Good morning! Paul & Graham are here with you today. Today's report is now finished.

Agenda -

Paul's Section:

Ted Baker (LON:TED) - an agreed cash takeover bid is announced at 110p, only an 18% premium. The 3 biggest shareholders (including the founder) have agreed it, so the company's trading and outlook can't be much good. This was not a convincing turnaround, so maybe this is a lucky escape for shareholders?

Sopheon (LON:SPE) (up 5% at c.550p - mkt cap £58m) [no section below] - announces a $11.2m, 5-year contract, with the US Navy’s submarines. It “will help to underpin financial goals for current and future years”, so forecasts not being raised at this stage. Sopheon always looks promising, but its profits have reduced every year since 2019, and only $0.8m PBT is forecast for FY 12/2022. So it’s certainly not a value share. Although longer-term, this could be an interesting company. Today’s contract win certainly sounds impressive as a reference for winning other business. If you like the company, then you can buy this share at half the price it was a year ago.

Smartspace Software (LON:SMRT) - H1 trading update today is in line with expectations. Still loss-making, but it seems to have enough cash (just), and cost control is mentioned. For such a tiny company, it seems to have lots of moving parts - different divisions/products, and operating in various countries. Despite some reservations, I think the share price shedding c.75% of last year's peak valuation, has brought it down to a more reasonable valuation which might be worth a little dabble at some point. Acceleration in growth is now key - if that happens, then the shares could do well. If it doesn't, then they might continue drifting down.

Tribal (LON:TRB) - interim results don't impress me at all. Too many adjustments that seem to recur each year, so genuine profit doesn't look much for the high market cap. Also I dislike the weak balance sheet, poor cash generation, and wobbly-sounding outlook statement. Risk:reward looks poor to me. Although sticky customers, with recurring revenues, could be attractive to a bidder - software companies often attract perplexingly high takeover bids. Or did anyway, in the latest tech boom.

Castings (LON:CGS) - a reassuring trading update today, shows that CGS is coping well with supply chain, higher costs, and passing on price rises to customers. It's a cracking value/income share, in my opinion.

Graham's Section:

Harland & Wolff group (LON:HARL) (£19m) - after delays with a gas storage project, Infrastrata (re-named Harland & Wolff Group Holdings plc) acquired a shipyard with a storied past from its administrators. Other yards have been acquired and Harland & Wolff is now a significant player in the bids for major Navy projects. Revenue aspirations are huge and make the HARL market cap look modest in comparison, but shareholder returns (for example in the form of dividends) are a long way off. I would treat these shares with the utmost caution.

Tremor International (LON:TRMR) (£545m) - H1 results and a Q2 update from this Israeli video ad technology company. The results are difficult to process but look OK at first glance, albeit with a weakening from Q1 to Q2. There’s a large acquisition coming down the tracks and my back-of-the-envelope calculations suggest that if the acquisition price is fair, then Tremor’s current market capitalisation is cheap. However, there are ongoing legal proceedings with an LG-controlled former strategic partner, which should be of interest to investors and may also provide an insight into the weakening performance. From my point of view, there are amber and red flags warning investors of danger here.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Ted Baker (LON:TED)

93p (pre market open)

Market cap £172m

Sky news reported this last night -

* REEBOK-OWNER ABG SEALS CUT-PRICE 200 MILLION STG TED BAKER TAKEOVER - SKY NEWS

It’s confirmed this morning with an announcement from Authentic Brands Group LLC, which says it has agreed with the Board of TED to take it over with a 110p cash bid. That’s only an 18.2% premium to last night’s price, and certainly not generous in terms of where the share price has traded in the last couple of years -

.

My initial reaction is why has the Board of TED agreed a takeover, at such a modest premium?

