Good morning from Paul & Graham! Today's report is now finished.

Agenda -

Paul's Section:

National World (LON:NWOR) (£53m) - I run through the bull and bear points for this newpaper/digital publisher. It looks cheap, and has almost half its market cap sitting in cash on the balance sheet, earmarked for acquisitions. Despite a strong H1 profit performance, macro storm clouds are gathering, with a deteriorating trend in revenues so far this year. Profits need further cost-cutting to be sustained, which can't carry on forever. It doesn't have any of the historic baggage of RCH (no pension deficit, or debt), but I'm lukewarm on the longer term prospects for NWOR.

Revolution Bars (LON:RBG) (£34m) (I hold) - a surprisingly upbeat year end (FY 6/2022) update. It's trading in line with expectations. House broker forecasts 1.6p EPS (£4.2m adj PBT). Extensive site refurbs (19 done, 18 more in new year). Successful trials of 2 new formats. Has solid balance sheet with net cash. Market still not convinced, due to historic, extensive problems, but the business looks in good shape now, and cheap. Really good mgt I think. Shrugging off macro conditions.

Gyg (LON:GYG) (£10m) - 20.5p (down 35%) [No section below] - H1 trading sounds fine, in line with mgt forecasts. H2 outlook is good, with strong order book & pipeline. In line with FY 12/2022 mkt exps of E5.0m EBITDA. Cashflow problems assisted by loan from major shareholder Harwood Capital.

Separate bombshell announcement that it plans to de-list (hence shares down 35%) - this is a big, and growing danger for holders of micro caps - beware! Particularly where there are a small number of controlling (over 50%) shareholders, as is the case here. Much though I admire Harwood Capital’s stock-picking skills generally, they also have form for persuading investee companies to de-list, thereby squeezing out private shareholders (at a bad time/price in this case). Although to be fair, GYG never should have floated, it’s unsuitable for public markets, and has had a disappointing & erratic performance. So there's little point in retaining the listing. It snatches the potential upside away from PIs though, which is a pity given that the trading update is good.

Revolution Beauty (LON:REVB) (£84m) - profit warning - shares have collapsed since the CFO left in May. Auditors need another month to check the FY 2/2022 figures. de-stocking by customers, and inflation/supply chain have hit the new financial year, with H1 (Mar-Aug 2022) now expected at breakeven, but still a good full year expected due to the H2 seasonal weighting of Xmas. My main concern is what looks like massive over-stocking, by my calculations nearly a year's worth of inventories are on hand, which is a potentially major problem. Hence I suspect it might need to warn on profits again, so am staying safely on the sidelines. EDIT: Zeus slashes forecasts for FY 2/2023 by two thirds, to just 1.5p adj EPS.

Graham's Section:

Devro (LON:DVO) (£312m) - Solid interim results from this international maker of sausage casings. Net debt falls despite an increased capex bill, as the company invests for growth. There is a small increase in the long-running dividend. Devro’s profitability is suffering slightly from the lag between cost increases and the passing on of those increases to its customers. Since this is the food industry, I share Devro’s confidence that it will be able to pass on the inflation to its customers. This stock is modestly valued and I’m not sure that this fairly reflects the quality and track record of the business.

A G Barr (LON:BAG) (£608m) - This soft drinks company provides a trading update that’s in line with expectations. Revenue growth is very impressive (19% underlying) but volume growth isn’t given yet, and may only be around 4%. At least the company is able to pass on price increases to customers without much difficulty! The balance sheet was very cash-rich the last time it was published, and BAG shares accordingly trade at a premium earnings multiple that they might not otherwise enjoy.

Filtronic (LON:FTC) (£32m) (+2%) [no section below] - this company has been listed for a long time, and the track record is patchy at best. But today’s results show profits of £1.5m on revenues of £17.1m (+10% versus the previous year), despite the company being impacted by the semiconductor shortage. Cash generation was good and the company finished the year with net cash of £3.1m (excluding leases).

Filtronic provides communication components and subsystems, and its success depends on contract wins in the aerospace, security and telecoms industries. Today’s outlook statement promises continued revenue growth and points to a healthy order book, though the CEO acknowledges “the somewhat unpredictable nature of the economic and the current geopolitical situation”.

