Good morning from Paul & Graham!

Agenda -

Paul's Section:

Brief comments (no sections below):

Aeorema Communications (LON:AEO) (82p - £7m) [no section bellow]- Too small for us to cover in detail, but thanks to members Dieselhead2 and tiswas, for flagging up in the comments section below a positive trading update from this live events company, now guiding FY 6/2022 results to be £12.2m revenues, and £830k+ profit before tax. The commentary sounds upbeat too. I know 4 of the >3% shareholders, all shrewdies! So this looks worth a closer look.

Intelligent Ultrasound (LON:IUG) (13p - £35m) [no section below] - I reviewed this serial loss-making company here in May 2022, and could see some appeal, but overall it looks too high risk. Looks like it could run out of cash in 2023. Dilution has been massive already, with a 10x increase in shares in issue in the last 6 years, as it remained relentlessly loss-making and cash-burning. Today’s interim results is more of the same. Good revenue growth, but some of that is a one-off big order from the NHS. Cash is down to £3.5m. Risk:reward doesn’t look good to me.

Full sections:

Made.Com (LON:MADE) - confirms press speculation that it is looking at a possible equity fundraising. It's been a disaster since floating just over a year ago, collapsing by 95% in price already. I don't see any way out of this, other than a deeply discounted placing, to keep the lights on into 2023. Longer term, unless it can drastically slash costs, it's difficult to see this becoming a viable business, so likely to disappear in 2023 I suspect. Hence it remains uninvestable for me. Pity, as it looked quite an interesting company originally, before growth collapsed.

Angling Direct (LON:ANG) - it's a profit warning, due to a variety of fairly predictable reasons. Although the dry weather here and in Europe has also had an adverse impact on fishing conditions. Forecasts are trimmed, with adj PBT now only £1.5m for FY 1/2023. It's the cash pile that is of most interest, which is almost 3/4 of the whole market cap! That nicely underpins this share, even if trading deteriorates further, which it might.

Immotion (LON:IMMO) - several readers have been discussing this VR entertainment company's trading update in the reader comments, which got me interested. I've had a look, and think there could be something interesting developing here. Although my main concerns are the possible need for more cash, and a growth rate that seems a little pedestrian so far, and limited mainly to aquariums. That said, I can see good potential here, if management are able to accelerate growth. Worth a closer look.

Graham's Section:

Zytronic (LON:ZYT) (£13m) - this maker of display touch screens publishes a revenue warning for FY Sep 2022. The final outcome for the year is unclear but the profit result may only marginally exceed last year. The contrarian in me finds this one interesting: it has nearly half of today’s market cap in cash and the results of the past two or three years have been hobbled by the closure of the casino and other industries, along with supply chain disruptions. The company abandoned its sales and marketing efforts but has now restarted them and I wonder if it might be able to make a partial recovery towards its pre-Covid profitability. Very little success is priced in at current levels, for investors who are able and willing to buy shares in companies of this tiny size.

Inspecs (LON:SPEC) (£228m) - this eyewear manufacturer delivers interim results that disappoint the market with a fall in underlying EBITDA compared to last year. However, the statutory numbers point to financial improvements and it looks like 2022 is shaping up to be a good year for the company. The disappointments relate to delays at a new manufacturing site and currency translation issues that don’t look serious to me. Of greater concern is the valuation: the stock is trading at a premium of around 100% to net asset value, and that’s before making any of the necessary deductions for intangible assets. How the company will justify this in the long-run is unclear.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Made.Com (LON:MADE)

9.9p (pre market open)

Market cap £39m

Background - we’ve been following this sorry tale here at the SCVR, with one profit warning after another.

The last profit warning which I reviewed here on 19 July was a disaster, with the anticipated loss before tax of £80m (per Liberum forecast) for FY 12/2022. This update also said the company was “considering options… to strengthen its balance sheet” - fairly obviously an equity fundraising, because nobody would be likely to want to lend to it, and anyway debt doesn’t strengthen the balance sheet, NAV remains the same.

