Good morning from Paul & Graham!

Today's report is now finished.

Podcasts - it was too hot here in Gozo for me to feel motivated to do anything energetic over the weekend, so I stayed in and recorded podcasts instead! Here we are, there are 2 for this weekend, with loads of (hopefully interesting) small caps news & views.

The burning issue this morning will be what happens at Metro Bank Holdings (LON:MTRO) - press reports are giving sketchy details of a deal having apparently been done, with an existing shareholding injecting more equity to take a controlling stake (at what price/dilution?) and apparently one level of bondholders taking a haircut. We'll look into the details once they are announced. Why anyone would want to be a small shareholder in a precarious bank, is beyond me - way too high risk. I discussed this one in the weekend podcast. What does impress me however is how fast regulators are now forcing refinancings at troubled banks - so far, preventing wider contagion. EDIT: apparently new shares will be issued at 30p, so not a bad outcome at all for existing shareholders, at first sight - but why did any small shareholders take the enormous risk, when they didn't have to?

Graham went into more detail on MTRO refinancing in his daily youtube show (recording here), flagging that he went AMBER on MTRO last week, because he thought the balance sheet numbers weren't bad enough for it to be a zero. Since a solvent solution for equity does seem to have been agreed over the weekend, thanks to a white knight investor buying new equity in what will be a controlling stake, then I suppose Graham's view has been vindicated! However, I maintain that risk:reward was terrible, since the positive outcome has only resulted in (at time of writing) a 16% gain in share price to 53p, which in order to have achieved this gain, shareholders ran a very big risk of a 100% wipeout. So regardless of outcome, risk:reward was terrible on this trade!

Reminder for Mello Monday - starting 17:00 tonight - 2 interesting companies presenting, both of which we've reviewed recently, Equals (LON:EQLS) and accesso Technology (LON:ACSO) . Also a guest interviewee, who David tells me has lots of interesting insights.

Graham's Youtube channel - I think it's fine to promote this here, as it's free, and Graham has confirmed he does NOT take any fees to promote individual companies (of course neither do I!) - our views are totally independent and honest, which can't be said of everyone giving views on shares out there. Graham's channel is a live show at 11:30 each weekday - not sure how long he'll be able to keep that up, sounds like a lot of work to me, to do straight after co-writing the SCVRs. It looks complementary to me, so I'll check it out myself when it starts shortly. He's going to mention MTRO in more detail I think, which saves me a job here! I think anyone putting out decent quality, independent content deserves our support & encouragement.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Summaries -

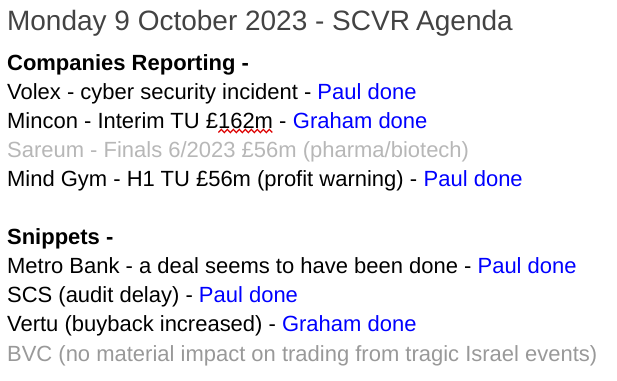

SCS (LON:SCS) - 167p (pre market) £56m - Audit delay - Paul (I hold) - GREEN

Audit delayed by a fortnight, but confirms results will be in line with previous trading update. So probably not a concern, but might trigger an attack of the vapours in this nervous market, who knows?! As audit delays are commonplace, and results in line, I'm sticking with my positive view from 3 August.

Volex (LON:VLX) - 310p (pre market) £563m - Cyber incident - Paul - GREEN

Reveals it has been hit by hackers, but reassures it's not impacted operations, and financial impact not material. So at this stage I'll give it the benefit of the doubt, although obviously unimpressed with IT security not being up to scratch.

