Good morning from Paul & Graham.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Agenda /Summaries

.

Paul’s Section:

Trifast (LON:TRI)

63p (down 32% yesterday)

Market cap £86m

Trading Update & Directorate Change

London, Monday, 20 February 2023: Trifast (LSE: Main Market symbol: TRI) provides the following update on the trading performance for the financial year ending 31 March 2023 ("FY23") and notification of a Directorate change.

This announcement hit the shares very hard (down c.40% in early trades yesterday morning), although there was some partial recovery later yesterday.

Profit warning - adj PBT guidance for FY 3/2023 is reduced from £14.3m to £9.0m. Obviously that’s a disappointment, but the trouble is, it doesn’t take a lot to change, on £243m forecast revenues, for the profit number to change a lot. This is why the PER is quite a bad way to value companies, because profits can be so volatile, depending on circumstances that can't be predicted easily.

What’s gone wrong? The main factor seems to be de-stocking by an Asian customer, which has offset gains made from price rises & cost savings. Higher interest costs on “elevated” net debt of £44m is also mentioned.

What are they doing about it? Another strategic review has been carried out, resulting in cost savings of £5m annualised (it’s not clear if these are new savings, or increased savings from what was originally planned).

The long-standing CEO has stepped down immediately, and been temporarily replaced with a NED.

My opinion - this isn’t a disaster, assuming all the bad news is out. The risk is that a new CEO might kitchen-sink the figures, to get all the bad news out in one go, and to provide a nice platform to demonstrate improved performance thereafter.

The last balance sheet looks pretty good, with almost £100m NTAV, with the market cap below that figure suggesting shares might be cheap. Although inventories of £103.6m now, £102.8m when reported at the last balance sheet date of 30 Sept 2022, are still stubbornly high, and need to come down. The risk is that high inventories often contain obsolete or slow-moving items, which have to be written off. So it seems to me that there’s a fair chance we could have another profit warning from Trifast, to clean up the year end accounts maybe? Although that’s guesswork on my part, so is more a risk than a certainty.

Bank financing doesn’t seem to be a problem, with yesterday’s update confirming it remains within facility limits, and covenants.

Overall then, I don’t see this share as being in a crisis situation. The risk of insolvency or a deeply discounted fundraising strikes me as quite low.

The trouble is, it’s now a fairly low margin business, in a sector that’s probably very competitive. So I’m struggling to see any reason to invest in this share.

It all depends on the extent and timing of a recovery in trading, and whether there’s likely to be another profit warning in the meantime? That’s impossible for me to gauge. I don’t see anything too serious in the profit warning, and with little balance sheet risk, I’ll declare myself as neutral (amber) on this share.

Looking below at the long-term chart, it's interesting to see that the share price has now given up all of the bull run, and is back to a similar price 10 years ago. The share count hasn't risen a huge amount in the last 6 years either, so a recovery in margins could trigger a decent share price recovery.

Finsbury Food (LON:FIF)

97p (down 2% at 09:56)

Market cap £126m

Finsbury Food Group Plc (AIM: FIF), a leading UK speciality bakery manufacturer of cake, bread and morning goods for the retail and foodservice channels, is pleased to announce its unaudited interim results for the six months ended 31 December 2022.

The company gives itself a pat on the back -

Encouraging H1 performance

The context here is that the food industry has been hit hard with cost increases - raw materials, energy, and labour. So for FIF it has been all about managing these cost increases, and passing them on to customers.

Some key numbers for H1 -

Revenues up 15% to £190.9m (the increase has all been due to higher prices, with volumes said to be “broadly flat”)

Operating profit margin is tight, and lower, at 3.4% (H1 LY: 3.9%)

Adj PBT of £4.4m vs £5.0m in H1 LY

Outlook - challenging macro, but on track to meet FY 6/2023 forecasts.

Net bank debt £22.8m, which is only 0.8x annualised EBITDA, which looks fine to me.