There was £31.5m in net cash at June 2022, forecast to drop to £5-30m by Dec 2022. So not terminal yet, but clearly heading that way.

My conclusion in July was that the business model has not been proven, and the high risk of a placing made MADE shares uninvestable. That was when the share price was 38.5p, and it’s now lost three-quarters of that already depressed price.

Remember that MADE floated as recently as June 2021, at 200p, so it’s already in the 95% club at 9.9p per share. To be fair, it looked an interesting growth company back then, with the story being that it was disrupting the traditional furniture market, and attracting trendy younger customers to its digitally native, quirky furniture offerings often from independent designers. The relatively small trading losses were explained as being due to expenditure to drive rapid growth - fair enough, if that growth continues. The trouble is, growth has now gone sharply into reverse (mainly due to consumer demand softening, and supply chain problems), and losses ballooned, which will clearly result in the previously comfortable cash pile rapidly disappearing.

Sky News (it’s always them, isn’t it!) blew the whistle last night, saying that MADE has called in advisers from PriceWaterhouseCoopers to -

help shore up its balance sheet as it weighs plans for a share sale to raise approximately £50m…

to examine cost-cutting and other restructuring options.

...weighs plans for a share sale to raise approximately £50m.

The launch of a cash call is not thought to be imminent, but is said to be likely to take the form of a placing…

Response to press speculation -

This morning’s update from MADE confirms that it is looking at possibly doing an equity raise -

Further to the Q2 trading update published on 19 July 2022, MADE notes the recent press speculation regarding the possibility of the Group undertaking a capital raise.

As indicated in the Q2 trading update, MADE is considering all options to allow it to strengthen its balance sheet. MADE confirms that these options include a potential equity capital raise. MADE continues to consider its options and a further announcement will be made if and when appropriate.

My opinion - none of this is a surprise, because the company had already told the market in July that it was looking at doing a fundraising. Hence I don’t see why today’s confirmation of the obvious should move the share price (it's down c.10% to 9p in early trades). Although market makers tend to mark things down at the open, so they don’t get hit by sellers.

The key question is, will MADE survive? It’s obvious that deep cost-cutting is the only way forwards, but can the business still operate with much leaner costs? If marketing spend is slashed, then it would likely wither away, due to falling sales. Fulfilment costs look very high, on looking back to its 2021 results. This is looking increasingly like a badly-run challenger that floated on a wave of optimism, rather than good economics. Whereas the more shrewd, experienced old timers in the sector are now looking likely to out-last this challenger, long-term.

From this point, it all hinges on what the existing shareholders are prepared to do. If the institutional shareholders are happy to back a fundraising, then they might want to protect the value of their existing shares. Although that seems unlikely to me, given that the largest holder’s stake, Level Equity Management LLC with 16.6%, is only worth £6.5m, so hardly worth defending for a fund that has raised $3bn since inception. It has only made 2 investments in the UK, being a mainly US-focused investor specialising in growth & tech companies, so is probably suffering badly at the moment, I imagine.

Hence I think the most likely outcome here is a deeply discounted fundraising, anyone’s guess on price - 10p? 5p? 1p? It could be anything. It depends on who is putting in the cash that MADE clearly will need to survive in 2023. Also a plan to slash costs would also be necessary to tempt investors, I think.

Overall then, I continue to see this an uninvestable, and there’s little to no value in the existing equity, which is likely to be heavily diluted. There are 395m existing shares. So to raise £50m, at a discount (say 5p per share) would require the issuance of 1bn new shares, increasing the share count by 3.5 times. If the price is 1p per share, then 5bn new shares would need to be issued, increasing the share count by over 13 times. And even then, the refinanced business would still be haemorrhaging cash, and likely to run out of cash again further into 2023.

