Good morning from Paul & Graham!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Other mid-morning movers (with news) -

Renalytix (LON:RENX) - down 33% to 30.5p (£30m) - Interims issued. Multi-year cash burner, but only has $5.6m cash at Dec 2023. So it’s bust if it can’t raise fresh cash, says: “Raising funds… is essential”. Also looking at non-dilutive funding. Christopher Mills is Chairman & 10% holder. Will he be kind to small shareholders in the next fundraise?! RED for me - bargepole job until it refinances.

DSW Capital (LON:DSW) - down 32% to 41p ( £9m). Profit warning following bad performance in Jan & Feb 2024. Says M&A market has stalled, but it remains profitable.

Genus (LON:GNS) - down 18% to 1,750p (£1.15bn) - animal genetics co. H1 to Dec 2023 in line exps. Tough market conditions, esp in China. FY 6/2024 guidance revised to £58m adj PBT, Liberum says that’s 20% below its forecasts. Highish PER share, so can’t afford to disappoint.

MicroSalt (LON:SALT) - up 24% to 105p (£46m) - very recent (1/2/2024) IPO - patented low sodium salt. Announces partnership with ATI, “a leading US food and beverage export company”.

Jarvis Securities (LON:JIM) - up 18% to 60p (£27m) - announces 1.75p quarterly divi. Does this imply the situation here might be under control after recent problems? The market seems pleasantly surprised. EDIT: Graham has now written an additional full section on this.

Summaries

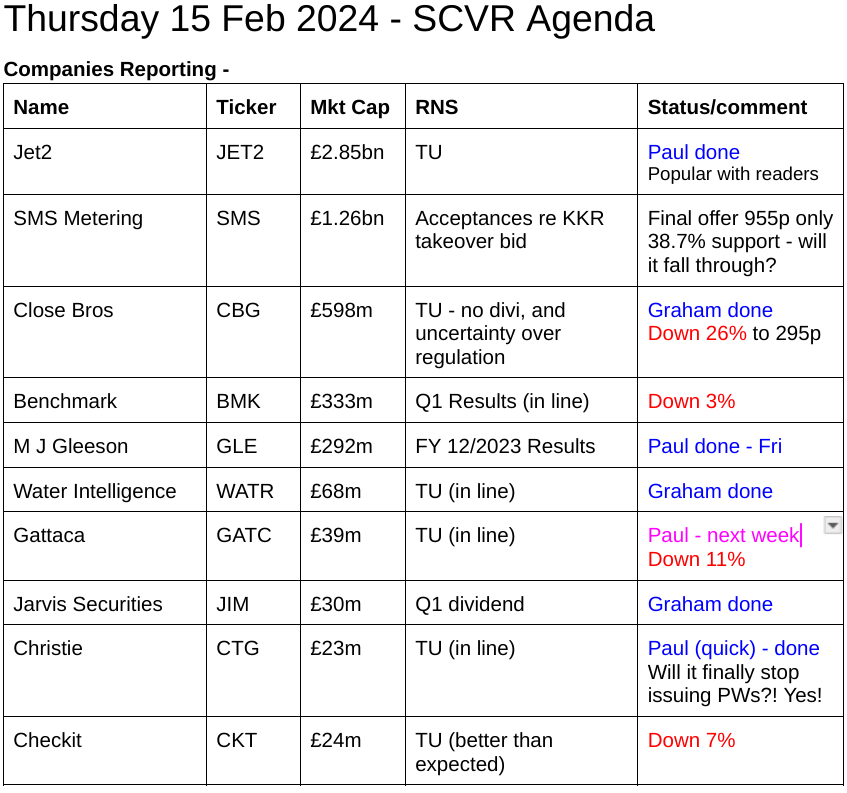

Christie (LON:CTG) - 85p (pre-market) £23m - Trading Update FY 12/2023 [in line] - Paul - AMBER

The profit warnings have finally stopped! No further reductions in guidance for FY 12/2023. More encouragingly, it says 2024 has got off to a good start. Overall, I can't see that much upside on the current share price, but it might have a bounce, who knows?

