Good morning from Paul & Graham!

I had an interesting email from Paul Hill over the weekend, making some really interesting points about if/when/why various valuation measures should or can be used (eg price to sale, EV/EBITDA). I'm thinking this is an interesting topic that would make a good discussion, so I'll ask him if he wants to do a podcast on it.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

** New SCVR summary spreadsheet for calendar 2024 ** This is the live one! (updated 6/9/2024)

Archive - SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia.

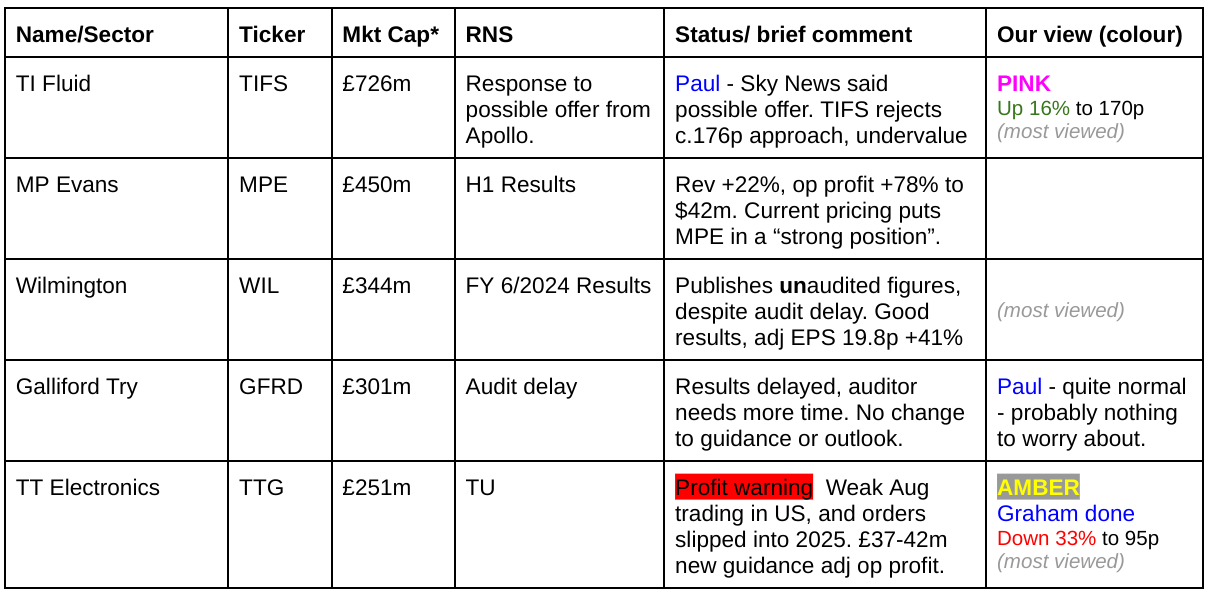

Companies Reporting

Summaries

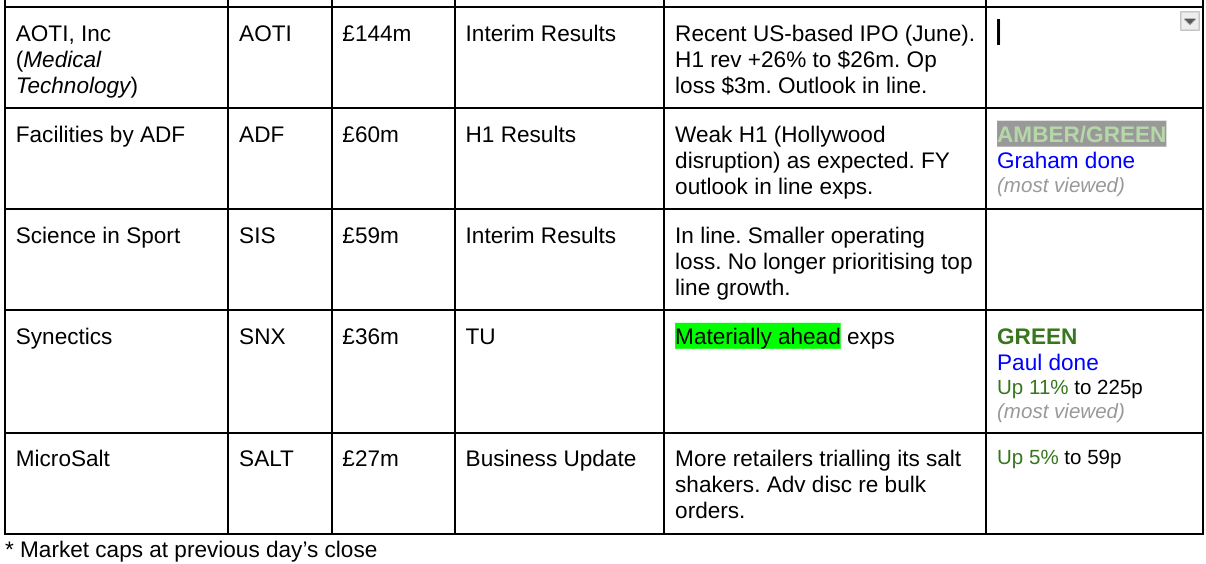

Synectics (LON:SNX) - up 11% to 225p (£40m) - Trading Update [ahead exps] - Paul - GREEN

An ahead of expectations update drives a useful broker upgrade. Taking into account that 20% of its market cap is supported by net cash, and good performance & outlook, I think this share remains cheap. However, it relies on large & lumpy orders, so future performance can't be guaranteed. If it meets ambitious forecasts, then I could see this share continuing to rise, c.300p looks doable providing the news remains positive.

TT electronics (LON:TTG) - down 36% to 91.4p (£162m) - Trading Update - Graham - AMBER

An awful profit warning from this component manufacturer which seems to be the company’s own fault, as it suffers from operational issues in North America. I’ve been positive on this one as it has deleveraged in recent years, but today’s update has severely affected my trust in the story and so I’m switching to a neutral stance. Perhaps I can turn GREEN again in the future, if they can fix these problems.

