Good morning, it's Paul & Graham here!

Webinar tonight at 18:00 - on how to use the StockRanks to pick the best value stocks in a recovering market. These occasional webinars are always fascinating and well attended, so I've set an alarm for 18:00 myself.

Roland has written an interesting article here which runs through his process for selecting high quality shares, well worth a read.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Companies Reporting

Summaries

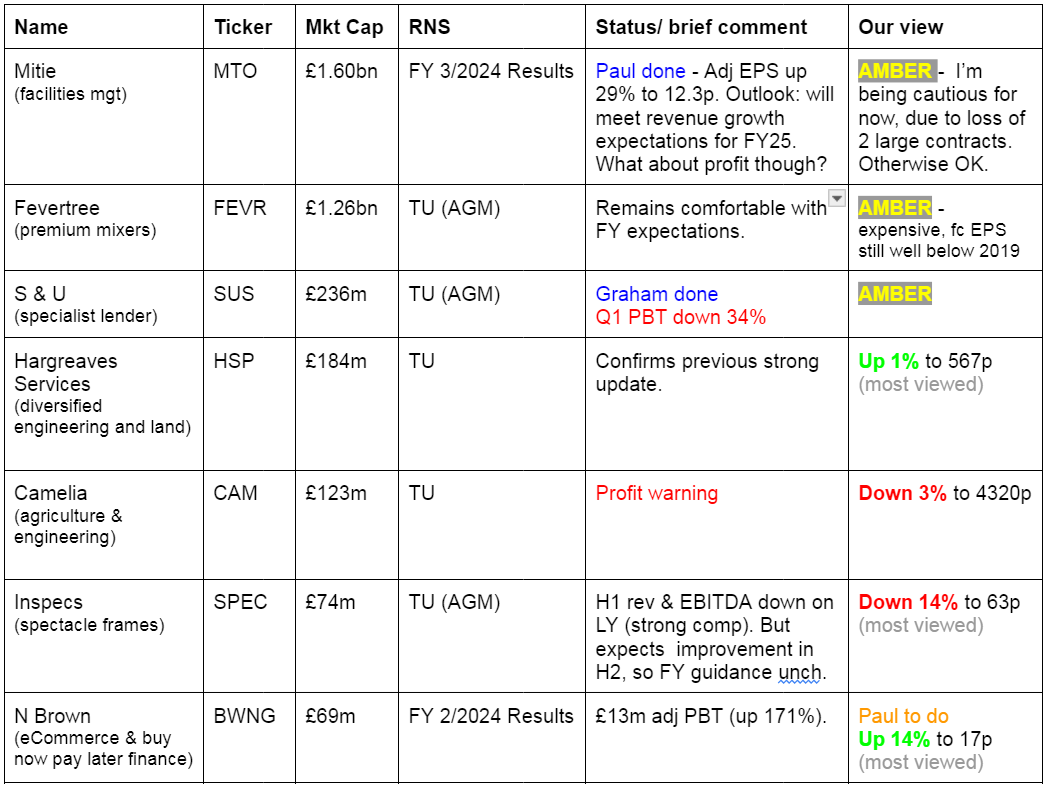

MITIE (LON:MTO) - up 2% to 122p (£1.63bn) - FY 3/2024 Results - Paul - AMBER

Excellent growth in profit, but a slightly wobbly outlook due to loss of 2 large contracts. I have a proper rummage into the numbers below, and am generally happy that everything looks OK. Maybe I could have been a bit more generous than amber, but I want to see how FY 3/2025 progresses, given the lost contracts.

