Good morning from Paul & Graham! Today's report is now finished.

An energy support package for business was announced yesterday, which I've yet to go through in detail. The crux of it seems to be substantial reductions in gas & electricity prices for businesses, coming directly off their bills, for 6 months from 1 Oct 2022. That's clearly going to help. There's also talk of Stamp Duty, and other tax reductions in the pipeline. No doubt we'll get more detail in due course, and I'll keep my eyes peeled for what companies start saying about these changes in their forthcoming outlook comments.

Agenda -

We're looking at today's newsfeed, but also want to cover (today or tomorrow) 2 backlog items in particular:

Warpaint London (LON:W7L) - we've run out of time today, so this will have to be tomorrow.

Hostmore (LON:MORE) - oh dear, things are starting to look grim, I'm afraid. FY 12/2022 is now expected to be a (small) loss. Forecasts for a bounce in 2023 just don't look realistic to me, so I'm worried trading could deteriorate further, and the current -14% vs pre-pandemic revenue trend is worryingly weak. I'm now concerned about the high bank debt. Risk now looks high. Profuse apologies for how badly this has turned out, but the fundamentals have dramatically deteriorated this year.

Today's news -

Paul's Section:

Begbies Traynor (LON:BEG) - puts out an in line with expectations update for Q1 of FY 4/2023. Some interesting additional detail is provided. With earnings likely to be buoyant due to increasing insolvencies/restructurings, and a PER of 14, this share continues to look a sensible place to hide.

Smiths News (LON:SNWS) - a surprisingly good update for FY 8/2022 - ahead of market expectations. Stunningly low valuation now, with the PER below 3, and the dividend yield of about 15%. It won't last forever probably, but the valuation currently looks compelling for value investors. I'm tempted to buy.

Aquis Exchange (LON:AQX) - interim figures from this junior stock exchange fail to impress. Although it does have a nice balance sheet, with plenty of cash. There could perhaps be strategic value in the business? Based on these numbers, I can't get anywhere close to the current market cap though. So I'm afraid it has to be a thumbs down from me, on valuation concerns.

Graham's Section:

Judges Scientific (LON:JDG) (£496m) - good interim results and the full year is set to be “significantly” ahead of expectations. The broker raises its EPS forecast for the year by 15%, but only raises next year’s forecast by 5%. This is due to the lumpy nature of revenues at Geotek, the company purchased by Judges earlier this year which focuses on the analysis of geological cores. Geotek’s services are provided through a relatively small number of large contracts, making it difficult to predict revenues from year to year. Overall, Judges appears to be trading well in these conditions albeit with limited growth in order intake.

Pensionbee (LON:PBEE) (£168m) - this online pension provider reports its latest interim results. There is a cash burn of £14m, leaving its cash balance at £29m. While the top-line growth figures are growing at a solid rate, I’m not sure they are enough to justify this market cap given the lack of profitability and the likelihood that meaningful profits are likely to be several years away. The valuation is around ten times annualised revenues. I give some comparisons with Nutmeg, which is also still unprofitable despite having both more assets and a higher amount of assets per customer. If Nutmeg can’t make money despite those advantages, then how is Pension Bee going to make money?

Venture Life (LON:VLG) (£27m) (-2%) (no section below) - this provider of consumer self-care products, owning brands such as Dentyl and Ultra Dex, also publishes its interim results. Trading is in line with expectations and total revenues are up strongly (+36%) to £18.9m, helped by acquisitions. The company is profitable (adjusted EBITDA £3.3m) although statutory operating profit is very modest at just £0.4m. The company highlights strong organic growth at the acquired business, but the underlying revenue growth is actually very modest at just 1.7%. This looks disappointing when you consider the inflationary environment which has seen the prices of so many consumer goods soar. The company says it has been “passing on price increases where possible”. The balance sheet is ok with net debt of £3.1 million and plenty of headroom available on a £30m RCF, which might be used for further acquisitions in the near future. I maintain my view that while VLG shares are superficially cheap against the profitability that its brand portfolio should be able to achieve, the lack of organic growth is a good reason for the shares to remain cheap. [no section below]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Begbies Traynor (LON:BEG)

141p (last night’s close)

Market cap £217m

Shares in this insolvency practitioner (and associated services) have been strong this year, along with sector peer Frp Advisory (LON:FRP) - fairly obviously, they are benefiting from increasing corporate distress. Administrations and liquidations are highly complex, and high margin work, so when the economy deteriorates, they tend to do well.

