Good morning from Paul & Graham.

Agenda -

Paul's Section:

accesso Technology (LON:ACSO) interim results seem to be in line with expectations, and this is confirmed for the full year too (with the key summer season now in the bag). Growth has almost entirely come from European markets bouncing back from the pandemic, with little underlying growth in evidence. The balance sheet looks great, with pots of cash. However, management seem to think spending $10m on shares for employees is more important than giving anything to shareholders, so the priorities don't look good. Cash generation is questionable too. Overall then, it's not for me.

Graham's Section:

Property Franchise (LON:TPFG) (£91m) - these interim results are in line with expectations, and the outlook is too. I’m a big fan of this company although I sold my small stake in it some time ago. Lettings revenues and other revenue streams have helped to cushion the blow caused by a sharp drop in UK sales transactions. The company was also very active on the acquisition front last year, and this caused some dilution, but at least the added businesses helped to produce growing revenues and PBT. Adjusted earnings per share for H1 are down by 8%, as a result of the dilution caused. I suspect that TPFG is well-positioned to make further progress, as soon as the economic backdrop allows for it.

Trustpilot (LON:TRST) (£319m) - this business review service reiterates its revenue guidance for 2022. But thanks to its “flexible operating model”, it expects “significantly more operating leverage in the second half of the year than previously anticipated”. The company remains unprofitable and has been expected to remain unprofitable for the foreseeable future, only reaching adjusted EBITDA breakeven two years from now. Perhaps it can speed up its progress towards positive net income but in the meanwhile I think there are signs of good operational progress. The potentially very strong network effects could help to create a very valuable company, in my view, although the risk of competition can’t be ruled out completely.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

accesso Technology (LON:ACSO)

590p (pre market open)

Market cap £244m

accesso Technology Group plc (AIM: ACSO), the premier technology solutions provider to leisure, entertainment, and cultural markets, today announces interim results for the six months ended 30 June 2022 ('H1 2022').

These are quite tricky numbers to analyse.

Going through my notes -

H1 revenues up 26% at $63.7m, which is mainly driven by a bounce back from depressed revenues in the prior year in the UK (its second largest market), due to the pandemic. So don’t expect this rate of revenue growth to continue. The largest market (USA/Canada) revenues only grew 4%.

Seasonality - Accesso normally has an H2 bias to revenues & profits.

Outlook - sounds OK -

Full year guidance expectation: With robust revenue growth, gross margin broadly in line with pre-pandemic levels, and a return of the cost base to more normal levels the Group expects its full year results, excluding the impact of its Food & Retail acquisition on its profit, to be in line with the Board's expectations at the start of the year.

Although there is a rather vague comment about a large customer, which seems to have reduced its spending with Accesso, but this sounds as if it’s been absorbed without impacting market expectations -

Short term change in dynamic with large accesso customer: Shift in strategy of large customer has significantly reduced their related virtual queuing revenue in the period and to a lesser degree impacted their eCommerce revenue. This pattern is expected to continue at least through 2022. The Group anticipates this dynamic to normalise long-term as customer's revised strategy takes hold.

Macro conditions - no apparent impact as yet -

We are not yet observing any negative dynamic in our marketplace and our most important trading period for the year is largely complete. Nevertheless, we are monitoring the situation closely.

Profitability - this is the tricky bit. The company trumpets $10.6m of “Cash EBITDA” in H1, but that only translates into $2.9m statutory PBT. Which figure should we be using? The bulk of the difference seems to be amortisation of intangibles, which I would usually ignore.

Capitalised development spending - this was previously a bugbear with Accesso, in that a very aggressive approach was taken, with a huge chunk of the payroll being capitalised. To be fair, this is no longer an issue, with only $0.8m development spend capitalised in H1.

Forex - there’s a large charge at the bottom of the P&L, for $4.9m, called “Exchange differences on translating foreign operations”

As it reports in dollars, and the dollar is strong, then I assume this must be something to do with converting non-dollar assets into dollars? If anyone talks to management or they do a webinar, this would be a useful question to ask for clarification.