It might not be able to find anyone to invest, because at the moment that would look like pouring money down the drain.

A miracle could happen though. Maybe someone might take it over, but even then, the price would probably be a token amount. Hence this share is just for gamblers at this stage.

No wonder the IPO market is dead now. It looks like the 2020-21 crop of IPOs were so poor, that the city might have killed off the golden goose. With many institutions now licking their wounds from over-priced, opportunistic floats like MADE, who would come back for more?! Still, buyer beware as they say in Latin. Nobody is forced to buy into IPOs. I wonder how many fund managers will want to dump these failed IPO positions in the market, so they don't have to be disclosed on year end portfolio reports?

.

Angling Direct (LON:ANG)

30p (down 18% at 09:48)

Market cap £23m

Angling Direct plc (AIM: ANG), the leading omni-channel specialist fishing tackle and equipment retailer, provides an update on trading for the six months ended 31 July 2022 ('H1 23').

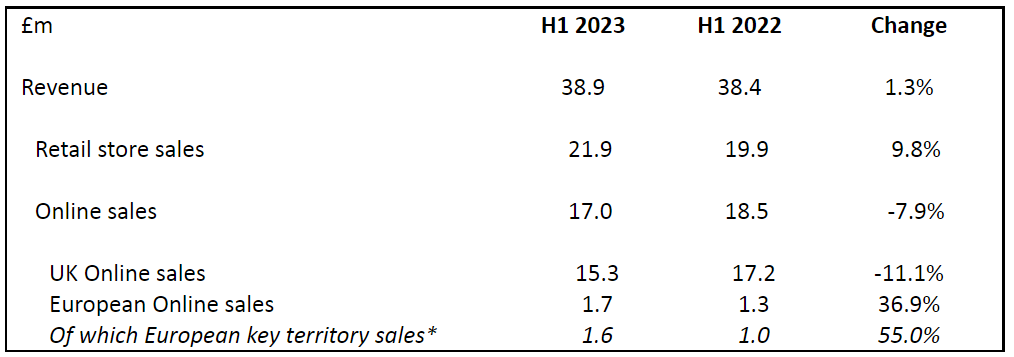

The highlights table provides a neat summary of H1 -

.

Note the shift towards physical stores, with online revenues down 7.9% - although still up 36% on the pre-pandemic level.

Total store sales rose +9.8%, and the more meaningful LFL growth (organic, i.e. before new store openings) was good, at +4.6%, helped by no more covid restrictions.

1 new store opened in H1, total now 43 sites.

Revenue growth trend from Q1 (Feb-Ap 22) to Q2 (May-Jul 22) deteriorated, from +5.4% to -1.6%

Net cash £17.1m at July 2022, amazingly that’s 74% of the market cap! A key bull point.

European expansion underway (attractive, highly fragmented market, ANG says), with a distribution centre opened in March 2022. Good growth, but from a low base.

Outlook - priority is to gain market share, in UK & Europe, implying that it’s not prioritising profitability as much.

Impact from cost of living pressures, consumer confidence, and cost inflation.

Dry summer has more recently impacted trading in August (adverse fishing conditions).

European heatwave has also impacted growth there.

Revised guidance - another one where they quote the meaningless EBITDA, it’s so annoying when companies do this, because EBITDA IS NOT PROFIT! -

As a result of these market headwinds the Group now expects to generate revenues marginally below current market expectations for FY 2023.

However, Pre-IFRS 16 EBITDA is now expected to be materially behind current market expectations for FY 2023 and in a range of between £3.0 million and £3.4 million.**

*Sales through German, French and Dutch native language websites

**Angling Direct believes that market expectations for the year ending 31 January 2023 prior to this announcement were revenue of £82.0 million and pre-IFRS 16 EBITDA of £4.3 million.

I don’t think that’s too bad. Guiding down from forecast EBITDA of £4.3m, to a range of £3.0-3.4m is disappointing, but not a disaster. The reasons given sound credible.

