Good morning from Graham & Paul!

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

** New SCVR summary spreadsheet for calendar 2024 ** This is the live one! (updated 26/8/2024)

Archive - SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia.

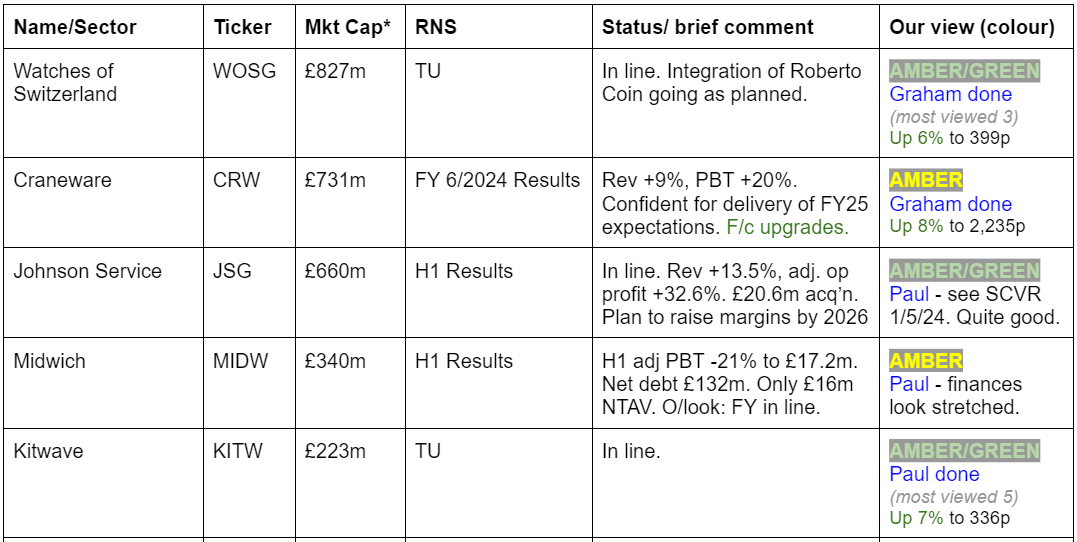

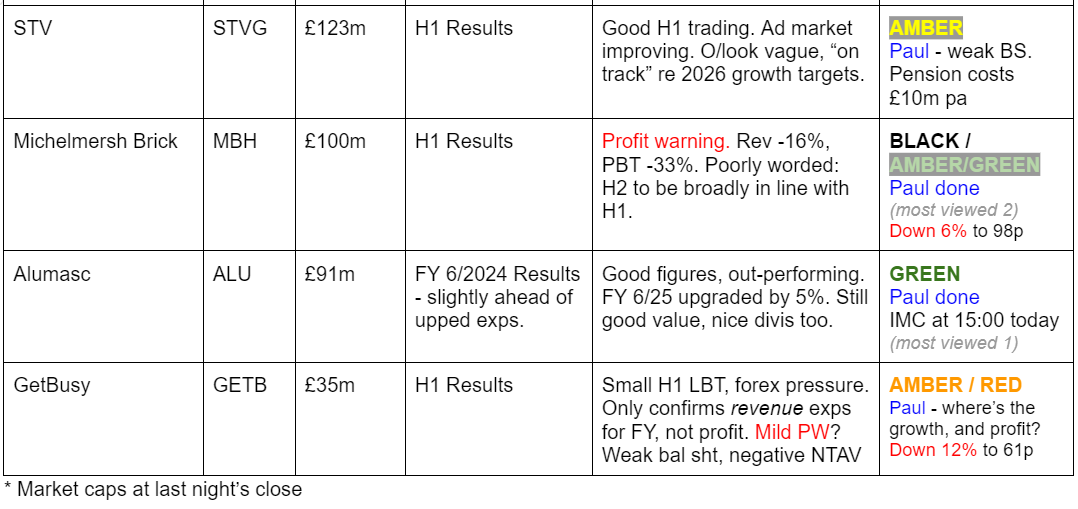

Companies Reporting

Summaries

Alumasc (LON:ALU) - up 5% to 265p (£96m) - Final Results - Paul - GREEN

Strong results, slightly ahead of forecasts that were raised in July. Everything looks good to me, with a decent balance sheet, and strong cashflows. This is a quality group of companies, with specialist environmentally good products, with pricing power. I think shares remain cheap on a PER of only 9x raised FY 6/25 forecasts. There should be a cyclical recovery to come too, so it might beat forecasts, as it did in FY 6/2024.

