Good morning! It's Paul & Graham here again today.

Agenda - we've done mostly shorter sections today, to get through more companies, and more quickly -

Paul’s Section:

Next (LON:NXT) (6746p - £8.7bn pre-open) [no section below] - Q2 (May-July ‘22) trading update - always of interest for sector trends from the best in class operator that also reports so promptly.

- Trading better than expected (especially in physical stores) - due to less competition on high streets, and warm/dry weather in June/July.

- FY 1/23 EPS guidance raised 7.2% (range: 543p-588p, PER = 11.5 to 12.4 = cheap IMO!).

- Pre-pandemic trends returning in product mix (formal wear up, sports/home down)

- Online returns rate back up to 42%.

- Is online in decline? No - just returning to long-term growth trend after a boom during pandemic - this is absolutely key, and confirms my theory that bombed out online shares could now be oversold, as market has wrongly assumed they’re now ex-growth!

- H2 guidance is cautious - sales growth slowing from +12.4% in H1 to +1.0% in H2 - due to impact on consumer spending from higher inflation.

- Share buybacks continuing, reduced share count by 2.6% so far this year. Amazing long-term strategy, boosting EPS considerably over time.

My opinion - I’m highly encouraged by Next’s update, as it confirms what I always thought - that the pandemic pulled forward demand for online shopping. We then had a hangover in calendar H2 2021 & H1 2022, but things are now returning to a (more modest) long-term growth rate for online. This could trigger a potentially big re-rating of bombed out eCommerce shares - one of my main investing themes for the rest of this year & next year, as the market realises they are actually still growth stocks (the ones with decent, differentiated product anyway), but many are currently priced too cheaply as if they were ex-growth.

SCS (LON:SCS) (147p down 4% at 10:09 - mkt cap £53m) (I hold) [no section below] - FY TU 52 wks ended 30 July 2022 - profit ahead of market expectations, due to positive trading, strong margin, and cost management - I’m impressed, as I was expecting another profit warning here. Although it does warn for FY 7/2023.

Cash of £70.8m (no debt) is above market cap. £7m share buyback continuing. Also note forecast 9% divi yield, which looks sustainable to me.

Orders reduced in recent months, lower consumer confidence expected to adversely impact FY 7/2023 - this really shouldn’t come as a surprise to anyone!

My opinion - the share price has already factored in a consumer slowdown, and is now almost down to pandemic lows again. That’s despite a bulletproof balance sheet (compare it with DFS!) and a falling share count. Trading likely to be soft during this cost of living squeeze. Should be good long-term, and no insolvency risk due to favourable working capital structure. Likely to benefit from competitors going bust (e.g. Made.Com (LON:MADE) possibly?) and others - e.g. lots of independents, now rent moratorium ended. No guidance provided for FY 7/2023, but Shore Capital update is now on Research Tree (many thanks) - lowers FY 7/2023 by 17% to 16.3p - that looks sensible. Long-term, I think EPS should recover to c.30p (way above current forecasts), and share price could double. But short-term, expect weaker trading. So this is short term pain, long-term gain in my opinion. Should be able to keep paying generous divis whilst we wait, and buybacks at this price make obvious sense.

Renold (LON:RNO) (25p - £54m) [no section below] - I’ve been covering the turnaround at Renold for several years, and have been impressed with progress made. Today’s news is a sizeable acquisition, £20m [E24m] being paid out of cash/debt (no equity dilution), about 37% of RNO’s market cap. Key points -

- Meaningful synergies

- Acquired company (Spanish) had revenues of E18.6m, and EBITDA of £3.1m (FY 6/2022).

- Reasonable price at 7.6x EBITDA (falling to below 7x once cost savings implemented)

- Accretive to both EPS and operating profit margin.

- Debt: EBITDA to rise from 0.6x to 1.5x, leaving scope for further deals.

- Acquired company has no pension scheme, so enlarged group helps dilute RNO’s big pension scheme.

- Management know the target company well, and think it’s a good fit.

My opinion - expanding a group with a big pension deficit is an excellent strategy to make the problem a relatively reduced problem, and hence can trigger a re-rating of the shares. I’m hoping to interview RNO’s CEO tomorrow (no fee, no holding personally), as I like this share and think it’s an interesting company, still modestly priced.

Sanderson Design (LON:SDG) - I've had a good look through this in line with expectations H1 update. It looks fine to me. Broker forecasts are maintained for the full year, and the PER is now really low on those confirmed numbers. Great balance sheet, with pots of cash too, so this share is right up my street. There's always a risk of a deteriorating macro picture denting H2 performance though, and the company does say today it's planning for a wide range of possible scenarios. Sounds sensible to me. Long term, I see this as a winner, short term, nobody knows! (More detail below)

Graham's Section:

Duke Royalty (LON:DUKE) (£141m) - Q1 revenue comes in slightly better than expected at this provider of royalty financing. An inflationary environment should be fine for Duke, which gets paid in accordance with the revenue generated by its investees (whether it is fine for the investees is another matter). Duke probably needs to scale up even more in the years ahead and so more equity placings are to be expected. The investment process has been tried and tested since c. 2015/2016, without too many accidents along the way. (More detail below).