My summary of today’s update -

FY 4/2022 was good, and ahead of original expectations (good trading, and acquisitions).

Strong track record - since 2018 business has more than doubled in size & profits. EPS up from 4.0p to 9.1p, and moved from net debt to net cash.

Good start made to FY 4/2023 in line with expectations.

Increasing number of larger (mid market) insolvency/restructuring cases emerging.

Guidance - is good, and a helpful footnote is provided. This is equivalent to approximately 10p EPS -

At this early stage of the financial year, we therefore remain confident of delivering market expectations* for the full year.

* current range of analyst forecasts for adjusted PBT of £19.7m-£20.6m (as compiled by the group)

My opinion - I’ve followed BEG for years, and think it’s a decent business, which seems to have successfully expanded through acquisitions, which have added value. Profits have gone up faster than new share issuance, which is what we want to see from acquisitive groups.

Current year forecasts are for about 10p, so the PER is about 14, which looks sensible to me. Given the horrible macro picture, it’s stating the obvious that insolvency practitioners are likely to be busy for several years (as cases can drag on for a long time, the more complex they are).

Hence this share continues to look a safe place to weather the storm.

Note below a strong share price, and high StockRank -

.

Smiths News (LON:SNWS)

27.7p (last nights close)

Market cap £66m

We’ve extensively reported on the turnaround at this newspaper/magazine distributor over the last few years. It’s now financially stable, with debt reduced, and paying big divis.

The extremely low PER reflects the reality that it’s in long-term, structural decline, although this is being impressively managed.

It’s a perhaps surprisingly positive update today, for FY 8/2022 -

Smiths News is pleased to report a good trading performance in the second half of FY2022 (H2), supported by a positive sales mix and focused operational control. The Board expects Adjusted EBITDA (ex. IFRS-16 leases) for the 52 week period ended 27 August 2022 to be not less than £40m, ahead of market expectations.

I reckon that translates into EPS of something between 10-12p, depending on which basis you use. So at 28p per share, the PER looks astonishingly low, below 3! Surely that’s too extreme?

Cost pressures have been well managed, and are as expected, demonstrating impressive management & budgeting.

Bad debt from McColls sounds like it might be a bit less than the £4.4m provision.

Dividends - this is what it’s all about. At least 2.7p final divi expected, with a 1.4p interim divi already paid in July 2022. That’s 4.1p (maybe more), so a yield of an amazing 14.8%!

Divis are restricted by an agreement with the bank to gradually de-gear.

Note the pension issues were wrapped up a while ago, so no issues there any more.

Outlook - nothing much said, but this bit does reassure -

We remain focused on providing excellent service to our retailers and publishers and expect to continue to deliver consistent financial performance and shareholder returns.

My opinion - for now anyway, SNWS is a consistent cash cow. It probably won’t last forever, as the business slowly declines, which is why the stock market isn’t interested.

At the current bombed out level of about 28p, this share does look compelling value to me. It’s very tempting.

.

Aquis Exchange (LON:AQX)

385p (down c.4% at 08:45)

Market cap £105m

Aquis is a junior stock exchange, below AIM. Its own shares are quoted on AIM.

Readers flagged up this share a while back. I did look at the previous accounts, but couldn’t really make much sense of them. In particular, it wasn’t clear where previous profits had come from, and there were also some unusual balance sheet items.

So I was keen to look at it afresh this morning.

Here are my notes on its H1 results -

Revenues for H1 of £8.3m, up 21%

Profit before tax (PBT) £0.7m, but that’s mainly come from releasing a £425k provision, so excluding that one-off, it’s only made £275k profit - negligible.

Claims market share of 5.2% of European share trading - seems a lot, and it’s not generating much revenue from that seemingly large market share.

42 “members” - I’m not sure if that is companies listed on Aquis, or whether it’s brokers that use the platform?

Balance sheet - is pretty good, with NTAV of about £19m, and a healthy cash pile of £13.3m. One odd item is £4.7m receivables in non-current assets, which is an unusual place to find receivables, so I would need to know what this is (not explained in the notes). Also previous impairments of receivables worries me - suggesting that some revenues may not be good quality maybe?

My opinion - judging from the figures, I would struggle to value this at much more than its own cash pile. Maybe £20-30m market cap might seem reasonable? Hence the £105m actual market cap looks to be including a lot of hope about future growth, or some potential strategic value in the business?