Balance sheet looks adequate, with about £35m NTAV

Cashflow - capex, increased working capital, and dividends paid absorbed the cash generated by the business.

Pensions - I didn’t quite understand the note about this, which could have been explained better -

The Group has one Defined Benefit Pension Scheme within its Memory Lane Cakes business in Cardiff. All remaining Group companies have Defined Contribution Schemes. The Memory Lane Cakes pension Scheme has been closed to future accruals and new members since 31 May 2010. The net pension deficit (before related deferred tax) was £6,582,000 at 2 July 2022. The Company entered into an Asset Backed Contribution (ABC) arrangement on 18 May 2022 to improve the funding of the Scheme. An investment of £16.0 million will be invested by the Company to the Scheme, the trustees have purchased a loan note from the Group via a Scottish Limited Partnership (SLP) structure, which will pay a defined income return to the Scheme over 20 years. The fixed repayment plan amounts to an income of £763,000 being paid to the Scheme annually. The estimated duration of the liabilities is around 15 years.

Valuation - it is forecast to make 10.7p EPS this year, so at 97p per share, the PER is 9.1x, a modest rating. Although as noted before, FIF shares always seem to attract quite a low rating.

My opinion - the share price has now fully recovered last autumn’s spurious fall, giving a c.50% gain from the lows. So it’s gone from stupidly cheap to just cheapish now. For that reason, I’ll go from green to amber.

It’s still a nice enough business, but the 3.4% operating margin doesn’t leave a lot of margin for error.

One interesting angle on this share, is whether the headwinds of the last year (higher energy, and raw materials) could become a future tailwind, as costs moderate? If so, that would possibly enable FIF to improve its profit margins in future? Given how much cheaper gas prices have become of late, then maybe we should be thinking beyond the energy crisis to what happens next, which might boost profits?

Graham’s Section:

National Milk Records (OFEX:NMRP)

Share price: 120p (-2%)

Market cap: £25m

This is one of the few Aquis-listed stocks (not AIM) I like to report on, because I have the impression that it’s a high-quality business.

It’s an information services provider to the UK dairy industry, whose customers include farmers, vets and milk buyers. Milk recording, milk testing and disease tests are the flagship categories. About 50% of the UK herd is tested by NMRP.

Here are the H1 highlights for the period to December 2022:

Turnover plus 5% to £12m

PBT plus 5.3% to £0.79m

Net debt reduces slightly to £0.9m

Net assets plus 30% to £9.3m

Comment from the FD:

"The results for the first half of the financial year show a solid performance year on year, albeit with EBITDA held back by the differing accounting treatment for vehicles not under finance leases, reorganisation costs for consolidating milk testing at our Four Ashes laboratory, and our investment in the opportunity for GenoCells in the US. On a like-for-like basis, EBITDA was approximately £290,000 higher, representing a year on year increase of 17%. At this level of analysis, the figures continue to demonstrate sustainable growth in revenues and earnings, in line with our medium term growth ambitions. In addition, the Group has increased its capital investment, whilst also reducing net debt and paying an increased full year dividend.

As I mentioned previously, NMRP is currently investing in a genomic testing service. The financial return it will make on this is unknowable, but I think it’s important to mention when there is a “wild card” attached to a stable, profitable business. This genomic technology, called “Genocells”, is to be launched in both the UK and the US later this year, with the aim of enabling farmers to manage mastitis in their herd more efficiently.

Management - the MD is currently undergoing medical treatment, and the FD has operational control on an interim basis.

Outlook

Some familiar inflation themes in the outlook statement:

Cost input inflation is “significant”; NMRP has “increased prices for its services, across the board, to maintain margins”.

Employment market creating (upward) pressure on wages.

Milk prices remain 50% higher than average over recent years.

It sounds like a favourable environment for NMRP:

Inflation has led to a scenario where marginal decision making for farmers carries more risk: higher costs for investment and higher input costs are making the need for robust data insights becoming ever more important. Furthermore, maximising the efficiency of a herd is the single most direct route for the dairy industry supply chain to achieve its sustainability objectives.