These are the best results I’ve seen from Filtronic in several years, and particularly impressive given the challenging supply chain backdrop. I can see why investors might feel that the shares are worth a flutter based on continued positive momentum in 5G investments, satellites and aerospace/defence spending. However, it is worth noting that analysts at Edison are modelling a fall in Filtronic’s adjusted PBT to £0.9m in the current financial year, due to a lower-margin product mix, before hopefully bouncing back in FY 2024.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

National World (LON:NWOR)

20.6p (up 8% at 11:00)

Market cap £53m

For the 6 months ended 2 July 2022, so half way through FY 12/2022.

This is a newspaper group, the reincarnation of the old Johnston Press, but without the legacy problems of debt, and pension schemes, both of which have gone. So think of it as a smaller, less complicated Reach (LON:RCH) .

Key H1 numbers -

Revenues £43.5m, iup 3% on H1 LY.

Slowing trend though - revs +5% in Q1, +1% in Q2, and down 6% in July.

Adj PBT £5.6m in H1, up from £3.5m H1 LY - a very good result - driven by slightly higher revenues, and tight cost control.

Digital revenues are useful, at £8.2m (up 41%).

Adjustments are mainly restructuring costs of £1.3m (£3.3m in H1 LY), which I would argue are not one-offs, but an essential way to keep a newspaper business profitable, as it slowly declines. Therefore I would lean towards valuing the business on statutory profit of £3.9m in H1 (£0.9m loss in H1 LY). See note 16 for the adjustments.

Note that, even though profits rose, EPS actually fell (H1: 1.6p adjusted, or 1.1p statutory) - due to an increased number of shares in issue.

Further cost savings of £3.0m annualised will be done by end 2022, but this restructuring is to cost £2.5m - mainly severance pay. See what I mean about restructuring being ongoing, not exceptional?

This is reinforced by staff numbers - down from 1,262 a year ago, to 1,179 now. So maybe NWOR is likely to keep incurring several £m’s each year in severance costs, as it gradually downsizes? How long can it keep cutting, is the other big question for this sector - also relevant for distributor Smiths News (LON:SNWS) which has almost run out of depots that it can close without impairing its ability to operate.

All of which means that profits in this sector are not sustainable, long-term. Hence the shares should be seen as cigar butt shares, and be on very low PERs, and have very high dividend yields because they’re not going to last.

Actively pursuing several acquisition targets - this is the most important thing, with cash being nearly half the market cap. So the outlook for this share really hinges on how wisely that money is spent. Potential upside here if good acquisitions are made at keen prices, which should be possible given how beaten up the sector is.

Minimal capex is expected - of £1.5m p.a. in future. There seems to be very little fixed assets, so NWOR must outsource printing of the newspapers externally.

Going concern note - is fine, and irrelevant due to the £25.7m cash pile.

Balance sheet - very good, with scope to fund acquisitions, a key bull case for this share.

NTAV is £21.7m, including a £25.7m cash pile. Although I would deduct these items from cash to arrive at net cash: last instalment of £2.5m deferred consideration due, £1.0m borrowings, and maybe the £1.5m provisions. So adjusted net cash is £22.2m, or £20.7m, depending on whether you want to adjust include provisions as a cash deduction.

So I would say NWO has a war chest of maybe £15-20m that it could safely use for acquisitions. I don’t know what potential acquisitions are out there, but in the past it has made sense for smaller publishers to be gobbled up into a group, then a load of duplicated costs removed. Or maybe NWOR will try to do something in the digital space, although they won’t get much for £15-20m.

Cashflow statement - is super simple. NWOR generates healthy, genuine cashflow, which is accumulating in a growing cash pile. The only significant cash outgoing was the penultimate £2.5m deferred consideration outflow. There were no divis paid, but the commentary today says a progressive dividend policy will start with 2022 results, so in spring 2023.

NWOR will have plenty of scope to pay out big divis, or retain cash for more acquisitions. That’ll be a tug of war between management and shareholders, I expect.

