Good morning, it's Paul & Graham here.

Agenda -

Paul's section:

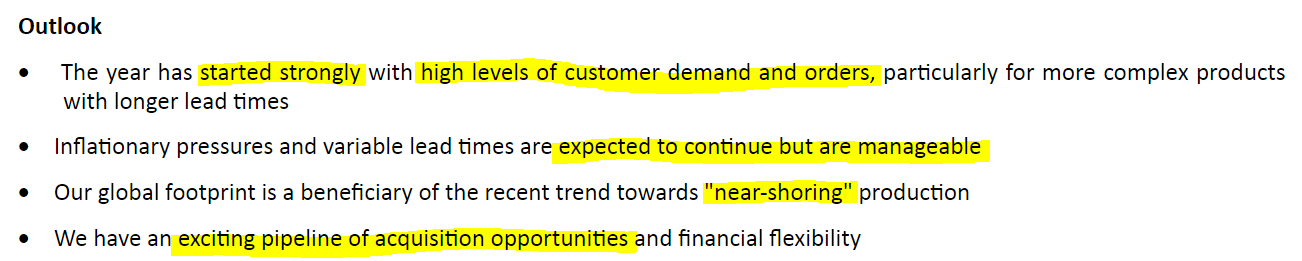

Volex (LON:VLX) (£379m) (I hold) results for FY 3/2022 look strong, and the valuation modest. Outlook comments are also surprisingly perky, with a strong start to FY 3/2023 indicated, with high demand & orders. Inflation is being passed through to customers. There's lots to like here, it's one of my favourite value/GARP shares at the moment. Patient, long-term investors should do very well on this, I reckon - with both earnings growth, and a higher PER possible once markets are through this current bear phase.

Naked Wines (LON:WINE) (£146m) - FY 3/2022 results don't look good - it's not making any profits, and growth has stalled, including forecast growth for this new year. Balance sheet is OK, but there is a cautious going concern statement. I'm worried that some customers might cancel wine subscription services, so WINE could be running to stand still. Not an attractive share at all, in my view.

iEnergizer (LON:IBPO) - readers flagged up sparkling results from this IT/outsourcing group. It looks highly profitable, and reasonably priced. But the CEO owns 83%. It's also up for sale at the moment, in bid talks. An intriguing situation for sure.

Graham's section:

Liontrust Asset Management (LON:LIO) (£610m) - Final Results yesterday showed an excellent performance in FY March 2022. However, the share price has been sliding lower for months as general investor sentiment has soured and Liontrust funds, with significant exposure to richly-valued US shares, have underperformed. The LIO share price decline has brought it arguably into value territory.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Volex (LON:VLX) (I hold)

240p (yesterday’s close)

Market cap £379m

Volex is a long-term holding for me. It was initially a strong turnaround, but is now acquisitive, bolting on reasonably priced businesses in the same sector (electrical power products & cable assemblies). So far, Exec Chairman, Nat Rothschild (24.5% shareholder) seems to have done a cracking job.

Despite putting out impressive trading updates, and constantly reminding the market that it is able to pass on cost increases through flexible contracts, the share price has sold off in this current bear market. Is this fall justified, with tougher times ahead, or is Mr Market irrationally depressed, and offering us a buying opportunity?

.

As I made clear here on 20 April 2022, with a positive year end (FY 3/2022) update from Volex, I’m firmly in the bullish camp, and wish I had some spare money to buy more now.

Here’s my quick view on an initial skim of the key numbers & outlook comments (I’ve printed off the full announcement to read at a more leisurely pace later) -

(reporting in US dollars)

Revenues up 39% to $615m (so a sizeable business now)

19% of revenue growth was organic - very impressive. Note that Volex has positive exposure to growth areas, particularly cables for electric vehicles, where revenues almost doubled to >$100m. Also pent-up demand from the medical machines sector. Industrial, and data centres are also positive sectors, so Volex seems to be in a good place, with favourable sector tailwinds, a positive antidote to darkening macro clouds in my view.

EPS fell, but that’s because of last year’s negative tax charge, which we already knew about, so no surprises there. Underlying EPS rose 6.3% once this tax effect is stripped out.

Underlying diluted (for share options) EPS was 25.2 US cents, or 20.6p in sterling.

Stockopedia shows 25.9 US cents broker consensus, so a slight miss, but a note from Liberum this morning says the results are ahead of its expectations. So I’ll probably just view it as in line.