EPS - adj basic EPS is up 104% to 13.0 US cents, for H1. With the seasonality, H2 should be higher. Note that EPS in 2021 was boosted by a negative tax charge, which seems to have been something to do with recognising a deferred tax asset.

Balance sheet - looks really good, better than I was expecting. NAV of $181.4m becomes NTAV of $68.4m, once intangible assets of £113m are written off.

Fixed assets are negligible, so this NTAV is sitting mainly in the bank account, with a very healthy $58.7m in net cash.

Where has all that cash come from? Mainly placings, as the share count has gone up from c.28m pre pandemic, to about 41.3m shares in issue now.

Dividends - given that Accesso has such a healthy cash position, why has it never paid any divis? Management says this today -

The Board maintains its consistent view that the payment of a dividend is unlikely in the short to medium term.

Why is that? Possibly because the company seems to be run more for the benefit of management & staff! This bit below particularly grates, given it dismisses any idea of paying shareholders -

Employee Benefit Trust share purchase

Up to $10m of the Group's cash reserves will be used to fund the Employee Benefit Trust to purchase shares in the Group starting in H2 2022. These shares will be used to settle future vests of equity compensation

I don’t know about you, but I think that’s outrageous!

Cashflow statement - isn’t great. The problem here is that all the supposed cash generation in H1 was consumed within adverse working capital movements. Although it looks as if that might have been pandemic-related distortions from the last year now normalising?

But I’m raising an amber flag here, that investors need to keep an eye on future cash generation, to make sure it does actually start properly generating cash - which should be used to pay divis of course.

My opinion - I’m struggling to get excited about Accesso. It’s been around for many years, and the growth story looks a bit stale now. Is there much organic growth to be had in future, now the bounce back from the pandemic has already happened?

If I were a big shareholder in Accesso, I’d be pressing management to demonstrate that it can generate cash, and pay shareholders divis.

The big customer apparently deciding to change strategy in some way, is also a concern. What does that mean? Will other customers follow suit? Who knows.

On the plus side, the balance sheet looks very healthy, so there shouldn’t be any more worries about further fundraisings and dilution.

I see the share price has slipped 9% this morning in early trades, so it looks as if others are also a bit underwhelmed by the results/outlook.

It doesn’t help that Numis is the broker. From my point of view, they’re one of the worst brokers for small caps, because they try to stop private investors getting access to research, and company meetings. I recall once, getting into a meeting at their office was like breaking into Fort Knox! Hence without access to any broker notes, I can’t really value this share.

Graham’s Section:

Property Franchise (LON:TPFG)

Share price: 285p (pre-market)

Market cap: £91m

This is a collection of franchised estate agents, much like Belvoir (LON:BLV) is.

I used to own a few shares of this one - attracted by its high margins, cash flow etc. Franchising can be a very lucrative activity, and TPFG (in my opinion) is an example of a company that does it well.

Let’s check out these interim results, that are in line with expectations:

- Revenue +18% to £13.1m

- Royalties +5% to £7.5m

- Adj. operating margin 41% (last year: 47%)

- PBT +9% to £3.8m

All of this looks fine, except for the decline in operating margin. I think this mostly relates to the £25m acquisition of Hunters last year: Hunters is not fully franchised and therefore some of the revenues and costs from its branches end up on the TPFG income statement.

The increase in the share count arising from the deal also causes an 8% reduction in adjusted EPS.

Lettings vs. Sales

It’s great to see that other revenue streams have taken up the slack caused by a reduction in sales:

The increased lettings revenue and developing financial services revenue from our long-standing businesses offset the impact on them of the market-led reduction in sales transactions.

On a like-for-like basis (excluding the impact of acquisitions), TPFG’s H1 revenues are actually down by 9%, caused by a 21% drop in royalties from property sales.

Offsetting that, there was a 7% increase in royalties from lettings. And then if you add in the impact of the acquisitions, you get the overall 18% increase in group revenues.

From an investor perspective, it’s comforting to see that the company can switch from a sales focus to a lettings focus. That definitely helps to reduce the risk levels, to some extent.