Outlook - the “at this stage” bit sounds hesitant - are they signalling that things could get worse? Sounds like it to me -

The trading environment remains difficult with the prospect of a further slowdown in the UK economy. Despite these macro-economic challenges, increased investment in the development of our portfolio of digital sites and commercial opportunities and the tight management of the cost base will support future profits and cash flow.

At this stage, the Board expects the business will perform in line with its expectations.

As the Group successfully implements its strategy, the Board anticipates being able to initiate dividends at the time of announcing the 2022 full year results with a progressive dividend policy.

Valuation - Dowgate has helpfully posted an update note on Research Tree, many thanks. This points out that H1 is well ahead of what was expected, at £5.6m H1 PBT (it expected £4.1m). So the full year forecast of £8.1m adj PBT looks soft, given that £5.6m is already in the bag from H1. Although a weakening of demand, and hence revenues, due to macro factors and structural industry decline, suggests to me that having soft forecasts is sensible to avoid a profit warning later in 2022.

My opinion - I can see why some readers like NWOR shares. Having almost half the market cap sitting in cash, which looks genuinely surplus to requirements, hence usable for acquisitions, does appeal.

Dividends are due to commence in 2023.

On the downside, newspapers are slowly dying, we’ve known that for years. Every now and then the stock market gets excited about digital growth, so this share (like RCH) is probably best seen as a cash cow for a few more years, in the hope that the cashflows are used to build something longer term in the digital space.

At least NWOR shareholders don’t have to worry about the huge and uncertain pension liabilities at RCH - which could melt away, or could remain a millstone, we don’t really know. At NWOR it’s much cleaner, with no pension issues that I’m aware of.

NWOR is set to make c.2.3p EPS this year, and next (if they’re lucky), but driven by constant cost-cutting, to offset declining revenues expected. That’s not a very good investment proposition, in my view, because they can't keep cutting forever.

The cash pile could be used for acquisitions, which could then boost earnings, and bring down the PER from 9 currently, to what maybe 5 or 6 possibly? But why would you want to pay any more for a declining business, that’s bolting on other stuff to prop up a fundamentally declining business?

For me, I’ll keep a watching brief, and it would really need to be something significant happening on the digital side that would make me want to take an interest in this share. It’s cheap for a very good reason, as is RCH and SNWS.

Share price since listing in Sept 2019 -

.

.

Revolution Bars (LON:RBG) (I hold)

14.6p (pre market open)

Market cap £34m

Here are my notes on key points -

Traded in line with expectations (upgraded on 14 June 2022). No footnote. I've already complained to the house broker!

LFL sales flat (vs LY, or pre-pandemic? Not clear).

Mitigating inflation (e.g. energy largely fixed until spring 2023).

Focus on staff retention, so spending less on recruitment.

Xmas bookings building much earlier than last year - confident in outlook. Corporate parties market coming back.

19 refurbs done (28% of estate) - delivering target 2-year payback.

2 new sites trading well.

Both trials of new formats (Playhouse, and Founders & Co) “initially been well received”, potential for expansion.

FY 6/2023: 18 more refurbs planned, and 6 new openings. Exciting pipeline of new sites.

Net cash £2.6m at 6/2022.

Significant & sufficient headroom (via bank facility).

Results out on 18 Oct 2022.

My view (I hold) - the market still hasn’t forgiven RBG for all the problems in the past, and heavy dilution (share count: 50m to 230m after 2 placings) means position sizes need to be much larger to recoup previous losses (if that happens at all). Refurbing sites is doing the trick - robust performance when others are struggling. Mgt are superb, hands-on operators, in my view. Finncap forecast is £4.2m adj PBT, 1.6p EPS. Target young customers not particularly impacted by cost of living squeeze, and want to "partay" as my niece says!

Shares look cheap to me, but the whole sector has been hit hard, understandable in current conditions. Time for me to do another mystery shop, I think, maybe this Friday afternoon?!

Revolution Beauty (LON:REVB)

27p (down 56% at 09:55)

Market cap £84m

Good grief, this has just come up on my top movers list, down 56% this morning, on high volume (7.8m shares traded so far today, and there will for sure be big, delayed prints later from institutional sellers). In total, there are nearly 310m shares in issue.