My problem with that, is that in previous incarnations, e.g Plus Markets, OFEX, etc, junior exchanges have never worked commercially, and ended up having little to no value.

Aquis looks somewhat better, and I’ve watched the enthusiastic webinars from the current boss, explaining his different charging model based on subscriptions, rather than transactional charges.

It’s looks a more viable business than in the past, but is not something I would pay anywhere near £105m market cap for, based on today’s numbers.

.

Hostmore (LON:MORE)

18p (down 6% today, at 09:22)

Market cap £23m

Hostmore plc ("Hostmore" or the "Company" and, together with its subsidiaries, the "Group"), the hospitality business with brands including 'Fridays', '63rd+1st' and 'Fridays and Go', is pleased to announce its interim results for the 26 weeks ended 3 July 2022 ("HY22").

H1 revenues £98.5m

Like-for-like (LFL) revenues down 7% vs pre-pandemic - not good.

EBITDA £7.1m (pre-IFRS 16) - the post-IFRS 16 EBITDA figure of £17.8m is best ignored, as it’s a fantasy number.

Loss before tax in H1 of £(17.0), due to £17.8m impairment charge. So it’s effectively a whisker above breakeven in H1, on an underlying basis.

Outlook - H2 so far, LFLs have deteriorated to -14% vs 2019 - clearly not good at all, so the consumer retrenchment is hitting MORE hard. They are hoping this will improve to -11% for H2 as a whole.

Some cost savings have been made.

Inflation - energy is hedged for this year, but hedges reduce next year. Expecting to take £5.8m additional energy costs in FY 12/2023, although this might reduce due to recent Govt price caps - unclear if this has been taken into account? Limited increases in food & drink costs.

Forecasts - thanks to Finncap for updating its model. FY 12/2022 is now expected to be a £(2.3)m loss at the adj PBT level. This is expected to improve in FY 12/2023 to £(0.4)m. I’ve got to say though, the 2023 forecast looks way too optimistic to me. If we assume flat revenues for 2023 vs 2022, then the company would be substantially loss-making, maybe as much as £(10)m, because of the operational gearing (high gross margin, and largely fixed costs).

So the downside scenario would probably trigger breach of bank covenants, and hence an equity fundraising or sale of the business would probably become inevitable. If that went badly, it could leave existing shareholders with little to nothing.

For this reason, unfortunately, I think this share has now become high risk.

Net bank debt was £26.2m at end June 2022, since reduced to £23.7m in last weeks, but the quarterly peaks are higher, with the next one expected to peak at £32.5m on 2 October, after rents and VAT are paid.

There are ample facilities available, but the bank is likely to want to reduce its exposure, as conditions deteriorate.

Going concern - this sounds surprisingly upbeat, but doesn't disclose what assumptions were made in the modelling. Nevertheless, the company reckons it can remain in compliance with the banking covenants. If that's correct, then the risk might not be as high as I fear -

Both scenarios, being the Group business plan and the severe but plausible downside, show that there will be no breach of the Group's covenant tests and that the Group has headroom above the minimum covenant levels.

Balance sheet - NAV is £111m, but we can deduct £146m of goodwill, resulting in NTAV negative at £(35)m. Although the main cause of this negative position is a yawning deficit of £46m on the lease entries: RoU Assets of £104m, less liabilities of £150m. If we eliminate lease entries, then the balance sheet NTAV would turn positive to £11m.

Overall, it’s not a disastrous balance sheet, but it’s very clear that bank debt is now too high, for what is probably now a loss-making business. Banks don’t like lending to loss-making companies.

The lease entries are also telling us that there are now some problem sites, generating losses. Hence why the £17.8m impairment charge was also necessary.

My opinion - I’m trying to keep the emotions out of this, and just look at the figures.

Trading has significantly deteriorated, and we now have a loss-making business, with too much bank debt.

So the dilution risk now looks high, and if trading gets worse, we could even have to consider insolvency risk.

Obviously this share has been a disaster, and I’m so sorry for anyone who followed me into this & has also experienced heavy losses. Things looked completely different a year ago, with it performing well, and having seemingly good expansion prospects, and consumers spending freely. I think expansion now looks completely off the table, and it needs to focus on survival, as consumers clearly don’t find its menu to be value for money, whatever management seem to think.

