Good morning from Paul & Graham!

It's another quiet news day, everyone's on holiday I suppose!

In case you missed it, I added a couple more sections later in the day to yesterday's report, on Stelrad (LON:SRAD) [GREEN] and Team Internet (LON:TIG) [AMBER/RED].

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia.

Other movers (with news)

Crest Nicholson Holdings (LON:CRST) - down 16% to 221p (£569m) - Bellway willnot be bidding - Paul - No view

Bellway says -

Bellway confirms that it does not intend to make a firm offer for Crest Nicholson.

No reason was given.

Crest Nicholson says -

The Board of Crest Nicholson Holdings plc ("Crest Nicholson") notes the recent announcement by Bellway p.l.c. ("Bellway") confirming that it does not intend to make a firm offer for Crest Nicholson under Rule 2.8 of the Takeover Code.

As previously announced, the Board of Crest Nicholson had engaged with Bellway in relation to a possible all-share offer for Crest Nicholson in response to a series of unsolicited proposals from Bellway.

As outlined in its half year results on 13 June 2024 for the period ended 30 April 2024, Crest Nicholson remains confident in its standalone prospects, in particular given conclusion of the review of provisions for completed development sites supported by external consultants, its highly attractive land portfolio and the new leadership of Martyn Clark.

This announcement has been made without the consent of Bellway.

Paul's view - none at present, I need to digest this. We previously liked the discount to NTAV at CRST, but it has been accident-prone with historic issues.

Summaries

Just (LON:JUST) - up 11% to 131p (£1.35bn) - H1 Results - Paul - AMBER

Very upbeat commentary, and says it's going to "substantially exceed" previous guidance. However, the numbers rely heavily on big adjustments. Looking through its large & complicated balance sheet reminds me why I don't touch this sector! On the upside, shares are in a lovely bull trend, and the market has responded very positively to today's announcement.

Genuit (LON:GEN) - down 4% to 448.5p (£1.12bn) - Half-year Report - Graham - AMBER

A mixed bag here. The statutory results are impacted by an impairment charge but if you are willing to look past the adjusting items, the profit result is not bad in the circumstances. The company says it is on track for full-year expectations (underlying operating profit £92-96m) even though it expects its end-markets to remain subdued. I run some comparisons with Marshalls (covered yesterday) and decide that I like Genuit more, although it’s not a high-conviction stance from me.

Synthomer (LON:SYNT) - up 2% to 241p (£394m) - H1 Results - Paul - AMBER/RED

No real sign of recovery in trading yet. Meanwhile its excessive debt means that finance costs consume all the operating profit, leaving nothing remaining to reduce the principal. However, bondholders don't perceive risk, with a normal coupon on the recently refinanced 2029 bond, which is even now trading at a 5% premium. Shareholders have to hope for a big recovery in profits, as currently this is a £2bn pa revenue group that doesn't make a bean in profit or cashflow.

Paul’s Section:

Synthomer (LON:SYNT)

Up 2% to 241p (£394m) - H1 Results - Paul - AMBER/RED

This is a substantial, international business -

“Synthomer plc is a leading supplier of high-performance, highly specialised polymers and ingredients that play vital roles in key sectors such as coatings, construction, adhesives, and health and protection - growing markets that serve billions of end users worldwide. Headquartered in London, UK and listed there since 1971, we employ c.4,200 employees across our five innovation centres of excellence and more than 30 manufacturing sites across Europe, North America, Middle East and Asia. “

However, it got into a serious mess due to reckless, excessive borrowings (which we warned about here in 2022), which combined with a drop in demand in 2023, forced it into a dilutive equity raise, and then a 20:1 share consolidation. As a result of which a great deal of shareholder value was destroyed, as you can see (the chart will have been adjusted for the share consolidation) -

The question now is whether the business is recovering (it was previously a decently profitable business pre-pandemic), or whether former customers are getting their products coated elsewhere? The other key question is whether its overly indebted balance sheet has been fixed? (the answer to that is no!)

The H1 highlights table seems to be showing a fairly static trading situation. 7% EBITDA margin doesn’t seem to demonstrate much pricing power, given it has large fixed assets (whose depreciation charge is ignored by EBITDA), plus very heavy finance costs from all the debt (£27m net finance charge in H1, annualises to £54m).