Mincon (LON:MCON) - down 5% to 72p (£158m/€183m) - Interim Trading Update (profit warning) - Graham - AMBER

This is down by just 5% despite the 2023 EBITDA forecast being slashed by nearly 30% (the prior EBITDA forecast is not included in today’s RNS). Weak mining demand and some other issues are hurting performance; I still think this has long-term potential and I remain neutral.

Vertu Motors (LON:VTU) - down 0.7% to 70.8p (£243m) - Share Buyback programme - Graham - GREEN

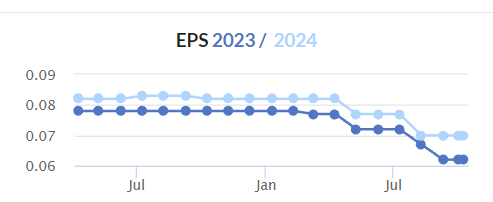

Just a quick note to say that Vertu is again enlarging its buyback programme. It originally announced a £3m buyback in May, then in June announced a further £3m. Today it announces another £3m! Paul observed recently that they had bought back 14% of the whole company in 7 years; the share count has fallen from a high of almost 400 million in 2018 to 341 million today. The stock trades at a PER of about 7x; I love to see companies at cheap valuations calling the market’s bluff and ploughing cash flow into their own stock. If they can keep this up, it has great long-term implications for EPS (so long as their underlying earnings power doesn’t fall off a cliff!). See Paul’s detailed comments for a longer discussion of the factors at play here.

(Paul adds - although bear in mind VTU took on a fair bit of debt to acquire Helston, so I'm a little surprised it's effectively using debt to fuel the buybacks, but it depends how you view it!)

Mind Gym (LON:MIND) - down 38% to 34.5p (£34m) - H1 Trading Update - Paul - RED

This looks a right can of worms! A big profit warning today, and scrutinising the last accounts, I see it's capitalising almost £5m of internal costs onto the balance sheet as development spend, with only a £740k amortisation charge! So the previous profits are not real (in cashflow terms). It's now set to burn through the rest of its cash pile by March 2024, according to Liberum. I would deploy my bargepole for this one. Pity, as it traded well pre-pandemic, but clearly has problems now.

Paul's Section:

SCS (LON:SCS)

167p (pre market) £56m - Audit delay - Paul (I hold) - GREEN

Says today that its FY 7/2023 results will be delayed from 10 Oct to 25 Oct.

It doesn’t give a satisfactory reason for the delay, but does reassure that the numbers will be in line with the FY TU (full year trading update), and that the board has “no concerns whatsoever”.

Paul’s view - audit delays seem commonplace at the moment, probably an overhang from the effect of lockdowns, with not enough trainees going through the system, I’m guessing.

Since ScS has specifically stated that the results are in line with expectations, then I’ll stick with my GREEN view, explained here on 3 August, with an in line TU, reassuring on order intake, and a cash pile larger than the market cap (which continuously rotates, it’s not a seasonal spike). I concluded it looked remarkably cheap, and has remained so! At least ScS shareholders can relax, knowing that they can ride out any downturn in demand, if one arises. Unlike DFS, with its crazily geared balance sheet (but much better brand and market share). [no section below]

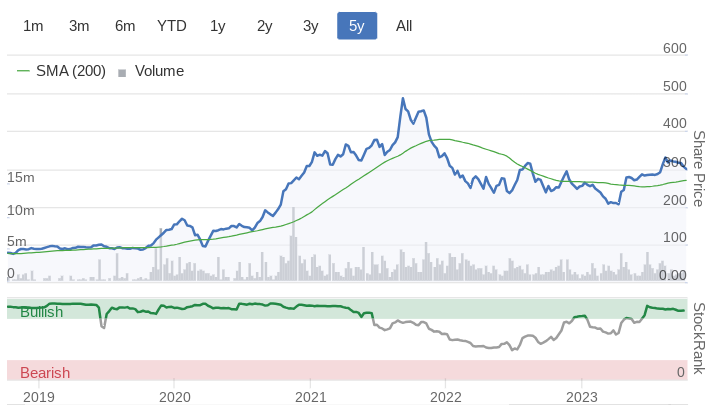

Is the chart forming a base I wonder? Note the consistently high StockRank -

Volex (LON:VLX)

