Good morning from Paul & Graham!

Weekend podcast - went up on Sunday. I was pleased with this one, some interesting stuff in it, even if I say so myself! See Friday's SCVR here for the mystery shares (3 of them last week). I'll also add a reader comment below to list the mystery shares (my best ideas from the week).

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

WANdisco (LON:WAND) (Paul holds)

1318p (pre market open)

Market cap £911m

This is self-explanatory -

As a dual UK and US headquartered technology company, WANdisco has long-stated its intention to consider an additional listing of its ordinary shares in the United States. The company can confirm that it is in the early stages of proactively exploring this option.

The Company also confirms that it remains committed to London's Alternative Investment Market ("AIM") and to maintaining its current UK AIM listing.

My opinion - I met management last week, with the overall picture being the same as my previous comments here on the company. The story is that it’s won a series of big contracts (which take time to convert into revenue) over the last c.9 months. WAND has special software for handling & moving large amounts of data, and it claims to be the only software capable of doing so accurately. With the proliferation of data caused by 5G, WAND says its software is now in big demand, initially from telecoms and car manufacturers.

If even part of what the super-bullish CEO claims for the company actually happens, then this company could become an important player in the infrastructure of the internet.

As the RNS says today, it’s been an open secret that WAND was considering a US listing.

Ironically, the UK has attributed a lofty valuation to WAND, whereas usually the complaint is that the UK markets are not liquid enough & don’t match the sky high tech company valuations that the far deeper liquidity of the US markets enable.

It will be interesting to see if WAND shares continue rising on this news. It’s interesting how private investors seem generally sceptical about WAND, and it is far from being a bulletin board favourite. Will that change I wonder?

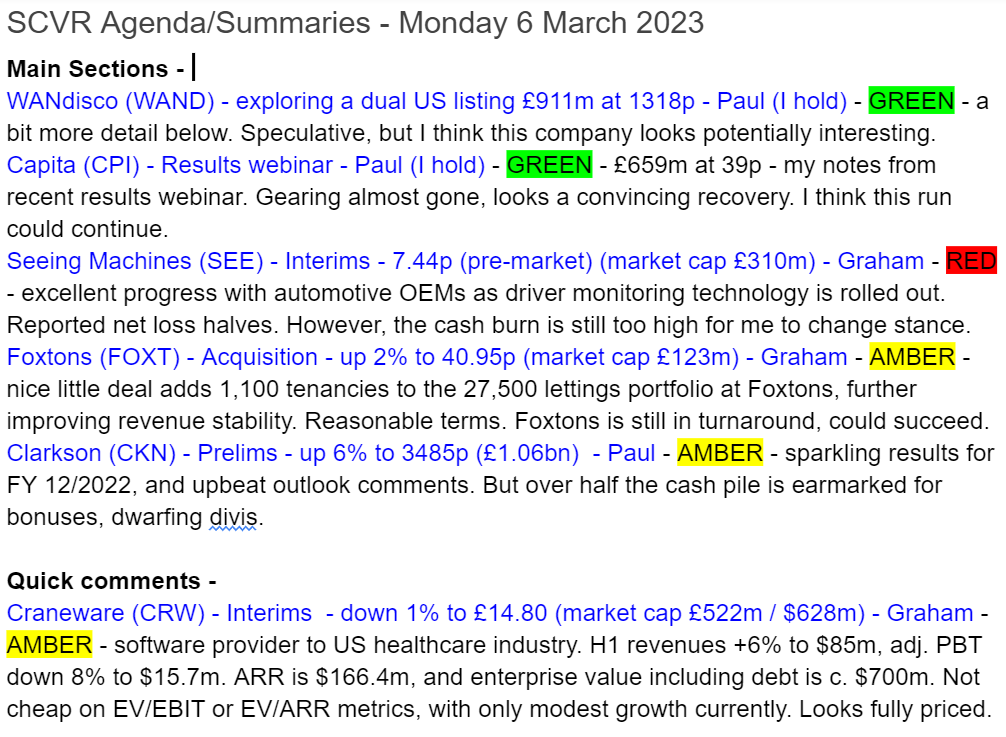

I remain intrigued by this share, with the contract wins having convinced me to buy. I’m sitting tight, and see this as a fairly speculative position, because it has had false dawns in the past. A value share, this is very much not! Past performance has been diabolical, so it's the future that investors are buying into.