It only floated in July 2021, as one of many eCommerce wonder stocks, that nearly all seem to have since crashed. It’s amazing to see a whole sector just collapse from being highly rated for many years as growth companies, to being increasingly bombed out & eschewed. As a value/GARP investor, I don’t care about stock market sentiment, so am looking for any potential bargains this sector drop might throw our way.

I’ve not covered REVB here before, so will have to go through the background first, before I get stuck into today’s update.

When things have fallen this much, one of the key things I always focus on is balance sheet strength, and whether there’s risk of equity dilution, or even insolvency.

(and change to final results announcement date)

Revolution Beauty Group Plc (AIM: REVB) the multi-channel mass beauty innovator, announces a change to its full year results announcement date and a trading update.

Accounts are very late and not coming out until end Aug 2022 - 6 months after the year end, which is ridiculous, so there must be something wrong (even if it’s just being disorganised), despite the denial below.

Final results for the year ended 28 February 2022

The Company will now report its final results for the year ended 28 February 2022 ("FY22") on 30 August 2022. This is due to additional time required to complete the Company's audit. Management is not aware of any material issues that have been raised by the auditors during the audit process to date. The annual report will be sent to shareholders and made available on our website on the 31 August 2022.

Although REVB did change its CFO in May 2022, which would have been disruptive I imagine. It’s unusual to see a CFO changed a couple of months after year end, as usually they would want to get the audited accounts done, then leave.

No wonder the market took fright at this, with the steep decline in share price getting underway in May 2022 (it’s now dropped by ¾ in the 3 months since then).

The trading update on 6 May 2022 said FY 2/2022 performance was in line with market exps, guiding revenues of £194m (up 42%) and adj EBITDA up 73% to c.£22m. Note there’s a heavy H2-weighting, as H1 adj EBITDA was £5.1m, so guidance in May ‘22 implies H2 adj EBITDA of £16.9m, a 23:77 ratio for H1:H2 adj EBITDA in FY 2/2022.

The trading update’s tone just 3 months ago sounded upbeat, including positive outlook comments.

Note that 71% of sales came via retail stores, and 29% online, which surprises me, as I thought REVB was supposed to be an online disruptor in the beauty market.

Further back, a small acquisition was made in Feb 2022.

Broker Liberum joined Zeus to become joint brokers on 30 June 2022 - prelude to a fundraising I speculate?

Getting back to today’s trading update -

REVB products are now in c.15,000 stores worldwide.

Q1 2023 (Mar, Apr, May 2022) - problems have emerged, which all seem rather obvious to me, why has this surprised the company? -

… we have seen short-term challenges as a result of post Covid retailer updates during Q1 FY23 (notably in the USA), cost inflation, supply chain issues and the war in Ukraine.

Profit warning for H1 of FY 2/2023 -

As such, we now expect the first half of the year to deliver low single digit revenue growth versus H1 FY22, resulting in a small adjusted EBITDA loss for the six month period ending 31 August 2022. For the full year to 28 February 2023, we now expect between £215m - £225m net sales and adj. EBITDA of between £18m - £20m.

Clearly that’s a bad performance currently, a small H1 loss, down from £5.1m adj EBITDA in H1 last year.

Although the full year guidance still looks decently profitable at £18-20m, although how real are adj EBITDA profits? I’ll have to look into that.

More detail, which is interesting -

US retailers over-stocked, so have reduced purchasing. Should normalise in H2. This is a recurring theme we're hearing from other companies, which could trigger plenty more profit warnings, I reckon, as supply chains begin to ease, and consumers buy less stuff but at higher prices. Hence retailers don’t need to buy as much stuff as they de-stock.

Digital customers also de-stocking as sales slow.

Russia/Ukraine - not just an excuse, REVB was trading in those countries, which ceased. £9m impact on annual revenue.

Cost inflation - especially in logistics & freight. Higher staff costs. Surely this should have been budgeted for, suggesting weak financial controls (perhaps explaining why the CFO was replaced?)