310p (pre market) £563m - Cyber incident - Paul - GREEN

Another all-too-common problem is companies being hacked - I assume by fraudsters who demand ransoms in bitcoin maybe? Although I’ve heard some IT people say that successful attacks expose poorly managed, insecure IT systems, so it doesn’t reflect well on the company’s IT people.

Consultants have been brought in to investigate. Actions taken to stop unauthorised access. All sites remain operational. “Minimal disruption”, and “Group continues to trade…” (I should hope so!).

Key point is, “At this stage, any financial impact resulting from the incident is not expected to be material”.

It might cause a markdown in share price today, I imagine, but I don’t see anything serious enough to change my GREEN view of this expanding group, with shares reasonably priced, and its key sectors seemingly enjoying industry tailwinds - so hopefully we can avoid a profit warning here, but I can’t be sure about that.

Another one with a high StockRank -

Mind Gym (LON:MIND)

Down 38% to 34.5p (£34m) - H1 Trading Update - Paul - RED

Mind Gym (AIM: MIND), the global provider of human capital and business improvement solutions, provides a trading update for the six months ended 30 September 2023 and updated outlook for the year ending 31 March 2024 ("FY24").

H1 trading has been below expectations.

Blames customers delaying or cancelling spend, due to macro factors.

Cost-cutting is underway, to reduce overheads.

Capex in H2 also being reduced - I’m surprised to hear capex mentioned for a services business, so it looks like they’re maybe capitalising internal costs? Oh blimey, yes they are, big time! I’ve just checked the last accounts, and it capitalised c.£5m in each of the last 2 years of development spending, whilst only amortising £740k in FY 3/2023. This means profits turn into negative cashflow, in both of the previous 2 years. That’s enough to rule it out for me, so by all means skip the rest of this section, as I’m going to conclude negatively.

Revised guidance -

As a result, the Group expects to report H1 FY24 revenues of c. £21m, (H1 FY23: £26.8m) and a loss at EBITDA level. The Group now expects FY24 revenues and profits to be significantly lower than current market expectations even though we have seen an improvement in market activity reflected in increased bookings for Q3 versus the comparative period in the prior year. Our H2 performance is expected to be stronger than H1 with revenues broadly similar to, and underlying EBITDA margins ahead of, the respective levels in H2 FY23.

Liberum update - many thanks for crunching the numbers. It’s really bad.

FY 3/2024 revenue forecast drops from £62.6m to £48.4m

Adj EPS goes from 4.7p positive, to (2.0)p negative.

Forecast year end net cash revised from £8m to just £1m for March 2024.

Paul’s opinion - this is really bad. Before investing or holding here, you must look at the cashflow statements. These show the profits are not real! It’s capitalising a ton of payroll (development spending) onto the balance sheet. This is why it’s burning through the cash pile, despite reporting adj profits. With Liberum forecasting almost all the cash will be gone by March 2024, I suspect this share could have much further to fall.

