Good morning from Paul & Graham!

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

** New SCVR summary spreadsheet for calendar 2024 ** This is the live one! (updated 6/9/2024)

Archive - SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia. More stock screening strategies here (possible bargains?) - 21/9/2024.

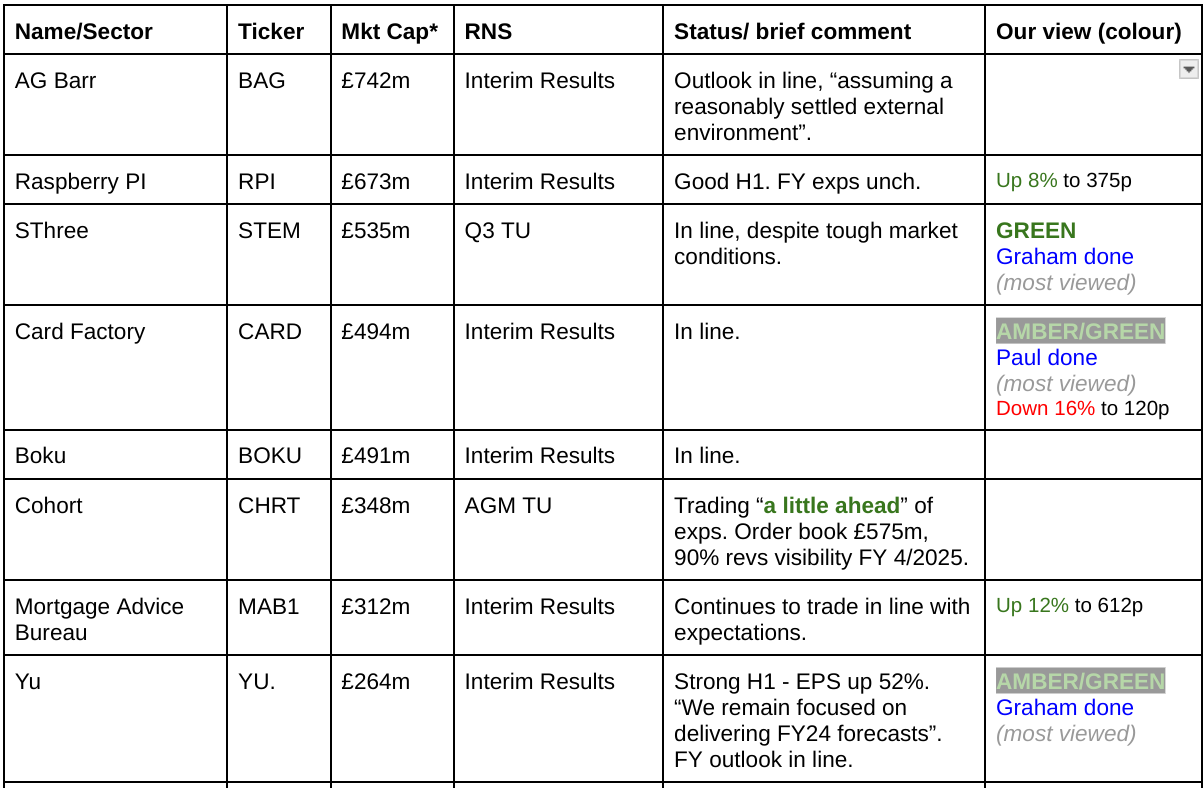

Companies Reporting

Summaries

SThree (LON:STEM) - down 2% to 388p (£524m) - Q3 Trading Update - Graham - GREEN

Tough market conditions for recruiters continue and STEM is not immune, posting an 8% reduction in net fees. The market may be a little disappointed that there has been no improvement yet, but I continue to rate this company highly both against its peers and as a standalone investment idea.

Card Factory (LON:CARD) - down 17% to 119p (£413m) - Interim Results - Paul - AMBER/GREEN

Weak H1 results, hit by higher wages costs, but it reiterates full year guidance, which will require a particularly strong H2 weighting, so some doubt has crept in. That said, the forward PER of c.8x allows room for some doubt. Good divis now, and the balance sheet has been sorted out without fresh equity being needed. Looks pretty good, but not as compelling risk:reward as it was earlier this year, so I moderate from green to AMBER/GREEN.