Craneware (LON:CRW) - up 8.5% to £22.46 (£793m / $1,041m) - FY24 Final Results - Graham - AMBER

A great set of results from Craneware and the analysts have updated their spreadsheets with higher revenues forecasts for the years ahead. The company is close to achieving the symbolically important “double digit growth” which I think could power the valuation to higher levels. For now, the valuation seems about right to me for a promising, high-performing software provider in the US healthcare space.

Kitwave (LON:KITW) - up 6% to 335p (£234m) - Trading Update - Paul - AMBER/GREEN

Decent summer trading seems to have eliminated the risk of an H2 profit warning, as it reiterates confidence in achieving FY 10/2024 profit expectations. It's an OK business at a fair price, although I can't get excited about it, due to pedestrian profit growth and rising debt from acquisitions.

Watches of Switzerland (LON:WOSG) - up 4% to 394p (£943m) - Trading Update - Graham - AMBER/GREEN

A sigh of relief for investors in this lowly-valued watch and jewellery retailer as it reports that trading has been in line in the first few months of the new financial year. Visibility over the rest of the year has improved and a large US-based acquisition is working out as planned. I was AMBER/GREEN on this earlier in the year and am happy to leave my position unchanged, as the company is executing well.

Michelmersh Brick Holdings (LON:MBH) - down 6% to 97p (£94m) - H1 Results - Paul - BLACK / On fundamentals: AMBER/GREEN

A 28% cut to FY 12/2024 forecasts does remarkably little damage to the share price of this premium brick maker. Despite today's disappointment, I like its balance sheet, generous divis, improving order book (which seems to contradict the H2 profit warning), and modest valuation on what could turn out to be bottom of the cycle earnings. I would pencil in c.25-50% share price upside in a recovering housebuilding market (maybe in 2025), as a distinct possibility.

Paul’s Section:

Michelmersh Brick Holdings (LON:MBH)

Down 6% to 97p (£94m) - H1 Results - Paul - BLACK / On fundamentals: AMBER/GREEN

Michelmersh Brick Holdings PLC (AIM: MBH), the specialist brick manufacturer and brick-fabricator, is pleased to report its half year results for the six months ended 30 June 2024.

We’re overdue a look at MBH, having not covered it so far in 2024, but we did 5 times in 2023, mostly favourably. Shares have been in a sideways trend for 2 years now. Actually it’s been in a broadly sideways trend for the last 10 years, with c.100p per share seemingly acting like a magnet on the shares, if they were made of metal.

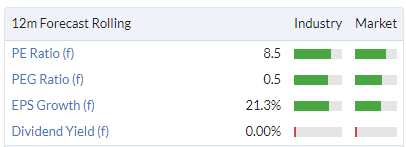

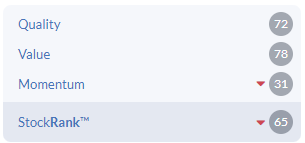

The Stockopedia fundamentals graphs below show a healthy picture, but a share which has de-rated onto a lower PER, and with a very nicely growing dividend yield, which has got my value antennae twitching!

I’m also liking the signs of a strong balance sheet, with a low price to tangible book, and good quality scores shown here -

H1 Results -

Revenue down 16% to £35.4m (it says this is as expected, and out-performs a market down 40%)

Adj PBT down 22% to £5.3m (not bad at all, as I would have expected an operationally geared, much larger % fall in profit)

Adj EPS down 25% to 4.28p.