PER is 11.7, based on FY 3/2022 actual EPS of 20.6p - that’s great value for a resilient, growing group.

Of course, earnings are likely to continue growing (organic & acquisitions), and a new 5-year plan is announced, with a target to double revenues to $1.2bn by FY 3/2027, at a operating margin of 9-10% (similar to what is currently being achieved). Hence there’s scope for this share to double earnings, and I suggest, re-rate onto a higher PER than 11.7 also, giving the possibility that this share could double or triple in the next few years. Also bear in mind, it over-achieved against the last plan, and has established a track record for making good acquisitions, which is not reflected in the current valuation.

Cost inflation (copper, plastic & wages mainly) is passed through to customers, with a lag, since contracts already factor in price rises either quarterly or annually. Copper rose a lot in 2020 & 2021, but has more recently been falling. Volex took all that in its stride, so this share looks a lot safer than many investors imagined, with chat on bulletin boards often focused on the price of copper, and some people selling the shares because they wrongly imagined it would hit profits at Volex.

Outlook - looks good -

Broker forecasts - have been set quite low, with only a modest increase in EPS for FY 3/2023. Today’s update that the new year has started strongly, and the benefit from 4 acquisitions made in FY 3/2022, suggests to me that the risk of a profit warning from Volex looks relatively low.

Balance sheet - net debt has shot up to $74.4m, to fund acquisitions, but is not alarmingly high. NTAV is fine, at $78m.

My opinion - there’s a lot to like here. Macro worries, and investor fear, seem to be throwing up bargains right now - we’re finding new ones almost every day here at the SCVR.

Volex is performing well, has tailwinds from growth in its key markets (especially EVs), is passing on cost increases to customers, and clearly has excellent management with big skin in the game, delivering well on its expansion plans. Yet we can buy this for a PER barely into double digits - that’s a clear opportunity in my view.

Once markets are more settled, then I imagine this share could be 50% higher than it is now, and longer term, considerably more than that, due to the organic & acquisitive growth. Unless something goes wrong (which is always possible), then this looks a very attractive GARP (growth at reasonable price) share right now.

As with everything, I’ve no idea what the short term share price is likely to do, as that’s sentiment-driven.

.

Naked Wines (LON:WINE)

198p (down 31% at 09:36)

Market cap £146m

A painful day, indeed year, for suffering shareholders in this subscription wine business.

Results for FY 3/2022 are out today.

As with most eCommerce businesses, it had a huge surge in demand in the pandemic, but is now struggling to demonstrate further growth (+5% this year, +78% prior year). That could provide an opportunity maybe, if growth returns this new year, on a longer-term structural level, rather than boom & bust growth in the pandemic. So the outlook comments are all-important.

Revenue £350m (up 3% reported, up 5% in constant currency, against tough comparatives during the pandemic)

I’ve never accepted the “Contribution profit” number, which is fantasy in my opinion. FWIW, this is £79m, and is meant to show profit from established customers.

That all disappears, due to heavy marketing spending, to win new customers (or replace churn, more like), so adj profit before tax is negligible at £3.0m (LY: £(0.5)m) - the business is effectively running at breakeven, and marketing spend is flexible, so can be dialled up and down as required.

Note the 5-year forecast payback for new customers has fallen to only 1.5x, which concerns me greatly. It looks as if the £41.3m “investment in new customers” is not good value for money. Guidance is for a reduction of £5m in this spend in FY 3/2023.

I’m also sceptical of the “Standstill EBIT” figure of £21.2m, which has fallen by almost half of last year’s £39.3m - so questions about the business model are growing.

UK sales are expected to be “relatively flat” in FY 3/2023.

Guidance - detailed, but shows the business is now effectively ex-growth - which I could accept last year (due to very tough pandemic comparatives), but not for this year, when structural growth should be returning. WINE doesn’t expect that to happen, despite the huge marketing spending (although to be fair, the consumer macro position is bound to be less favourable for discretionary spending like a wine subscription) -

.

.

Going concern note - flags a “material uncertainty”, in downside forecasts, although the company does point out it has options to reduce things like marketing spending, and reducing inventories. I’m not overly concerned about this, because the balance sheet looks fine for now. But if future performance drops heavily (possible as consumers often cancel subscriptions when incomes are squeezed), then I would start to get worried.