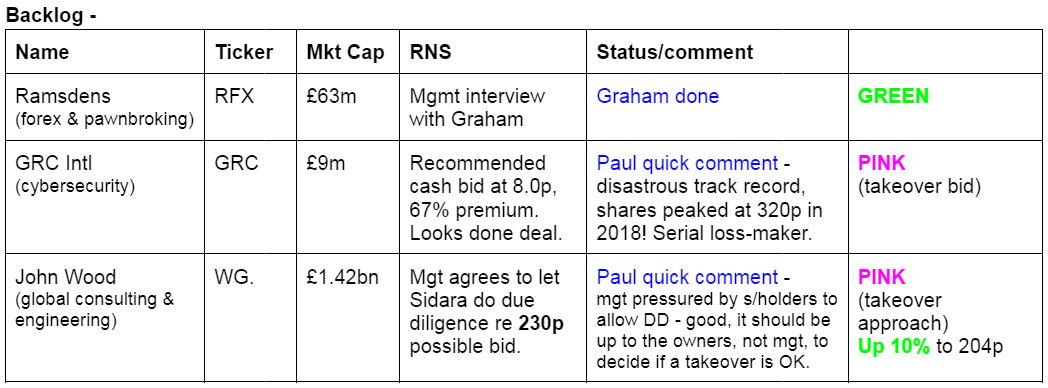

Ramsdens Holdings (LON:RFX) - 199p (£63m) - Graham - GREEN

I provide my typed up notes after getting a Q&A session with the management at Ramsdens. Nearly all questions were provided by readers and we covered everything from regulatory risk to competition to the company’s new travel card product. A great way to understand not just the company but also how management thinks about the challenges they face.

S&U (LON:SUS) - down 4% to £18.75p (£228m) - AGM Statement and Trading Update - Graham - AMBER

This update reveals a sharp fall in Q1 PBT as motor finance repayments have fallen further. Discussions with the FCA/Skilled Person are ongoing and S&U feel that they must be cautious in relation to how they approach repayments in these circumstances. I am similarly cautious on the stock until we have clarity.

Paul’s Section:

MITIE (LON:MTO)

Up 2% to 122p (£1.63bn) - FY 3/2024 Results - Paul - AMBER

I’ll start with Mitie shares (facilities management group) today, as the figures look good, and the valuation reasonable. I moderated my view to amber last time on 15/4/2024 because shares had risen strongly to 120p and I wondered if they were up with events?

A strong headline for the FY 3/2024 Results -

A record year of delivery

Revenue +11%; Operating profit +30%; EPS +29%

Here are some key numbers vs guidance, FY 3/2024 -

Revenue is massive at £4,511m (guidance: at least £4.5bn, tick!)

Adj operating profit £210m (guidance: at least £200m, double tick!)

Adj PBT £201m

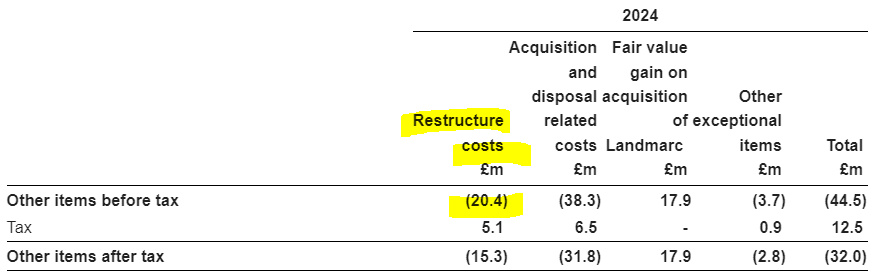

That’s all good, but note that adjustments are considerable at £44.5m, making statutory PBT of £156m, 22% lower than adjusted PBT.

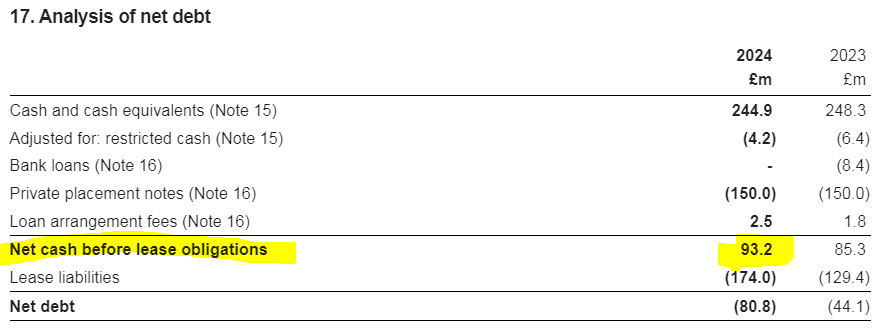

Closing net debt £80.8m (guidance: £85m, another tick) - NB this includes leases, it's actually net cash excluding them.