Interim divi up 7% to 1.6p, “underlines the Board’s confidence in the outlook…”

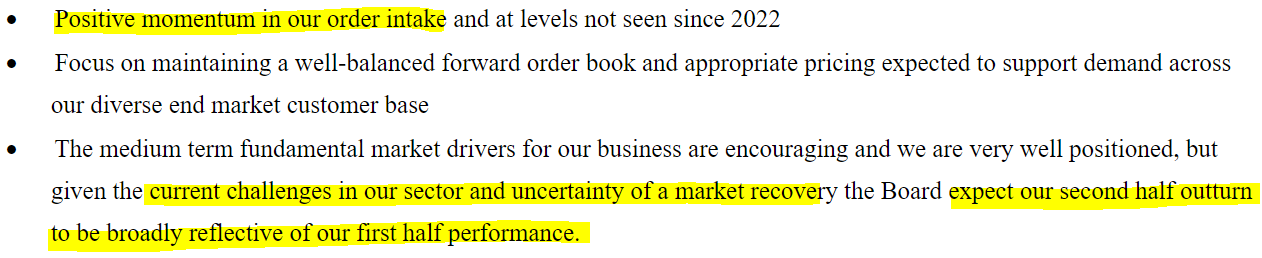

Outlook - some quite good things in here - but a sting in the tail, with the final point amounting to a FY 12/2024 profit warning -

“Across the Group, current order intake is running ahead of our manufacturing capacity which is contributing to a growing quality forward order book underpinning our second half revenue expectations.”

Surely that last quote contradicts the profit warning for H2? Rather confusing.

The above implies something like 8.0p EPS for FY 12/2024 maybe?

Canaccord comes to a similar view, taking an axe to its 10.7p previous adj EPS forecast, and revising it down 28% to 7.7p - actually quite a nasty profit warning, despite the attempt by MBH to PR their way out of a tight spot in the announcement.

That said, at 97p/share, after today’s surprisingly modest 6% fall in share price, the PER of 12.6x is hardly demanding, considering this could turn out to be bottom of the cycle earnings, as housebuilders are saying they expect a recovery in 2025, so logically MBH should benefit from that. Although it does make speciality bricks, so I’d be interested to know what proportion go to mainstream housebuilders, and how much to private, or smaller builders?

The new Govt supposedly wants to increase the number of new houses being built, so there should be a tailwind there, with hopefully lower interest rates also being a much needed catalyst for the sector.

MBH should be benefiting from lower energy costs now too, which it says are hedged (80% 2024, 40% for 2025).

Balance sheet - the stand out number is inventories, which has almost doubled vs a year ago to £19.5m, which is the opposite of what I would have expected in a sector recession with lower sales. They must be stockpiling for a recovery. The commentary says they’ve built up stocks to cover a 2-month factory shutdown for planned maintenance. It also says the industry as a whole has higher than usual inventories. So that could be a drag on prices in future maybe, if there's a glut of bricks?

Overall the balance sheet looks excellent, with £91m NAV, less £23m intangible assets, giving NTAV of £68m - supporting 72% of the market cap.

An unusual item is a £15.4m deferred tax liability - what’s caused that, and what significance is it? I never properly understood deferred tax, which is probably why I failed my ACA finals exams. Let someone else worry about deferred tax, was my attitude - not ideal for passing exams arguably, but it worked out fine as that’s exactly what I did when I was an FD not long afterwards in the 1990s - letting Ernst & Young do the deferred tax calculations, and to this day I still don’t understand it. Something to do with timing differences?

Anyway, the balance sheet is smashing. Net cash has fallen sharply, due to the inventory build. So there’s only £4.1m net cash remaining from £11.8m a year earlier, but it has a £20m bank facility available, so liquidity is fine.

Cashflow statement - is poor, because of the big inventory buildup. Let’s hope that reverses in H2, which seems to be what the commentary is pointing {geddit?!} towards.