More realistic numbers further down show adj PBT at breakeven, of £0.1m.

Then there’s £32.5m of adjustments, taking the H1 statutory PBT to £(32.4)m loss before tax. Adjustments are mainly goodwill amortisation, which it’s customary to adjust out. Although note it’s still showing restructuring costs as adjustments, despite being at a similar level to H1 last year at £6.7m.

Note there’s £37.6m on the balance sheet as provisions, which are future cash outflows, for restructuring and onerous contracts.

Pensions are also an issue here, with a net £50.7m accounting deficit.

Debt - the big equity raise last year got SYNT out of immediate trouble, but I think it still has far too much remaining debt, which will take years to reduce from cashflow. Maybe there are more disposals that could help bring it lower?

Although refinancing its bonds is a positive sign, and extends maturities nicely -

“At 30 June 2024, net debt was £560.6m (30 June 2023: £795.8m, 31 December 2023: £499.7m). The increase since the year end principally reflects settlement of the EC fine in January, the divestment proceeds of the Compounds business and the Free Cash Flow movements noted above.

In April, we successfully tendered for €370m of our bonds due 2025 reducing gross debt and extending maturities by issuing €350m of bonds due 2029.”

The coupon on its 2029 bonds is 7.375%, which is a surprisingly small premium to the risk-free rate, so clearly bondholders are relaxed about default risk. In recent months the 2029 bonds have moved to a premium to par, now priced at c.105. I didn’t expect to see that, but there we are. The bond market isn’t worried about the debt at all, by the looks of it.

It’s somewhat different for equity holders though, as we take all the risk, and don’t get paid anything in divis until debt has come down to something more sensible.

There’s more debt beyond the bonds though, and the leverage multiple is way above what I would consider normal -

“As at 30 June 2024, committed borrowing facilities principally comprised: a €300m RCF maturing in July 2027, €350m of five-year 7.375% senior unsecured loan notes maturing May 2029, the remaining €150m outstanding of five-year 3.875% senior unsecured loan notes maturing July 2025 and the UK Export Finance (UKEF) facilities of €288m and $230m both maturing October 2027. At 30 June 2024, the RCF was undrawn and the UKEF facilities were fully drawn. The Group's net debt: EBITDA for the purposes of the leverage ratio covenant increased from 4.2x at 31 December 2023 to 4.7x at 30 June 2024, principally due to the higher net debt at the period end, as described elsewhere.

The RCF and the UKEF facilities are subject to one leverage ratio covenant. For prudence, the Group agreed in March 2024 to extend the period of temporary covenant relaxation to ensure that appropriate headroom was maintained. Accordingly, the net debt: EBITDA ratios required under the covenant have been set at not more than 6.0x in June 2024, 5.75x in December 2024, 5.0x in June 2025 and 4.75x in December 2025. Reducing leverage further towards our 1-2x medium-term target range remains a key priority for the Group.”

Overall then, I view this as a dangerously highly geared business, which has been given time by the lenders to reduce debt significantly. Hence I would forget any idea of shareholders receiving any divis for the foreseeable future.

What if cashflows don’t improve, and it can’t reduce debt? Then it would probably need to do another equity fundraise in maybe 2-3 years’ time. Remember bondholders don’t care about equity being savagely diluted, as it doesn’t affect them. So I think equity dilution risk here is still elevated, although not immediate.

Debt is expensive too, consuming all of the operating profit right now -

“The Group expects net financing costs of c.£60-65m in 2024 and c.£65-70m in 2025 as a result of higher interest rates, the recent bond refinancing and other changes to the Group's financing arrangements. The Group's committed liquidity at 30 June 2024 was in excess of £500m.”

If they’re struggling to pay the interest, then they can’t repay any principal. Trading has to dramatically improve to make this situation comfortable, and there’s no sign of that yet.