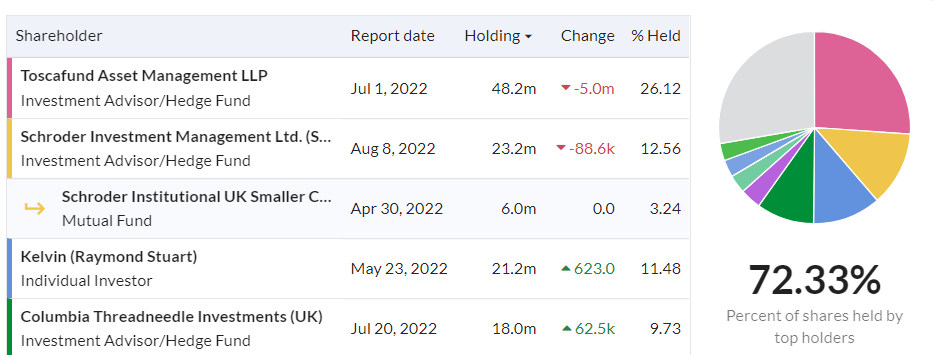

The shareholder register is concentrated, as you can see below, with the top 4 holders holding 60% - so there would be little point in agreeing a takeover bid unless these big shareholders had given the deal their blessing, I imagine.

ABG says it has agreement from holders of 50.7% of the company, and appendix 3 gives the details, which do indeed include agreement of the top 3 shareholders, Toscafund, founder Ray Kelvin, and Schroders. So this looks like a done deal. They clearly don’t have much confidence in the company’s turnaround, to be selling at this price.

.

.

ABG says it will not improve on the offer, it’s final (unless someone else makes a counter-bid).

My opinion - TED has been unconvincing as a turnaround so far. Reading between the lines of today’s announcement, it strikes me that maybe the major shareholders could be worried about the outlook, and are hence happy to cash in their investment, rather than have to pump in more cash to keep it going in a recession, e.g. -

the Acquisition provides an opportunity for Ted Baker Shareholders to crystallise, in cash, their investment in Ted Baker at a valuation that the Ted Baker Board considers fair in view of the significant recent deterioration of the macro-economic environment and outlook as well as the potential for an extended period of recession in the UK;

If the major shareholders, and the Board, think it’s a fair price, then it probably is. So I don’t think small shareholders have much to complain about here. The chances of a higher competing bid are probably slim, as the company has been for sale for a while. With the macro environment worsening, I’d be inclined to bank my profits in the market if the share price is close to the 110p bid, just in case the bid falls through for any reason. Or sometimes with takeover bids, I sell half in the market, and let the balance run, but it depends on price. Giving away say 1p to an arbitrageur is a small price to pay for the certainty of a deal, and having fresh funds to put into something else that’s cheaper.

.

Smartspace Software (LON:SMRT)

43p (down 8% at 08:22)

Market cap £12m

Very small, so I’ll keep this brief.

My notes are here from Feb 2022, where I remained unconvinced about this company. Results for FY 1/2022 were poor, with another heavy loss chalked up, and cash starting to look a little tight. The bull story is that it’s growing good quality, recurring revenues, and might become profitable in future. People returning to offices could also be a tailwind for performance, previously restricted by lockdowns & work from home.

Here’s the latest -

SmartSpace Software plc, (AIM:SMRT) the leading provider of 'Integrated Space Management Software' for smart buildings and commercial spaces, is pleased to announce a trading update for the six month period ending 31 July 2022.

H1 revenues £3.6m (up 46%)

Two thirds of revenues are recurring in nature.

Net cash £2.0m, and the rate of decline has slowed (only down £0.4m in the last 6 months), which I find reassuring, as cash was worrying me a bit - because this is clearly not a good time to be asking investors for more money.

There’s plenty more detail in today’s update. It seems to have 3 divisions or products - SwipedOn, Space Connect, and Anders & Kern.

SwipedOn looks to be growing well, and makes up 56% of group revenues.

Space Connect - this seems to be struggling to grow, and is tiny at £0.3m revenues. Worth pursuing? Depends on what the costs are.

Anders & Kern has recovered to pre-pandemic revenue, and H2 outlook is positive.

Outlook - sounds OK, in line with expectations -

We finished the period with strong revenue growth, and £2.3m of cash, the same level disclosed at the end of April 2022. This was helped by the increase in cash inflows from Naso, as sales grew and continued cash generation within SwipedOn. We remain focused on continuing this momentum over the next period both in terms of sales growth and cost control as we implement our plans to transition into a profitable and cash generative business.