It's been a 5-bagger in the last 12 months. Looking at the longer-term chart below, you can see where it promised the world, and failed to deliver before. Hence why I'm holding on to some scepticism, and not going in too big with my position sizing for my personal holding in WAND -

Capita (LON:CPI) (Paul holds)

39p (Friday’s close)

Market cap £659m

I flagged this share on Friday as looking like a potentially interesting recovery share. This weekend I did a bit more digging, but am still only part way through my research process. Previously I rejected Capita as way too high risk. Indeed, re-reading my notes here from Nov 2020, Capita looked insolvent, with a balance sheet that had negative NTAV of a staggering £(1.6)bn.

Since then, the group has been transformed, with loads of disposals, and only small dilution from new share issuance. The balance sheet at end 2022 was still quite weak, but NTAV was £(360)m, a dramatic improvement.

Net debt has also been almost eliminated, and is expected to move into net cash by mid-2023, with further smaller disposals.

The financial risk has almost gone, so it’s a completely different investment proposition now, and it looks quite appealing to me.

I made the following notes of the main points whilst watching the recording of this webinar, for FY 12/2022 results -

Moved into profit

Positive free cashflow

Big disposals almost eliminated net financial debt down to £85m, with remaining disposals expected to at least wipe out this remaining debt later in 2023

Resilient business, with long-term contracts & very high renewals rate of 97% - which it says proves the quality services provided

CEO describes his 7 years at the helm thus - 2018-21: transformation, 2022: stabilisation, 2023: acceleration

Good pipeline of new contracts

Capita Public Service division: £1,445m revenues, £91.5m operating profit, a decent enough 6.3% margin

Capita Experience (which seems to be private sector clients): £1,151m revenues, £38.5m operating profit, a lower margin of 3.3%

Pension deficit funding - now £30m pa, due to fall to £15m pa. Now in accounting surplus, and the CFO reckons the 2023 actuarial valuation is likely to also be in surplus. So it looks as if the pension deficit should be permanently resolved in perhaps 2024.

Capex - being spent better now, “capex goes a lot further now” (CEO)

Cost reductions continuing, including making more use of its outsourcing (IT, etc) operations in Poland, S.Africa, and India

EBIT margin of 2.9% expected to “at least double in medium term”, CFO warned not to expect too great a step change in 2023, so this will be gradual

Revenue growth guidance in next few years, is c.5% pa

Cash generation in 2023 likely to be similar to 2022’s £99m

Embraced hybrid working for staff, lowers office costs, and reduced absenteeism

CEO - key phrase used, “We’re NOT going to repeat the mistakes made in the past”

UK public sector - Capita has 10% market share, with strong growth potential

All contract renewals saw improved terms, and two thirds of contracts already have in-built protection against higher inflation. CEO reckons they can be more aggressive on pricing in future

Experience division - large, growing market. Book to bill was 1.2 in 2022

AI based innovation is important & growing. Gave example of Scottish Power new contract, using chat bots, customer “delighted” with the service

Going concern - auditors “material uncertainty” view was eliminated in latest results. CEO praised CFO, who rebutted this, saying it’s the strong cash generation (mainly from disposal of Pay 360) which caused this to no longer be required - seems a good dynamic between the CEO & CFO

Dividends - not yet committed to anything definite, but it seems obvious that divis will resume in 2023, since it should reach a net cash position

Summary - I think this looks very interesting, with possibly a lot more scope for this share to re-rate further (if I had to guess, 70p strikes me as possible, with patience, versus the current 39p)

Plan to double EBIT margin from 2.9% to c.6% would itself drive share price a lot higher, I reckon

“De minimis” financial debt now expected by mid-2023, maybe even net cash - that’s totally transformed from a couple of years ago, and it seems to me this could now be driving a re-rating of Capita shares

Pension deficit - pretty much sorted, on both accounting (already in surplus £40m), and soon to also be actuarial basis, probably

Inflation protection already in most contracts

Upbeat outlook comments

Dividends due to resume this year, probably

Put that lot together, and I suspect we’re seeing a sustainable re-rating in this share, and it still looks cheap. Whereas just over 2 years ago, it looked like a complete basket case.