Outlook - uninspiring, but at least they’re being realistic here -

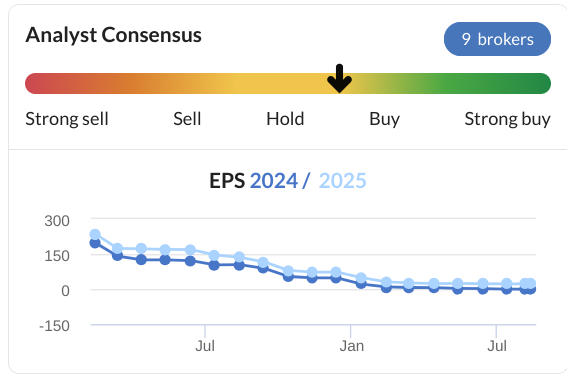

Broker forecasts - note the very poor trend in broker consensus below. Have end markets really fallen this much, or are competitors getting the business instead, or at least forcing lower pricing on SYNT maybe?

Paul’s opinion - I think this is still quite a big mess. Bulls must be hoping to see a dramatic improvement in future profitability, which is needed to reduce debt down to more normal levels.

To me, risk:reward seems poor right now, with a mountain of debt to service, let alone repay.

Cashflow looks very poor in H1, and wasn’t great last year either, with the only significant cash inflows coming from disposals, and the £266m equity fundraise last year. I reckon that probably won’t be the last equity raise.

Remember I’m only analysing the basic numbers, not trying to predict how the business will perform in future. If you think there’s a spectacular turnaround opportunity here, then it might be worth taking on all the risk. Each 1% rise in profit margin is £20m extra profit - not bad if they can raise margins in an economic recovery.

For me, it has to be AMBER/RED again, to flag that this is still an overly-indebted business, and it’s not trading very well either, with no particular upside yet apparent in the outlook comments either. Shareholders have to hope that changes for the better.

Maybe I've missed something, as the StockRanks are mildly positive on this share -

Just (LON:JUST)

Up 11% to 131p (£1.35bn) - H1 Results - Paul - AMBER

“The insurance segment writes insurance products for the retirement market – which include Guaranteed Income for Life Solutions, Defined Benefit De-risking Solutions, Care Plans and Protection – and invests the premiums received from these contracts in debt and other fixed income securities, gilts, liquidity funds, Lifetime Mortgage advances and other illiquid assets.

The advisory segments of the professional services business, HUB, represents the other operating segments.”

This is reflected in a large & complicated balance sheet, which has £31.0bn in financial investments - mainly bonds/gilts. Total assets are £33.4bn.

The creditors side of the balance sheet is mainly £24.9bn insurance contract liabilities - which will be the future payments it has to pay out to pensioners. There are £7.25bn other liabilities.

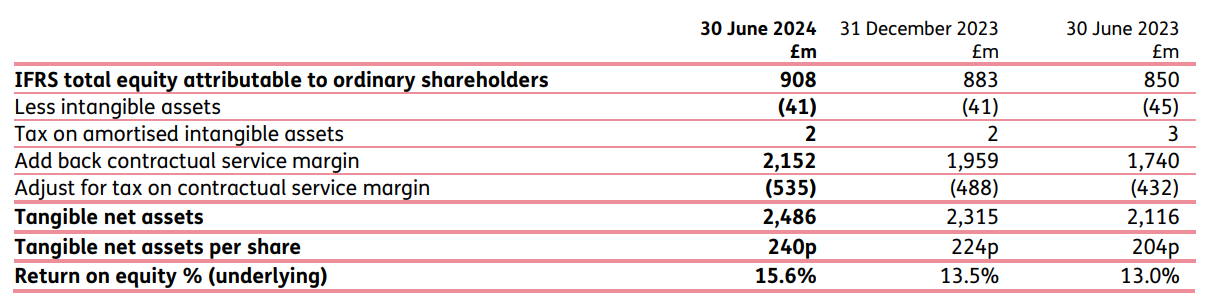

This leaves only a sliver of equity, at £908m, plus £322m “tier 1 notes” shown separately, giving a total equity of £1.23bn. That means equity is only 3.8% of total liabilities. So it wouldn’t take a large or unexpected change in any of the big assets or creditor lines, to have a very highly geared impact (or benefit) to total equity. This is what puts me off investing in insurers, banks, etc, as their profit figures are a combination of estimates and assumptions, on very large balance sheet numbers. We have to take it on trust that all the accounting is being done prudently, and that nothing untoward is being covered up.