Water Intelligence (LON:WATR) - down 0.7% to 387.4p (£68m/$85m) - Trading Update - Graham - GREEN

Upgrading my stance to positive after an in-line trading update. WATR has a solid track over many years and yet shares trade at an enormous discount to prior levels (both in absolute terms and in terms of PER). Net debt of $7m is modest and the Chairman is well-aligned.

Jarvis Securities (LON:JIM) - up 33% to 68p (£30m) - Dividend Declaration - Graham - GREEN

The market breathes a sigh of relief as Jarvis declares a 1.75p Q1 dividend, after it failed to make a Q4 payment last year. A “skilled person” review will be delivered to the FCA by the end of the month, so we should hopefully get clarity on the company’s position soon.

Jet2 (LON:JET2) up 4% to 1,377p (£2.94bn) - Trading Update [ahead] - Paul - GREEN

A positive update today, with Canaccord raising its estimates for both FY 3/2024 and FY 3/2025. Shares have risen a lot in the last 3 months, but still seem good value to me. So a continuing thumbs up from me, if you're happy with the sector risk.

Close Brothers (LON:CBG) - down 26% to 295p (£444m) - Trading Statement and Dividend Announcement - Graham - GREEN

An enormous fall in the equity value here as Close Brothers admits it is vulnerable to an unknown, unquantifiable impact from the FCA’s review of historical commission arrangements for motor loans. The dividend is suspended. Amazingly cheap but high-risk.

Paul’s Section:

Christie (LON:CTG)

85p (pre-market) £23m - Trading Update FY 12/2023 [in line] - Paul - AMBER

Christie Group plc, quoted on AIM, is a leading professional business services group with 37 offices across the UK and Europe, catering to its specialist markets in the hospitality, leisure, healthcare, medical, childcare & education and retail sectors.

Christie Group operates in two complementary business divisions: Professional & Financial Services (PFS) and Stock & Inventory Systems & Services (SISS). These divisions trade under the brand names: PFS - Christie & Co, Pinders, Christie Finance and Christie Insurance: SISS - Orridge, Venners and Vennersys.

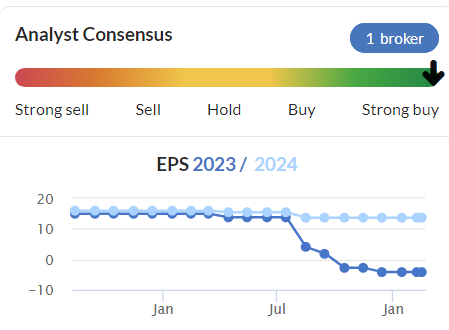

We covered this a fair bit in 2023, with a series of profit warnings, blamed mostly on project delays in its core property advisory business. As you can see below the EPS forecast collapsed into an expected loss of -4.2p for FY 12/2023, which is consistent with a note I have here from Shore Capital (many thanks) issued on 8 Dec 2023.

The static EPS forecast for FY 12/2024 looks suspect, as it’s unusual for companies to fully bounce back after a really bad year. I suppose it’s possible though, if delayed deals in 2023 do complete in 2024.

Today’s update confirms no further deterioration, which is something -

The Board of Christie Group plc (CTG.L) advises that, as anticipated, it will report an improved second half trading performance in 2023 compared to the first-half. The full year result, before exceptional costs, is expected to be in line with market expectations which were revised in early December.

2024 outlook - sounds more encouraging -

The Group is seeing positive and encouraging activity levels across its sectors at the start of 2024, with its UK transactional and advisory pipelines having now recovered to a significantly improved position from a year ago.

2024 for the Group has started positively, with particularly strong January invoicing in its UK agency and advisory business, Christie & Co.

Paul’s opinion - my view of the company was badly dented by the lousy performance in 2023, especially given that several competitors reported conditions being normal.