Contract renewals rate fell from >90% in FY3/23, to 79% in FY3/24 due to “the loss of two notable contracts”.

Adj EPS up strongly, 29% to 12.3p - giving a PER of 9.9x (looks decent value). This seems to be ahead of broker consensus of 11.1p - so I think it might be an earnings beat, but there are no broker notes available, so I can’t be certain (because figures are often worked out differently, adjusted in different ways, etc, diluted or not, so we may not be comparing apples with apples).

Total divis up 38% to 4.0p, yield of 3.3%, plus buybacks are ongoing too.

Huge order book of £11.4bn (up from £9.7bn a year earlier), and even bigger pipeline.

“Our divisions are all performing well”

“we have met or significantly exceeded all of the financial targets set out in the previous Three-Year Plan (FY22 - FY24), and this has been reflected in Mitie's Total Shareholder Return over the period (80% TSR; #10 in FTSE 250).”

Adjustments to profit - are they reasonable? See note 4 below. I accept acquisition-related adjustments (usually goodwill) which is customary to adjust out, and is just a book entry and nothing to do with actual trading.

However Mitie seems rather too regularly to adjust out restructuring costs. £20m this year, and £17m last year. I’d argue that for a sprawling group like this (with 68k staff) there are always going to be parts of the group that need to be reorganised in the normal course of business. This is about 10% of profit, so I personally would adjust EPS down by about 10% to better reflect reality that these costs are real, and do seem to repeat in some form each year.

Outlook - this strikes me as sounding a little wobbly in the short term -

"We have secured a number of new contracts and projects in the fourth quarter of FY24 and first quarter of FY25, which give us good business momentum and we expect to offset, in the medium-term, the contracts lost and ending in FY24. Margin enhancement initiatives are also expected to deliver further benefits in the current year, and we will continue to generate strong cash flows and enhanced shareholder returns.

"FY25 will be another year of delivery towards our medium-term targets and meeting our high single digit revenue growth expectations for the year."

The key thing I look for in all outlook comments is simple confirmation that trading is in line with expectations. Mitie dodges saying that today, which together with the contract losses and comments above about medium term recouping the losses, suggests that there might be a question mark over performance in the new year, FY 3/2025.

Balance sheet - is not good. NAV of £474m includes £645m of intangible assets (mostly goodwill, but also includes £50m of capitalised software and development spend). NTAV is negative, at £(171)m.

Mitie had £245m in cash on 31/3/2024. It had £150m of gross borrowings (US private placement notes - unsecured, but with typical covenants it says have been complied with) which are mostly very cheap, at a fixed coupon of 2.94%, a canny move, with an average maturity of 10 years from 2022. Secure, cheap borrowings, good to see.

There also seems to be an unused £250m RCF to Oct 2027.

Overall then the liquidity position looks comfortable, hence I’m not overly concerned about the negative overall NTAV.

Average daily net debt is the key additional disclosure we need from all companies, and MTO gets a gold star from me with this disclosure -

The Group uses an average net debt measure as this reflects its financing requirements throughout the period. The Group calculates its average net debt based on the daily closing figures, including its foreign currency bank loans translated at the closing exchange rate for the previous month end. This measure showed average daily net debt of £160.7m for the year ended 31 March 2024, compared with £84.3m for the year ended 31 March 2023.