The share price has risen c.11% today, which takes the market cap up to c.£1.35bn, which is slightly above NAV of £1.23bn (there are only £41m of intangible assets, so I’ve ignored that as immaterial).

The company reckons it has 240p/share in NTAV, way above how I calculate it. The reason is they’re heavily adjusting this figure! -

I’ve just had a look for comparison at the much larger balance sheet at Legal & General (LON:LGEN) and this is even more extreme, with equity of only £3.9bn, versus total liabilities of £522.6bn! Under 1% equity compared with the huge liabilities. I’m surprised that large insurance companies like this are so weakly capitalised, and yet still meet the capital requirement regulations.

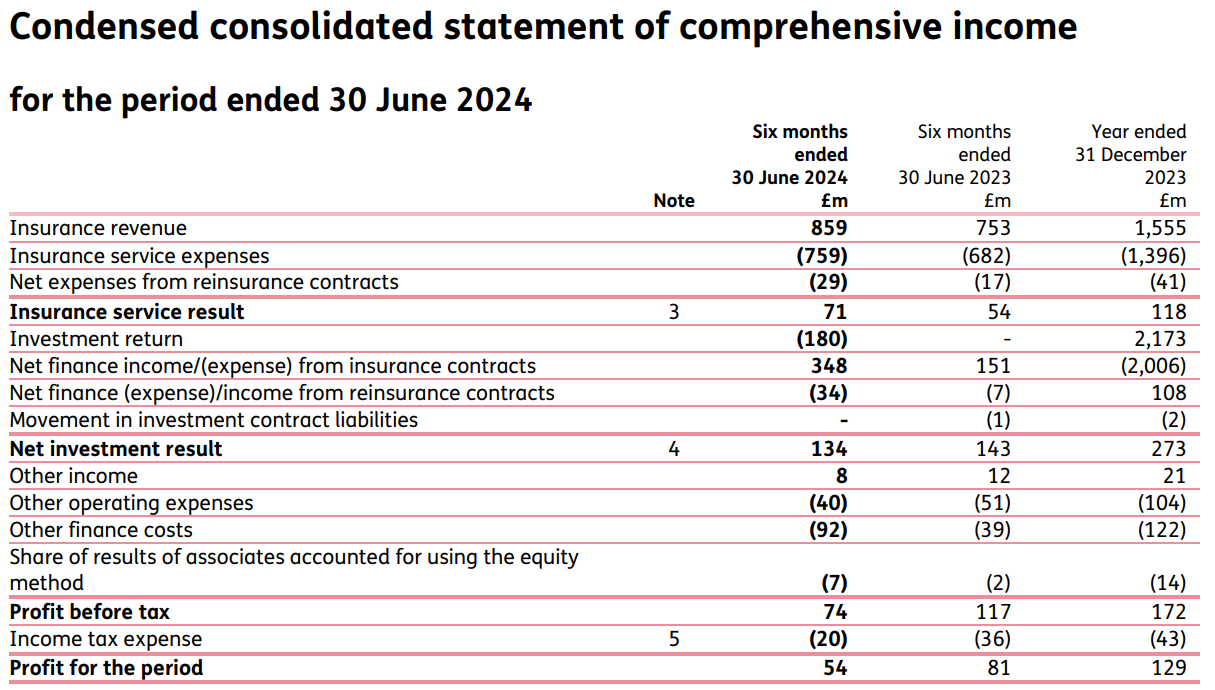

H1 profit - this P&L below is in a format I’m not familiar with - I didn’t really want to review this company (I marked it as too complicated last time I had a look here on 8/3/2024), but given that there’s so little other news, and its share price is so strong, I felt obliged to take a closer look today.

The number that stands out is the £(180)m investment return in H1 this year.

Also how small the PBT figure is at £74m, well down on £117m in the H1 LY. This makes me wary, as the profit number (very much like the balance sheet equity) is a small sliver from much larger numbers, and not necessarily under the company’s control (eg investment returns, actuarial issues, etc), which further puts me off wanting to invest in this sector. It worries me that the bumper dividend yields (9.6% at LGEN) don’t have a lot of backing, so could be vulnerable if something unexpected were to happen.