Facilities by ADF (LON:ADF) - down 2.5% to 53.9p (£58m) - Half year results - Graham - AMBER/GREEN

The outlook from this provider of film/TV production facilities is in line with expectations. The H1 results in isolation are poor but they do reflect an industry affected by highly unusual strike activity and the company is now enjoying positive momentum as it integrates a significant acquisition announced last month.

Paul’s Section:

Synectics (LON:SNX)

Up 11% to 225p (£40m) - Trading Update [ahead exps] - Paul - GREEN

I should start by saying how sorry I was to hear of the recent sudden death of CEO Paul Webb. Our condolences to his family, friends, and colleagues.

“Synectics plc (AIM: SNX), a leader in advanced security and surveillance systems, provides an update on trading for the year ending 30 November 2024 ("FY 2024"), following the conclusion of its third quarter, ended 31 August 2024.”

Trading is going well -

“Continued positive trading in the third quarter - FY 2024 now expected to be materially ahead of market expectations”

“*Prior to this announcement, FY 2024 market expectations were revenue of £52.9m and adjusted PBT of £3.5m”

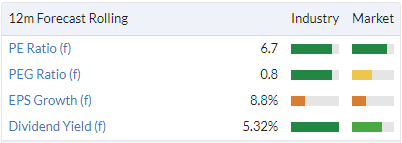

Materially ahead usually means at least 10% above (profit). Shore Capital helpfully updates us, raising adj PBT estimate from £3.5m to £3.9m. This is 18.6p adj EPS (previously 16.8p). I’m not sure that justifies an 11% increase in the value of the company. On the new forecast, the PER is 12.1x, which looks about right to me for this type of business.