Many thanks to Singer for giving us more meaningful figures today. It forecasts using the bottom end of the company’s range for EBITDA, at £3.0m, which becomes £1.5m of adj PBT - this is the number I work on.

Adj EPS is 1.5p, so a PER of 20 at 30p per share. Not cheap, but remember when a three-quarters of the market cap is supported by its cash pile, then PER is not so appropriate.

Balance sheet - not reported today (other than the £17.1m net cash), so I’ve looked back to 31 Jan 2022.

ANG has a superb balance sheet. NAV is £36.4m, taking off £6.2m intangible assets, gives NTAV of £30.2m - that’s now about 31% greater than the market cap!

A lot of capital is tied up in inventories, at £16.3m, then there was a similar sized cash pile of £16.6m (now slightly higher, 6m later, at £17.1m).

The question is, whether the company is making good use of this capital, as it's only generating about a 5% return on NTAV (£1.5m profit before tax, on £30.2m NTAV)?

Trade payables are modest, at £8.7m, and the only other significant liabilities are the IFRS 16 lease entries, which net off to about nil versus the RoU asset - implying that pretty much all stores must be profitable, or at least not loss-making to any significant extent.

ANG clearly has surplus cash, which gives management firepower to do more acquisitions & continue expanding, and ride out a recession (whilst weaker competition goes bust maybe?), from a very comfortable position.

The main risk I see, is if management blow the cash on an unwise acquisition, but given their track record of being maybe too cautious, it’s probably not something to worry about. I can't help thinking that it might create more shareholder value to look at using the cash pile to buy an unrelated business in a lucrative sector, and build a mini-conglomerate? Or maybe buy another company that could be co-located in ANG's physical sites?

My opinion - this share is strikingly cheap, once you take into account its cash pile.

If management use the cash wisely, then there could be nice opportunities ahead to bolt on more earnings - e.g. from picking up assets from administrators (as e.g. Portmeirion (LON:PMP) announced this week), or opening new sites at very low rents.

Against that, it’s sensible to expect macro conditions to have some further downward pressure on sales in the more immediate future, possibly?

That said, despite today’s profit warning, it’s still trading profitably, and has a ton of surplus cash sitting on the balance sheet. Therefore I see this as a low risk way to get exposure to improving consumer confidence once we get through this cost of living crisis.

A key issue for online businesses (about half ANG is online) is online marketing costs, which seem to have shot up, as Google & Facebook (mainly) price gouge their customers to grab profit for themselves instead. These internet behemoths are like a global tax, flowing to the US. ANG doesn't mention this key issue today. I'm coming round to the view that having a hybrid operation - some stores, and some online business, may actually be a better idea, rather than online only, as operations can be merged in various ways (e.g. stores handling online returns, and dispatching goods where needed, rather than everything coming from a central warehouse). Plus if your customers are walking into a physical store, you can sell to them direct, rather than having to pay Facebook to give you access to customers.

ANG is not the best business in the world, but it looks OK, and above all has bulletproof finances, and a super-cheap valuation. So I like ANG, as a value investment. I appreciate it must be very frustrating to own this share, and see it relentlessly dropping. I know the feeling very well, but I think it's important not to sell in despair, as that would probably be at or near the low. We just have to be patient, and wait for good companies to interest other investors again.

We're back down to the early pandemic low again, which seems very surprising, with the fall looking overdone to me -

.

Immotion (LON:IMMO)

3.4p (up 5% at 11:25)

Market cap £14m

Some interesting posts (from fwyburd, Fegger, and Monty9 - thanks to them) in the comments section below caught my eye, so thought I’d take a look.

I’ve only previously looked at IMMO here once, in Dec 2020, and remember thinking it looked moderately interesting, but a bit early stage. Also obviously impacted by lockdowns, which are now abating for its indoor leisure activities, using Virtual Reality headsets.