Overall then, it gets a thumbs up from me, but I do want to reiterate that it’s a large complex business, so I’m a little out of my comfort zone analysing this.

Note the StockRank is quite high, at 84.

I am ignoring the weak Z-score, because recent disposals have resolved the previously over-geared balance sheet.

Clarkson (LON:CKN)

3475p (up 5% at 09:22)

Market cap £1.06bn

Tremendous figures announced today for this shipping services group, for FY 12/2022 -

At 3475p per share, that makes the PER on FY 12/2022 earnings 13.9x which seems reasonable.

Are earnings sustainable though? Or has this been a boost from all the pandemic-related disruption to shipping? That’s the key question.

Outlook - this is encouraging, with Clarkson suggesting it has favourable market conditions for some time to come -

"Whilst the global geo-political outlook for 2023 and beyond remains uncertain, the green transition is driving significant activity in our industry. This, coupled with a supply and demand balance that will create meaningful supply-side constraints supporting the market, and our strong forward order book, gives us confidence in the outlook for Clarksons."...

Whilst there are considerable uncertainties in the geo-political landscape, we are confident that supply-side constraints brought about by years of underinvestment and the pressure on shipowners and charterers to decarbonise, will provide significant opportunities for Clarksons long into the future.

Balance sheet - my obligatory check of the finances. This looks very good at first sight.

NAV is £413m, take off £189m intangibles (so it’s done some hefty acquisitions to accumulate a figure this big), and NTAV is still decent at £224m.

There’s a big cash pile of £384m gross, although given the large trade creditors, it looks like a fair bit of that will be client cash - does the company earn interest on that now, I wonder?

There’s a small accounting surplus of £15.8m for the pension scheme.