The fact that revenues increased only thanks to acquisitions and declined on an organic basis is far from ideal, but I would venture that it’s understandable in the circumstances. After all, UK property transactions were 28% lower in H1 2022 than H1 2021; it’s impossible to avoid being impacted by this macro backdrop.

Hybrid agents - one of the reasons I’ve had an interest in TPFG is their work on providing “hybrid” services through Ewemove (and more recently through Hunters Personal).

The two brands have expanded to new territories in H1 2022, and TPFG calls it “a very strong performance against the macro environment”. Ewemove’s royalty income increased by 3% in H1.

TPFG also owns Mortgage Genie, but this is still at a small scale.

Outlook - is in line with expectations, and sounds confident (emphasis added below):

"We are extremely well-placed in the current environment and have a substantial growth opportunity to capitalise on. Post period end activity indicates the second half will perform at least as strongly as the first and ahead of H2 2021. As a result, the Board expects the full year results to be in-line with market expectations and this confidence is reflected in the interim dividend for 2022, which I am pleased to report is up 11% on 2021."

The acquisition of Hunters has gone well: “We are delighted with the synergies we have achieved with the Hunters acquisition and by the year end we expect to have achieved all those set out in our original plan.”

My view

In my opinion, TPFG is showing an impressive level of resilience and proving itself as a lower-risk investment in the residential property sector.

You might think that owning an estate agent is a lower-risk method of investing in residential property. But what about owning the estate agent brand and the services that estate agents use? I’m still a very happy shareholder in Rightmove (LON:RMV) and if I was going to add something else from the residential property sector, I’d almost certainly get back into TPFG. Others may find Belvoir (LON:BLV) appealing.

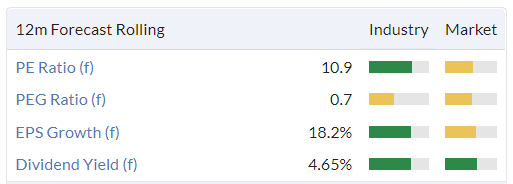

The company is carrying only very modest net debt (£2.6m) and looks cheap to me:

So what have I missed? There must be a bear case that I’ve overlooked?

The only negatives I see are:

- Uncertainty around the macro picture for UK property transactions, which might continue to hurt organic revenue performance.

- The company went from a net cash to a net debt profile, to make acquisitions, and needs a little more time to eliminate its net debt.

- The company might be tempted to get involved with more deals, creating more dilution and spreading management’s attention more thinly (although I don’t see anything wrong with the deals done last year).

Trustpilot (LON:TRST)

Share price: 71p (+15%)

Market cap: £319m

This was priced at 265p at its IPO back in March 2021.

My “IPO rule” is to wait until a recent IPO has fallen by a large amount (say 50%+) before allowing myself to get interested in it.

You could argue that if 2-3 years have gone by since the IPO, then the risk of a severely overpriced company having been brought to market has passed. But more often than not, in my experience, there will be problems and accidents within the first 2-3 years. So there is a good chance that a much better buying opportunity will present itself.

Even after this morning’s gains, Trustpilot is still down by more than 70% from the IPO level. So I’m now interested to see if there are any signs of value on offer here.

How it makes money - before getting into the results, I’d like to explain how Trustpilot generates revenues. This may not be entirely obvious because, as consumers, we get to use it for free.

The company sells “several paid subscription modules for businesses, providing increasing levels of functionality and offered on a software-as-a service basis. These tools enable Trustpilot's paying business customers to invite more reviews, manage those reviews, to derive high-value, actionable insights from them, and to showcase their TrustScores across their marketing channels.

Results - here are the highlights from H1 2022 interims:

- Revenue +25% at constant currency

- Actual revenue +18% to $73m (mismatch in these growth rates caused by the strong dollar).

- Annual recurring revenue +23% at constant currency to $149m.

- Loss of $9m (H1 last year: $17m).

- Net cash $73 million.