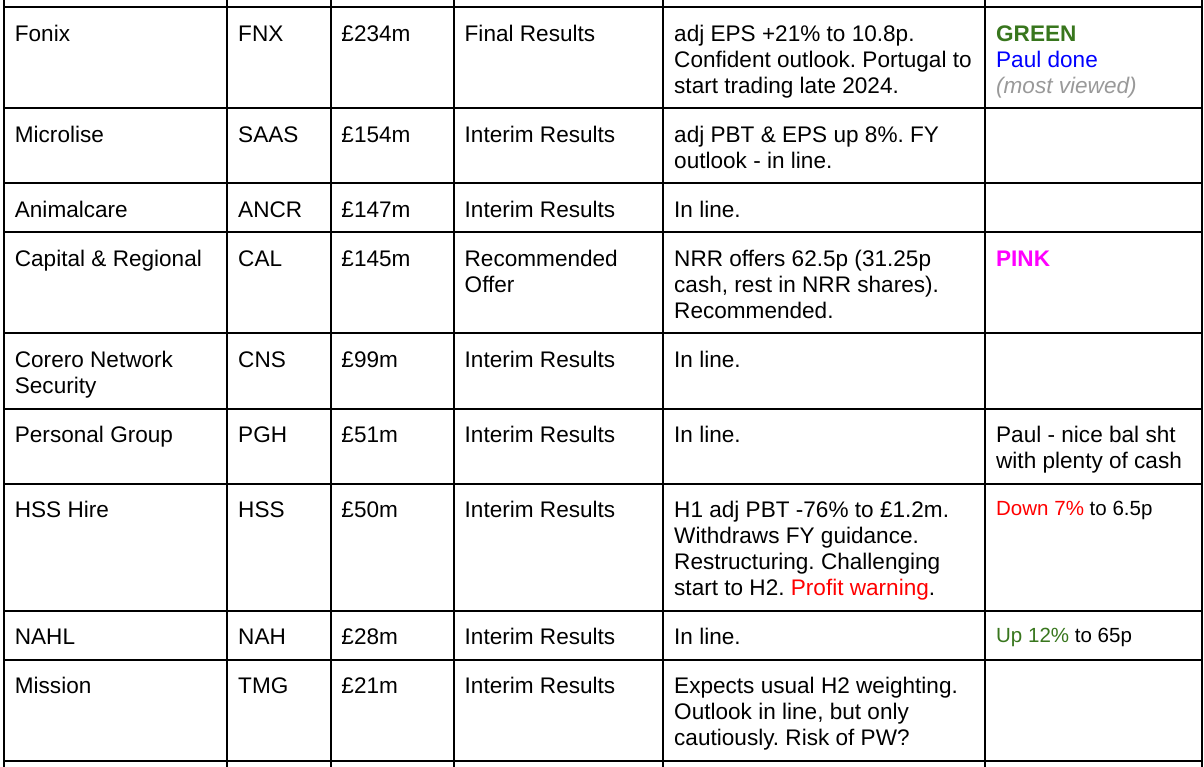

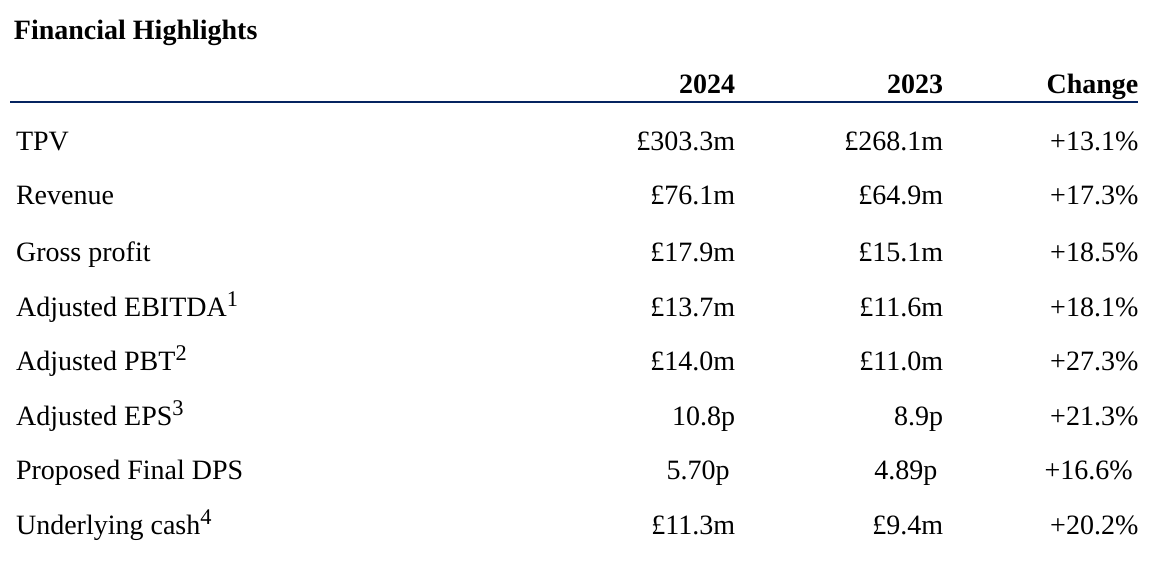

Fonix (LON:FNX) - down 1% to 235p (£232m) - FY 6/2024 Results - Paul - GREEN

Smashing numbers again from this quality company. Sticky clients, good cashflow, and a capital-light model means it pays out decent, and growing divis - quite unusual for a small tech company. I like the international growth continuing, with a fresh launch into Portugal imminent. Valuation looks reasonable, and broker forecasts set low, and likely to be beaten. A keen GREEN from me again!

Yu (LON:YU.). - up 3% to £15.90.50 (£267m) - Interim Results - Graham - AMBER/GREEN

I’ve upgraded my stance here as I find the organic growth in revenues (+60%) and profits (+122%) too good to ignore. The good news probably can’t last forever as margins are bound to fluctuate, but I have to sit up and take notice when a company posts numbers like this. The CEO (and largest shareholder) appears frustrated with the lack of share price momentum - and maybe he has a point?

Paul’s Section:

Fonix (LON:FNX)

Down 1% to 235p (£232m) - FY 6/2024 Results - Paul - GREEN

One of our favourite shares here at the SCVR. Fonix provides the IT/telecoms services for TV viewer voting, eg charity things like Children In Need, and eviction type reality TV shows. Also Eurovision for the first time in 2024.

It’s lucrative work, with very sticky clients who stay with Fonix because it always works, hence clients are not interested in taking the risk of switching supplier for their mission-critical revenues. I think that’s a decent moat.