The Board expects to deliver revenue and profitability results in-line with current market expectations for the full year, whilst ARR is expected to be lower than market expectations reflecting the updated ARR calculation methodology and performance to date.

There is a footnote explaining that ARR (annual recurring revenue, a key measure for software companies) is being recalculated on what looks a more prudent basis.

My opinion - there are some positive things going on at SMRT, but it’s a tiny business, in what must be a crowded sector. Also, it seems to have a mix of different products/services, and operates in several countries. Surely it would be better to keep the overheads more lean, and focus on deepening sales in one niche? It seems a bit of a scattergun approach at the moment.

Current forecasts show it having just about enough cash, but forecast cash burn seems a lot lower than losses on the P&L, which implies maybe creditors are being stretched to conserve cash? Hence I’d like to see the interim accounts to get the full picture.

The market cap of £12m looks a lot more realistic to me, better reflecting risk:reward than the peak last year of about £50m.

It all now hinges on the potential to accelerate growth, as offices return to more normal operating conditions, as staff are dragged back into offices, from “pretending to work from home” (as Elon Musk put it!)

Overall, I think SMRT shares could be worth a little dabble at £12m market cap, or at least adding to the watch list for when more bullish market conditions return. If growth does accelerate, and breakeven comes into view, then I could see this share maybe doubling or tripling? In the meantime though, it could continue drifting down, so maybe no immediate rush to get involved? Timing the buys & sells is up to you though, I just look at the company fundamentals here.

It’s not a blue sky company, but more a loss-making company that needs to grow quite fast to achieve breakeven & then profits. Bear in mind that the payroll will be costing a good bit more each year, as software companies main cost is expensive & scarce skilled staff.

Stockopedia tends to be brutal with loss-making companies (a useful wake-up call, that most shares like this do badly, other than in the euphoric phase of bull markets), as you can see from the poor StockRank, in the red -

.

Tribal (LON:TRB)

81.5p (down 6%, at 10:29)

Market cap £172m

Tribal (AIM: TRB), a leading provider of software and services to the international education market, is pleased to announce its interim results for the six months ended 30 June 2022.

I covered TRB here in June 2022, when it issued a mild profit warning for H1, due to increased costs on a major customer project implementation (in Singapore). Although it did confirm full year expectations.

A few numbers -

H1 revenue up 7.9% to £42.4m

“Adjusted Operating Profit (EBITDA)” is down 23% to £7.1m

Adjusted PBT is £5.7m, down 28% vs H1 LY.

Statutory PBT is only £3.1m, down 47% on H1 LY.