Balance sheet - looks OK for now, with NTAV of £76.5m.

Remember that if business does decline, then the benefit of receiving cash up-front from customers (reflected in cash, and deferred income creditor) would shrink, which could put pressure on the cash position.

My opinion - online, subscription businesses for discretionary purchases strike me as possibly one of the worst places to invest right now, as consumers retrench.

I’ve tried out Naked Wines, twice, and it’s clever the way they hook you into a regular monthly payment, but I’ve recently cancelled it. The wine was OK, but nothing special. Connoisseurs might like all the stuff about choosing vineyards, etc, but I can’t see the point for most people. Just looking at the reviews on Waitrose seems to me a quicker and easier way to find nice wines, for the vast majority of people. Or just buy lovely wines from Aldi/Lidl, which are cheap, and generally very good.

I suppose the key question is whether WINE is now cheap, and hence worth a punt? Is it cheap though? £146m market cap, for a business that isn’t making any profit, and isn’t growing now either, doesn’t look cheap to me at all.

So definitely not for me, despite the 75%+ share price fall from last year. It wasn’t worth the previous lofty valuation, in my view.

If growth does resume later this year, then WINE shares could be worth revisiting. For now though, I don’t see any appeal.

.

.

iEnergizer (LON:IBPO)

508p (up 13%, at 10:48)

Market cap £967m

Many thanks to ridavies and DAZZA64 for flagging sparkling results today from this share, which for some reason we missed here at the SCVR, despite it now having been a 40-bagger since 2016! What a pity, and apologies I somehow overlooked this company, no idea why.

Researching it from scratch, the company’s own description of its activities is of almost zero use, what on earth does this mean? -

iEnergizer, the technology services and media solutions leader for the digital age… a unique, end-to-end digital solution enabler.

It then gives a more detailed description, which I’m still finding very hard to understand or visualise. Maybe you can understand this? -

iEnergizer is an AIM quoted, independent, integrated software and service pioneer. The Company is a publishing and technology leader, which is set to benefit from the dual disruptive waves of big data and the cloud in the digital age. With its expertise and cutting-edge technology, iEnergizer is uniquely positioned to facilitate the transformation to a digital world and support clients in this transition.

iEnergizer provides services across the entire customer lifecycle and offers a comprehensive suite of Content & Publishing Process Outsourcing Solutions (Content Services) and Customer Management Services (Business Process Outsource) that include Transaction Processing, customer acquisition, customer care, technical support, billing & collections, dispute handling, off the shelf courseware, and market research & analytics using various platforms including voice - inbound and outbound, back-office support, online chat, mail room and other business support services.

Our award-winning content and publishing services provide complete, end-to-end solutions for information providers and all businesses involved in content production. Our differentiation is in focusing on solutions and services that enable customers to find new ways to monetize their content assets, measurably improve performance, and increase revenues across their entire operation. From digital product conception, content creation and multichannel distribution, to post-delivery customer and IT support, we align ourselves with our customers as they streamline their operations to maximize cost-efficiencies and improve their ROI while connecting them with new, digitally savvy audiences.

On the basis that I have very little idea what the company actually does, I’ll let the numbers do the talking instead.

Anil Aggarwal (aged 61) is the CEO, and owns 82.6% of the shares! So everyone else is along for the ride, and what a ride it’s been!

On 9 June 2022 the company announced it is reviewing strategic options, and has entered preliminary discussions with BPEA Advisors Private Ltd about a possible sale.

There was an ahead of expectations trading update on 21 Feb 2022.

Annual Results - FY 3/2022

Revenues up 32% to $265m

Profit before tax up 56% to $83.2m - that’s a staggeringly high profit margin of 31%, so whatever IBPO does, it clearly has immense pricing power.

EPS of $0.39, converts to 31.8 pence, so the PER is 16.0 times - which looks great value, if you think profits can keep rising strongly.

Balance sheet - is weak, with NAV of $58.6m, less intangible assets of $115.3m, gives NTAV of negative $(56.7)m.

There’s a fair bit of borrowings $9.8m current, and $129.9m non-current, offset partially by cash of $56.3m, giving net debt of $83.4m. The company says net debt is $100m, the difference being lease liabilities of $16.7m.

Given the huge profits, then this level of debt, and the weak balance sheet, are really not a problem. They would only become issues if profitability collapsed, which seems very unlikely, given the track record.

