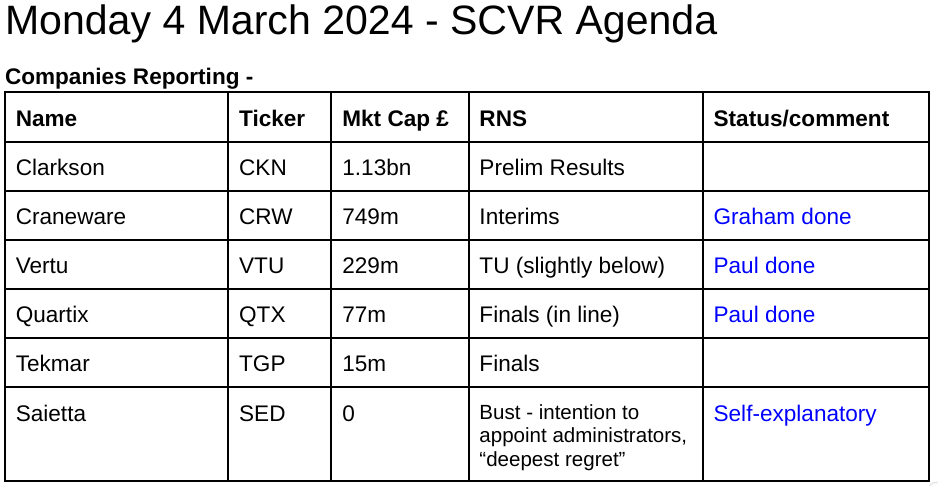

Good morning, it's Paul & Graham here!

The Week Ahead - today's article from Megan is an interesting read. Looks like Graham and I will be very busy Tue-Thu this week, with loads of results coming out, and of course the Budget on Weds (see Tuesday's papers for details!)

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Paul's 2023 share ideas, with live prices.

New SCVR summary spreadsheet from July 2023 to date, updated at weekends (very useful quick reference tool, search for ticker using CTRL+F). Hover over cell for pop-up notes.

Frozen SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

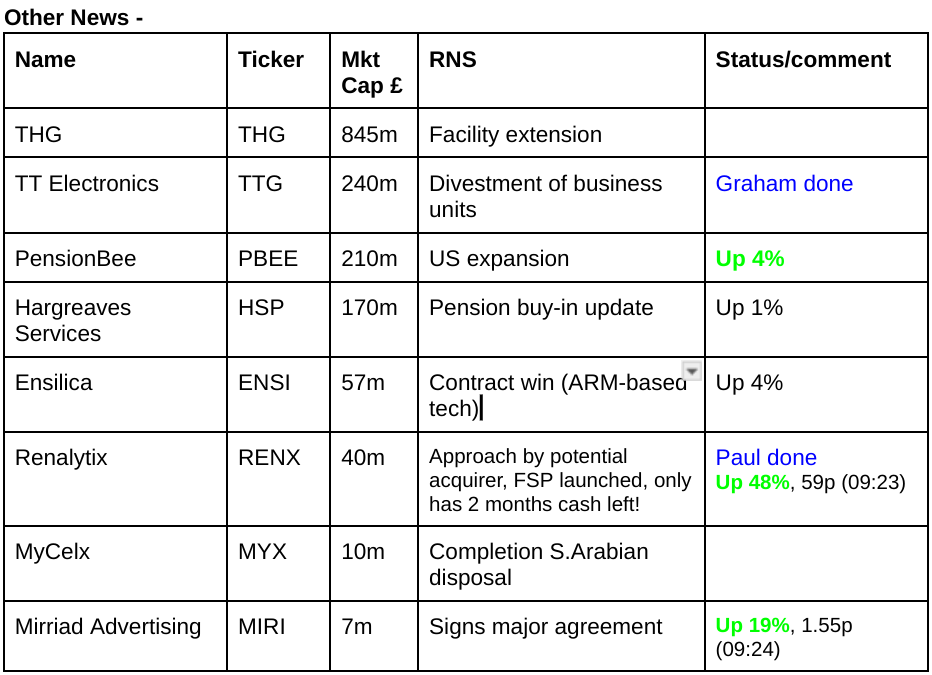

Mid-morning movers (with news) -

Shoe Zone (LON:SHOE) - up 7% to 260p - tipped in Times (persuasive article, it does look cheap!) & SCSW over weekend.