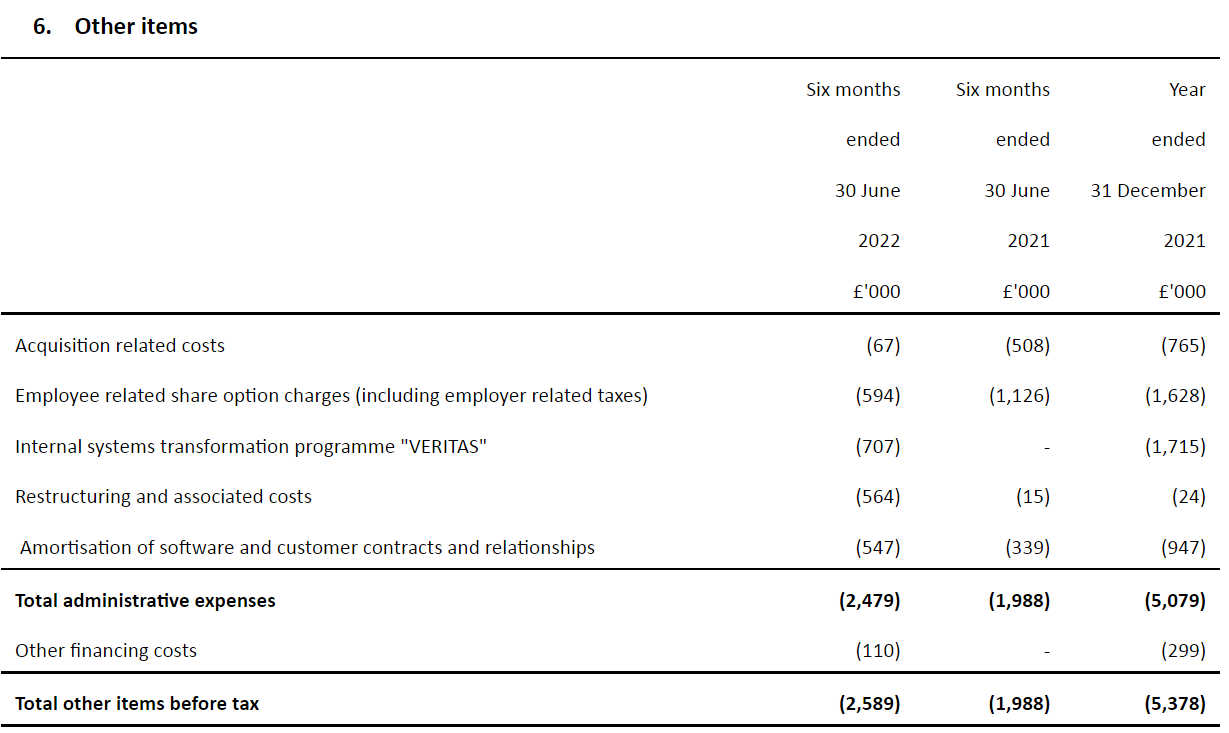

Adjustments flatter profit by £2.6m - are the adjustments reasonable, and one-offs? Not really, no. Note 6 details the adjustments, which seem to have a habit of being repeated -

.

Development spend is being capitalised at a high level, £5.6m in H1 (£10.2m in FY 12/2021), hence EBITDA is meaningless here.

Cash generation is poor - particularly in H1 this year, but it was also poor last full year - this is why the divis are so small, because it’s not really a cash generative business, once you take into account development spending.

Balance sheet - is horrible. NAV of £49.6m turns negative £(20.2)m NTAV, once intangible assets have been written off. Does this matter? Maybe not, because software companies often get paid up-front, and have little fixed assets, so they don’t need strong balance sheets. Bank debt is not excessive at TRB, so I’m not ringing alarm bells here, just pointing out that it doesn’t have any asset-backing to fall back on in hard times, which you may or may not be comfortable with, that’s up to you. Recurring revenues, and sticky long-term contracts probably protect the downside pretty well.