My previous notes show we’ve been GREEN 3 times this year: 24/1/2024 - marginally ahead TU, 19/4/2024 Directors sell in secondary placing, and 22/7/2024 ahead exps TU.

The only question marks with FNX have been how to value the shares (they tend to be on a fairly punchy rating of 20-30x PER), and if the growth can continue.

As you can see below, +27% growth in adj PBT ticks the growth box! -

Adj EPS of 10.8p gives a PER of 21.8x, which I think is justified by the growth. That's likely to drop into the high teens by this time next year, from higher earnings.

Dividends - 2.6p interim already paid, plus 5.7p final = 8.3p total, a 3.5% growing) yield. Not bad. Note that 77% of earnings are paid out in divis, as this is a capital-light business model that doesn’t need cash for any other purposes, the ideal scenario for investors.

Note that higher interest received on cash balances boosted profit by about £0.8m vs LY (last year).

Outlook -

“The business maintains a robust pipeline of prospects going into the next financial year…”

“The Board remains confident in Fonix's growth potential for FY25 and beyond, supported by high levels of recurring revenue with a strong run-rate, an expanded commercial offering, and significant opportunities for further international expansion.”

It’s keeping things updated with new payment methods and features, eg -

“Significant investment in new product features in the Year, including live broadcaster voting, online payment portals, new payment integrations, new mobile network operator connections and advanced campaign scheduling.”