Note that Shore is pencilling in quite large further increases in EPS to 23.9p and 29.0p in FY 11/2025 & 26 respectively. If it achieves those (and Shore points out SNX has established a track record of meeting/beating expectations recently) then I suspect a share price nearer 300p would be likely - quite good upside. Although you never really know, as it all depends on what contracts it is able to win, and on what terms - which depends on a wide range of factors that as investors we cannot predict.

Outlook -

“Continued momentum across its key markets”

Good order intake -

“Order intake remains strong and recent contract wins have included a $1.2m contract for the installation of a new security and surveillance system at a casino resort in the Philippines, further contract wins with Saudi Aramco, and a strategically important order for the Company's first installation, of a new security and surveillance system for a casino resort, in Cambodia.”

“The Company continues to focus on further strengthening its already healthy FY 2025 order book.”

Paul’s opinion - I see Graham reviewed its 11/2023 results back in February, concluding he liked it, so GREEN, at 187p/share. We’re now higher at 225p/share, and I think it still looks good value, due to the forecasts having risen, and trading/outlook comments today being good.

So I’ll stick with GREEN. There’s always the risk that a gap could appear in the order book, so you can never really sleep soundly with this type of company (with mostly non-recurring revenues). Hence why investors don’t tend to be prepared to pay a high rating (rightly so).

It pays smallish divis, and has a nice solid debt-free balance sheet that included £6.4m net cash at 31/5/2024, c.20% of the market cap.

All looks good to me, GREEN it is!

It's quite surprising how much this share has gone up recently. Just shows that there are plenty of decent companies on the UK market at attractive prices, despite all the doom & gloom.It's established a nice recovery in EPS since the pandemic -

TT electronics (LON:TTG)

Down 36% to 91.4p (£162m) - Trading Update - Graham - AMBER

This is a horrible trading update from a company I’ve been “GREEN” on, and the share price has crashed this morning on heavy volumes:

Here is the bad news:

August trading results are weak due to “operational efficiency issues in two North American sites”. These issues are causing both delays and higher production costs. Plans are in place to rectify the issues “during the remainder of the year and potentially into Q1 2025”. It seems that the issues are entirely the company’s own fault and flow from problems to do with “factory planning and factory layout”.

Aside from the financial impact, this really makes me question management and if the right people are in charge.

Additionally, recent order intake in the higher-margin North American components business has been for delivery in 2025, not 2024 as expected. Perhaps it’s to be expected that customers would not want to send in more orders for short-term delivery, if the company is struggling to execute current orders?

The result is that TTG’s H2 revenue will be c. £15-20m lower than expected, and operating profit will be lower by £13-18m.

The rest of the group is trading “broadly in line” but we still have a big hit to group profitability; full-year operating profit will now be £37-42m (last year: £53m, previous year: £47m).

Leverage is now expected to finish 2024 “around or marginally above” the target range of 1-2x.

(Context: leverage had fallen from 2x (at the end of 2022) to 1.7x (at the end of 2023), so this is a step backwards).

Medium-term targets are unchanged, including a 12% operating margin in 2026, but it’s understandably difficult for investors to look past the poor performance in the current year.

Graham’s view

With a hit to profitability of up to 35%, it makes sense that the share price would fall by this amount or more, especially considering that there are balance sheet implications.

A leverage multiple of 2x is not where the company ought to be; it has worked very hard to reduce leverage and this backward step is a big blow to the investment thesis.

I wouldn’t question the company’s solvency at this degree of leverage, but the big attraction for me has been the deleveraging story and so it’s very frustrating to see it going in the wrong direction..

I’m therefore inclined to switch to a neutral stance on this share. This may be a poorly-timed change of stance. But when I’ve been wrong, sometimes it’s best to take the hint that the market is giving me!