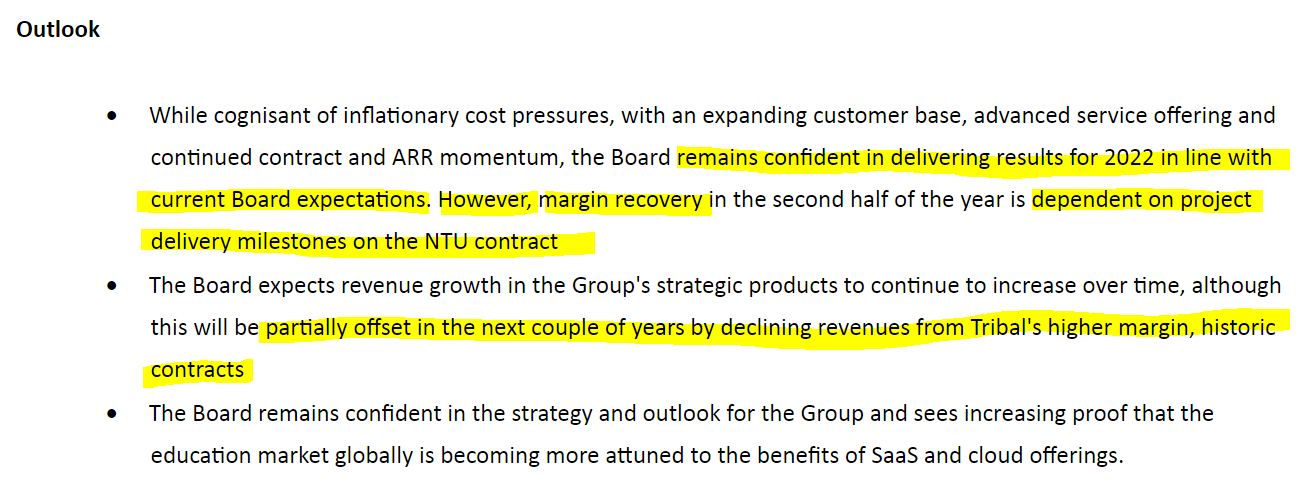

Outlook - this sounds quite wobbly to me, and I’d probably be hitting the sell button if I held this share, as it sounds to me as if there’s ample scope for another profit warning later this year. TRB has been prone to things going wrong in the past too.

.

.

My opinion - to summarise then, it’s got a weak balance sheet, poor cash generation, capitalises a ton of the payroll onto the balance sheet, pays a small divi, and has a wobbly-sounding outlook section, so the risk of another profit warning looks high.

Also I think the adjusted profit numbers look inflated.

It’s not even cheap either. The forward PER is about 17 times, which doesn’t look at all attractive to me. So a thumbs down I’m afraid.

For balance, bulls might point to good recurring revenues, and growth potential overseas.

.

Castings (LON:CGS)

309p (flat at 12:38)

Market cap £134m

AGM Statement (trading update)

Graham did a nice review here of the FY 3/2022 results, which I’ve just read to get up to speed.

Today’s update looks good to me, and covers the main topics of concern at present (cost inflation, supply chains, and pricing power). Here it is in full -

We previously reported in June that demand from our commercial vehicle customers (70% of group revenue) was increasing; it is pleasing to note that these higher levels have been maintained with relatively little disruption resulting from supply chain issues.

The forward demand schedules continue to reflect the higher build rates that the heavy truck OEMs require to satisfy their orderbooks. The group will see the benefit of the greater content won on the new customer platforms as these are now in production.

Input prices have continued to rise in the current financial year and are being passed onto our customers. The most significant increase will be on 1 October 2022 following the end of our fixed price electricity contract. The higher unit cost for power will be surcharged to our customers immediately and will therefore increase revenue in the second half of the year. Whilst this should not adversely affect group profit as it is a pass-through of a direct cost increase, there will be a dilutionary impact on the margin percentage.

We continue to invest in automation technologies to improve our productivity and profitability as evidenced by the commissioning of a partially automated pouring process on one of our largest production lines.

Broker update - many thanks to Zeus for updating us today.

Forecast EPS is 28.2p for this year, FY 3/2023.

The share price of 309p is a PER of 11.0x. That looks very reasonable to me. Maybe the market is worried about the long-term, with turbochargers (a key product CGS makes for trucks) likely to become redundant if electrification takes hold?

Also bear in mind CGS has a fabulous balance sheet, with mountains of surplus capital in there, net cash, and no debt.

This enables it to pay remarkably consistent divis, even during the pandemic, and it sometimes pays special divis too.

My opinion - for cautious investors, and maybe income seekers, this share is top notch I think. Not only can you lock in a lovely flow of future divis, but it’s also bulletproof financially. It’s clear from today’s update that inflation, and supply chain are being handled well, and price rises passed on to customers.

Despite all these positives, you can buy today at close to a 5-year low. That doesn’t make sense to me, so I see this as a buying opportunity.

.

Graham’s Section:

Harland & Wolff group (LON:HARL)

Share price: 11.6p (pre-market)

Market cap: £19m

On a day with few announcements, I get to look at companies that I have never or only very rarely studied before. Harland & Wolff is one of these.

Previously known as Infrastrata, this company was focused on the proposed gas storage facility at Islandmagee in County Antrim. This project promises to hold up to 25% of the UK’s natural gas storage capacity, but is still held up in legal limbo. A hearing is scheduled to take place some time in “winter 2022”.

While the gas storage project slowly moves toward construction, Infrastrata has used its public listing to raise money and purchase Harland & Wolff, and then other shipyards.

The H&W purchase was announced in October 2019, as a “strategic acquisition” that would “bring in-house a large part of the fabrication requirements for the Company's Islandmagee Gas Storage Project and proposed FSRU project” (I think the FSRU project has since been abandoned).