Rosslyn Data Technologies (LON:RDT) - down 28% to 11.75p (£3m) - another year of heavy losses expected, due to contract signing delays. Only £800k cash left, so another fundraise or delisting now look inevitable. “confident of securing further sizeable contracts in the near-term.”. Looks very high risk, and a stale story (v poor track record), but it’s in a sexy sector - could sentiment turn on contract win announcements maybe? Claims that its new AI module, “offers a transformational opportunity”. One for optimists only!

Hipgnosis Songs Fund (LON:SONG) - down 10% to 56.8p - bombshell from the new Board. Says its songs catalogue NAV is worth a third less than previously advised. Dividends stopped “for foreseeable future” to focus cashflows on reducing debt - the 8.3% yield was the main reason to own the shares, so this looks bad.

Summaries of main sections

Renalytix (LON:RENX) - up 58% to 63p (08:48) (£63m) - Possible bid, FSP, funding - Paul - RED

Trying its best to sound positive, but this almost-bust heavy cash-burner admits it only has 2 months' cash remaining. So potential bidders might be motivated to try to buy it from an administrator, rather than existing shareholders? It remains very high risk until fresh funding raised and/or bid talks held. Yet another blue sky project that has destroyed an immense amount of shareholder value, and run out of cash.

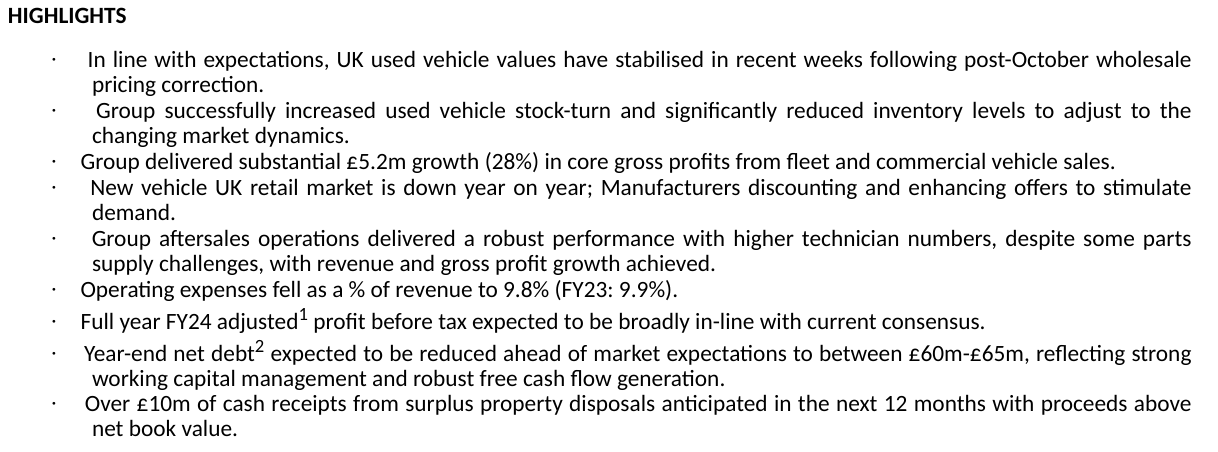

Vertu Motors (LON:VTU) - 68p (pre-market) £228m - Trading Update - Paul - GREEN

Slightly below expectations update for the 11-months to 31/1/2024, within FY 2/2024. Shares are slightly up in early trades, so looks like traders are reassured that things are not any worse after a profit warning in Dec 2023 (caused by a sharp fall in used car prices). I'm happy to go back up to green, as uncertainty removed from the previous PW. Shares are at par with NTAV, so 100% asset-backed (mainly freehold property).