I’ve had a quick look through the FY 12/2021 results, which show signs of something interesting happening (in H2 when pandemic restrictions were mostly lifted). Cash is getting tight, so they’ve decided to spin out the HBE and Uvisan startups, which require additional capital to develop them further. I doubt these are worth much, but could be a nice little bonus if IMMO is able to e.g. have a free carry, with an external investor providing the growth capital perhaps?

The focus is now on the core activity, Location Based Entertainment, e.g. providing immersive experiences at aquariums mainly, also zoos, etc. The revenue figures per headset (VR) are really impressive, over £20k per annum per headset. I think that might be gross, not the net figure that IMMO gets, it’s not clear? With only just over 400 headsets currently in operation, at a small number of sites in various countries (especially good to see the US being a main market) it’s easy to see how IMMO could really scale up this business, and have high margin, recurring revenues, with great operational gearing. I like this business model, and can see considerable potential! c.£10m revenues this year from c.400-500 headsets is pretty impressive. I reckon this is a business which could conceivably scale up say 10x over the long-term. That definitely gets me interested.

Here’s the latest update -

Immotion, the UK-based immersive entertainment group, is pleased to announce an update on recent trading.

H1 revenue up 91% to £4.4m (core business only) - but comparatives are soft, due to lockdowns. A better comparative would be H2 LY, which was £4.0m, so really just a 10% improvement in sequential half years.

“Very strong trading” currently, in July 2022, achieving £1.3m revenues (unaudited) - this is probably peak seasonality I would imagine.

Current trading in August 2022, “also started very strongly”.

Current portfolio is 54 locations, with 488 seats.

2 small installations done, at Chester Zoo (has anyone tried it?), and Legoland Philadelphia.

Pipeline doesn’t sound much, with only an expectation to “comfortably pass the 500 seat mark by the end of H2 2022” - I was hoping to see much more ambitious growth coming through.

“Advanced stage” discussions underway re spin out of 2 small, non-core operations. Possible upside here, but not a key reason to invest in IMMO.

Diary date - H1 results due out w/c 26 Sept 2022, so we’ll have a look at those in due course.

CEO comments - are upbeat, and I particularly like the comment re positive cashflow -

Martin Higginson, CEO of Immotion, commented: "The first six months of the year have shown solid year-on-year improvement and, with July exceeding all previous revenue numbers, the summer trading period is looking very encouraging.

"Demand for the Group's core LBE offering remains strong and, with solid operating cash flow generation from the key summer months, we are now well positioned for further installations and growth of the LBE estate."

My opinion - I like this company! There’s clear evidence that IMMO has found an interesting, and potentially lucrative niche in VR entertainment. Whether it can be scaled up, that’s the big question? At the moment, judging from its website, the sites seem to nearly all be aquariums. Although there’s also a gorilla trek, and a cartoon mermaid themed video about plastics in the sea.

Hopefully the actual roll-out of new sites (and enlarging existing ones) could be faster than indicated at the moment, I think it would take a material increase in the growth rate to get me more interested to a point where I’d want to allocate my scarce resources to this particular share. In a bull market, I would have bought some on a speculative basis.

I can see that each new site opened would add to the credibility of the company, acting as reference sites. The next thing we need to do, is look at customer reviews online, to see how these installations are being received by customers.

Overall, I think this looks potentially interesting, and worthy of a closer look, for more risk-tolerant, growth company small cap investors. We all need to have a little bit of fun in our portfolios! It looks to be close to breakeven now, so if it can break into profit, and not need another placing, that would be good.

.

Graham’s Section:

Zytronic (LON:ZYT)

Share price: 130p (-9%)

Market cap: £13m

I’m disappointed by how this company has performed in recent years: it was always a stock with lumpy revenues and its growth was always quite limited, but the revenue collapse over 2020 and 2021 took me, and the company, by surprise.