Paul’s opinion - I think MBH shares got off lightly today with only a 6% fall, despite a 28% reduction in current year forecast EPS.

That said, we could be at or near the low point of the earnings cycle, and it’s still reasonably priced. So people might quite reasonably now be factoring in improving earnings in 2025 and beyond.

With a cracking balance sheet, and a 4.6% yield, with divis increasing, I think patient investors could do quite well on this one, on a tuck away and forget basis. Although the lesson from the long-term chart is maybe to sell the big surges, and wait for it to come back down again!

Kitwave (LON:KITW)

Up 6% to 335p (£234m) - Trading Update - Paul - AMBER/GREEN

Checking my previous notes in 2024 for this food/drink wholesaler -

28/2/2024 - GREEN at 297p - in line FY 10/2023 results, all looks fine. A decent GARP share.

2/5/2024 - AMBER/GREEN at 407p - in line FY 10/24, but H1 demand soft due to bad spring weather. Price up with events now.

2/7/2024 - AMBER/GREEN at 316p - lacklustre H1 results. Risk of PW if H2 weighting doesn’t happen. Balance sheet has a bit too much debt. Valuation more reasonable after recent falls.

Latest trading update today -

“Kitwave Group plc (AIM: KITW), the delivered wholesale business, today provides a trading update covering the four months to 31 August 2024.”

It’s good news, key summer trading has been robust -

“The Board is pleased to report that trading over the summer, traditionally the busiest period for the Group, has been robust. As such, the Group remains confident of delivering financial results in line with expectations for the full year ending 31 October 2024. “

That removes my main worry, of the H2 weighting not happening enough to offset the soft H1 (when operating profit was down 8% vs LY).

More details -

- Customer demand strong.

- Efficiency gains, eg voice-picking technology at a distribution centre.

- 2 acquisitions helped growth, integrating as planned.

Broker update - thanks to Canaccord for its update. Forecasts are unchanged today, at £29.0m adj PBT (up 5% on LY). That’s 29.9p adj EPS, giving a PER of 11.2x, which doesn’t look demanding, although a business of this type wouldn’t usually command a PER much higher than that anyway. Profit only growing 5% Y-on-Y, despite 2 acquisitions is not exactly stellar is it?

Paul’s opinion - this looks a decent enough business, shifting a lot of other people's products, for a 5% operating margin. It’s done a lot of bolt-on acquisitions, so the strategy is to be an industry consolidator, which might possibly allow it to increase margins a bit over time?

Finance costs are creeping up, as it loads up on debt, which was a tad too high for my liking at 30/4/2024 at £53m interest-bearing debt (excl. leases) gross, with £5m cash that’s net debt of £48m, or c.21% of the market cap in net debt.

Overall I think it’s OK, not madly exciting, and there could be maybe 10-20% upside on the current valuation - not enough to get me excited.

You are getting a c.4.2% dividend yield, but I don’t think the company should be paying such generous divis, at the same time as it’s accumulating debt to fund acquisitions. The cashflow statements do show that it could comfortably pay divis if it wasn’t also spending c.£20m pa on acquisitions.

The £78m goodwill on the balance sheet leaves only c.£7m in NTAV when it’s eliminated, which I think is getting a bit stretched given this is a significant sized business.

Is it worth sticking at AMBER/GREEN? Just about I’d say, as the risk of an H2 profit warning seems to have gone now, after a strong summer trading. Valuation looks reasonable, but I can’t get excited about the pedestrian profit growth, and rising net debt. Although note that Canaccord assumes it can pay off nearly all the bank debt over the next two years, which would be impressive if achieved. Put it like this, I can’t find anything particularly wrong in the numbers, and it’s an OK business at a fairly reasonable price, so let’s stick with AMBER/GREEN.

Good performance since listing, and note the high StockRank -

Alumasc (LON:ALU)

Up 5% to 265p (£96m) - Final Results - Paul - GREEN

Alumasc (ALU.L), the premium sustainable building products, systems and solutions Group, announces results for the year ended 30 June 2024.