International - at present Fonix is mainly UK, but has also done well in the smaller Ireland market. This is exciting - Portugal is the next market it’s hoping to crack -

"We have made significant strides in our growth strategy this year, expanding our commercial offering and capitalising on a client-driven opportunity to build a substantial sales pipeline in a third geographical market, together underpinning our growth expectations for the year ahead.

In the next 12 months, we plan to further enhance our products, building on the strong progress achieved in FY24. Our serviceable market is expanding significantly with new direct network connectivity in Portugal, and we will explore additional direct connectivity opportunities in other territories in FY25 as we determine the most effective routes to market.

With a fair wind, we hope to begin transacting in Portugal before the Christmas trading period commences. By achieving this and continuing to nurture growth from our existing clients, we believe we have a strong opportunity to further build on our outstanding record since IPO."

Forecasts from Cavendish (many thanks) are modestly set, so FNX looks well set up to publish “ahead of expectations” updates as FY 6/2025 progresses, so very little risk of a profit warning, given the sticky repeating clients.

Balance sheet - is quite modest, as there’s not much in fixed assets, and no inventories. NTAV is c.£9m, which is enough.

Net cash of £26.5m is not quite as good as it looks, as some of that cash is passing through. Net current assets are £9.2m, which I would use as effectively the company’s own surplus cash. I imagine cash balances would be quite erratic, depending on when large amounts come in suddenly from a popular show, but then large remittances have to be paid over to the TV companies some time later. Anyway, it’s all fine, so nothing to worry about.

Finance income of £1,127k on the P&L suggests to me that Fonix probably sits on an average cash balance of c.£28m, assuming it earns c.4% on cash. That’s very close to the year end £26.5m cash, giving me comfort that the cash is real, and not a spike up for window-dressing purposes.

Paul’s opinion - this is a lovely business, with sticky revenues generating good margins and plenty of free cashflow. It hasn’t put a foot wrong since listing. I’m impressed at the continuing growth, and entering a new market, Portugal, sounds intriguing. It would be interesting to hear from management as to why they’re going into Portugal? Presumably each country has its own incumbent competition? Maybe FNX can win business by offering better features?

This strikes me as the type of share that you could just buy and forget, enjoying a steady stream of growing divis, and in say 5 years’ time the shares would probably be usefully higher. Who knows though, I wonder what direction technology might take this in future? Are there any potential risks on the horizon? The main short term risk would be a catastrophic meltdown in its IT, say if hackers went for it & got through, because it only has a short window of time to take in large amounts of viewer calls.

It has to be GREEN again.

If brokers would float more things like Fonix, then AIM would be a much healthier market!

Card Factory (LON:CARD)