Note the Mitie seems to include lease liabilities in its figures, whereas I want to see the net debt excluding leases, which better reflects reality in my view. Leases are future operating costs, not debt (since they can’t be withdrawn, don’t have covenants, etc, so completely different to other forms of debt).

Here we are, note 17 shows that Mitie is actually holding net cash excluding leases, so I wonder why they haven’t given proper prominence to this favourable point? A presentational own goal here - which makes the group look higher risk than it actually is -

Overall this looks fine I think.

Note that there is almost nothing in inventories, which means Mitie can operate OK with a leaner balance sheet than say a manufacturing company which would have to fund substantial inventories.

Large and public sector clients can often be good payers too (with little to no bad debt risk), if favourable payment terms are negotiated into the contracts, which it looks like MTO already does.

Pensions - the cashflow statement shows £13.2m in “defined benefit pension contributions” going out, so it looks as if there are still deficit recovery cash outflows.

Note 19 indicates that £18.1m + £22.1m was paid into defined contribution, and auto-enrolment schemes, but these are fine because they go through the P&L statement as a payroll cost. No problem there. It’s the defined benefit pension schemes that are a menace if they’re in actuarial deficit, because deficit recovery cash payments do not go through the P&L, so they’re an additional cash outflow with money that could otherwise have been paid out in divis. Hence why shares with big deficits on their pension schemes are usually priced on low PERs to adjust for this. Although higher interest rates are causing some big improvements in some pension schemes, so an interesting area with potential opportunities.

It seems that the deficit at Mitie has indeed improved dramatically, and hence I think we can tick off pensions from my list of potential concerns, as not being significant -

The most recent triennial valuation was carried out as at 31 March 2023, which indicated an actuarial deficit of £19.4m, an improvement of £72.7m since the last valuation. During the year, Mitie paid £10.6m of deficit repair contributions and the Group has agreed to pay total deficit repair contributions of £22.5m over the next four years.

Cashflow statement - share based payments of £20.3m (LY: £17.3m) is almost 10% of operating profit, so management have got their hands deep in the till.

Post-tax cash generation is much better this year at £198m (LY: £83m) but that’s mainly due to a large negative move in receivables last year reversing this year. I would deduct £41m in lease payments too, which appear further down.

The main use of the cash generated is £34m acquisitions, and shareholder returns of £78m buybacks, and £42m divis paid.

So it’s a genuinely cash generative business that is mostly using that cash for shareholder returns, pretty good.

Paul’s opinion - hopefully I picked up all the main points there. Annual accounts are a good opportunity to have a good rummage and find the things that companies don’t want to tell you in their trading updates!

I can’t find anything serious here, it mostly looks pretty good.

My main concern though is the outlook section, where two lost contracts is clearly having some impact on FY 3/2025. I’m worried that this could cause brokers to slip through some moderation of the forecasts perhaps? Maybe not, and the valuation is quite modest really at about 11x existing consensus for FY 3/2025. Although if I make my adjustment for reversing the restructuring charge, then I get to a higher PER of about 12x. That’s not expensive, for what is a pretty impressive, large and cash generative business.

Let’s go with AMBER for now, as I’d like to see how the lost contracts affect the new year’s numbers before becoming more bullish, and the shares have had a lovely run from the 2020 lows, quadrupling. It’s in a nice up-trend, which might attract momentum buyers.

Very good StockRank of 92.

Graham’s Section:

Ramsdens Holdings (LON:RFX)

199p (£63m) - Graham - GREEN

Many thanks to readers for submitting your questions for my Q&A with Ramsdens Holdings (LON:RFX). I asked almost all of them.

Here are the written notes from my conversation with CEO Peter Kenyon and CFO Martin Clyburn.

Q1. Regulation.

I asked if the company was currently worried about the possibility of changes in lending regulations, especially with if there was a change in government.

A: They would be exceptionally surprised if the FCA changed the way they act towards pawnbrokers. There is a high bar in the UK on regulation, and some pawnbrokers do find this frustrating and exit the market. But pawnbroking is centuries old. The FCA knows that their previous actions have already had a huge impact on payday loans and doorstep lending.