Most highlighted profit comes from adjustments. Note the £74m H1 profit above, which becomes much larger thanks to big adjustments -

3 Contractual Service Margin.

Outlook - the commentary is bullish, and this bit below is clearly what’s driven the shares up strongly today -

“Given the strong first half outcome, the positive market dynamics, and our forward-looking pipeline, we expect to substantially exceed previous 2024 guidance of doubling 2021’s £211m operating profit in three years.”

“Momentum remains strong as we enter the second half of 2024. We forecast second half new business volumes to be similar to the excellent performance in the first half, albeit with slightly lower margins due to business mix. We expect the strong structural growth drivers of our markets to continue well into the future. “

Given that the profits are mainly coming from adjustments, plus numerous complicated accounting judgements, then personally I wouldn’t be particularly confident about relying on the adjusted numbers.

Paul’s opinion - not my sector at all, so this is just a review of the basic numbers from a generalist.

I can see why this share is in a bullish uptrend, as it seems to be winning plenty of new business, eg from companies wanting to de-risk their defined benefit pension schemes. Higher interest rates have created more favourable circumstances, often reducing deficits, and making it possible and affordable for companies to offload their pension schemes, eg as we’ve seen with several companies we follow here (eg recently Sanderson Design (LON:SDG) disposed of a small pension scheme to an insurer).

The insurers just have to hope that they’ve got all their actuarial calculations right, and that nothing untoward happens in future (eg medical advances) resulting in people living longer than expected.

Just is only paying a modest c.2% dividend yield. So the question for investors in this sector, is do you want a very much larger yield from a bigger insurer (eg LGEN at 9.6%), or do you accept a lower yield from JUST in the hope of it achieving faster growth, and not blowing itself up?!

Interest rates coming down could boost the value of JUST’s substantial bond portfolio maybe?

Another key point is your attitude towards the large adjustments JUST makes to its profit & balance sheet NTAV. If you accept those adjustments, then this share looks cheap.

With so many variable large numbers in the accounts, I question how reliable profit numbers are? It strikes me that these could be very volatile, hence applying a low PER is probably sensible.

As it’s not a sector I would ever invest in, for me it’s not of any interest, so I’ll sit on the fence with AMBER.

Investors are however enjoying a good bull run, so let’s hope it continues. Today’s bullish outlook comments seem to reinforce the upside.

Up until late 2020 the performance of JUST shares was poor. It’s now in an up-trend since then -

Graham’s Section:

Genuit (LON:GEN)

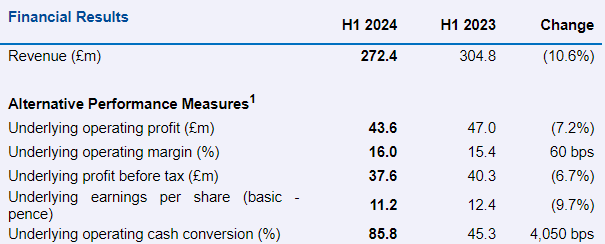

Down 4% to 448.5p (£1.12bn) - Half-year Report - Graham - AMBER

Genuit Group plc…, the UK's largest provider of sustainable water, climate and ventilation solutions for the built environment, today announces its unaudited interim results for the six months ended 30 June 2024.

It’s topical that we look at this one, after covering Marshalls (LON:MSLH) yesterday.

Genuit, formerly known as Polypipe, has enjoyed a share price recovery in 2024, but the long-term picture is uninspiring. Here’s a 3-year chart:

Here are Genuit’s interim results:

At least in this case we don’t have negative operating leverage: the fall in (adjusted) profitability is no larger (in fact it’s smaller) than the fall in revenue.

Adjusting items: unfortunately, the company has used a heavy set of adjusting items to smooth out the numbers. Actual operating profit is only £21m (down 41% year-on-year) while actual PBT is only £15m, down 48% year-on-year.

The culprit is a big impairment charge (£12m) that has increased the adjusting items from £7m to £19m.

The impairment is at ADEY, a company that makes products for heating and cooling systems (e.g. magnetic filters for boilers).

ADEY was acquired by Genuit/Polypipe in 2021, for a cash price of £210m. It was bought from LDC, the private equity arm of Lloyds.