One of our favourite shares here at the SCVR, which readers flagged to me on 9/2/2024 as looking interesting. I gave it an enthusiastic thumbs up at 179p, on in line H1 results and a bargain valuation. Broker consensus forecasts have been rising gradually this year, and we next looked at it here again on 18/7/2024, with another thumbs up (green) at 221p on an ahead of expectations trading update.

Today we get strong results for FY 6/2024, with this headline -

“DELIVERY OF STRATEGIC PRIORITIES DRIVING MARKET OUTPERFORMANCE WITH FURTHER UPGRADE TO 2024 PROFIT”

How much of an upgrade? Cavendish says it’s beaten FY 6/2024 EPS forecast by 2.3%, so a slight beat. Cavendish re-works the numbers to report a 26.6p adj diluted EPS (close to the underlying EPS of 26.9p in the results announcement), giving a PER of 10.0x based on this morning’s higher 265p share price. Not expensive, despite the strong rise in share price this year.

It’s notable that ALU is bucking the trend, out-performing a sector which has generally been struggling this year. Could that be lucky one-off orders, or possibly a sign that its innovative products are in demand, despite soft sector fundamentals (which could point to even stronger performance once markets are more buoyant).

I had a very good call with management earlier this year, and it struck me what a good job they’re doing in particular with product innovation, which is offsetting weakness elsewhere. The strategy to innovate, and command higher margins, is clearly working. The market is gradually waking up to the quiet transformation that seems to be underway at ALU - this is a quality business, with pricing power (and well-established brands/reputation), not just a distributor of generic products -

“Group underlying operating margin* of 14.1% (2023: 13.6%), progressing towards 15-20% target margin range, with all divisions contributing to the improvement”

Adjustments to profit are only small, and look acceptable to me.

Dividends are an attractive feature of this share, and are growing - the yield is a handy 4.1% -

“Progressive dividend policy reflects Board's continued confidence in outlook. Final dividend proposed at 7.3p (2023: 6.9p) per share, contributing to a total dividend of 10.75p (2023: 10.3p) per share, within our medium term objective of 2.5-3.0 times earnings cover”

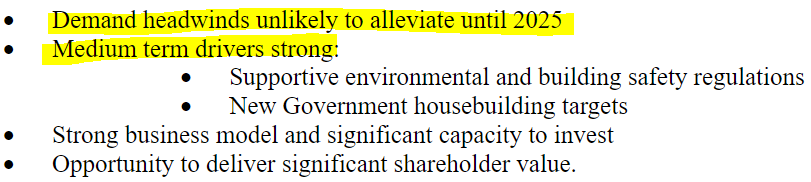

Outlook comments are general, but optimistic in tone - eg

“While demand headwinds in Alumasc's commercial markets are likely to persist for the remainder of 2024, we are encouraged by early indicators of easing in planning, improving consumer confidence and the interest rate outlook which suggests an improved trading outlook in due course. With the positive trading momentum Alumasc has carried into the new financial year, and the improving economic environment, the Board is optimistic for another year of growth.”...

“While we still expect market headwinds to persist in the near term before commercial conditions strengthen materially, including anticipated further interest rate reductions, Alumasc is confident in its future prospects. Our recent track record of consistently delivering profitable growth; investments in people/processes/new products/ARP; the evolving regulatory/environmental and construction/housebuilding landscape; and our self help measures cause us to be optimistic about the delivery of our medium term aspirations, as market conditions improve.”

Cavendish has raised forecasts today for the new year, FY 6/2025 - raising forecast adj EPS by 5% from 28.0p to 29.4p (PER 9.0x).

Hopefully these numbers might be beaten, as the sector sees a macro recovery in 205 maybe?

Acquisitions - ALU seems good at these, and doesn’t rush into lots of deals. ARP has gone well -

“Since we completed the strategic acquisition of ARP Group and welcomed our new colleagues, the business has performed extremely well, bringing exciting synergies and opportunities for cross-selling to the business.”