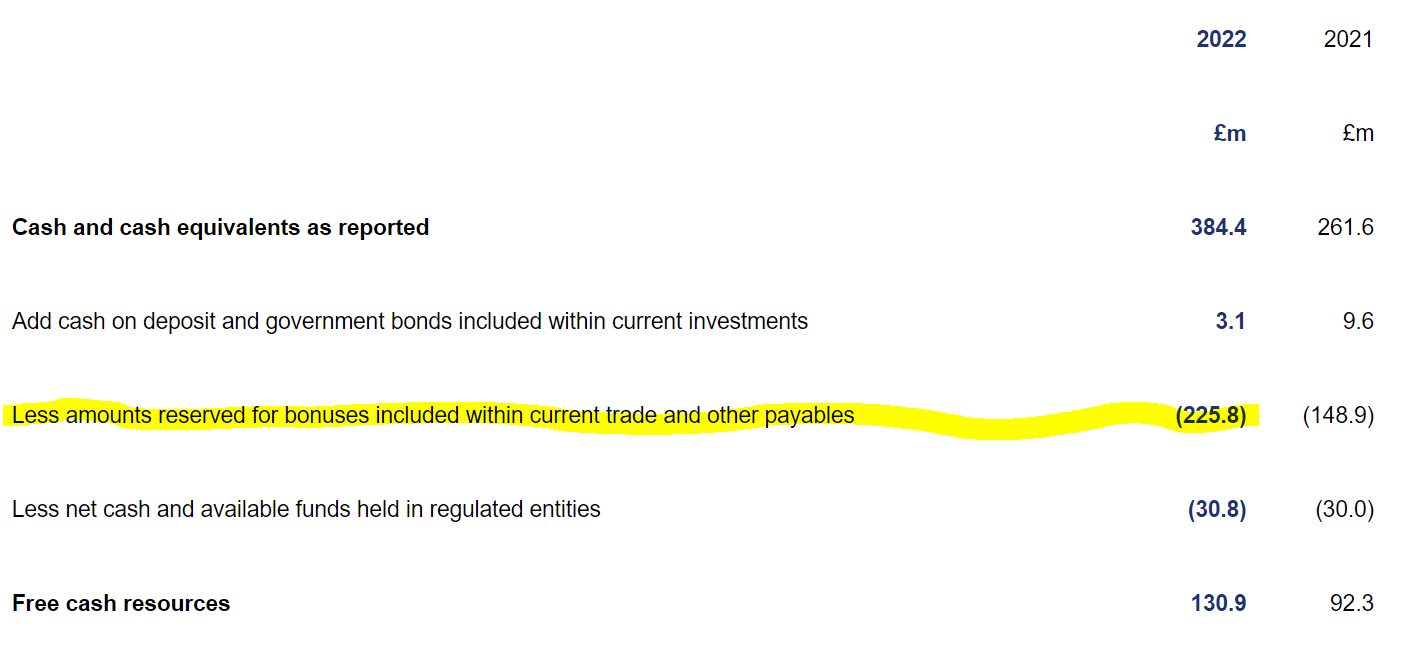

On digging a bit deeper, I’ve found something rather alarming in the notes, right at the end, it says that most of the cash pile is due to be paid out in bonuses, a colossal amount!

I also note from the cashflow statement that £20.4m was spent buying shares for the employees’ ESOP. Plus an £88.8m increase in the “bonus accrual”. This dwarfs the cash paid to shareholders, divis of £25.9m.

My opinion - I was going to conclude positively, until I found those massive bonus numbers, which does make me wonder for whose benefit this company is run?

If more than half the cash pile is to be paid out in bonuses, dwarfing divis, I would find this very challenging to invest in.

Hence I’m obliged to raise the questions about Clarkson, and hence can only mark it as amber.

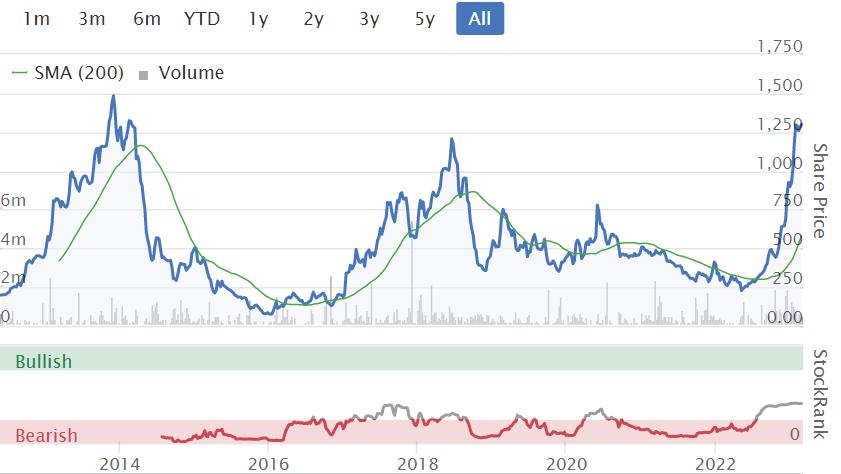

Shares have zig-zagged sideways for the last 5 years, but the longer term trend is good.

Also note that Stockopedia likes it, with a strong StockRank-

Graham’s Section:

Seeing Machines (LON:SEE)

Share price: 7.44p (pre-market)

Market cap: £310m ($373m)

This describes itself as “the advanced computer vision technology company that designs AI-powered operator monitoring systems to improve transport safety”. We last covered it in October.

I don’t normally spend too much time covering cash-burning, blue-sky type companies, but this one has a market cap of over £300m and so it has clearly captured the imaginations of some investors.

Today’s interim results are presented in US dollars for the first time (previously Australian dollars - the company is headquartered in Canberra).