Cashflow statement - looks fine to me. It seems a genuinely cash generative business, which since 2019 has been paying generous, and growing dividends. The forecast yield is good, at c.5%.

Outlook - sounds upbeat -

"Importantly, we have secured several new customers across each of our divisions, as well as maintaining and deepening relationships with our existing key customers. The business has maintained a successful focus on recurring revenue streams, by capitalizing on iEnergizer's advantageous position to service existing and new customers' needs in the evolving digital technology landscape.

"The first three months of fiscal 2023 have started well, continuing the recent positive trend, with extensions of existing contracts.

"With iEnergizer's solid foundation, its proven strength in operational execution, new sales initiatives, differentiated offerings, healthy balance sheet, and with substantial opportunities for further growth identified, the Board is confident in the Company's continued growth path as a unique, end-to-end digital solution enabler."

My opinion - what an interesting company! I’d like to learn more about the history, in particular what caused the share price to collapse from 2013 to 2016, then recover in spectacular fashion, as a major multibagger since then? Looking back at the 2015 results, they were poor, and the group was swamped by excessive net debt. Hence probably why the equity was so bombed out. There's since been a geared turnaround, with all the benefit flowing to equity, in a major multibagger. Just shows, every now and then, a really risky, highly indebted company can deliver a stunning result for shareholders who are prepared to risk a wipe out.

The ownership structure obviously means that the CEO can do anything he wants, with over 75% of the shares, which is a risk.

If current bid talks fall through, then there could be a risk the share price might give up some of the recent gains.

Or a bid might come at a nice premium, who knows? IT companies do seem to attract high prices when bids occur.

Overall, very interesting. It’s too soon for me to form an opinion on it, but the numbers look fantastic, and valuation quite modest.

.

.

Graham’s Section:

Liontrust Asset Management (LON:LIO)

£610m (+1% yesterday)

Good morning, everyone.

I’ve been looking at Liontrust today, as many readers are interested in it, and it was in the 2022 New Year NAPS. It released its final results yesterday.

One of the wonderful things about investing in fund managers is that it’s often quite easy to put yourselves in the shoes of the company’s customers: all you have to do is find the fund literature, and read it.

So I’ve been looking through the company’s funds. What really stands out, first of all, is the size of Liontrust’s “sustainable” funds.

Here’s a breakdown of the company’s AUM by category. You can see how big the Sustainable category is:

“Sustainable” is a word with many meanings, and Liontrust uses it in a variety of ways.

For example, its funds have invested in a childcare company because “better work-life balance” and “reducing stress for parents” is “part of a more sustainable future” (link).

There is a sustainable theme to go with every investment. The theme for investing in a bank, for example, is “saving for the future”.

The Sustainable Future Managed Fund is one of the most interesting funds at Liontrust – currently £2.9 billion in assets (according to the May factsheet).

This fund has two managers, one of whom is the head of the Sustainable Investment Team with over a dozen people reporting to him. The fund has in the region of 140 equity holdings, or around 160 holdings in total.

Personally, I find it difficult to keep track of my nine-stock portfolio. Keeping track of 160 holdings, while managing a team of fund managers? I don’t see how it can be done, except if the due diligence and research applied to each individual holding and potential holding is shallow.

I’ve looked up the StockRanks for many of the shares mentioned in Liontrust’s sustainable fund updates, or coming up in the lists of top ten holdings at these funds.

What I’ve noticed is that very many of the companies held by Liontrust’s sustainable funds are quantitatively poor value, and have a long way to go in order to prove themselves financially.

These ones came up on an initial survey:

· ADSK – ValueRank 13 .

· AMT – ValueRank 15.

· CDNS – ValueRank 10.

· DOCU – ValueRank 12.

· EQIX – ValueRank 10.

· ISRG – ValueRank 12.

· TMO – ValueRank 19.

· SPLK – ValueRank 7.

· SPOT – ValueRank 14.

· PAWN – ValueRank 8.

· Trainline (LON:TRN) – ValueRank 26

· Oxford BioMedica (LON:OXB) – ValueRank 30.

Many of these valuations are, in my view, hard to justify. Importantly, the ValueRanks shown above are calculated after the huge sell-off that has already occurred.

So if the value offered by these shares is going to improve, then many of them will have to sell off quite a lot more than they already have. Or else their financial performance is going to have to improve considerably.