TT electronics (LON:TTG) - up 0.6% to 136p (£241m) - Divestment - Graham - GREEN

TTG accelerates its deleveraging process with the £20.8m disposal of some business units. In combination with healthy profits in 2023 (even if they are at the lower end of the previously forecast range), I’m looking forward to a very meaningful reduction in its £139m net debt.

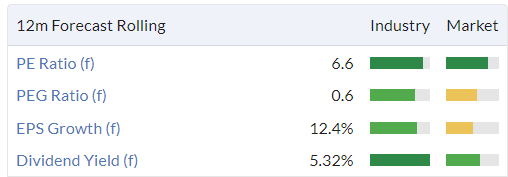

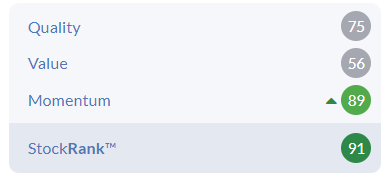

Quartix Technologies (LON:QTX) - up 2% to 163p (£79m) - Final Results - Paul - AMBER/GREEN

In line with expectations audited numbers for FY 12/2023. Confident outlook for 2024, and I wonder if the reduced forecasts might be beaten later in 2024? Some problems, but these are being dealt with by the Exec Chmn/founder who has come out of retirement to sort things out in a back to basics strategy that looks simple common sense to me. Overall I'd like it a bit cheaper to buy some myself, but I see more upside than downside, so let's go with AMBER/GREEN.

Craneware (LON:CRW) - unch. at £21m (£743m) - Interim results - Graham - AMBER

Solid numbers from Craneware today as they report 8% revenue growth in H1, an improvement on the growth number reported at the most recent full-year results. The outlook for the year is unchanged. An impressive software success in the US healthcare sector.

Paul’s Section:

Renalytix (LON:RENX)

Up 58% to 63p (08:48) (£63m) - Possible bid, FSP, funding - Paul - RED

I mentioned this share recently, pointing out that despite positive-sounding operational news, the figures showed that the company was almost bust, having run out of cash. So it's highly precarious until refinanced.

Today news says -

Possible bid approach -

“Renalytix has received an unsolicited approach from a large and well-capitalised publicly listed strategic diagnostics company, which is in the process of evaluating an acquisition of the entire issued, and to be issued, share capital of the Company.”

Great, but on what terms, given that the company is in such a weak financial position?

Formal Sale Process (FSP) launched, to drum up more potential interest. Might decide to remain independent & stock market listed (mentions AIM and NASDAQ).

Takeover panel has given a dispensation from 28-day PUSU rule, and that potential bidders will not have to be publicly named.

Stifel is being appointed adviser for FSP.

Cash position - admits it’s almost out of cash -

As part of a review of funding options currently being explored, the directors of Renalytix (the "Board") are considering possible sources of funding, including equity and debt. The Company is in advanced discussions with certain existing shareholders as well as potential new equity and debt providers.

The Company has cash on hand of $2.3 million and marketable securities of approximately $1.4 million as at 3 March 2024. As reported on February 15, 2024, operating cost reductions commenced during the fiscal second quarter continued with a fiscal third quarter cash burn target approximately 33% less than in the prior quarter and approximately 50% less than in the first quarter of fiscal 2024. The Company expects existing cash resources to finance the business through April 2024, foregoing the possible Sale of the Company and/or its assets, or successful completion of the advanced financing activities noted above.

Paul’s opinion - an interesting project, with some impressive shareholders (Harwood has 10%), but cash burn has been large, and it’s been obvious for some time that the cash was running out - hence terrible shareholder value destruction.

It’s now just a lottery, to see if anyone is either prepared to buy it (at what price though?), or refinance it. RENX is in such an obviously weak position, it would only have any bargaining power if several parties are prepared to compete to buy or refinance it. So a fairly good chance that small shareholders get hung out to dry, I'd say, but anything could happen.

Yet another blue sky project that has been a disaster for shareholders, and inadequately financed.