Is this business actually any good, especially given that performance seems quite erratic, and they’ve proven inept at forecasting?

Actually the historic track record isn’t bad. It’s usually profitable, and dividend-paying. I’m not clear why this company is listed, as it’s ex-growth and doesn’t seem to have a clear strategy to use the listing for anything.

There hasn’t been any dilution during the pandemic, so if it can get EPS back to historic levels of about 10p/share, then at 85p the share price would make sense at this level, possibly slightly higher.

I don’t see any great appeal overall therefore. There’s the chance of a trading bounce, on the more upbeat tone today, but the wide spread & illiquidity could make it difficult to make much money on this.

I’m lukewarm, so will go with AMBER.

Jet2 (LON:JET2)

Up 4% to 1,377p (£2.94bn) - Trading Update - Paul - GREEN

Jet2 plc, the Leisure Travel group, announces the following update on trading.

Trading for year ending 31 March 2024 (FY24)

Things are going well, with the conclusion -

… we tighten and slightly raise our guidance for Group profit before FX revaluation and taxation for the financial year to between £510m and £525m (previously £480m to £520m), which remains dependent on no material extraneous events in the balance of the financial year.

Trading for year ending 31 March 2025 (FY25)

This is much more vague, with no specific profit guidance, saying -

The Group will provide a further update in April 2024 and will announce its Preliminary Results for the year ending 31 March 2024 on 11 July 2024, which will include a fuller outlook for the all-important Summer 2024 trading period.

The rest of the commentary seems to be saying overall that forward bookings are “encouraging”, tempered by some cost increases.

Broker update - many thanks to Canaccord, with an unusually bullish note today, explicitly stating this share is significantly undervalued. I agree.

In EPS terms, Canaccord raises FY 3/2024 from 160.3p to 167.2p.

It also raises FY 3/2025 from 157.4p to 164.9p.

In both years that gives a PER of about 8.3x

I imagine there might be further upside potential on the FY 3/2025 forecasts, which seem modestly set considering demand is up. Holidays seem to be a high priority for households, something we’re hearing from other companies too, as people get back to normal post-pandemic, and want to do things we enjoy again.

Paul’s opinion - this is a good update today, with broker forecasts raised a bit.

I looked at JET2’s interim results here on 23 Nov 2023, in response to a lot of interest from subscribers here. I concluded very positively, when the share price was 1084p.

It’s risen a lot since, but the way I see it, JET2 has gone from ridiculously cheap, to just cheap now. So I’m happy to remain at GREEN, like last time.

Sector risk is something to bear in mind though - maybe some investors may want to eschew travel shares, as the whole industry can so readily be shut down if another pandemic were to happen.

Graham’s Section:

Water Intelligence (LON:WATR)

Share price: 387.4p (-0.7%)

Market cap: $85m

Water Intelligence plc (AIM: WATR.L) ("Water Intelligence" or the "Group"), a leading multinational provider of precision, minimally-invasive leak detection and remediation solutions for both potable and non-potable water, is pleased to provide a trading update for the year ended 31 December 2023…

This is an in line with expectations trading update.

Checking our previous notes on this one, I’ve been neutral but leaning towards taking a positive view on it, as it trades at much cheaper levels than it did before:

It’s a franchise type of business, making its own direct sales to customers but also having franchisees under its various brands. And it has a heavy weighting to the United States through its core business American Leak Detection.

Today’s news:

Trading in line “despite the sharp rise in interest rates and persistent inflation adversely shaping consumer spending decisions”.

Pittsburgh franchise is being bought back for $0.5m and will be operated directly by American Leak Detection rather than by franchisees.

Whenever a franchise company buys back a franchise, I tend to view it with mixed feelings.

On the one hand, it implies that the franchise business model isn’t working, which is unfortunate (as it’s such a profitable business model when it works).

On the other hand, it can also be a demonstration that the owner of the brand is determined to fix any problems that have arisen, which is a good thing for customers and for the long-term health of the brand.