H&W was up for sale after collapsing into administration in August 2019.

I wrote yesterday in very positive terms about the deals which are possible when a company falls into administration. But this is a complicated and special case: H&W was already up for sale for a year prior to administration, and there were major legacy issues to do with pensions and worker contracts (the union wanted the company to be nationalised).

It looks to me like the Pension Protection Fund is now paying H&W’s legacy pensions, and the new pensions are all “defined contribution” in nature.

All of which helps to bring us up to the present, where Infrastrata has been renamed as Harland & Wolff, and has acquired multiple shipyards across England and Scotland.

You might not be surprised to learn that investors have been diluted to smithereens during this process. If you invested in this company several years ago, your stake in the company has been reduced to almost nothing:

Let’s take a look at today’s trading update (emphasis added throughout):

Harland & Wolff Group Holdings plc (AIM: HARL), the UK-quoted company focused on strategic infrastructure projects and physical asset lifecycle management, is pleased to provide a business and trading update for the year ended 31 December 2022 and an outline of management's aspirations for financial year 2023 ("FY23") and financial year 2024 ("FY24"). Given the many variables which need to be considered, these aspirations should not be construed as forecasts but as management's framework for the direction of the business.

I wouldn’t go too hard on a business admitting that it’s unable to make forecasts. After all: it’s much better to know that predicting the future is impossible, than to rely on bad forecasts.

FY22: three large contracts have been won, including a huge £55m contract relating to an ex-Navy mine-hunting vessel.

Combine that with a steady stream of small, regular work and “management maintains that it remains comfortable with market guidance of revenues between £65 million - £75 million for FY22.”

FY23/FY24: there’s a £40m backlog relating to FY23, thanks to recent contract wins.

In addition, there are “opportunities amounting to approximately £1.2 billion, across the Company's five key markets; cruise & ferry, commercial fabrication, energy, defence and renewables.”

I wouldn’t pay too much attention to the £1.2 billion figure; this is just the size of the addressable market, in the view of management. The challenge is to win a small fraction of this business as profitably as possible, not to win as much of it as it can, at all costs.

There is, however, an interesting comment in relation to the massive Fleet Solid Support shipbuilding programme:

The UK continues to suffer from insufficient fabrication capacity to take on all the fabrication work that is due to commence from 2023/24. Harland & Wolff retains one of the largest fabrication footprints in the country and has enormous flexibility and optionality across the yards to offer optimum fabrication solutions, particularly for its defence and renewables clients. In summary, the Board believes that the Company is well placed to play an important part in the FSS Programme.

The revenue “aspiration” for FY23 is £100m - £115m, rising to £200m - £230m for FY24, and the target gross margin is 24%-27%. Take these numbers with a pinch of salt.

As for profitability?

At turnover levels of £200 million and above, the Company would expect to be in a position to generate sufficient cashflow to initiate returns to shareholders… The Company believes that annualised cashflow break-even is achievable on revenues of between £80 million - £100 million depending on the mix of contract wins.

My view

I’ve enjoyed reading about the evolution of this company from a gas storage proposal to a collection of shipyards hoping to take part in the construction of major Navy vessels.

In March 2022, the company entered into an agreement for a large (up to $70m) debt facility, with the funds being used “primarily” for offshore wind development.

As I often do, I’ve studied the terms of this deal - because if I know how risky the debt of a company is, that’s a big clue for figuring out how risky the equity is!

The debt has the following features:

- Interest of 9% plus the overnight financing rate.

- Expires September 2023; H&W may extend it but must pay even higher interest to do so.

- The lender also gets 10 million warrants over HARL shares.

- The deal is “securitised against substantially all the assets of the Company, including land, property, plant and machinery and receivables.”

What does this tell me? In a nutshell, it tells me that the equity is extremely high risk. I would have guessed that anyway, but this gives it to me in black and white.

Putting it another way, I would be much happier to be this lender than to be an equity holder. The lender gets equity-like investment returns of over 9%, also gets free shares in the company, and will end up owning the company outright, if things don’t work out.