Vertu Motors (LON:VTU)

68p (pre-market) £228m - Trading Update - Paul - GREEN

Vertu Motors, a leading UK automotive retailer with a network of 188 sales and aftersales outlets, is pleased to announce the following update with regards to the five-month period to 31 January 2024 (the "Period") ahead of its preliminary results for the year ended 29 February 2024 to be announced on 15 May 2024.

It packs a lot into this headline below! -

Used car prices stabilised; new vehicle market uncertain; aftersales robust. Strong year-end cash position

Key point is this -

Full year FY24 adjusted1 profit before tax expected to be broadly in-line with current consensus.

1 Adjusted for exceptional items, share based payments charges and amortisation.

How much below then?

I’ve not yet seen any updates from brokers. Zeus downgraded FY 2/2024 forecast EPS by 17% to 8.2p back in Dec 2023, in reaction to news that secondhand car prices had plunged unexpectedly quickly and by a significant amount. We had similar news from Motorpoint (LON:MOTR) too so it’s a sector thing, and should be a temporary impact.

“Broadly in line” probably means something like 8.0p EPS maybe? I’ll have to wait for broker updates to feed through.

EPS of 8.0p would mean a PER of 8.5x

Other points - I’ll copy this to save typing -

Valuation - Stockopedia stats are based on the forecasts, which is 10.0p EPS for FY 2/2025, hence the PER below being lower than my figure above for FY 2/2024.

Also note the very strong asset backing (mostly freehold property) which we’ve mentioned here many times before. Despite this, Vertu is one of the few car dealers that didn’t receive a takeover bid!

Paul’s opinion - the share price reacted badly to the profit warning late last year, and now looks into attractive value territory again.

Questions are also being asked about the imminent Chinese invasion of something like 20 new electric car brands, which surely must do some damage to European makers? Although there also seems reluctance from the public to buy electric cars.

With a share price now at par with NTAV, I see VTU as an attractive each way bet (part car dealer, part property company). Last time in Dec 2023 I went down to amber, due to uncertainty over the profit warning and used car values. Now that we know trading has stabilised, I’m happy to see it as GREEN again.

Quartix Technologies (LON:QTX)

Up 2% to 163p (£79m) - Final Results - Paul - AMBER/GREEN

Quartix Technologies plc (AIM:QTX), a leading supplier of subscription-based vehicle tracking systems, analytical software and services, is pleased to announce its audited results for the year ended 31 December 2023.

This 10-minute video from Quartix’s Exec Chairman (and founder) Andy Walters is a good summary, with useful slides, outlining the main points.

Revenue up 8.6% to £29.9m

(revenue growth of 10.6% in the core fleet business has been partially masked [over several years] by a wind-down of its small insurance telematics division, now almost eliminated)

Adjusted profit before tax decreased by 12.2% to £5.1m (2022: £5.8m) - mostly blamed on operating losses from a failed acquisition (Konetik) made by former mgt.

Statutory loss (first in the company's history) of £(0.9)m caused by £3.8m provision to replace old 2G boxes in France, and a £2.7m goodwill write off re Konetik.

Adj diluted EPS down 20% to 8.74p = PER 18.6x

Dividends cut to a total of 3.0p, down from 10.15p (incl specials) for 2022.

What went wrong? Well explained previously, and in today’s results - former management are blamed for a poor acquisition, which is now being dealt with. So that’s a temporary issue, which doesn’t worry me. Secondly, former management lost focus on the core business.

What’s being done about it? The founder returned, and is implementing a straightforward back to basics strategy -

Accelerate growth

Konetik acquisition - eliminate future costs

Lower manufacturing costs to improve gross margin on kit

Improve product features

Stop price erosion with RPI increases in contracts

That all sounds completely sensible to me, and should allow profit to recover, and divis to return to the previously generous levels of the past.

Outlook - sounds confident -

We have started the new financial year positively, with new installations in January approximately 10% ahead of the same period in 2023. This, alongside the opportunities for continued growth in all territories, and particularly in Continental Europe, underpins our confidence for 2024 and beyond."