Q2. Staff costs.

I asked about the company’s experience of wage inflation over the past 12 months and how they see it developing over the next year?

A: The real living wage has increased 10% in each of the last two years. Ramsdens has not responded by increasing the interest rate charged to pawnbroking customers, but there have been adjustments in the FX margin and the retail margin. They do not think a 10% increase every year is likely or sustainable, and they do not think there will be a 10% increase next year. Of course a Labour government may want to see a faster increase in wages.

The point was also made that Ramsdens is diversified and provides a range of goods and services. Wages aren’t the only cost and the company can efficiently spread out the impact of higher wages across its operations (vs. competitors where wages may be a higher percentage of their costs).

Q3. Competition.

I asked how they are finding competition during their expansion and generally, not just against their main pawnbroking competitor but also against smaller/independent operators.

A: They gave an example of Warrington where Albemarle Bond used to be active, but where Ramsdens and H&T are now both successful. In general, they can succeed in a town with a population as low as 9-10,000. But there are c. 350 towns across the UK with a population of 30,000 or more. So there are plenty of opportunities.

Another benefit of being diversified is that they can provide jewellery, pawnbroking, or whichever other services are most in demand in a particular area. They have also found that the high street in some ways offers weaker competition than it did before as travel agents have moved off the high street and jewellery chains have been shrinking their estates. Independent pawnbrokers often struggle to get the banking facilities which might enable them to expand to their 2nd or 3rd stores.

Q4. High value customers.

I asked about the “past due” number rising by £500k in yesterday’s results, due to one high value customer. Can they reveal how many high value customers they have and give information about the security on these loans, as we found it quite surprising that Ramsdens had this sort of exposure?

A: They helpfully revealed that they only have two customers with borrowings of more than £100k. One of them has borrowed on a watch, and the other has borrowed on gold jewellery. The interest rates on these loans are lower than Ramsdens normally charges, as they are high-value loans. However the loan-to-value is within the 75% limit that applies to all Ramsdens loans.

Q5. Travel cards.

I asked how Ramsdens can compete with a prepaid travel card product seeing as travellers have many similar products to choose from.

A: Ramsdens has had over 1 million customers. They have 168 stores that customers can walk into and touch. And they think their prepaid currency card is a better product than the card offered by the Post Office.

When it comes to the likes of Revolut and similar online offerings, they think those products are less straightforward for customers than the Ramsdens travel card, and they query whether these products make any money and if the companies behind them will be around for the long-term.

Q6. Travel cards part 2.

I asked if the company shared customer concerns that prepaid travel cards might end up with large amounts of money left on them, that people might find it difficult to get their money back out of them, and that customers might suffer high fees for refunds.

A: They do think about this issue and answered this question in a number of ways. Firstly, they pointed out that it’s normal for travel cards to start charging utilisation fees on unused balances after 12 months. Their own card does not charge these fees for 18 months.

Secondly, they said that in partnership with Mastercard, they do speak to customers to urge them to make sure that they use their card! They want this product to succeed because customers are using their balances on holiday, not through fees on dormant balances.

They also pointed out that the prepaid card can be topped up in real-time, while on holiday (at a competitive price). So people don’t need to add more than they intend to use. And if they wish, they can always convert back to Sterling and use their remaining balance when they get home.

Graham’s view: this was a very helpful interview for me and I hope you have found it useful, too. I feel more knowledgeable about this company than ever before! And I’m happy to maintain a positive stance on it.

Huge thanks to Tommy H, davisj99, cheeky_minnows and ridavies for all the questions, even if I didn’t get around to every single one of them.

S&U (LON:SUS)

Down 4% to £18.75p (£228m) - AGM Statement and Trading Update - Graham - AMBER

I was previously a huge fan of this stock, and in many ways I still am. However, I have felt obliged to take a neutral stance due to some regulatory question marks hanging over it (for the avoidance of doubt, I am confident that S&U have done absolutely nothing wrong. But I do not know if the FCA will agree.)

