

The Company is pleased to announce that during the Period, Group revenue was up by more than 24% and profit before tax was up by more than 35% compared with the six months ended 31 April 2022 ("H1 2022"), driven by a strong performance across all of the Group's key business areas and its 19 operating markets.

Photobooths - revenue up 25%. Strong demand for photo ID. Focusing R&D on photobooth innovation, including biometrics - “should be the norm by 2025”. Anti-spoofing patented.

Laundry - “continued to perform very strongly”, revenue up 36%. Rolling out a new App.

Other smaller divisions also trading well.

Outlook - nice clear guidance here for FY 10/2023 -

As a consequence of this strong trading performance in H1 2023, the Board is pleased to increase its outlook for the current financial year, ahead of previous expectations, with revenue between £300 million and £320 million, EBITDA between £100 million and £110 million and profit before tax between £64 million and £67 million.

This compares favourably with the guidance provided on 1 March 2023, which said -

* The Group's compiled analysts' consensus forecast for the financial year ended 31 October 2023 shows revenue of £284.8m, EBITDA of £91.1m and profit before tax of £58.5m. [1 March 2023 RNS]

That’s a 12% increase in PBT guidance, if we take the mid-point of the new range of £64-67m.

Broker updates - many thanks to both Canaccord and Finncap, for publishing notes via Research Tree, it’s so helpful. Canaccord seems to have anticipated strong performance, and already had £62m adj PBT pencilled in, but has raised that by £2.0m to £64.0m, noting that there’s a good chance actual results could come in ahead of this new forecast.

Equivalent EPS (adj and diluted) is raised from 12.7p to 13.1p.

At 158p per share, that’s a PER of 12.1x, which looks good value still, despite the share price having doubled in the last year.

Paul’s opinion - remains very positive, so I’m happy to maintain my thumbs up/GREEN view of this share. As always, the one thing I cannot do is predict the future. So you have to do the deeper research, to form a view on what the future might hold. All I do is review the facts, figures and forecasts as they are today. On that basis, this share looks excellent to me.

I particularly like that this share is no longer a one trick pony of photobooths. The laundry business is significant too, and the other growth areas sound promising, including the food/juice vending machines. As it’s operated booths for so many years, there must be immense experience & know-how within MEGP, which is hidden value I think.

Downside risks? I suppose the main risk is if some technical development makes photobooths redundant. People have been worrying about that for many years, but MEGP seems to have successfully innovated, and stayed ahead of the curve. The biometric comments in today’s update particularly intrigues me. If any readers have looked into this in more detail, then please do share your views in the comments. As always, my stuff is just an introductory review, not an in depth analysis of the products, markets, or competition.

MEGP (formerly Photo-Me) shares have been quite a rollercoaster in the past -

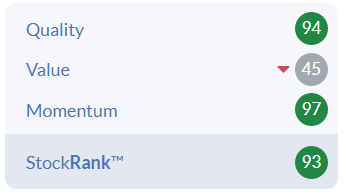

A very strong StockRank further encourages me -

Today's News

Shoe Zone (LON:SHOE)

Up 11% to 233p (at 09:31)

Market cap £108m

This cheap shoes retailer had been a star performer, but shares wobbled on publication of disappointing interim results & only in line FY 9/2023 expectations, which I reviewed here on 16 May 2023.

I think the share price had risen to c.250p based on expectations from investors that the company would continue a run of beating market expectations, hence why in line wasn’t really good enough to support a continuing rising share price.

Investors who stuck with it have been rewarded today, with an ahead of expectations update -

Shoe Zone is pleased to announce that since the publication of its Interim results on 16 May 2023, trading has exceeded expectations due to particularly strong recent trading through May and early June. This is a combination of strong early demand for summer products and lower container rates contributing to improved margins.

As a result, the Company now expects adjusted1 profit before tax for the financial year ending 2 October 2023 to be not less than £10.5m.