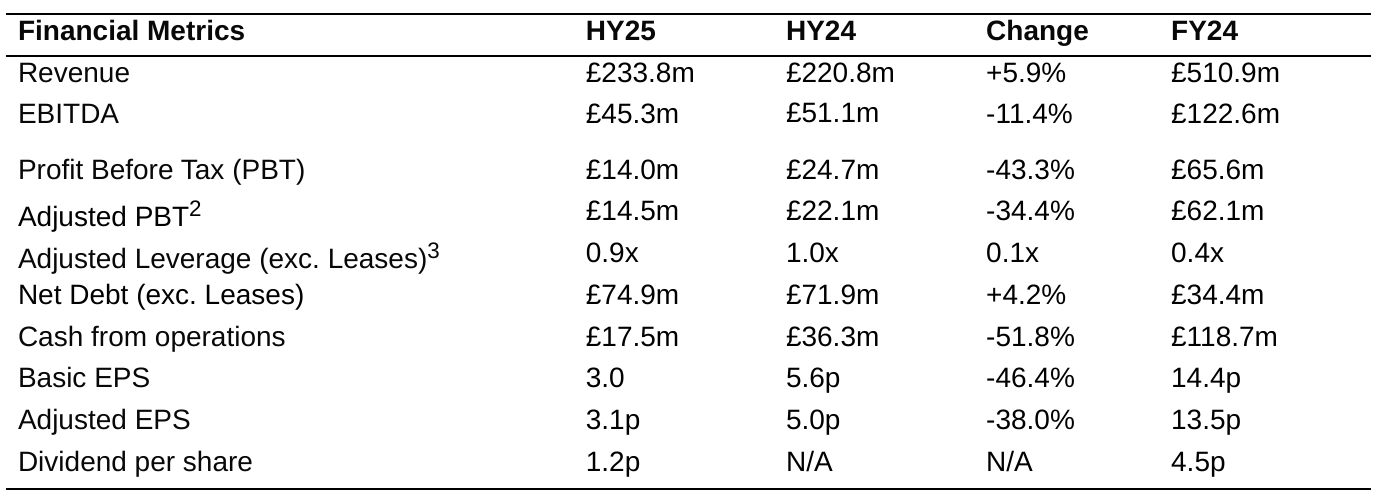

Down 17% to 119p (£413m) - Interim Results - Paul - AMBER/GREEN

cardfactory, the UK's leading specialist retailer of greeting cards, gifts and celebration essentials, announces its interim results for the six months ended 31 July 2024 ('HY25').

Quite a sharp correction this morning, with the recent gains being given back. That’s quite surprising given that it reiterates FY Jan 2025 expectations in the headline -

“Resilient revenue performance with further strategic progress achieved including successful partnerships expansion. Full year expectations unchanged.”

However, once I looked at the H1 highlights table, I can see why the shares have fallen today - due to poor H1 profits, being well down on H1 LY -

This is the explanation for profit being down 34% -

“HY25 Adjusted PBT was down £7.6 million to £14.5 million, reflecting substantial increases in National Living Wage, plus freight inflation and phasing of strategic investments. As previously guided, the benefit of our strategic investments and robust programme of productivity measures and efficiency savings in FY25 are weighted to the second half of the year and we have already seen these positively impact the cost base.”

Outlook comments - start off with this rather ambiguous point -

“Trading since the period end has been in line with the first half…”

Is that good or bad? The commentary talks as if H1 was good, but it wasn’t - profit was sharply down.

Cost pressures sound like they’re still an issue -

“Whilst macro-inflationary pressures have started to ease in the second half, we continue to manage specific retail impacts.”

It does provide good reasons for expecting an improvement in H2 -

“There are several factors that are supporting our profit margin performance going into the second half of the year. Approximately half of the margin growth in the second half will be driven by the seasonality of sales. Our robust programme of productivity and efficiency savings will also make a material contribution. In addition, we expect to benefit from margin-enhancing range development and prudent management of operating costs. “

Unchanged full year expectations, but obviously with a particularly heavy H2 weighting, and the risk that brings with it -

“Albeit we are yet to trade through the key Christmas period, the strong topline performance in the first half, combined with our robust actions to mitigate inflationary pressures, means that our expectations for the full year are unchanged.”

Broker forecasts have been edging up, which sits oddly with the weak H1 profit performance -

H1 actual adj EPS is 3.1p (down from 5.0p in H1 LY).

H2 LY was 8.5p (calculated as 13.5p adj EPS for FY 1/2024, less 5.0p H1)

The StockReport has 14.5p adj EPS forecast for FY 1/2025, so this implies a substantial increase to 11.4p (up 34% on H2 LY) in H2 performance. It’s quite unusual to see such a big improvement in H2 performance after H1 was sharply down. Hence I think there has to be an element of doubt about how realistic the 14.5p EPS forecast is? That could be what motivated sellers early today perhaps?

As I have some doubt over the 14.5p forecast, I’d be happier with a lower PER. Let’s say 8x, to allow wiggle room if H2 is not the barnstormer that is forecast, gives me a 116p valuation - pretty much bang on what the current price actually is, after a sharp fall today.

I see the word “resilient” is used by management to describe performance. I had to chuckle at the excellent Small Caps Live blog, which humorously (but actually quite accurately) says whenever they see the word “resilient”, they know things are really bad! Management have slipped in one instance of the deliberately vague phrase “profitable growth” too.

For balance though, there’s plenty of positive-sounding stuff in the commentary too.

Balance sheet - has been nicely repaired, from retained profits, with negligible dilution over the last 6 years. That’s a considerable achievement, as remember this company teetered on the edge of going bust since it went into the pandemic with excessive bank borrowings.