Outlook - I’m not sure I have much confidence in their confidence -

As we approach the seasonally stronger second half, and actively manage costs across the business, we will benefit from leveraging our overhead base in line with previous years.

Confidence in the second half is underpinned by significantly increased retailer distribution in H2 FY23 versus H2 FY22.

"While the Group has been impacted by near-term economic and political headwinds, we remain confident in the strength of our long-term strategy and the significant growth opportunities open to us. In particular, we remain focused on innovation and the development of new categories while continuing to further build brand awareness, especially in the US.

"This has been a period in which we have strengthened our market position and built sales across geographies, despite the unprecedented macro-economic backdrop. We have continued to deliver against our omni-channel strategy and are now in 15,000 stores worldwide. We secured a second UK retail partner with Boots and launched into 2,800 Walgreen stores. This has been achieved by providing our customers with the highest quality beauty products at the best possible price."

Debt - oh dear, it has net debt, although it doesn’t look to be at problem level -

As at 31 July 2022, the Group had net debt of £21.2m driven by an increase in stock, working capital and capex requirements. The Group has a £40m revolving credit facility which the directors believe provides sufficient liquidity for the future.

Remember that higher inflation impacts cashflow at many companies - because rising prices means that 2 debits go up in value on the balance sheet (inventories and receivables), but only one credit goes up (payables). Hence the impact of higher inflation means more cash is sucked into working capital.

The last published accounts showed net cash of £17.6m at 31 Aug 2021, so to have moved into a net debt position of £21.2m in 11 months is unsettling, even if it was planned (a new £40m facility was put in place in Oct 2021.

Balance sheet - the last published one was as at 31 Aug 2021.

This shows NAV of £86.5m, including £22.6m intangible assets, so NTAV was £63.9m - adequate, I would say.

It also includes the entries for the only significant acquisition made (from a related party, hmmm) called Medichem, with £16m of the consideration deferred into 4 annual payments of £4m each, yet to be made.

Hence the structure of the balance sheet should not have significantly changed since 31 August 2022.

Inventories look very high at £89.9m (at cost price remember) at 31 Aug 2021, and it sounds like that figure will have gone up even more, given that today’s update refers to “an increase in stock”.

This reminds me of Seraphine (LON:BUMP) (I hold) yesterday, in that REVB looks to be massively over-stocked. Deducing that it might currently have about £100m in inventories at cost, then applying a gross margin og 48% (achieved in H1), I estimate that current inventories would fuel about £192m in revenues (excl.VAT). With full year revenues of c.£220m expected for this new year, that means it could be holding about 319 days worth of sales in its warehouses! Which is crazily high.

This is the main question to ask management - why are they holding such excessive inventories? How much of that is slow-moving? Maybe this is why the audit is delayed, as the auditors have to check inventories for slow-moving lines, and make a provision against anything that can’t be sold above cost.

Hence I’m ringing an alarm bell here, that I think REVB has problem levels of inventories, maybe it was budgeting/buying for much larger sales? Or maybe some stock has been provided to retailers on a sale or return basis?

It’s not right anyway, so the excessive inventories are a red flag for me. There could be trouble ahead, with another profit warning, I suspect - if the company needs to take write-downs against some of the inventories. Looking at the product on REVB’s website, a lot of it is subject to the vagaries of fashion. On a 48% gross margin (H1 actual), anything REVB has to sell at half price, turns from a 48% gross profit, into a (2)% negative gross margin. So that would need a partial stock provision against it, because it’s net realisable value in accounting standards, which would presumably include the costs of selling it.

My opinion - it’s easy to get too gloomy when a profit warning comes out, and the share price plunges.

The market cap has dropped to only £84m here now.

Is it going bust? No, I don’t think so, the balance sheet looks OK, although I am very worried about what seems like extreme over-stocking, which could result in the auditor (who needs more time, remember) insisting on a heavy provision against slow-moving stock. Or, if the slow-moving stock is dribbled out in the new financial year, at discounted prices, that would hit the profits again. Either way, I reckon another profit warning is probably already gestating. So why get involved now, when there’s all this uncertainty?