Trustpilot has a “commitment to breakeven adjusted EBITDA and underlying unlevered free cash flow” for 2024. In plain English, this means that it should be approximately cash-flow neutral, but the company will be able to apply very heavy adjustments to come up with this result.

The operational highlights are impressive: total cumulative reviews posted on Trustpilot have increased by 32%, and the number of domains reviewed is up by 29%.

Additionally, a “step up in deterrents, detection accuracy, and additional measures introduced to frustrate efforts to manipulate the platform, have led to a year-on-year reduction in the number of fake reviews flagged and removed”.

The whole point of Trustpilot is to help people understand which businesses and websites can be trusted, so these initiatives are crucial. Trustpilot itself needs to be beyond question in terms of the veracity of the content that it hosts. Every fake review that is prevented from reaching the site is a step in the right direction.

Outlook - the revenue outlook for FY 2022 is reiterated (consensus figures suggest that c. $157m can be achieved, per the StockReport).

The bit that has excited the share price (up 15% today) is likely to be this sentence I’ve put in bold:

While we have not seen any significant changes in overall customer demand in our end markets in H1 FY22, we continue to monitor the uncertain macroeconomic environment closely and we think it is prudent to take a more cautious approach to our assumptions for new business growth and retention near-term. However, we benefit from a flexible operating model and expect to see significantly more operating leverage in the second half of the year than previously anticipated.

Remember that the company has just reported a $9m loss on $73m of revenues. The point being made is that small gains in revenues (or small reductions in expenses) can lead to significant percentage changes in profit/loss.

This means that profit/loss might improve faster than expected, even if top-line revenues are only trading in line with expectations.

My view

I’m a big fan of this one. It hasn’t achieved much yet from a financial point of view, but it does offer some things that I look for in a business:

- Network effects: Trustpilot itself talks about the “powerful viral network effect” which it is creating. The more people who use Trustpilot, the more valuable it becomes as a measure of business trustworthiness. There is a “self-reinforcing cycle” as businesses want to show customers their Trustpilot score, and customers want to know if the business they are buying from has a good score.

- Recurring revenue: it’s a software-based subscription service for businesses, with a potentially open-ended lifespan. So long as Trustpilot is helpful, there is no reason for businesses to stop using it.

- Founder-led: the founder remains in charge as the CEO, implementing his long-term vision. The only disappointment is that his remaining stake isn’t bigger (currently 2% of the company).

- Unlimited growth potential: I don’t usually find it impressive when a company talks about its “addressable market”. But I do find it impressive when a potential monopoly in a particular niche still has a very long growth runway. Trustpilot says:

“We believe there has never been a greater need for a universal symbol of trust. At Trustpilot, we are creating a platform that we believe will eventually be used by billions of people and millions of companies.

So what are the downsides?

There are at least two major downsides from my point of view:

- It hasn’t yet made any money. Fortunately, the losses aren’t very large in comparison to its cash pile, and it talks today of positive impacts from operating leverage. Hopefully it will hit its goal of being around breakeven (on an adjusted basis) by 2024. But clearly there is a risk that it will not make any meaningful profits until 2025, 2026, or later, and it could even use up its cash pile over that time.

- It’s possible that some large tech giant - I presume it would be Google - would attempt to eat its lunch (disclosure: I own shares in Alphabet, the parent company of Google). Trustpilot has already generated great scale, but it probably needs to, because otherwise it could wake up some day and find that Alphabet has decided to create a rival product. Google already has an amazing business review service for local businesses on Maps, for example, and could attempt to roll this out to a broader set of businesses.

If you adjust out the cash balance, I think Trustpilot is trading at around 2x ARR (annualised recurring revenues).

I’ve recently been active on the US website Seeking Alpha, where I studied an unprofitable SaaS business trading at an ARR multiple of 20x, i.e. ten times the valuation given to Trustpilot.

If Trustpilot was on the NASDAQ instead of the LSE, I can imagine that it too would achieve an ARR multiple of 20x, and that would definitely price me out of investing in it.

But at 2x, I’m not priced out at all and indeed I find it intriguing.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.