The share price over the past year has reflected these concerns:

Today’s update continues the theme.

In relation to the motor finance division (“Advantage Finance”), we have the following news:

At Advantage, our cautious approach to repayments in the light of continuing discussions with the FCA and Skilled Person on interpreting and adapting to the new Consumer Duty regime and the sector wide review of Borrowers in Financial Difficulty, have had a significant impact on repayments and profitability. We anticipate that these discussions will be concluded during the second half of the year, when we will welcome the new regulatory clarity which will provide a strong platform for the continuing growth of the business.

I’m sure that investors will also welcome clarity, and I’ll be glad to take a “GREEN” stance on S&U again, when it’s clear what we are dealing with in terms of regulatory action.

The result of these circumstances is that Q1 PBT is only £6.9m (Q1 last year: £10.5m).

They say: “Increased impairment provisioning arising from the lower repayments at Advantage accounted for £3.6m of this reduction [in PBT]”,

If my maths is correct, this means that a normal repayment experience would have resulted in a flat PBT performance.

Forecasts published by Edison in April this year suggested that the full-year adj. PBT result would be £37.3m. S&U tend not to use many adjustments in their results so I’m inclined to treat this as a forecast for clean PBT.

That being the case, Q1 PBT of only £6.9m leaves a lot of work to do over the rest of the year, if the forecast is to be met.

Advantage Finance

Some more detail that is worth emphasising:

Advantage's discussions with the regulators mainly revolve around affordability and forbearance, arising from the FCA's industry-wide focus on borrowers in financial difficulty. These come as industrywide used car advances are 7% down on 2023, accompanied by a 6% fall in transaction numbers. However, demand for Advantage's products remains strong…

Due to S&U’s caution in this period of regulatory uncertainty, live monthly collections have reduced from 92.1% at the end of January to 87.7% in Q1. But there is hope:

Belated recognition by regulators that for some customers repossession may be the best outcome, is gradually seeing a return to normality. Hence Advantage's empathetic and flexible customer relations are also expected to resume in the second half of the year.

Live collections had previously been as high as 94% - see my report in Dec 2023 when I first switched to a neutral stance on this stock, noting that collections had started to drop off.

Aspen Bridging

This property finance company continues to grow with advances in Q1 more than doubling year-on-year. PBT in Q1 was £1.45m, and ROCE reached 11%.

Comment on the outlook for Aspen:

More promising still are signs in the UK residential market of an increase in sales instructions and prices. Nationwide recently reported the latter up 1.3% on last year, despite a delay by the Bank of England in reducing interest rates. Aspen expects both favourable trends to continue and possibly accelerate.

S&U’s borrowings: £237m vs. facilities of £280m.

Chairman comment:

Although fully cognisant of the challenges currently being negotiated at Advantage, an improving economic outlook both for consumers and businesses, a strong labour market and greater political stability will all benefit S&U over the coming year. We wrestle on with confidence."

I’ve remarked in previous articles on how downbeat he has been. This is the most positive collection of words I’ve heard from him in a while!

Graham’s view

The situation at Advantage is fluid with a range of possible outcomes over the next 6-12 months. Will the regulators do nothing (unlikely), make cosmetic changes (quite possible) or could they seriously hamper S&U’s ability to trade? Could they find instances of wrongdoing by S&U?

The problem for investors is that it’s often very difficult to predict what view a regulator might take. But based on what I know about Advantage Finance, it seems to me that it’s a responsible and reasonable lender. So I don’t expect that it should face any worse outcome than any other lender in the industry.

But with the regulatory review ongoing, I still don’t think I can raise my neutral stance.

For those with even more confidence than I have in S&U, the shares can now be purchased at a very reasonable valuation offering plenty of upside when the dust settles. But personally I’d prefer to wait until I know for sure what the FCA is thinking.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.