On the plus side, make up is a decent margin sector, and REVB has built up a decent-sized business. My niece tells me the products are good, and reasonably priced.

At some stage then, it could be an interesting share to look at, but for me, not before the auditor has approved the FY 2/2022 results in about a month. Then we can look at it again with fresh eyes (with maybe just a touch of mascara, if I decide to mystery shop this company too!)

EDIT: Many thanks to Zeus, I've just seen an update note from them. It makes sobering reading. Forecast profit for FY 2/2023 and next year, are slashed by two thirds. This becomes only 1.5p adj EPS for this year, and 1.9p next year. That's terrible! So if that's the new base line level of profits, then it's difficult to justify a share price of any more than say 20-40p. the current price is 27p, so it's probably in the right range, based on the information we currently have. End of edit.

Graham’s Section:

Devro (LON:DVO)

- Share price: 186.2p (-0.5%)

- Market cap: £312m

This is a mature business involved in the making of collagen casings for sausages. It doesn’t tend to cause much controversy or attract much comment, but a quick look at the quality metrics will show that it’s probably a decent business:

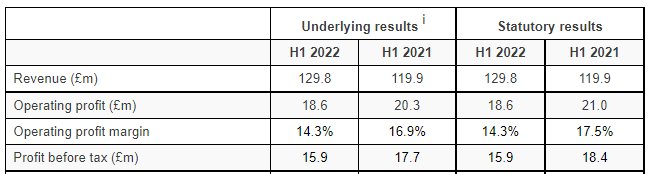

Today’s half-year results are described in a neat little table:

As you can hopefully see, there is no difference between the underlying and the statutory results in H1 2022. So it’s a clean set of results.

Sales - We have an 8.3% revenue increase, or 8.8% at constant currencies.

Food price inflation is obviously quite high right now, so some of the revenue increase is going to be due to that - the company says revenues grew to the “continued success of our strategy, as we take market share, and the initial benefits of our pricing actions”.

The company then provides a very helpful revenue bridge (wouldn’t it be great if every company did this?):

This makes it crystal clear: about half of the revenue increase came from higher volumes, and nearly the same amount came from changes in prices and the product mix.

Profits - as the first table showed us, there was a reduction in profitability and the operating profit margin. An explanation:

Operating profit reflects good operating leverage offset by inflationary pressure, which will be fully offset, mainly by higher selling prices in the full year, and higher costs to drive growth including new product development.

We’ve said before that in times of high inflation, that pricing power becomes important: can companies pass on their rising costs to customers, and can they do it quickly? Doing it slowly, for some companies, might mean the difference between surviving and not surviving!

There is little doubt that food producers are able to pass on their costs, and are able to do it quickly. In the case of Devro, it might not yet have fully passed on rising costs, but it’s in the process of doing it - and it’s confident that it will be able to pass them on this year.

Free cash flow - £3.2m. This seems low, but there is a regular capex bill at Devro and they’ve spent a little more this year, trying to develop new products and increase capacity:

We have also recently committed to further production capacity increases in 2023 leading to capital expenditure remaining slightly above depreciation next year. These capacity increases are required based on the multi-year demand growth we see in our planning. The financial returns on the incremental capacity are well above our cost of capital. We expect the capacity added in China and Czech Republic during the second quarter of 2022 to be fully utilised by the 2022 year-end.

As you can see, this is another international company with broad geographical exposure - that’s very valuable to have, in my view!

Balance sheet - net debt is £95m, which is down compared to the same date last year. As I’ve already said, the Devro capex bill can be expensive, but cash generation from operations tends to be strong enough to pay for it (and also to pay out some dividends - the company has paid a dividend for nearly 30 years).

On the balance sheet, total borrowings add up to £120m, and I’ve noticed that a big chunk of this falls within “current liabilities” - i.e. it might need to be paid back within a year.

It turns out that about half of the borrowings are in the form of a bank RCF that is maturing in June 2023. The going concern note tells us more:

The group is well advanced with the banking syndicate to renew the facility, with an expectation of signing the renewal in September 2022. However, should this facility not be renewed, the group's financial forecasts indicate adequate headroom to operate under various scenarios having taken account of different mitigating actions within the Directors' control.