My view

I think there’s enough in this statement to retain my positive view on the company. Admittedly, growth in the short-term is not too exciting. However, revenue from “Genomics” has doubled compared to H1 last year, and while it’s still very small, I think this could add a fresh growth spurt to NMRP’s results over time.

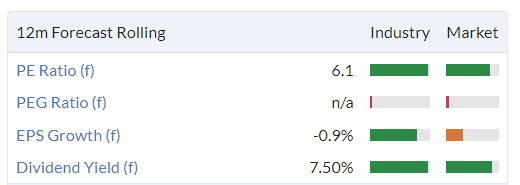

Valuation has remained reasonable, with a PER that would be suitable for companies of much lower quality:

Helping to confirm its status as an under-the-radar stock, it passes Stockopedia’s Neglected Firms screen:

In summary, while I don’t see any immediate growth drivers for NMRP, I think Genomics could help to accelerate results over the medium-term. I also think the underlying business is very high-quality (as demonstrated by its high market share and financial returns), and the valuation is reasonable. So it gets the thumbs up from me.

Springfield Properties (LON:SPR)

Share price: 80p (-9%)

Market cap: £95m

Let’s take a look at the interim results from this Scottish housebuilder, for the period ending November 2022.

Revenue +85% to £162m (helped by acquisitions)

Gross margin 14% (H1 last year: 18.5%)

Adj. operating profit +21% to £8.2m

PBT down 5% to £5.9m

The profit result looks disappointing compared to the revenue growth, but we do get the explanation very quickly, and promised actions:

Significant impact from build cost inflation, particularly on fixed-price contracts in affordable housing, affecting margins across the Group.

Decisive action taken during, and post, period across the business to address the market conditions, resulting in expected annualised cost savings of approximately £3.0m

Housing categories

Private housing is by far the largest category at Springfield (ahead of affordable housing and contract housing), where I note that “reduced homebuyer confidence impacted private housing reservations towards the end of the period”.

More encouragingly, “since period end, the Group has been encouraged by the reservation levels across its brands”.

When it comes to affordable housing, Springfield has decided “to temporarily pause entering new long-term affordable housing contracts until market conditions improve”.

Similarly, plans to produce contract housing for the private rented sector have been withdrawn, “ following the Scottish Government's intervention in rent control”.

So the two smaller categories are both on hold, and Springfield looks set to focus instead on private housing.

Land bank sounds healthy with 16,975 plots (31 May 2022: 16,652), having Gross Development Value of £3.7bn (31 May 2022: £3.5bn). Given the market conditions, they reduced their land buying activity and wanted to make additional land sales, but could not get “acceptable value” for them.

Net debt rises to £74m (previous year: £43m) after two acquisitions. Land sales could be useful to keep a lid on this debt figure.

Facilities: the company has an £87.5m RCF and a temporarily increased £12.5m overdraft. My impression is that headroom is limited.

Dividend: possibly confirming my impression that headroom is limited, the company cancels its interim dividend. The company says that it does have a “strong financial position”, but that cancelling the dividend is “an appropriate and prudent measure to preserve liquidity in these uncertain times”.

Outlook is cautious, given the market backdrop. But official guidance is unchanged for the current financial year (Progressive are forecasting adj. PBT of £17m, rising to £20.2m next year).

My view

On balance, I’m inclined to think that this one could be undervalued. The factors impacting margin are, in my view, likely to be temporary in nature. Affordable housing will be purchased again, at margins which make it feasible for the builders. And rent control policies - which affect Springfield’s “contract housing” category - don't usually last forever. But of course the timing of when these categories might recover is uncertain.

Tangible net assets of £137m are significantly higher than the market cap.

Also, the land bank is very healthy and is possibly even too large, given Springfield’s debt load and lack of headroom. Some strategic land sales would be welcome.

Overall, I’ll stay neutral on Springfield, pending further research. Without the financial risk associated with using a temporary overdraft, I could consider taking an outright positive view on it.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.