Balance sheet - note the pension scheme consumes £1.2m pa in cash contributions towards the actuarial deficit. It has moved into a small accounting surplus of £0.8m, so hopefully in due course the actuarial-based contributions might subside somewhat. I’m working on the basis the £1.2m pa is likely to continue for several more years (next actuarial assessment is 2025, and they often take a year or more to agree).

Bank debt is modest, and has risen due to the cost of acquisitions. I ignore leases, as it’s not debt, it’s future years’ operating costs, and there are no covenants or risk of withdrawal. Leases are only a problem if they are onerous. So the old accounting method was far superior and reflected commercial reality, whereas IFRS 16 has screwed up all the numbers and needs to be adjusted out for the accounts to make sense. Maybe the new Govt could have a clear-out of the accounting standards bodies too, as not fit for purpose?!

Overall the balance sheet looks fine to me, with c.£14m NTAV. Nothing untoward in there.

Cashflow statement - again, very clean numbers. It generated £14.1m in post-tax operating cashflow. About a quarter of that was spent on capex. The biggest item is £8.5m outflow (net of cash acquired) for an acquisition - this is why net debt went up as noted above.

Bank interest was nearly £1m, and dividends cost £3.7m. Plus £0.6m spent on buying back its own shares.

All very good - it’s able to pay out good shareholder returns, and self-fund an acquisition, with only a modest increase in net debt.

Paul’s opinion - I think this is an excellent business, and still reasonably priced.

Therefore it has to be another GREEN. I think it could be short-sighted to be banking profits below 300p. If a cyclical recovery starts in the sector, earnings could increase to well over 30p. Put that on a PER of say 12-13, and I’m thinking 360p - 390p looks possible with a say 1-2 year view. Plus a 4% divi whilst you wait. That makes this share remain attractive to me at 265p. Of course, something could go wrong, that’s the risk we take with all equities, but I’d much rather buy or hold something where risk:reward seems to be in my favour, as it looks to be here.

Stockopedia loves it too, so it gets the man+machine thumbs up!

Graham’s Section:

Watches of Switzerland (LON:WOSG)

Up 4% to 394p (£943m) - Trading Update - Graham - AMBER/GREEN

I’ve been mildly positive on this one, given the lower valuation on offer vs. 2022 and the interesting acquisition it made in the United States (see coverage in May 2024).

As a reminder, here is a chart of the company’s share price performance since IPO in 2019:

The bursting of the watch bubble has seen it drop back to cheap multiples:

Today’s update is in line, after the first 18 weeks of the financial year (FY April 2025), and WOSG is confident in the delivery of FY25 guidance.

Key points:

Stabilisation of the UK market in luxury watches and jewellery.

US: performance will be second half weighted (amber flag?).

US: increasing inventory to enhance displays (probably fine, but it will drag on cash).

The acquisition of Roberto Coin is “progressing to plan”. This was an important and large ($130m) acquisition of a jewellery distributor that was already being used by WOSG. So I’m pleased to hear that everything is fine with the integration so far.

Some of the detail on future plans:

Looking ahead, we are working closely with our new colleagues on exciting growth plans for the US market. We intend to grow and develop the Roberto Coin brand and are actively negotiating new mono-brand boutiques in the US, alongside concession models with department store partners. In addition, luxury branded jewellery has also performed well globally, and we are pleased to announce the exclusive launches of David Yurman and Repossi in the UK…

Graham’s view

My mildly positive stance here seems to be working out, in the sense that the company is delivering on its plans and uncertainty is receding. Today they mention “increased certainty on the timing of key showroom projects, and visibility of new product launches”.

All we need now is for Roberto Coin to make a meaningful contribution to profitability, and shareholders should have a pleasant few years to look forward to.

I’ll be watching out for news on the company’s debt levels, as it borrowed to fund the Roberto Coin takeover, and its inventory position in the next results statement.

