Good morning from Paul & Graham.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda - to follow.

Graham’s Section:

S&U (LON:SUS)

Share price: £20.90 (pre-market)

Market cap: £254m

This specialist lender issues a full-year trading statement for the year ending 31st January.

We covered the last update, issued in early December, here.

Thankfully, trading in both of S&U’s operating businesses remains “excellent” and the full-year results will “meet expectations and exceed budget”.

The company notes that “UK business confidence is reported by the ICAEW to be a thirteen year low whilst a potential recession and rising interest rates continue to pose challenges” - and I agree that this adds to the impressiveness of S&U’s performance.

Their loan books continue to grow strongly even at the same time as lending criteria are tightened:

Despite the period seeing prudent adjustments to underwriting and the scorecard, and some rate increases to protect net interest margins as both operational and financial costs grow, group net receivables have now reached c£420m against £370m at the half year. That ultimate measure of quality - collections - remains good in both businesses.

Motor finance division (Advantage Finance)

This loan book is now £306m (up from £296m two months ago).

S&U argues that these customers are “nearer” to prime than they were bevore, after lending criteria were tightened up. They also “marginally” reduced interest rates in this division, “to attract a higher quality customer profile”.

Average loan size has increased 9% to £7,800, loan terms have lengthened (they can afford to do this for more creditworthy customers), and importantly transaction volumes increased 21% versus the prior financial year, as the car market recovers from its many Covid-related problems.

This loan book is now £114m (up from £108m two months ago).

I’m relieved to think that this division might be slowing down. As a new venture, in a property market that has some issues, do they need to go hell for leather? I don’t think so.

House prices have now been reported to have fallen for five consecutive months, whilst mortgage approvals and transaction activity have been restricted by rising interest rates and cost of living pressures.

These trends are expected to continue during 2023. Prudence has therefore dictated further rises in Aspen's own interest rate and tightening of its already conservative loan-to-value requirements.

Even at a slower pace of growth, profits at Aspen have still exceeded budget, thanks to the lack of customer defaults.

Funding - I’ve noted previously that S&U’s borrowing facilities don’t seem to be big enough. They will need to increase them again soon, to accommodate current growth. However, debt funding as a percentage of their total balance sheet is likely to remain conservative, in my view (I’ll check this again when full-year results are published).

Second dividend - 38p, up from 36p last year (S&U pays three dividends each year).

Chairman comment:

Whilst the uncertainties of forecasting and fly casting have much in common, 2023 is likely to see constrained levels of consumer confidence and spending in the UK. Nevertheless, historically this has and, I believe, will continue to present good, responsible, lending opportunities for S&U.

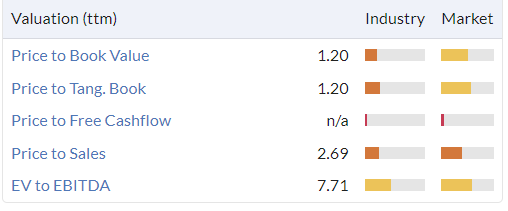

My view

No reason at all for me to change my view on this one. A modest premium to book value for a family business that historically and currently earns terrific ROE, seemingly without excessive risk, strikes me as more than fair:

Argo Blockchain (LON:ARB)

Share price: 17p (-6%)

Market cap: £81m

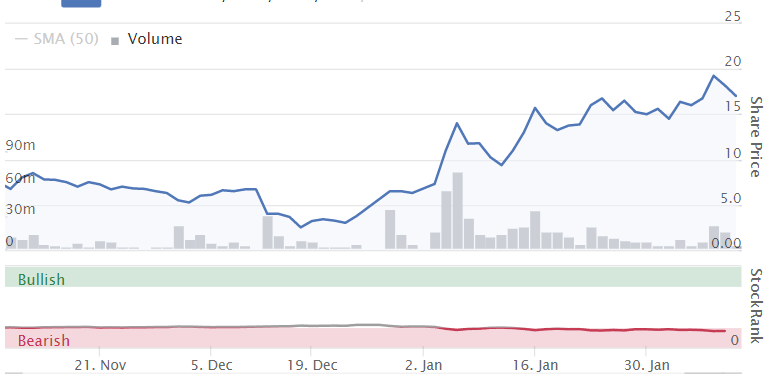

This bitcoin miner has enjoyed a renaissance in its share price ever since the December announcement of a major refinancing agreement (which we covered here).

The deal meant selling the ownership of its Texas facility to a specialist lender, “Galaxy Digital Holdings”. This helped to deleverage the balance sheet, but it also means that Argo is on the hook for both interest and rental payments to Galaxy from now on.

However, that’s not what today’s news is about. Today we learn that the Argo CEO (who lives in Canada) is stepping down, “to pursue other opportunities”.

He says:

It has been a great privilege to have led Argo Blockchain over the past three years. It has been quite a journey, and we have come a long way. I am pleased to have recently led the successful Galaxy deal, and I thank all my colleagues at Argo for their dedication, support, and enthusiasm in driving Argo forward. Onwards and upwards!"

Here’s the Argo share price over the past three years. Quite a journey indeed!

Last year, I checked out Mr. Wall’s career history, to see how he came to lead a crypto mining business.

A background in computing, perhaps in hardware or cryptography, is what I expected to find. But instead I found that he was a filmmaker.

This is no secret - his LinkedIn clearly shows that he has many years of experience in videojournalism, and he has also been involved in events management, building a co-working space, and corporate communications.

Ten years ago, he gave an excellent TedX talk in which he described the benefits of making fun films with his kids on their holidays.

Now maybe you’ll think it’s unfair to question the credentials of a CEO after he is gone. Perhaps it is. But I think we really need to look for CEOs who have a passion and a strong professional background in the specific industry in which their company operates. I don’t think it’s too much to ask.

Based on the presentations I’ve viewed, Mr. Wall is extremely likeable. A great communicator and very funny. Probably a great leader to work for. It’s easy to understand how he inspired thousands of private investors to believe in his project.

However, many of these investors have been led off a financial cliff as the Argo share price has soared and then crashed over the past few years. The risks the company took with its balance sheet were reckless - I discussed them here, when the market cap was still nearly £200m.

Lawsuit - I note in passing that Argo and various of its Directors are being sued in New York in connection with their 2021 US IPO. The lawsuit alleges that:

…the Offering Documents and Defendants made false and/or misleading statements and/or failed to disclose that: (i) Argo was highly susceptible to and/or suffered from significant capital constraints, electricity and other costs, and network difficulties; (ii) the foregoing issues hampered, inter alia, Argo’s ability to mine BTC, execute its business strategy, meet its obligations, and operate its Helios facility; (iii) as a result, Argo’s business was less sustainable than Defendants had led investors to believe; (iv) accordingly, Argo’s business and financial prospects were overstated; and (v) as a result, the Offering Documents and Defendants’ public statements throughout the Class Period were materially false and/or misleading and failed to state information required to be stated therein.

The complaint can be read for free here. The case should make for an interesting comparison of how listed companies are treated in the UK vs. the US.

My view is that Argo should hire a CEO with a strong professional background in computing. It should also pursue a sustainable financial strategy. This strategy might be less exciting to the crowd, but it could last.

As for the merits of these shares currently, I would say they are uninvestable. The company has not published useful financial information for some time, it will bleed cash to Galaxy Digital for the foreseeable future, and it has lost its CEO. I would continue to enthusiastically avoid these shares.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.