The Company believes that market expectations for 2024 are as follows: revenue: £32.1m ; free cash flow*: £3.4m ; adjusted EBITDA: £5.4m

* Note excludes expected cash expenditure of £2.5m on 4G upgrade programme during the year.

Balance sheet - only £2.3m NTAV, but it’s an asset-light, and cash generative business that pays out cash generated as dividends. Maybe it should keep a bigger cash buffer, for any future unforeseen problems?

Paul’s opinion -

Bull points

- High recurring revenues

- Sticky customers (SMEs) with long lifetime

- Historically high margin, and cash generation, with generous divis - unusual for a tech co

- Owner-managed still

- Large Director buy recently

- Turnaround plan looks highly likely to succeed, just going back to basics

- Bear points

- Price erosion & (low) customer attrition combined can offset new customer wins

- Loss of focus and a poor acquisition - but these are now being corrected

- EPS has been declining for 5 years - can this be reversed into growth?

- Valuation is still not cheap, despite big share price falls

- Substantial costs of mobile network changeovers, has hit profits several times

- Possible selling overhangs from institutions?

Overall, I suspect QTX shares could be getting near to the low point, although I like things to be astonishingly cheap, and sentiment on the floor, to coax me into buying. So I’m not sure risk:reward is quite good enough to make me a buyer, but I can certainly see a good turnaround here being the most likely outcome in the next few years. If growth in international markets really starts to take off, then this share could get a decent upward re-rating.

I’ll stick with AMBER/GREEN for now - moderately positive overall.

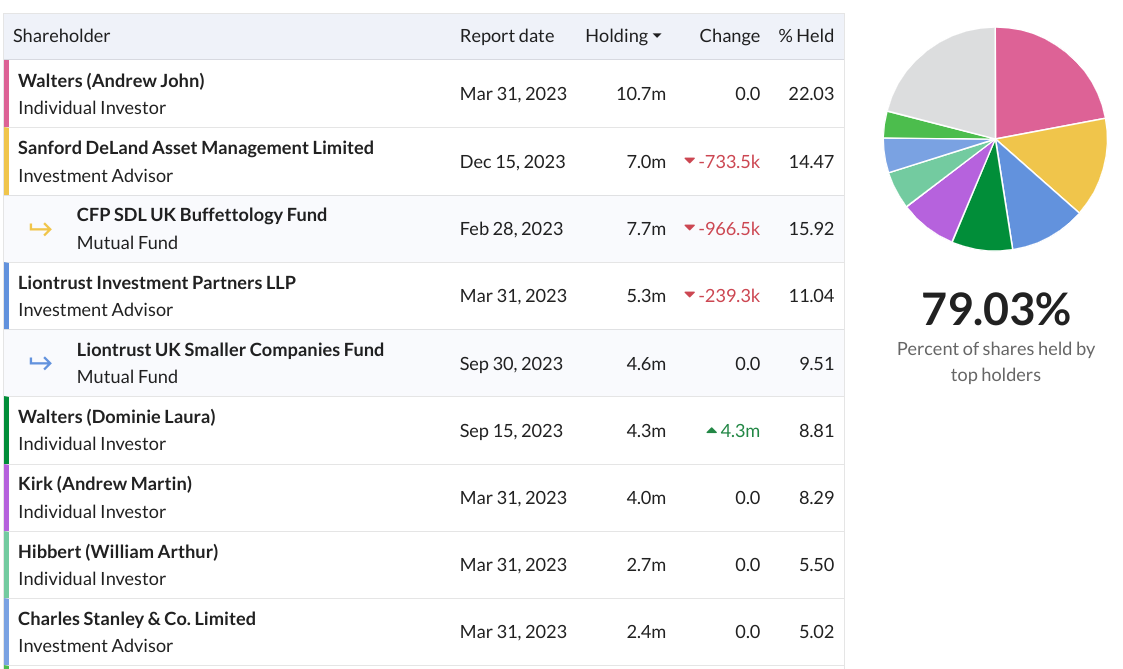

Shares have almost done a 10-year round trip, albeit with shareholders collecting generous divis along the way -

Not much free float, so QTX shares tend to be illiquid with a wide spread - note 2 instis seem to be sellers, especially SDL which has had a problem with redemptions -

Graham’s Section:

TT electronics (LON:TTG)

Share price: 136p (+0.6%)

Market cap: £241m

For over a year, I’ve been positive on this “global provider of engineered electronics for performance critical applications”.