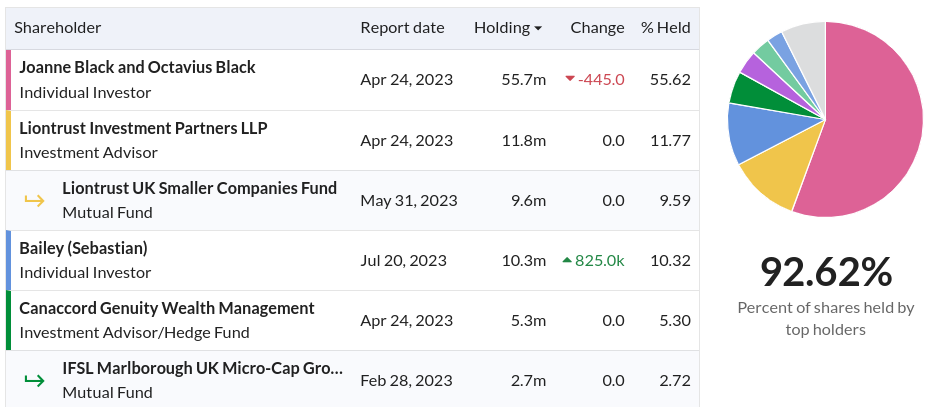

It’s owner-managed though, which usually means resilience, but it could also mean delisting risk, since the CEO owns 56%, with 2 other large shareholders meaning that the free float is small.

Historic performance before the pandemic was good though, so it’s not clear what’s since gone wrong. I’m not going to stick around to find out, as the numbers look dreadful to me, it’s a bright RED I’m afraid.

Note that Canaccord are known for brutally ditching stuff that they lose faith in, so I'd be worried to see them on the major shareholder list here -

A very poorly performing & disappointing float, to date -

Graham’s Section:

Mincon (LON:MCON)

Share price: 72p (-5%)

Market cap: £158m (€183m)

Mincon Group plc (Euronext:MIO; AIM:MCON), the Irish engineering group specialising in the design, manufacture, sale and servicing of rock drilling tools and associated consumable products, today provides a trading update for the period from 1st January 2023 to date, incorporating the nine months to 30th September 2023.

I last looked at this one back in May, taking a neutral stance as the company attempted to overcome some company-specific and macro challenges.

Unfortunately, this morning’s announcement is a profit warning. Revenues have “contracted” again in Q3. Year-to-date revenues (first nine months of 2023) are down 7% year-on-year.

The macro challenge posed by weakness in the mining sector is mentioned as an ongoing challenge. Additionally, “two large scale construction projects in North America… will no longer take place as planned”.

Other points:

Working capital position has improved, leading to an improved cash position.

Gross margin falls to 30.4% year-to-date (corresponding figure for last year: 32%).

Exceptional cost of €0.8m to implement a cost reduction programme.

Outlook:

In light of the above, looking ahead to the remainder of the year we now expect to deliver full year EBITDA of approximately €20 million. Our outlook for the medium term is positive, we will continue to invest, to improve our competitiveness within our current industries, and focus on delivering new opportunities in current and new industries to deliver better returns for the Group.

Estimates: according to a note published by Shore Capital in August, the 2023 EBITDA forecast at the time was €28 million. So the new EBITDA forecast of around €20 million is almost 30% lower.

The adjusted PBT forecast for 2023 falls from €17 million to only €8.8 million.

(It would be helpful if the RNS included the prior forecast in addition to the new forecast, as companies are increasingly doing these days.)

Graham’s view

Many thanks to Shore Capital for publishing their updated forecasts today. I’ve been neutral on this stock, admiring its long-term profitability while remaining cognisant that the company has had some difficulties over the past year or so.

Here’s a brief financial summary:

And here’s a summary of the difficulties faced by the company:

Supply chain: I think this is now resolved, with the company reporting today that it has been able to reduce inventory (although seemingly at the cost of some gross margin).

Freight conditions: Mincon previously resorted to using expensive air freight. There is no mention of this today and I believe it has been resolved.

Greenhammer project: this project ran into difficulties earlier this year. The interim results in August mentioned a new test being planned to take place in the United States. This is not resolved.

Demand from the primary market served by Mincon, the mining industry, remains in a slump and this problem is not resolved (but there is little that Mincon can do about it).

Net debt should improve thanks to the inventory reduction; it was last seen at €15m. This is partially resolved.

As you can see, it’s a mixed bag. Earnings momentum has been negative:

And valuation still isn’t as cheap as many other small-caps:

So for me, this is a name where I have to remain neutral. If it overcame its challenges, or if the stock ever fell into deep value territory, I think it would be very interesting, but I’m neutral for now.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.