In summary: I wouldn’t be fooled by H&W’s low market cap, relative to the revenues it might generate. The company itself says that there won’t be shareholder returns until revenues are over £200m, and the deal with lenders demonstrates what professionals think of the risk profile. This is a share of the most speculative nature.

Tremor International (LON:TRMR)

Share price: 368p (-16%)

Market cap: £545m ($654m)

This one rebranded from Taptica (TAP) in back 2019. The explanation was as follows:

Tremor International Ltd (AIM: TRMR), a global leader in advertising technologies, today announced that it has rebranded… positioning itself as one of the leading independent video advertising companies in the U.S… ‘The new branding and structure better reflect our stronghold in the video advertising space,’ said Ofer Druker, CEO of Tremor International. ‘It also reinforces our ability to address the significant opportunity in Advanced TV, bringing increased scale, audience targeting and ad formats to clients.’

I have to be honest and admit that I never felt like I properly understood what Taptica did, and how it made money.

With the change to Tremor, things haven’t got much easier.

For example, Tremor uses something called “Contribution ex-TAC” as a major KPI. Many other companies in the online advertising sector use this too, but it takes some getting used to. The idea is to show gross profits excluding the impact of traffic acquisition costs. It’s an indicator of the size of the company, but is a very long distance from the bottom line net profits.

Let’s see what’s happening with these H1 results:

- Revenues +3% to $157m

- Contribution ex-TAC +4% to $142m

- Gross profit +10% to $120m

- Operating profit minus 18% to $30m

Q2 numbers are shown and they are worse than Q1. The reason given for the weak performance of Contribution ex-TAC is “challenging macroeconomic conditions”.

Also, the H1 tax charge comes in very large at $10m and I can’t see any explanation for why it is so much bigger than last year.

Acquisition

There is a $239m acquisition coming: Tremor is buying another Isreali company Amobee. You can read about the transaction in the Israeli press.

Tremor should easily afford this: it claims to have a $360m cash position as of the end of June, and also expects to have a $150m debt facility (not sure why it needs to have any debt facility at all, given the cash balance?).

Amobee is said to have generated Contribution ex-TAC of $150m over the past 12 months. So it’s only being bought for 1.6x its Contribution ex-TAC (without making any adjustment for cash or debts that Amobee might have).

If we valued Tremor on the same basis (i.e. 1.6x its trailing Contribution ex-TAC), we’d get a value of $454m (using twice the H1 figure, not allowing for any seasonality).

Add the $360m cash balance on, and we get a possible market cap in the region of $800m.

The actual market cap after today’s share price fall is $654m, which also does not provide for any synergies from the combination of the two companies.

This means that if the Amobee valuation makes sense, then the Tremor valuation looks cheap (assuming that the two companies are of similar quality - but some people think that Tremor is a higher-quality business, which would make Tremor even more undervalued).

Legal issues?

There’s a comment below by Malcolmbell, talking about a dispute between Tremor and Alphonso, which is controlled by the TV manufacturer LG. Malcolm suggests that this dispute is at the heart of Tremor’s weak recent performance.

Indeed, there’s a lawsuit classified as “pending” in the New York County Courts with Tremor as plaintiff and Alphonso as defendant. The dispute is not mentioned in today’s RNS, but it was described in the results filed by Tremor in February 2022.

Alphonso also counter-sued Tremor:

On May 24, 2021, Alphonso filed a complaint against the Company in the Supreme Court of the State of New York, County of New York, asserting claims for breach of contract, unfair competition, and tortious interference with business relations.

My view

Tremor (or Taptica) is a classic example of an Israeli stock: claiming to be cash-rich and to be doing very innovative things online, but perceived as having some issues (perhaps legal or ethical in nature), and isn’t fully trusted by investors in other parts of the world. Think of the histories of XLMedia (LON:XLM) and Plus500 (LON:PLUS) .

If Tremor was trusted, it wouldn’t have value statistics like this:

Maybe I just need to spend more time studying it, but Tremor International (LON:TRMR) hasn’t yet convinced me that it makes its money in a sustainable and predictable way. I like it when companies speak plainly, but I don’t believe that Tremor does this. For this reason, it’s not something I could consider investing in at this point.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.