But the market hasn’t been too impressed by it:

Things weren’t helped by a profit warning which we covered here in November. Adjusted PBT for 2023 would hit the lower end of the range (c. £43m), due to the breakdown of some machinery in its “Sensors and Specialist Components” division.

The investment thesis at TTG is that the company will successfully deleverage (net debt last seen at £139m), and this will get its valuation back to a more respectable level:

Today’s news should be positive from that perspective. The company has:

…reached an agreement to sell three business units within the GMS (GN note: Global Manufacturing) and Power and Connectivity divisions to the Cicor Group for a cash consideration of £20.8 million on a cash and debt free basis, subject to normal completion account adjustments.

Two of the units being sold are in the UK, while the third is in China.

The buyer is listed on the Swiss Exchange (ticker: CICN) and is not actually bigger than TTG, either in terms of revenues or market cap. But its balance sheet is probably much safer!

The benefits of the disposal to TTG are:

£20.8 cash consideration will be used reduce TT’s existing debt

“Expected operating margin enhancement of c. 50-70 basis points”

“Simplified operational footprint”

Comment by TTG CEO:

"We are focused on being a more profitable and resilient business underpinned by a strong balance sheet and operating in attractive growth markets.

This simplification of our portfolio will further improve our financial profile and allows TT to focus on delivering value to our stakeholders by focusing on our core growth markets, strengthening the balance sheet and driving margin progression. Today's announcement demonstrates our disciplined approach to our portfolio and provides a good home for our colleagues transferring to Cicor.

Graham’s view

As a general rule, stock market investors should be pleased when their CEOs choose to make principled divestments. Incentives for management teams usually guide them away from reducing the size of their empire.

Secondly, as disclosed in today’s RNS, the units being sold by TTG haven’t been contributing much towards profitability. For a start, their disposal will increase the operating margin of TTG as a whole. And in 2022, they contributed a small pre-tax loss despite aggregate revenues of £72.5m. So I’d hope that this disposal might help to improve TTG’s quality metrics in 2023 and beyond.

I was hoping that TTG would deleverage by itself, using its own profitability, but I can’t really complain about a c. £20m disposal to help speed the process up. Especially as it seems the units being sold weren’t contributing much to the financial performance of the group as a whole - hopefully they can be improved in the hands of their new owner.

So I’ll keep my positive stance on these shares. With c. £43m of PBT in 2023 and now with the help of this disposal, I’m hoping for a very meaningful reduction in net debt. Perhaps the market will then start to treat these shares with a bit more respect?

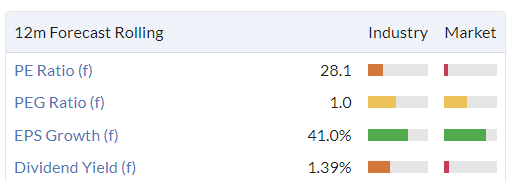

Craneware (LON:CRW)

Share price: £21 (unch.)

Market cap: £743m

Craneware (AIM: CRW.L), the market leader in Value Cycle solutions for the US healthcare market, is pleased to announce its unaudited results for the six months ended 31 December 2023 (H1 FY24).

I’ve had a call with the management at Craneware this morning so my thanks to them and to their advisors at Alma for setting this up.

Craneware is a highly rated stock whose valuation has more than doubled from the low it was at last year:

Before giving you the bullet points from my management Q&A, here are the interim results highlights:

Revenue +8% to $91.2m

ARR +3% to $171.4m

Adjusted PBT +8% to $17m

EPS +4% to 42.8 cents per share (33.8p per share)

As for cash and debt, the company reports cash reserves of $64m vs. total bank debt of $59m.