The company doesn’t pay a dividend (correctly, in my view) and does need to carefully manage its risks as it has financial debt, lease liabilities and a volatile retail market to contend with. But currently, everything is under control.

I’ll leave my stance here unchanged, looking forward to more of the same with the interim results.

Stockopedia’s calculations share my view that this stock potentially offers some value and is worth a second look:

Craneware (LON:CRW)

Up 8.5% to £22.46 (£793m / $1,041m) - FY24 Final Results - Graham - AMBER

Craneware (AIM: CRW.L), the market leader in Value Cycle software solutions for the US healthcare market, announces its audited results for the year ended 30 June 2024.

We covered Craneware’s full-year update in July, when we learned that revenue would beat expectations for the year, and that EBITDA was towards the top end of expectations.

Today we have the complete full-year results statement.

Let’s take a look at some of the key bullet points:

Rev +9% to $189m (slightly higher than the growth suggested in the trading update).

Adj. EBITDA +6% to $58m.

Small increase in ARR to $172m.

PBT +20% to $15.7m.

It was a fine year (and I look forward to chatting with management later this morning); the only stumbling block I’ve had when it comes to the investment proposition here has been valuation. More on that later.

Operational highlights - one of the standout elements here is the strategic alliance with Microsoft, involving collaboration and the sale of Trisus on Microsoft’s Azure Marketplace.

Outlook

Increasing opportunity ahead, including accelerated innovation via the alliance with Microsoft

Momentum has continued post-year end, with good levels of trading and customer confidence, providing the Board with confidence in continued growth momentum for FY25, delivering on current expectations and the sustainable return to double digit growth rates.

In previous reports, I’ve been suggesting that double-digit growth was needed to help support the valuation of this one, and so it’s interesting to see the company specifically mention this as something they are working towards.

Estimates have been published this morning by Capital Access on Research Tree, and they have raised their forecasts on the back of the strong revenue performance and outlook.

Revenue growth was previously estimated at an average of 6% p.a. (from FY24 to FY27), and this is raised to an average of 8.5% p.a. This also flows through to increases in profit estimates; their adj. EBITDA forecast for FY June 2025 is $62.5m.

Peel Hunt have also pushed through some small revenue upgrades.

CEO comment:

"The strong financial results during the year demonstrates the strength of the Trisus platform, our increasing platform partnership successes and the role we play in helping healthcare providers drive for better value in the US healthcare market.

We see increased opportunity ahead. Our alliance with Microsoft will allow us to accelerate innovation and explore new AI-based applications in an efficient manner which, alongside the breadth of the Trisus platform, our unique data assets and our considerable and extensive customer base provides significant scope for expansion in the size of our addressable market…

We have commenced FY25 with a good level of trading, and remain confident in achieving another positive year ahead, growth acceleration over the near term, and our ability to create further long-term value for all stakeholders."

Cash/Debt: I should mention that the company finished the financial year with cash of $34.6m offset by bank debt of $35.4m.

Graham’s view

I’m wondering if I can upgrade my stance here to AMBER/GREEN, on the back of higher revenue growth forecasts.

The share price was soft going into today’s results, but has found some bidding interest this morning:

On valuation, the market cap (which in this instance is the same thing as the enterprise value) gives us the following multiples based on FY25 forecasts:

Price to sales: 5.1x

EV/current ARR (annualised recurring revenue): 6.1x

EV/EBITDA: 16.4x

Adj. PER: 28x

You may agree with me that none of these multiples are screaming “value” but if you do a comparison against the US tech sector/healthcare sector you may find that the valuation starts to make more sense.

I still think that Craneware’s valuation is quite normal for its sector, and that it does have the possibility to outperform given its enormous data set, the potential for 3rd parties to want to work with this data, and the alliance with Microsoft.

If the share price hadn’t jumped higher this morning, I might have switched to AMBER/GREEN, but for now I remain comfortable with AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.