The company’s touch screens are used (for example) in casinos, and one of the effects of the response to Covid-19 was to cancel most of the orders that Zytronic would normally have received from this industry. Another was to disrupt the supply chains on which Zytronic relies.

And in addition to the problems caused by Covid-19, Zytronic has lost out on contracts related to ATM production. Long-term, the need for ATMs is reducing as more and more people go cashless. So even if these contracts had been won, they wouldn’t be a permanent source of profitability.

These major problems resulted in Zytronic becoming a much smaller business. Thankfully, the company did the right thing and reduced its share count: it offered £10m to shareholders in a tender offer at 145p (shareholders accepted £6.7m in aggregate) and also spent £2m on a buyback at an average price of 161p.

This was a cash-rich company and I’m glad to see that its funds weren’t wasted.

But what of the future? Let’s see what’s contained in today’s trading update:

As anticipated in the interim results statement issued on 17 May 2022, due to continued global economic disruptions, the availability and cost of both raw materials and electronic components have proven to be persistent challenges as the second half of FY22 has progressed. This has had a knock-on effect on the Group's customers and has resulted in a lower than anticipated level of order intake being observed over the second half to date.

The result is that revenues for FY September 2022 will only be 5% higher than last year’s £11.7m, i.e. revenues will be around £12.3m.

Forecasts published in May suggested that revenues would be £13.8m, an 18% increase on last year. So this is a significant miss.

And as for profits? “Although still a fluid consideration, profitability for the year is currently expected to be ahead of that reported at the pre-tax level for the year to 30 September 2021.”

Adjusted PBT was supposed to double from £500k to £1m and now it’s far from certain what the final outcome will be.

For an apparently ex-growth, publicly-listed company to be persistently unable to earn a meaningful profit is a worry - remember that the listing fees alone are a six-figure cost. This will be the third consecutive year without a meaningful profit (which I would define as over £1m in net income).

Cash - the year-end forecast is £6m, down from £7.5m at the interims. The company has been buying back its own shares and also talks of a working capital increase as sales and marketing activities resume “after a near two-year hiatus”. So for me, the decline in the cash is not a worry (obviously I would like to see the full-year financial statements to confirm this stance).

Outlook - management are still optimistic for future years:

With an improving log of opportunities and the ability to commit further resources to business development and project progression activities, management remains confident in the positioning, ongoing recovery, and longer-term growth prospects for the Group.

My view

I should mention that with a company this small, it would only be possible to purchase small amounts of it, and some of you may prefer to stick with larger companies as a rule.

Personally, I find this one quite interesting at the current level.

The enterprise value, using the latest cash balance forecast, is £7m. Maybe that’s fair given that adjusted PBT is likely to come in somewhere north of £500k. The question is whether management can turn things around and get this moving back in the direction of its pre-Covid profitability.

The ATM business looks like it is almost finished, but maybe there are still opportunities in casinos and in vending machines?

The key part of today’s update I would focus on is that the company says that its sales and marketing activities were essentially non-existent over the past two years (resuming after a “near two-year hiatus”).

If true, this means that the recent performance (especially considering the other Covid-related impacts) is not at all representative of what the Zytronic should be able to do in “normal” times.

With nearly half the market cap in cash, and the company having demonstrated a strong shareholder orientation by returning cash instead of wasting it during the bad years, maybe there is scope for patient shareholders to experience a nice recovery with limited downside risk?