GYM (LON:GYM) (£323m) (+1.6%) [no section below] - an upbeat set of interim results from this operator of low-cost, 24-hour gyms. At the Q&A session, the CEO has just said that the company should be back at 2019 levels of like-for-like performance later this year. July is in line with expectations, and the company is looking forward to students returning to university and the continued normalisation of working patterns. As of June 2022, total membership numbers remain below H1 2019, but the company has 50 more gyms than it did then (215 in total). There is a small loss for the period (4.4m) and net debt finishes at £57.6m. GYM is targeting 300+ sites and £40m-£50m of PBT by FY Dec 2025, and I’m open-minded to this possibility (for context, operating profit was £21.6m in FY Dec 2019). This share offers an attractive growth story in the low-cost gym niche, with lots of upside from the current valuation if management can execute.

TT electronics (LON:TTG) (£315m) (-2.8%) [no section below] - full-year expectations are unchanged at this provider of electronics equipment. Revenue growth is 8% (organic) or 10% in total, at constant currencies. Excellent demand is seen with a book-to-bill ratio of 144% and the order book at twice pre-pandemic levels. Inflation is causing some complications but is being passed onto customers, and the dividend beats inflation too, with an 11% increase in the interim payout. Some financial risk as net debt including leases is high at £142m; the company is hoping to reduce leverage over the next six months. EPS for the period is disappointing at 2.3p and this is partly due to a much higher finance charge caused by that increased debt load, higher interest rates and the fees associated with borrowing facilities. I like the prospects for shareholders here with a PE ratio of c. 10x and a dividend yield of 4%, but it will be an easier bet after the company has paid down its loans to more comfortable levels.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

I'm doing shorter sections above to begin with, to get through more companies.

Sanderson Design (LON:SDG) (I hold)

107p (down 5% at 11:30)

Market cap £76m

Sanderson Design Group PLC (AIM: SDG), the luxury interior design and furnishings group, is pleased to announce its trading update for the six months ended 31 July 2022.

H1 revenues flat vs H1 LY at constant currency, up 1% reported, at £57.9m

H1 profitability - we’re not told what it is, but that it’s in line with the Board’s expectations. That’s fine, this usually means that the company is on track to achieve full year forecasts, unless there’s something nasty in the outlook section (it’s fine, see below).

The table giving a breakdown of H1 revenue is probably more information than I need, some bits are up, some down.

Licensing revenue is the stand-out number, at +90% to £3.8m - doesn’t sound much, but remember licensing revenues are pure profit, so this is the highest quality revenue stream, and it’s up strongly, so a tick here. That might have offset softer profit elsewhere, at a guess? A new note from Progressive says the increase is due to “accelerated income from recent agreements” which sounds one-off in nature, so we probably shouldn’t be getting too excited about this - although all licensing income is a validator of the valuable brands & designs that SDG owns.

Net cash of £15.0m at 31 July 2022 is still very healthy - down a bit from £19.1m 6 months ago, partially due to “a strategic investment in inventory of our best-selling collections” - that’s fine by me, as long as it’s only best sellers, and not over-stocking of slow-moving lines, which I doubt would occur under this CEO who has systematically reduced product lines, and cleared excess inventories in the last couple of years.

Outlook -

As set out in our AGM statement on 12 July 2022, we remain vigilant in respect of the world economic environment. Current market conditions are difficult to predict and we are planning for a wide range of possible scenarios in the second half.

Despite this, full year trading currently remains in line with the Board's expectations.

The Group's strong cash position enables continued investment in the business and also provides protection in the event of any material adverse changes in trading conditions.

I think that’s fine, given current macro conditions. Maybe some investors may have interpreted the bit about a wide range of possible H2 scenarios more negatively, I don’t know?

CEO comments are interesting, and seem fairly upbeat to me -

Lisa Montague, Chief Executive Officer of Sanderson Design Group, commented: "I am pleased to be reporting good strategic progress in the first six months of the year. It is encouraging to see licensing partnerships with major retailers both in the UK and US being extended, underpinning their belief in our brands and products.

"The two-year contract extension with Williams Sonoma, a leading US retailer, signals the confidence it has in the strength of a collection that is yet to launch, and emphasises the progress we are making in the US, a core growth market for the Group.

"We retain a rather cautious outlook, mindful of the cost, supply chain and consumer confidence issues that impact the macro-environment, though we are committed to delivering further strategic progress during the remainder of the year."

Update from Progressive - this is directly commissioned research, so I always regard this as effectively coming from the company itself.

Forecasts are unchanged at £119.1m revenues, £13.0m adj PBT, and 14.7p EPS for this year, FY 1/2023.