NAV is £312m, of which £332m is intangible assets (goodwill mainly), so NTAV is still negative, but only £(20)m, which is not a worry at all, given that inventories and receivables are fairly low, and property is mostly leased (there is £17m in freehold property too), so it’s an asset-light business model that generates plenty of cash, so it can comfortably carry some debt. I don’t have any remaining concerns at all about the balance sheet, as mentioned before, it’s fine now.

Let’s hope management learn from the mistakes of the past, and don’t gear it up again at the top of the cycle.

Going concern is clean, and with bank facilities renewed, and covenants comfortably complied with, there’s nothing to worry about.

Cashflow looks poor in H1, but given the H2 seasonality, I think we need to see the full year numbers before making a judgement.

Dividends are now being paid again. The StockReport shows broker consensus divis of 5.22p this year, and 5.83p next year, so on today’s reduced share price (down 15% at 122p at 09:46) gives a healthy (well-covered almost 3x) between 4.3% and 4.8%. Given that the divis are in a rising trend, then this looks attractive to me.

Paul’s opinion - I can see why some holders might see the H1 results as disappointing. It’s now relying on a particularly strong H2 weighting to meet forecasts, which does make me a little uneasy. That said, the valuation now reflects this risk I think.

It’s a pretty good business, trading on an undemanding multiple of about 8x, paying good divis, and with its financial risk now resolved.

I was green twice earlier this year, at 100p and 107p. We’re now at 122p, and H1 results have underwhelmed, putting more pressure on the H2 upturn to be particularly strong. Therefore I think risk:reward is not as good as it was when Teleios selling was suppressing the price (since gone).

Overall then, I’ll moderate to AMBER/GREEN today.

Graham’s Section:

SThree (LON:STEM)

Down 2% to 388p (£524m) - Q3 Trading Update - Graham - GREEN

We have an in line Q3 update from my favourite recruitment stock.

However, expectations were modest and the growth numbers are as follows:

Net fees down 7%.

Contractor order book down 6%.

Net cash fell to £45m (a year ago: £83m), “reflective of the timing of certain client payments, with net cash expected to return towards normalised levels over the coming months”.

At first glance, that might seem to be an alarming fall in the cash balance. But in my management Q&A with the company, I was told that SThree needs about £60m to fund “business as usual” along with planned contractor growth. In other words, swings in the cash balance are expected - let’s hope that it swings back towards the previous, higher level by the end of the year.

CEO comment:

Despite the challenging conditions in the market, which have extended beyond our industry's expectations, our strategic focus on Contract continues to underpin the Group's competitive positioning. The Contract order book, down 6%, reflects protracted soft new placement activity partially offset by ongoing strong Contract extensions.

The “Technology Improvement Programme” remains on track - one other interesting thing I learned from my Q&A was that SThree might be more open to doing acquisitions, when this is complete. The idea is that acquired companies would run more efficiently when they can be plugged into SThree’s new technological framework.

Revenue breakdown: geographically all regions are down except for the smallest one, “Middle East & Asia”.

As usual, Life Sciences had the sharpest fall, down 14% year-on-year as the post-Covid slump continues for now. The larger categories, Engineering and Technology, were down 7% each.

Graham’s view

The ongoing decline in fees is a disappointment but I think there are two points to bear in mind against that.

Firstly, this is an industry-wide issue and other recruiters are doing worse than SThree. For one example, Hays (LON:HAS) recently reported net fees down 14% in the twelve months to June 2024.

Secondly, despite the pressure on fees, SThree has remained highly profitable and protected its bottom line (so far). See our coverage of the interim results in July.

Therefore, I’m going to leave my positive stance on this one unchanged. I appreciate many things about it: the focus on Contract recruitment in scientific sectors, its technological efficiency, and its geographic diversification.

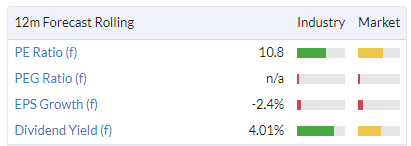

It continues to trade at attractive earnings multiples, in my view, making no adjustment for the cash balance:

The StockRanks love it, and it passes seven bullish stock screens.