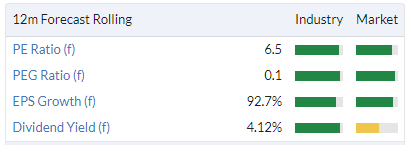

For what it’s worth, here are the multiples/ratios the company was trading at as of last night:

I thought this cheap valuation should have been sufficient to price in some bad news, but a surprise 35% hit to profitability is beyond what I thought was possible.

Could this be the low? Perhaps. Leverage (i.e. net debt divided by adj. EBITDA) is returning to the top end of the range but I think this is almost entirely because of lower EBITDA/profitability, not because of an adverse movement in net debt. And as the issues that are causing lower profitability get resolved, the leverage multiple and the valuation of TTG should hopefully recover.

However, I can’t confidently build an investment thesis here, after the company has disappointed me like this. I no longer trust it, so I can’t stay GREEN. I’m going back to a neutral stance.

Facilities by ADF (LON:ADF)

Down 2.5% to 53.9p (£58m) - Half year results - Graham - AMBER/GREEN

Facilities by ADF, the leading provider of premium serviced production facilities to the UK film and high-end television industry ("HETV") announces its unaudited half year results for the six months ended 30 June 2024 (H1-FY24).

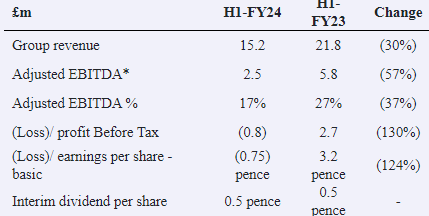

These results suffered from the knock-on effects of the Hollywood strikes. It posts a large drop in year-on-year revenues and a loss, but maintains its dividend:

The performance is described as “resilient” and as an improvement from H2 2023 (but not from H1).

ADF supported “38 high-profile productions” during the period. Checking last year’s interim report, I see that they supported 46 then.

Last month (only a few weeks ago really), ADF announced the £21m acquisition of Autotrak that was covered by Paul in superb detail here. Paul had a positive view of that deal.

Outlook statement: in line with market expectations. H1 “finished strongly” with the order book for H2 “building well across the summer months as momentum returns across the market following the Strikes”.

CEO comment:

"We are proud of the performance delivered in H1-FY24, demonstrating the Group's resilience and leading market position as the Film and HETV [high-end television] industry continues to recover from the impact of last year's strike disruptions. With the market normalising, we continue to be well-positioned to achieve our goal of becoming a One-Stop-Shop…

"As we continue to invest in our fleet and explore further acquisition opportunities, alongside the increased investment anticipated across the industry in the UK in the coming years, we remain confident in achieving our aim of generating £100m revenue in the medium-term."

Dividend: it’s a little cheeky of the company to say that their unchanged dividend of 0.5p “is reflective of the Group's progressive dividend policy”.

The share count has gone up after the recent fundraising, and the unchanged interim dividend (per share) will therefore cost the company more in total than it did last year.

But in my book, a dividend is defined in terms of its per-share payment, not in terms of its total cost to the company. So I see this as a dividend that is currently flat, not one that is progressively increasing!

However, I acknowledge that the company must have quite a lot of confidence if it is willing to make this payment, given the loss-making circumstances it finds itself in.

Net debt excluding leases was £13m at the end of June. The Autotrak acquisition was funded by a £10m placing for the upfront £10m cost, with the rest of the cost spread out in future periods.

Graham’s view

We have interim results that are as expected, an in-line trading update, and a confident outlook statement. So I am happy to leave Paul’s AMBER/GREEN on this unchanged.

That said, I think reporting here could be more straightforward - why does the company bother giving us adj. EBITDA when depreciation is one of the most important charges, and is clearly a real cost to the business?

The depreciation charge was £2.6m in H1, similar to previous periods, and should not be ignored.

I tend to agree that the Hollywood strikes were very rare events that should not repeat for many years, so that ADF should be in the clear for the foreseeable future.

Rightly or wrongly, the market doesn’t seem to be pricing in too much success:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.