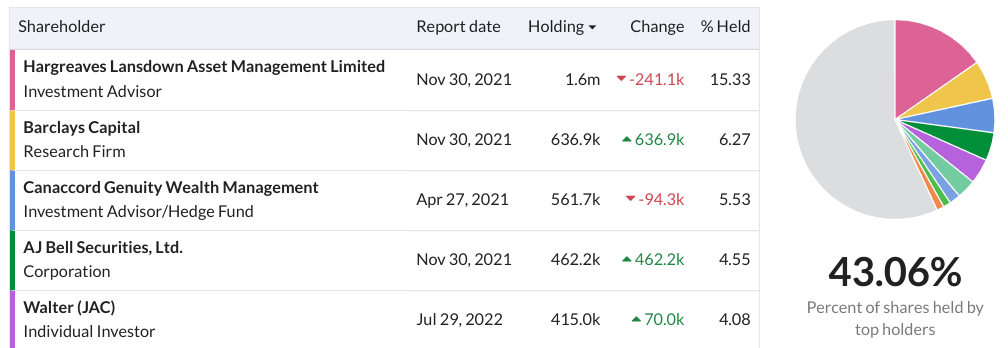

The major risk with a company this size is often delisting risk, if the big shareholders decided that it was no longer big enough to justify the listing. However, having checked out the top shareholders with the help of Stockopedia’s useful tool, I can’t see this one delisting any time soon:

Inspecs (LON:SPEC)

Share price: 224.5p (-6%)

Market cap: £228m ($273m)

This one IPO’d at 195p in 2020.

My IPO rule is simple: don’t buy them. I have seen so many of them go wrong, that I have learned to steer clear of them. The only time I broke the rule (I knew I was breaking it, at the time) was with DP Eurasia NV (LON:DPEU) and that experience only strengthened the rule.

I haven’t proven it numerically, but my experience is that nearly all IPOs trade at a very significant discount to their IPO price before too long. Maybe at a 50%+ discount, they are worth another look?

Inspecs is still trading above its IPO price - it even doubled in price at first, before coming back to earth:

It is “one of a handful of global companies which produce large volumes of the highest quality eyewear in-house for supply to the biggest retailers”.

Since listing, it has engaged in a spate of acquisitions, and is still digesting all of these additions to the business. If the strategy succeeds, there will be gains from increased negotiating power: Inspecs talks today of “Group companies working together to ensure enhanced distribution rates for our products”.

Financial headlines for H1:

- Revenue +10% to $138.4m (it was up nearly 16% at constant FX)

- Operating profit more than doubles to $5.8m

- Pre-tax profit $0.8m

- After-tax loss $2.8m

The company has three new factories: a relocated lens factory that is now fully operational, and two others (in Vietnam and Portugal) that are in development.

The underlying EBITDA figure, often the focus of City-based investors and analysts, failed to improve compared to H1 last year, and the CEO explains why:

- The lens factory “took longer than expected to reach optimal production following the move and as a result, we were not able to engage fully with our optical customers as delays were caused by infrastructure issues and the recalibration of machinery following the move”

- “…whilst our European business performed ahead of internal budget for the first half, our reported results were affected by a rapid decline in the Euro against the US Dollar.”

These are disappointments, sure, but the first is just a bump in the road while the second is an accounting issue that doesn’t necessarily hurt the business (depending on how revenues and expenses are spread geographically).

Net debt (excluding leases) falls to $26.2 million.

Outlook:

Our Group order books are ahead as of 30 June 2022 compared to 30 June 2021, and we enter the second half of the year in a good position. Whilst we remain cautious of the overall economic outlook for the UK and European market, we remain focused on executing a number of strategic priorities that will increase production, enabling us to bring innovative new products to market and continue to deliver shareholder value."

My view

Overall, this company has done well for investors since IPO and while today’s results have disappointed the market, they don’t signal any very serious problems to me.

My main question is around the company’s IP: does it have any proprietary, unique assets? Or is it better thought of as a manufacturer of commoditised products?

If it’s best thought of as a manufacturer, then we need to be careful with valuation. As a general principle, In the absence of IP, manufacturers shouldn’t trade far above their book values.

Inspecs has net assets of $134m according to today’s balance sheet, but this falls to just $15m if we exclude the large entries for goodwill and intangible assets. At a market cap equivalent to c. $270m there is a huge premium built in, and I’m not sure how it’s going to justify this.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.