None of this guarantees success, of course. As someone who likes the business, I just like to see when the stock screens agree with me!

Share price performance has been flat in recent years - it’s a slow burner, but a company I believe in.

Yu (LON:YU.).

Up 3% to £15.90.50 (£267m) - Interim Results - Graham - AMBER/GREEN

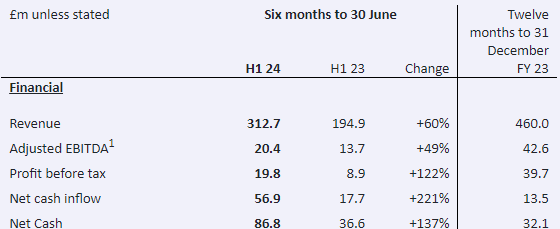

Yü Group (AIM: YU.), the independent supplier of gas and electricity, meter asset owner, and installer of smart meters to the UK corporate sector, is pleased to announce its unaudited half-year results for the six months to 30 June 2024.

These are fabulous numbers, which I believe are in line with expectations.

The growth is all organic. There was a remarkable 110% growth in the volume of energy supplied, leading to the following financial results.

Lower down, in their operational KPIs, they include their Trustpilot (LON:TRST) score! I think this is the first time I’ve ever seen a company do this. Their score is up from 3.5 to 4.3 (out of 5) over 12 months. Cynics may wonder if this coincides with Yu upgrading their Trustpilot subscription!

Getting back to Yu’s tangible achievements. They have seen an 80% increase in meter points supplied, and a 125% increase in smart meter installations.

Net cash, as shown in the table above, has more than doubled to £87m. The company has also cancelled its share premium account (an accounting item, on the balance sheet). This gives them the flexibility to return more cash to shareholders, if they choose to.

Outlook: EPS will increase in H2 vs H1, in line with expectations (adj. EPS in H1 was 88p).

CEO comment: starts out positively.

Yü Smart continues to go from strength to strength. Like all new startups, we've experienced growing pains and building teams who share our values and habits has required management attention. However, I'm satisfied good progress has been made and we have positioned ourselves for significant meter installation growth. Smart meter installations are up by 125% and engineering headcount is up 300%.

It ends with some more critical comments which I guess may reflect frustration with the company’s share price. Note that the CEO is the majority shareholder here:

The lack of Institutional engagement has been disappointing, despite management delivering colossal value year on year. Many AIM companies are questioning the market's future and the desirability of remaining listed. This has been reflected in the reduction of quoted companies. The AIM market's future is delicately balanced and won't be helped if the current government further punishes and disincentivises entrepreneurial high growth companies. This lack of recognition is frustrating; however, we remain focussed on delivering FY24 forecasts and positioning the Group for another record-breaking performance in 2025.

I’m completely speculating here but one interpretation is that he may have wished to sell a portion of his holdings, and expected that he would be able to do so at a higher share price.

The value metrics are indeed on the cheaper end of the spectrum:

Strategy - a five year agreement with Shell is underpinning Yu’s long-term supply. Market share has grown from 1.4% to 1.8% and organic growth remains the focus.

Graham’s view

I’m intrigued by the statement that mild Spring temperatures, and lower commodity prices, held back these results. YU could have done even better than this!

Roland was neutral on this in July when he covered the H1 trading update.

The share price is a touch lower than it was then, and I’m tempted to give the stance an upgrade to AMBER/GREEN.

It comes down to your view on the sustainability of profit margins - when all is said and done, YU is a supplier of commodities to extraordinarily price-conscious customers (small and medium sized business).

We’ve also seen YU struggle in the past, as it did from 2018 to 2020, partly due to accounting problems.

It’s a much bigger business now, however. With scale comes certain advantages and the tie-up with Shell could be an example of this. Perhaps it is now a safer investment proposition, having reached this size? Revenues are forecast at £668m this year, versus only £279m in 2022 (source: SP Angel).

This may be generous but I’ll tentatively give this an AMBER/GREEN. When a company posts organic growth like this, it has to be worth looking at in closer detail. Like my co-writers, I suspect that current profit margins may be unsustainable - but if its customer numbers keep growing quickly, maybe that isn’t the most important thing?

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.