I’m not tempted to buy, despite the bombed out share price, because the risk now looks too high for me. Although if it manages to scrape through this downturn without dilution, and performance improves, then of course it could be a multibagger. We’ll just have to see what happens.

.

Graham’s Section:

Judges Scientific (LON:JDG)

Share price: £78 (+2%)

Market cap: £496m

Interim results are out from this buy-and-build operator in the scientific instruments sector.

The current year is shaping up to be significantly ahead of market expectations (so the mere 2% rise in the share price is puzzling).

Key points:

- Revenue +8% to £46.4m. Organic revenues +7%.

- Adjusted PBT +13.4% to £9.6m

- Actual PBT (without adjustments) minus 42.3% to £3.9m

We already had a clue about some of these results from the H1 trading update.

Adjusting items: the major adjusting items are amortisation of acquired intangible assets and acquisition costs. I would cautiously allow the acquisition costs to be adjusted out, but as usual I would be cautious about the amortisation adjustment.

If I only add back the acquisition costs, I get an adjusted PBT of about £7m.

Balance sheet & cash flow: net debt rises to £54.9m, following the £80m acquisition made earlier this year.

However, Judges appears to be happy with the progress at Geotek, a company specialising in geological analysis, and expresses this with an increase of the interim dividend (from 19p to 22p).

Cash generated from operations during H1 was stable, at £8.2m. Note that this isn’t too far off the adjusted PBT figure of £7m that I came up with.

Outlook: as we already knew, the different geographies in which Judges operates are offering different challenges. The prior trading update disclosed that order intake was down in both China/Hong Kong and the UK.

However, it appears that Geotek is driving the positivity. “The Board now expects that the full earn-out will be payable”, i.e. Geotek has performed at the upper end of the parameters that were agreed between Judges and Geotek’s sellers.

This means that Geotek is expected to earn an adjusted EBIT of at least £11.4m in the 2022 calendar year (perhaps more). The result is that an additional £35m will be payable to Geotek’s sellers, half in cash and half in shares.

For Judges, “the Board now expects that the Group will be significantly ahead of market expectations for the current year”.

Forecasts: Liberum have today raised their 2022 EPS forecast from 292.5p to 335.6p (up by 15%).

However, they have only raised their 2023 EPS forecast from 348.4p to 365p, on the grounds that “while Geotek’s revenues are not particularly cyclical, they can be lumpy”. They have therefore assumed a modest reduction in Geotek’s profitability next year, admitting that this “may well prove too cautious”.

I observed previously that Geotek, according to Judges, had a “reliance on a small number of large contracts”. This implies a lower quality of earnings, but the uncertainty around these contracts can result in positive or negative surprises. I’m glad to see a broker taking a cautious approach - this is all too rare.

As the 2023 EPS forecast is only raised by 5%, that might help to explain why the JDG share price hasn’t moved far today. But if Geotek’s momentum does carry through to next year, I imagine there should be significant upside for JDG shareholders from the current level!

Business performance

Let’s remind ourselves of some of the key points around JDG’s performance within the scientific instruments sector.

- Supply chain issues continue to dog the company, “probably aggravated by the Chinese lockdowns and the war in Ukraine”.

- The return of international travel has helped, but organic order intake was still “only” up by 4%. In other words of Judges, “this cannot be considered a full recovery to the pre-Covid growth trajectory”.

- China/Hong Kong/UK/Europe all lower or flat. Growth in North America and the Rest of the World.

Return on capital is strong, but unfortunately will be reduced by Geotek:

Organic Return on Total Invested Capital ("ROTIC") recovered to 29.6% for the trailing 12 months ended 30 June 2022 (30 June 2021: 25.0%). However, once Geotek is included, a sharp reduction of ROTIC must be expected.

My view

I will link you again back to my analysis of the H1 trading update, as I explained my views on JDG in some detail there.

The only difference now is that we can have more confidence in the success of Geotek and (hopefully) in the ability of JDG to carry out bigger acquisitions. This comes with the proviso that Geotek’s senior management - the sellers of the company - were very heavily incentivised to ensure that 2022 had a favourable outturn. As noted by Liberum, we can’t assume that 2023 is going to continue in the same positive direction.

Overall, however, there is no doubt that JDG is performing well in difficult circumstances. As I said in July, my view is that JDG shares are a nice long-term hold but if I was timing a purchase, I don’t see the current valuation as particularly attractive.