1 Adjusted to exclude the profit on the sale of freehold property and foreign exchange revaluations.

I can’t find what previous guidance from SHOE was, so am referring to a note from Zeus (many thanks) dated 16 May 2023. This shows underlying PBT of £8.5m for FY 10/2023. So today’s update looks to be a c.24% increase in profit expectations - excellent news!

By my calculations that would be EPS of 16.8p (previously 13.5p).

Paul’s opinion - all is forgiven! This is a much better performance, than was previously indicated, and it’s good to see better margins coming through from lower container freight costs.

Based on the much improved profit outlook, I’m happy to go back to GREEN now (previously AMBER after the disappointing outlook comments last time).

Expect a decent share price rise today (I haven't looked at the live price yet!).

EDIT: it's up 11% at 09:31, which looks justified to me.

Also note that the StockRank is jammed on maximum!

NWF (LON:NWF)

Up 7% to 275p

Market cap £136m

Trading Update & Renewed Banking facilities

NWF Group plc ('NWF' the 'Company' or the 'Group'), the specialist distributor of fuel, food and feed across the UK, today provides a trading update for the year ended 31 May 2023 ("FY23"), together with details of its renewed banking facilities.

Reading through my previous notes here, we’ve been positive (green) on NWF for some time, noting in the SCVR for 1 Feb 2023 that it looked like a beat against expectations was coming, given record H1 (Nov 2022) figures, and a very confident outlook.

Sure enough, the next update on 9 Mar 2023 was ”significantly ahead”, with profit guidance raised from £12.3m to £17.5m.

My only worry is whether the booming profits are sustainable, given that competitor Wynnstay (LON:WYN) had reported a bumper one-off boom year, due to the knock-on effects of the energy crisis, causing selling prices to rise substantially, but maybe not sustainably?

Looking at today’s update, things are still looking very good - it’s another guidance raise -

As set out in the trading update of 9 March 2023, the Group delivered strong performances from all businesses in the first half. Pleasingly, this positive momentum has been sustained through the second half and consequently, FY23 headline profit before tax is now anticipated to be ahead of the current market expectation1 and in excess of £19.0 million2.

1. Company compiled consensus headline PBT of £17.5 million; information for investors including analyst consensus forecasts, can be found on the Group's website at www.nwf.co.uk

2. Stated before amortisation of acquired intangibles and the net finance cost of the Group's defined benefit scheme

Acquisitions - Sweetfuels (bought for £10m) is performing strongly. More acquisitions are planned, the strategy being to consolidate a fragmented market - I like that approach, and it should be quite low risk, in that management will know what they’re buying (i.e. not branching out into unknown areas).

Bank facilities renewed -

The Group has completed the renewal of its banking facilities with NatWest Group for a three year term on competitive rates, with an option to extend by two years. The facilities of £61 million comprise an invoice discounting facility of £50 million, a revolving credit facility of £10 million and an overdraft of £1 million, with a further £20 million accordion available to support the development strategy of the Group.

Net cash was £1.2m at the last accounts (interims at 30 Nov 2022).

Today we’re told net cash at 31 May 2023 year-end date is higher than expected, but not provided with a number, which I would have liked -

Net cash at the year-end is also higher than previous expectations as a result of the stronger trading result, ongoing disciplined cash management across the Group and some positive working capital movements.

Balance sheet - I’ve looked at the last balance sheet, and it’s OK. Although it reports net cash on the last balance sheet date, both receivables and payables within working capital are large (both over £100m), so I imagine there would be quite large intra-month swings in cash/debt, depending on when suppliers are paid, and also the timing of customers paying invoices. Hence why borrowing facilities would be needed.

What we really need is the average daily net cash/debt figure. All companies should report that figure as best practice.

Note there’s a pension deficit of £10.5m, so you would need to check that out properly, I haven’t got time right now, as a webinar is about to start!

Paul’s opinion - based on another ahead of expectations update today, and a still-reasonable valuation, I maintain my positive view of NWF shares. But as usual, I’ve no idea what will happen in the future, in particular whether the big jump in earnings over the last 2 years is sustainable, or a boost from the energy crisis? That’s the key area to research if you’re digging deeper on this share.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.