Liontrust’s willingness to hold these richly valued shares has contributed to the weak performance of their funds in Q1 and what will likely be another weak performance in Q2.

Liontrust’s Sustainable Future Managed Fund is down 23.9% year-to-date (and note that this is not a pure equity fund – it’s a mix of equities and bonds). The pure-equity Sustainable Future Global Growth Fund is down 27% year-to-date (this is a £1.6 billion fund).

We’re writing a Value Report, and valuation is important to me. So personally, because of the poor value offered by so many holdings, these are not funds that I would want to own, and I wouldn’t mention them to my family and friends.

I’ve also looked at the long-term performance of the Sustainable Future Global Growth Fund, because it’s one of the most prominent pure-equity sustainable funds at Liontrust.

Against the MSCI World, a global benchmark index, this fund has underperformed on a 1-year view, on a 3-year view, on a 10-year view, and since its inception in 2001.

Why it matters

There is a long-term trend towards passive investing, as active funds fail to beat passive indexes. UK fund managers often focus on their performance against other funds, rather than against the index. It’s much, much easier to beat other funds than it is to beat a passive index!

In order to maintain relevance in a world where the default choice for investors is to own a passive fund, active managers need to have at least one of the following:

1. The ability to beat passive indexes (very rare).

2. The ability to access investments or structure portfolios that the customer can’t.

It looks like Liontrust’s main success, and strategy, is in marketing itself as a “sustainable” specialist, helping customers to own funds that they can feel positively about. It’s no surprise that ESG and “Net Zero” are mentioned so often.

These themes are incredibly popular right now, but will their popularity survive a period of high interest rates and a protracted bear market, when hungry investors give a higher priority to returns? I’m not so sure!

FY March 2022 Results

I’ve not said anything about yesterday’s results yet, so here’s a quick summary:

· Revenues +41% to £231m

· Pre-tax profit +127% to £79m

· AUMA (assets under management and advice) +8.5% to £33.5bn (before acquiring Majedie, with an extra £5.2bn).

Markets are forward-looking, of course, last year’s results aren’t considered particularly important. Liontrust shares are down nearly 60% year-to-date, despite the imminent announcement of these excellent growth figures.

Net inflows were positive for the year but there were net outflows in Q4 (Jan-March 2022), as investor sentiment soured. I assume that there will be more pressure on flows in the current financial year, given the overall trends in investor sentiment.

My view

It’s amazing how quickly the Liontrust share price turned from optimism to pessimism. I’ve remarked before that when you buy shares in a fund manager, you are buying a turbo-charged stock market investment: you will get inflows and rising profits in a bull market, and outflows and falling profits in a bear market.

The operational leverage at a fund manager plays a big role in this. Additional revenues tend to drop through to the bottom line very easily, without bringing many additional operating costs. Operating expenses were up 17% at Liontrust, which is significant, but revenues grew at more than double the pace, making it a much more profitable company.

But if revenues fall, this works in reverse, and profitability can collapse very quickly.

Ironically, after their steep decline, Liontrust shares are now offering decent value (ValueRank 65). There is now, according to the forecasts, a single-digit PE multiple. And if the share price falls much further, it’s possible that the PE multiple could fall below the dividend yield – another classic sign of a value stock.

Your view on the stock may depend on your belief in the longevity of the “Sustainability” theme. Would Liontrust be able to pivot to a new marketing strategy, if Sustainability was no longer considered important by investors?

In the short-term, I would be wary of continued poor fund performance. I find many holdings in Liontrust funds whose valuations, in my opinion, remain extremely vulnerable to further depreciation. Higher rates will wash out the remaining excesses in the US markets, and this may impact Liontrust’s funds more than their competitors.

I also have questions as to the extent of the due diligence and research that their fund managers can carry out, given the number of holdings in some funds.

Perhaps this has all been priced in, at Liontrust’s current share price? If I were a Liontrust shareholder, I’d be braced for at least a year of poor fund performance, with a big risk of outflows. But whenever the markets bottom and valuations have found a floor, investor sentiment will turn around again, as it always does.

I do think that the prospective risk/reward for long-term LIO shareholders is much better at 900p than it was at £20, and that the company can easily afford the dividends it has paid. So perhaps the best thing to do now is to think of it as an income play, and forget about the share price!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.