Highlights:

Revenue up 54% to $24.4m, led by strong growth in the “Automotive and Aviation” category. Revenue in the “Aftermarket” category declined.

Gross profit more than doubled to $15.5m

Net loss halved to $5.4m.

The cash balance finished H1 at $52.2m.

Convertible note: Seeing Machines has borrowed $30m under the facility I previously discussed (a convertible note that charges 8% and can be converted to equity at 11p). The company says it is “fully funded to deliver on its current business plan for the foreseeable future”.

Deals: the company now has “15 automotive programs spanning 10 individual OEMs, covering more than 160 distinct vehicle models”. The initial lifetime value of all of these deals is $321m.

The company’s technology is currently monitoring 46,000 individual vehicles.

Outlook for FY June 2023: in line with expectations (revenue $53.9m, EBITDA of minus $12.7m).

My view

I’m impressed by some aspects of this report. The net less halving to $5.4m is a big one: if losses and cash burn slowed down considerably, then I might have to review my negative stance on this stock.

But then I remembered that Seeing Machines capitalises lots of development costs, i.e. it keeps them off the income statement by turning them into balance sheet assets instead.

Today’s cash flow statement shows $11m of capitalised development costs, up from $8.6m in H1 last year.

Indeed, if I simply add the operating cash outflow and the investing cash outflows together, I find a cash burn (before financing activities) of $18.5m in H1, up from $16.9m in H1 last year.

So even though the net loss halved, the cash burn was the same for the six-month period.

Also, while the $52m gross cash balance is impressive, net cash is only $22m when you deduct the face value of the outstanding convertible note. This note is not due for repayment until 2026, which does at least give the company time. And there is always the possibility of conversion at 11p, which will negate the challenge of repaying it.

The progress on deals with automotive OEMs is undeniably impressive. However, based on the financial numbers, I’m going to have to retain my negative stance on this one. The cash burn is still too strong for me to do otherwise.

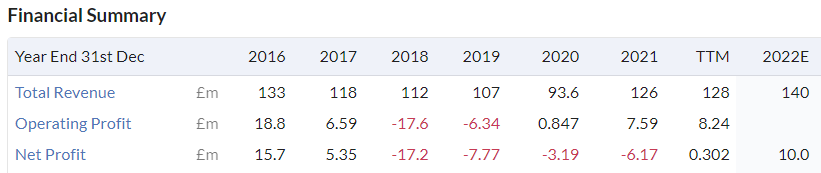

Foxtons (LON:FOXT)

Share price: 40.95p (+2%)

Market cap: £123m

This London estate agent announces the £7m acquisition of an agent with four branches in Central East London - Atkinson McLeod.

It’s not immediately obvious from their website, but Atkinson McLeod is very heavily weighted towards lettings with 90% of their revenues coming from that side of the business.

The strategic rationale:

The acquisition of Atkinson McLeod represents further progress against our strategy of acquiring lettings businesses that deliver an attractive return on invested capital, enhance earnings and improve the resilience of the Group's earnings, whilst also reinforcing Foxtons as London's largest lettings brand.

As we’ve discussed many times before, lettings management provides a very dependable source of income.

Foxtons remind us of their performance in 2022: “non-cyclical and recurring revenues, primarily delivered by lettings, represented c.65% of Group revenue, significantly enhancing the earnings resilience of the Group.”

The acquired business generated an operating profit of £0.9m on revenues of £3m in FY March 2022. Strip out some costs to increase profitability and the earnings multiple on this deal should be very reasonable. It has c. 1,100 tenancies under management (Foxtons has 27,500).

My view

While I like this acquisition, I haven’t got a strong view on the merits of Foxtons shares. It has had a difficult few years and can still be classified as a turnaround stock:

In “normal” property market conditions it should do very well, and maybe those conditions aren’t too far away. Revenue stability is also much better now, given the heavy focus on lettings. And it passes some of Stockopedia’s bullish stock screens:

So it could be worth researching in greater detail.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.