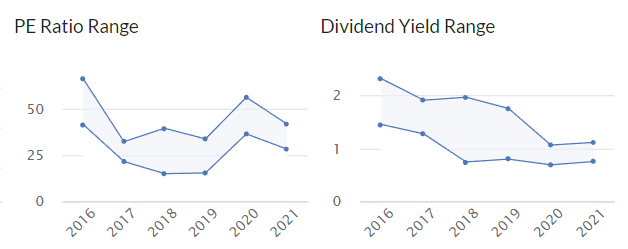

As the Stockopedia graphics demonstrate, it has been possible to buy JDG at lower PE ratios and at higher dividend yields. Maybe we will get buying opportunities like that again, some day?

Pensionbee (LON:PBEE)

Share price: 75.5p (-1%)

Market cap: £168m

This pension fintech releases interim results.

We’ve only checked it one time before: at July’s trading update.

It joined the market in a 2021 IPO, priced at 160p.

My main concern has been valuation: I can understand the rationale to pay a multiple of several times annualised recurring revenues for a growing, subscription-based business that has yet to reach bottom-line profitability.

But I struggle when faced with a price to sales multiple of 10x (or even 20x, as often occurred during the bull market).

When the price to sales multiple is so large that it starts to resemble a price to earnings ratio, for a company that isn’t profitable, I get very worried.

PensionBee announces that H1 revenues are up 53% to £8.3m, and that annualised run rate revenue is up 37% to £16.8m. Assets under administration are now some £2.7 billion.

Unfortunately, the market cap is still at a multiple of 10x ARR, even after the share price has collapsed since IPO and the company’s ARR has made decent gains.

Call it what you want, but I refuse to believe that an unprofitable company trading at 10x ARR can be a “value” share (although judging by my experience on Seeking Alpha recently, many Americans would disagree!).

PensionBee’s H1 pre-tax loss was £16.9m, worse than last year. It was unprofitable even at the adjusted EBITDA level, and worse than last year.

More positively, the company reports a score of 4.6 on Trustpilot (see for yourself here) and a customer retention rate of over 95%. Customer satisfaction is of course critical for any startup.

CEO comment:

Our approach has remained focused and consistent with our plan and ambitions to scale our business while achieving our near term profitability objectives. Our robust cash position means we are well-positioned to continue growing our market share, expecting to achieve high double-digit Revenue growth in the short-term and monthly Adjusted EBITDA profitability by the end of 2023.

PensionBee already has a quarter of a million active customers. I wonder what are the limits it might run into, as it expands market share?

We could compare it to Nutmeg, now owned by JP Morgan. According to Citywire, Nutmeg posted a £19m loss in 2021. Nutmeg has never made a profit despite the number of clients reaching some 170,000 and its asset base hitting £4.6 billion (£27,000 per client).

PensionBee has 246,000 “active customers” and 159,000 “invested customers” (shouldn’t those numbers be the same?). Yet it has just £2.7 billion in assets. That means assets per invested customer for PensionBee is just £17,000, much lower than Nutmeg.

The margin earned on assets is 0.69%, i.e. PensionBee earns £117 per customer per year, on average.

That’s less than half of the amount it spends to recruit a customer in advertising and marketing costs, so there is a considerable payback period just to get those costs covered.

My view

Like many financial companies, this needs serious scale to work properly for shareholders, in my opinion. In mountaineering terms, it is still at Base Camp and I fear that it has a long road ahead, to reach the scale that is needed.

It is working towards “monthly profitability breakeven by the end of 2023”, which would be a great achievement, even if profitability is being measured by adjusted EBITDA. Positive net income could be further away and if the experience of Nutmeg is relevant, it could be several years away.

There’s no doubt in my mind that this share is highly speculative - if I had to invest in it, I would want to do so in a bombed-out placing when the company needs to raise money. With the cash balance having reduced to £29m after a £14m cash burn in six months, I think it’s a distinct possibility that fresh funds will be needed here at some point.

What I wouldn’t want to do is pay full price, e.g. 10x ARR, which is the valuation given by the current market cap (admittedly, you could reduce this a bit if you deduct the cash balance from the market cap, but I’m not sure how much longer the cash is going to be there).

In summary, I think the algorithm is correct to identify this as a Sucker Stock: it might offer a fantastic customer experience, and it might turn out to be a highly successful business in the fullness of time, but these shares today offer poor statistical odds.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.