The share price is 107p, so the current year PER, confirmed today as in line, is only 7.3 - that seems remarkably cheap to me. The market is clearly imagining that there could be an H2 profit warning, which can’t be ruled out, given how wobbly the macro position appears to be.

There again, SDG customers really won’t be worrying about food or utility bills - have you seen their prices?!

Anyway, it seems to me that the current price factors in a large margin of safety - maybe that’s sensible, given that the company itself says a wide range of possible outcomes are being planned for.

My opinion - this share is right up my street. It’s unloved, yet performing well, and has a superb balance sheet, so there should be no dilution or insolvency risk.

As with so many other shares right now, I could see this easily doubling in price, once economic conditions are more normal, however long that takes? Usually macro problems sort themselves out in a couple of years. That strikes me as a very good investment proposition, if you’re prepared to turn off your screen and ignore market sentiment in the shorter term. The same could be said for plenty of other bombed out small caps right now.

.

Graham’s Section:

Duke Royalty (LON:DUKE)

- Share price: 33.9p (+3%)

- Market cap: £141m

I was briefly a shareholder in this investment vehicle, from June 2018 until August 2019. I got out at breakeven, before counting dividends.

Duke’s purpose is to offer a rare form of financing that few businesses use, and which Duke thinks should be used more often: the royalty. This form of financing allows for very high yields, which in turn enables Duke to offer big payouts to its shareholders.

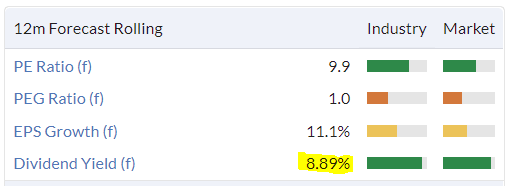

Here’s the forecast yield according to Stocko:

And here are the highlights for today’s Q1 update:

- “Normalised cash revenue” is £5.1m, exceeding expectations of £5.0m (this is basically how much cash the company received from investees, before counting any one-off transactions).

- Since there were no one-off transactions, the “Total Cash Revenue” is the same number, i.e. £5.1m.

- Outlook: in Q2, Duke is expecting normalised cash revenue of £5.2m.

Operational Highlights

One feature that I like is Duke’s tendency to do follow-on investments. This is consistent with the idea that the best investments are often the ones that you already own. The obvious downside with this is that it doesn’t improve Duke’s diversification.

During Q1, Duke invested over £5m in companies where it had already made substantial investments. In each case, the purpose of the funding was to pay for an acquisition (sectors: care homes and managed IT services).

During the quarter, Duke also raised £20m at 35p. It has a successful track record when it comes to fundraising for itself. In 2021, it raised £32m, also at 35p.

The dividend paid out in the quarter was 0.7p, and was “well covered by operating cash flow”.

Based on the current share count, that dividend should have cost the company £2.9m. Remember that cash revenue from investees was £5.1m - so there is a buffer to pay interest, salaries and other administrative expenses.

Outlook statement

CEO Neil Johnson mentions the “inflationary macro-environment” in the context of Duke’s revenue outlook. It’s a good point: remember that Duke’s revenues are tied to the revenues of their investees. As prices rise, even if purely as a consequence of inflation, this feeds back to Duke.

There are now 48 underlying operating companies, in “a diverse portfolio of profitable, long-established businesses in low-risk sectors”.

My view

I still find this share interesting, but have no plans to invest in it again.

What I like:

- Improved diversification as the company has scaled up (however, it would make sense for the company to scale up much more).

- The company has successfully exited some of its investments, generating attractive returns and proving that the investment process worked.

- Duke got rid of its investment in riverboats on the Rhine and Danube rivers, without making a huge loss (although most of the money from that sale hasn’t been received yet, so there’s still an element of uncertainty).

What I don’t like:

- Duke pays interest to Honeycomb Investment Trust (LON:HONY) of LIBOR plus 7.25%. Firstly, this says a lot about Duke’s risk profile, and secondly, it’s only profitable if Duke generates extremely high yields on its own investments.

- Duke has taken equity shares in its investees, as part of its deal agreements. If it gets this equity very cheaply then that’s fair enough, but it highlights that this form of financing has a lot in common with high-risk equity investing.

- The investees are frequently engaged in buy-and-build acquisition strategies, and this is likely to remain the case. Think of the complexity and the layers of management involved: we invest in Duke, who invests in Company A, who uses the money to invest in Company B. There are simpler ways to invest than this!

Having studied Duke in some detail in the past, I’m currently neutral on it. I think it’s worth keeping tabs on, as it builds its reputation and track record, and as an income play it may have some appeal.

Balance sheet net assets were £122m as of September 2021, and the company has generated plenty of income and raised £20m since then. So from that perspective, Duke’s shares may not be overly expensive, at the current market cap (though bear in mind that there are likely to be more placings along the way).

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.