What you definitely don’t want to see, as a shareholder, is a company buying back its franchises in order to pad its revenue figures.

With respect to Pittsburgh, this is what WATR says:

The Group believes that the Pittsburgh location was underperforming as a franchise and sees an opportunity to increase its growth trajectory.

I’m happy to take that at face value.

Financial highlights for 2023:

Network sales (all sales to customers, including by franchisees) up 3% to $170m (2022: $165m)

Revenue up 7% to $76m (2022: $71.3m)

PBT up 13% to $6.2m (2022: $5.5m)

US inflation was 3.4% in 2023, so you can see that WATR’s total network sales - including international sales - did not quite match inflation during the year.

But there are signs of operational leverage, with PBT still growing at a healthy rate.

Profit margins all increased, another positive sign.

Net debt is $7m after subtracting bank debt and deferred acquisition payments ($22.8m) from cash ($15.8m). I agree with WATR that this is a “conservative” positioning. They say they have “dry powder” for further investments!

Compensation in shares

We are told that:

Consistent with prior years, members of the Board have elected that they would prefer to receive their compensation in equity, in lieu of cash compensation for the year ended 31 December 2023, in order to benefit from capital gains as the Company executes on its growth strategy.

I’ve gone back to the 2022 annual report to see what happened then. Chairman DeSouza was paid $591k, but also received stock options worth $80k in lieu of cash.

So while this has been presented in an unusual way, I think it’s actually quite normal. Most compensation is still in the form of cash.

Chairman comment: it seems as if more franchise reacquisitions are on the cards.

Given our strong balance sheet and continued performance in generating profits, we are able to invest in capital projects that sustain our long-term growth: (i) strategic franchise reacquisitions to provide regional corporate support to grow neighboring franchisees; (ii) customization and implementation of web applications to promote operating efficiencies and upselling opportunities; (iii) new products and solutions for water and wastewater infrastructure problems.

Graham’s view

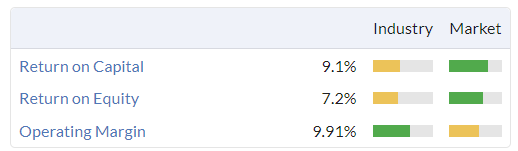

I remain impressed by the long-term trajectory here. I’m also interested in it by default, given the capital-light business model which in theory should lead to high returns. Although that hasn’t quite happened yet:

However, the latest results do show margins improving and I’m hopeful that this can feed through to higher returns over time.

The Chairman owns 28% of the company and I think he remains well-aligned with other shareholders.

Top-line growth has been a little slow but perhaps we can write off 2023 as a particularly difficult year.

The enterprise value (market cap plus net debt) is $92m, vs. PBT of $6.2m. Again, I feel that my stance here is finely balanced: should I upgrade my stance, or leave it neutral?

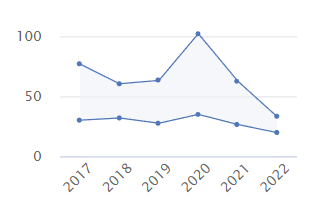

Checking the broker notes, I see that WH Ireland is putting it on a PER of 12x, versus a historical average of 20x.

Stockopedia also puts it currently at the bottom end of the range of its historical PER:

Given the consistent track record, I will upgrade my stance here.

Jarvis Securities (LON:JIM)

Share price: 68p (+33%)

Market cap: £30m

I’m not sure if I can remember such a positive response to a dividend declaration before.

The Board of Jarvis announces that it is declaring a first quarterly interim dividend of 1.75 pence per share, to be paid on 19 March 2024 to shareholders on the register on 23 February 2024 and the shares will become ex-dividend on 22 February 2024.

News flow from Jarvis has been quiet since 13th November, causing some shareholders to fear the worst:

We covered that 13th November update in some detail.

In particular, the company said at the time that there would be no Q4 dividend for 2023.