Unfortunately, ADEY hasn’t lived up to the expectations attached to that buyout price:

Due to the ongoing softness in the boiler filter and chemicals market and a delay to recovery in volumes, related to a suppressed RMI market there has been a reduction in the value in use of the Adey CGU. This has resulted in an impairment charge of £12.4m… any negative changes in key assumptions would result in the recognition of an additional impairment loss.

Impairment is of course a non-cash charge, but It speaks to the success (or failure) of prior acquisitions to create value. So for a company that is likely to engage in more M&A, I think it’s good to be aware of impairment losses.

Genuit has £441m of remaining goodwill on its balance sheet, from all prior acquisitions including ADEY. Let’s hope that the impairment charges stop here.

Balance sheet: emphasising that this company has been built by acquisitions, it has balance sheet net assets of £627m. But if you take away goodwill and other acquired intangibles, and you are left with only around £50m.

Net debt: reduces to £122m (excluding leases). The leverage multiple of 1.1x is already modest but Genuit expects it to fall to 1.0x by year end, “providing further opportunities to deploy capital for accretive M&A”.

CEO comment excerpts:

"Whilst the market remains subdued in 2024, the Group demonstrated continued operating margin improvement in the first half over prior year, as the benefits of our strategic actions continue…

As we look forward into the second half, we currently anticipate these market conditions to remain, offset by continued operational and strategic progress. We continue to expect full year underlying operating profit to be within the range of analyst forecasts. The Genuit Group is exceptionally well positioned to benefit from eventual market recovery, with business simplification complete, at least 20% available capacity to ramp production and improved operational gearing providing confidence in medium term targets."

Outlook

Genuit expects more of the same in H2. “a backdrop of low volumes of new housebuilding, a softer commercial construction sector and an RMI market that has been waiting for interest rate reductions”, but they do expect to generate a profit within the range of forecasts.

The outlook statement from Genuit stands in contrast to Marshalls, who were “cautiously optimistic of a modest recovery” in H2, based on the assumption that the macro environment would improve.

There is no such optimism from Genuit, and I applaud them for it - it’s good to be ready for an economic recovery, but we can’t assume it will happen!

Forecasts: Genuit is forecast to generate an underlying operating profit of £92.1m - £96m this year.

Graham’s view

I apologise that I can’t bring a high-conviction positive or negative stance to this one.

As with Marshalls, I think there are easier ways to find value than to get involved here. But if you are very positive on the economy, then this cyclically exposed stock would probably be a fine way to express that view.

I do have a slight preference for this one over Marshalls. Marshalls seemed to hang their hat on a macroeconomic recovery in H2, and on the basis of that expectation they said their results would be “broadly” in line.

Genuit, on the other hand, seems to have no expectation of a recovery, and yet it says that its results are still trending in line - with no use of the word “broadly”!

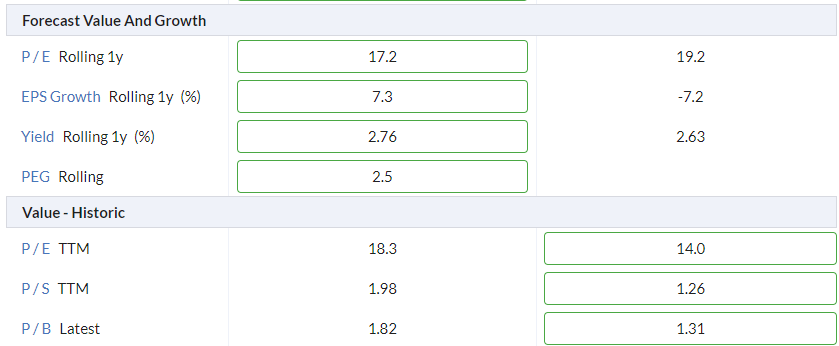

Stockopedia’s useful “Compare” tool agrees with me: in a head-to-head battle, Genuit wins 22 out of 37 comparisons.

Marshalls (right hand side) wins on historic value, but Genuit (left hand side) wins on forecast value and growth:

I also have a slight preference for the shareholder register at Genuit: it has more fund managers whose research I’d be happy to piggyback on (and who might not own it simply because it’s needed in an ETF)..

At the end of the day, though, I’m still neutral on this one.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.