It doesn’t seem like there is too much to worry about here. Devro is a mature, profitable business that is well within its banking covenants.

Outlook - full year expectations are unchanged. The “robust first half performance, solid order books, pricing action and ongoing momentum” give confidence.

My view - as I said at the top, this one doesn’t cause much of a fuss in the world of small-cap investors. It’s a bit boring and it generally just does what it’s supposed to do: make collagen casings and sell them at a profit, and pay a dividend to shareholders.

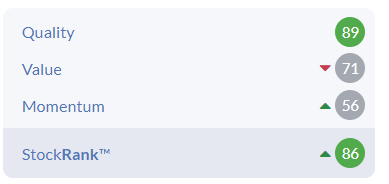

That dividend is now offering a decent yield, according to Stocko:

Stocko also likes the quality and value:

Personally, I feel that this company is a little bit unloved and underappreciated. It probably won’t multi-bag in the short-term, but the same is also true of most companies.

On the other hand, it probably will continue to report annual profits and dividends, which it has done almost without interruption for decades. It’s a far more reliable performer than most companies of this size. What’s not to like?

.

A G Barr (LON:BAG)

- Share price: 543p (unch.)

- Market cap: £608m

This is a well-known drinks company, though I must admit that I’ve not tried many of its brands. I’ve had IRN-BRU and Snapple, and I think I’ve had Strathmore (but this is just water!). As for the others, I’m not sure!

Anyway, this H1 trading update is in line with expectations. Like the rest of us, drinks companies have had a tricky few years to deal with, and it’s reassuring to see some stability in the performance now:

Like-for-like revenue growth in H1 is 19%; the actual reported revenue growth is 16%.

(Small calendar differences from one year to the next can easily knock a percentage or two off top-line figures, but not every company reports these differences - just something to bear in mind. There’s always an element of interpretation at work in financial analysis, even for something that you might think should be straightforward, like the sales number!)

Here’s the company’s explanation of their success in H1:

Our growth has been driven by ongoing brand investment and the successful execution of our pricing and promotional activity. Trading performance further benefited from the year on year Covid recovery across the market, particularly in the on-trade and out of home sectors, as well as the exceptional British summer weather in recent weeks.

This all sounds very positive, but note that this trading update doesn’t give any detail in terms of volume growth.

The broker note does give an opinion on this: they think that volumes increased by 3% to 4%.

If volumes are up by less than 4%, and like-for-like revenues are up by 19%, this leaves lots of room for inflationary price increases. Some of the price increases might be due to “brand investment” (i.e. the company itself stimulating demand) but probably most of the increases are down to the fact that there is too much money chasing too few goods.

The outlook statement helps to confirm the importance of inflation:

We anticipate that the UK's current high level of inflation will continue across the balance of the year, with economic conditions becoming increasingly challenging for consumers and industry alike. Across the second half of the financial year we will continue to invest behind our brands and believe that our strategy will support continued growth. At the same time we will take appropriate mitigating action to limit the full year impact of cost inflation.

My view

BAG shares are more on the expensive side, but there’s still a lot to like here:

I’ve double-checked the January 2022 balance sheet. The company had effectively zero borrowings and net cash of £68m. That’s a very significant war chest for a company of this size and needs to be reflected in the market cap (currently around £600m).

If you subtract the cash balance from the market cap, you’re left with a company trading at around 13x next year’s PBT estimate. It’s not so very expensive, in my view.

Why wouldn’t I buy the shares? Well for one thing, as already mentioned, I haven’t got much familiarity with the company’s drinks, beyond two or three of them.

I also think that the heatwave this year should have helped the company a lot, but volume growth of perhaps 4% doesn’t strike me as particularly strong, and the trading update is merely in line with expectations.

These aren’t serious quibbles: as a long-term hold, I think that A.G. Barr is a decent choice. It’s clearly quite good at passing on inflationary prices to its customers.

You may have more conviction than me, especially if you’ve researched their portfolio in greater detail and if you aren’t hoping to time your purchase to coincide with a rainy summer (when the share price might be more depressed than it is now!).

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.