Given the ongoing regulatory reviews, it was reasonable for shareholders to be concerned that bad news was coming with respect to 2024 dividends. Perhaps trading could have deteriorated to such an extent that a dividend would be considered unaffordable, or perhaps the FCA might have objected to a dividend payment.

Those concerns are now shown to be unfounded, at least for the time being, as the company declares a 1.75p payout.

Last year, the company paid out 3p for Q1, but then it failed to pay anything in Q4 and the entire annual payment was 8.75p.

Therefore, I would say that 1.75p is a decent Q1 payment, giving the company scope to pay 7p-9p this year, if it can manage four quarterly payments. (WH Ireland have today reduced their estimate for JIM’s annual dividends in 2024, from 9.1p to 8p.)

We do badly need an update on the regulatory situation and on trading. There is a deadline for the current review to be delivered to the FCA by the end of this month. The dividend payment doesn’t tell us anything about the contents of this review, but it does seem to hint that the contents might not be damning.

For now, little has changed since my comments in November, when I cautiously gave this stock the thumbs up (at 56p). We now know the company is able and willing to continue making dividend payments.

On that basis, I have to leave my positive stance here unchanged. It may be high-risk given regulatory involvement but at the same time, the market is expecting PBT of £6.6m for 2023 (before regulatory costs of £1.3m). Given the £30m market cap, I remain optimistic for shareholders.

Close Brothers (LON:CBG)

Share price: 295p (-26%)

Market cap: £444m

This relates to last month’s FCA announcement regarding discretionary commissions for motor loans, whereby brokers could be incentivised to arrange loans at higher rates. These types of commissions are now banned, but the FCA is studying historical arrangements to determine whether some customers may be entitled to compensation.

Close Motor Finance may be affected; here is the latest from Close Brothers Group:

There is significant uncertainty about the outcome of the FCA's review, and the timing, scope and quantum of any potential financial impact on the group cannot be reliably estimated at present.

The market hates uncertainty, and the value of CBG shares is lower by £155m today.

The company was already trading at an astonishing valuation, even before this:

They provide reassurances around their financial strength: they expect to report £94m of adjusted operating profit in H1 (period ending Jan 2024) and have a common equity tier 1 ratio of 12.5%. Their liquidity is “comfortably ahead of both internal risk appetite and regulatory requirements”.

However, unlike Jarvis, they won’t be making any dividend payments. So the 17% yield in the above table is a mirage:

While there is no certainty regarding any potential financial impact as a result of the FCA's review, the Board recognises the need to plan for a range of possible outcomes. It is a long-standing priority of the group to maintain a strong balance sheet and prudent approach to managing its financial resources…

Therefore, the group will not pay any dividends on its ordinary shares for the current financial year, and the reinstatement of dividends in the 2025 financial year and beyond will be reviewed once the FCA has concluded its process and any financial consequences for the group have been assessed.

Graham’s view

I can understand why shareholders might be rushing for the exits. The danger of financial loss relating to this issue will have been known, but now the company is a) acknowledging that it faces an unknown, unquantifiable impact, and b) suspending its enormous dividend in advance of any loss.

Personally, I would be open to betting on Close Brothers here.

Let’s put it this way: today’s movement in the share price implies an additional £150m of expected costs/loss of economic value.

Before today’s fall, the market cap already made little sense if any reasonably stable performance could be achieved.

So if the potential penalties/costs relating to motor commissions amount to less than £150m, and if a reasonably stable performance is achieved in the coming years, then I think investors should do very well.

However, there is no getting away from the risky nature of it: nobody can tell how large (and damaging) any potential costs and penalties might be.

And for income-seeking investors, there is no telling how long we might have to wait before Close Brothers pays another dividend.

The July 2023 balance sheet showed £1.4 billion of tangible equity, several multiples of the current market cap.

I’m giving this the thumbs up, with a disclaimer that I view it as being even higher-risk than most shares I take a positive stance on!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.