I asked the company about its cash/debt strategy in my previous Q&A with them. They signalled at the time that they were comfortable with the small net debt position they were carrying, but that they may seek to pay down some of their debts early - which they have now done.

Operational highlights summary:

Positive response to new "Optimization suites” for hospitals.

Customer retention over 90%

Partner programme contributing to revenue growth (3rd parties now using Craneware’s data platform Trisus).

Outlook is in line with expectations.

“Market backdrop strengthening with US healthcare and hospital customers re-focusing on their future”.

“Continued and growing high levels of contracted recurring revenue”.

CEO comment:

"Our growth in the first half of the year is tangible evidence of the return of healthcare providers' focus to their strategic priorities and their increasing investment in technology to provide the insights to achieve them.

"Through our investments in the Trisus platform, Craneware is well positioned to support our customers in this transformation of the business of US healthcare, providing us with a sizeable opportunity and growth lasting for the long term.

"We have entered the second half of the year with good sales momentum and focus. We remain confident in the delivery of results for the year in line with current consensus, further growth acceleration over the near term, and our ability to create further long-term value for all stakeholders."

Management Q&A

Many thanks to Keith Neilson (KN) and Craig Peston (CP) for answering some questions for me.

Sales momentum - KN pointed out that “sales”, revenue and ARR are growing at different rates in accordance with the accounting rules and revenue recognition. Sales agreements might grow quickly, but then revenue and ARR will be lagged as it takes time for the revenue to be recognised and for it to be recognised within recurring revenue. The argument being made is that while ARR growth was 3% and revenue growth was 8%, the underlying sales momentum points to these growth rates picking up in future periods.

Revenue from 3rd party businesses using Craneware’s platform - Craneware has collected a vast amount of data on its platform (“200 million unique patient encounters”) and it has recently found new ways to monetise this. Examples given include pharmacy businesses reconciling cash movements, distributors using the platform to solve logistics problems, and other software companies plugging into it with their own solutions. This is still early-stage but the company is keen to continue growing this source of revenues.

Healthcare customers, current economic conditions - the US healthcare system is now in a post-Covid environment and while the effects of that era haven’t completely lifted, more than half of Craneware’s customers are now thought to be profitable again (and therefore in a position to invest for the future).

Growth profile - about 80% of sales growth is sales of new products to existing customers, whereas 20% of sales growth is from new customers (who in future periods will contribute to that 80% growth). The Optimisation Suites are an important source of growth: this is where individual products are packaged together to solve particular problems.

Competition? KN acknowledged that individual products have competitors, but said that the overall Craneware platform did not have competition. In terms of market share, the company estimated that 40% of US hospitals have been reached as a “landing point”. In terms of individual product categories, Craneware is thought to be the largest in the three core categories of Strategic Pricing, 340B and Pricing Integrity.

Financial strategy - with investors in mind, management were keen to point out that the company has reduced its debts and offers a modest but well-covered progressive dividend yield (yield is 1.3% according to Stockopedia).

Graham’s view

My personal stance on this company has been neutral, on valuation grounds. I would normally expect higher revenue growth from such a highly-rated company:

The share price gains over the past 12 months suggest that I’ve been too cautious, but what of the future?

I think the company could generate upside for investors if:

Double-digit sales growth translates to sustainable double-digit revenue/ARR growth. Maybe a boom in healthcare spending, after a relatively quiet period over the past few years, stimulates demand for new and existing products from Craneware?

Other businesses could become highly profitable customers as they seek to use the enormous Craneware dataset and platform.

Valuation: the market cap translated to dollars is c. $940m.

Net cash is approximately zero so let’s use this figure as the enterprise value.

With an ARR of $171m, the company is therefore trading at about 5.5x ARR.

In a US context, I think that this would be considered quite ordinary, i.e. still offering plenty of upside if the company outperforms or turns out to be of higher quality than the average software stock.

Personally, I would look for better bargains than this, but I remain impressed by Craneware’s progress.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.