Good morning, it's Paul & Roland on SCVR duty today.

Agenda -

Paul's Section:

Volex (LON:VLX) (I hold) - a reassuring update for FY 3/2022 year end. Ahead of expectations (only slightly for profits). Lots of other positive remarks, including continued ability to pass on higher costs. Supply chain disruption could even be a positive, with customers increasing forward orders for certainty of supply. Even after a 14% rise this morning, this share still looks a bargain to me.

Naked Wines (LON:WINE) - trading update is in line. I'm wary of this business model.

Roland's Section:

Carr's (LON:CARR) - this agricultural feed and engineering business has underperformed the market in recent years but has a strong long-term record. Commodity market conditions put pressure on margins in H1, but this should unwind in H2. A strategic review could result in improved focus and growth potential. I can see decent value potential here.

Severfield (LON:SFR) - the structural steel group appears to be trading well with a strong order book. Full-year results are said to be in line with expectations, although I can’t entirely dismiss concerns about cyclical risks here. Even so, the shares do look decent value to me at current levels.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to

Paul’s Section

Volex (LON:VLX) (I hold)

247p (pre market open)

Market cap £390m

Volex plc (AIM:VLX), the global supplier of integrated manufacturing services and power products, provides the following update on trading ahead of the announcement of the Group's full year results for the 52 weeks ended 3 April 2022 ("the year").

The share price has been relentlessly falling, which of course makes us all worry that things might be going badly. The reason I’ve been fairly comfortable holding Volex, is because the company recently agreed substantially increased bank facilities. That matters, because banks are all over the management accounts, and would not be expected to increase lending if things were going badly. So that was an important sign, that the market seemed to ignore.

Sure enough, things are going well. Today we’re told -

Results ahead of expectations

Volex is pleased to confirm that the Group's revenues and underlying operating profits are expected to be ahead of consensus market expectations1 for the year.

The Group expects, subject to finalisation of the accounts and audit, revenues to be in excess of $605 million (FY2021: $443 million) and underlying operating profit2 to be in excess of $55.0 million (FY2021: $42.9 million).

1. The Company has compiled forecasts from four analysts with current market forecasts for the 52 weeks ending 3 April 2022 for revenue to be in the range of $575.0m to $586.3m, with a consensus of $581.2m, and for underlying operating profit to be in the range of $53.8m to $54.6m, with a consensus of $54.2m.

So before we get too excited, profit is only slightly above expectations. Still, to have achieved that in a time of supply chain turmoil, and heightened inflation, is impressive.

Strong demand -

Volex has continued to trade strongly, delivering robust organic revenue growth, including a significant contribution from the Electric Vehicles sector, where revenue has almost doubled. Demand has increased during the year with greater visibility of forward orders as customers look to secure manufacturing capacity.

That last bit that I’ve bolded sounds highly significant. It sounds as if Volex could be a beneficiary of supply chain problems, in that customers are committing more forward orders. This probably also means Volex has improved pricing power, since customers presumably are more likely to accept price rises, in return for certainty of supply, in a disrupted world.

Inflation - once again, Volex has confirmed that it is successfully passing on cost rises to customers. Management has been telling us this for a while, but again for some bizarre reason, some investors have ignored this, and made the incorrect assumption that Volex must be suffering from higher copper & plastic prices.

Acquisitions - four have been done this year. Volex seems to have a disciplined approach to making acquisitions (not over-paying, and only buying companies that are a good strategic fit).

This should have led to a re-rating for the shares, but in this small caps bear market, the valuation has actually been falling, which doesn’t make sense at all to me.

Directorspeak - sounds upbeat -

Nat Rothschild, Executive Chairman said, "We have delivered an excellent performance in a challenging environment and are now well ahead of the five year plan we set out in October 2019. This is a validation of an effective strategy which has created a resilient and diversified business. We continue to pursue a number of exciting organic growth opportunities, while successfully acquiring and integrating compelling acquisitions, leaving us well placed for the future."

Valuation - many thanks to Singers for crunching the numbers.

I find EPS easiest, which are (converted by me at £1 = $1.30)

FY 3/2021 actual: 23.1p (boosted by an unusually low tax charge)

FY 3/2022 forecast: 20.3p (this should be close to actual, as guidance given today)

FY 3/2023 forecast: 22.2p

FY 3/2024 forecast: 23.8p

Remember that Volex is acquisitive, so these numbers could be boosted with further acquisitions.

Whilst I’ve been typing the above, the market has opened, and Volex has shot up c.14% to 280p, so it makes sense to use 280p as my valuation share price. This gives us a PER of only 13.8 times for the year just finished, FY 3/2022. Dropping to 12.6 for the new year. This is obviously bargain basement territory, and makes this share a clearly attractive buy, even after this morning’s 14% rise. Obviously just my personal opinion.

My opinion - it’s a bargain! That’s assuming you think performance can be maintained. I don’t think we need to worry about cost inflation, or supply chain - Volex seems firmly on top of those issues, and might even benefit from competitors struggling, allowing Volex to expand its margins possibly?

I’m so glad I held the line on this one, and didn’t let fear of further losses induce me to panic sell. We’re in a very difficult market right now. Everything (almost) has dropped a lot, and we simply don’t know if that’s due to deteriorating fundamentals, or just the background noise of nervous holders selling through fear.

Decision-making is particularly difficult for all of us right now.

.

Naked Wines (LON:WINE)

374p (up 13% at 08:31)

Market cap £274m

This is an update for FY 3/2022, from this online wine retailer.

Company headline is -

Performance in-line with expectations driven by Repeat Customer sales, strong retention and demand from existing members

Revenues are only up 3% on LY (5% at constant currency). The suggestion is that demand was pulled forward by the pandemic, hence the 2 year growth rate is much higher, at +72%. I think that’s a fair point, as we’ve heard similar from many other online businesses. The interesting question is what level (if any) growth settles at longer term? Are these online businesses still in structural growth, or have they gone ex-growth? There might be an opportunity in this sector, as valuations of online companies are really bombed out at the moment, yet some might be demonstrating stronger growth next year, against softer comparatives maybe?

Various KPIs are mentioned, but these tend to distract me from matters - is this a viable, scalable business model? The growth potential from the USA looks interesting - obviously a huge market compared with the UK.

Profitability - the story in the past is that WINE has a highly profitable, long-term user base, which is uses to fund expansionary marketing spend. With growth now stalled to a snail’s pace, the jury’s out on that.

Today, it refers to “positive EBIT”, but only in “low single digits”

Balance sheet - a very large increase in inventories, to £143m, up £66m. Cash of c.£40m, presumably some or all of that might relate to customer deposits under the monthly prepayments programme (also used by Virgin Wines Uk (LON:VINO) )

My opinion - I’d need to see the full accounts, to see how it all fits together.

It’s difficult to see why today’s, in line with expectations update would trigger a 13% share price rise today. Maybe it just coincided with people being ready to buy, after a typical big fall which so many smaller companies have seen.

I’m mindful that Netflix dropped 20% after hours yesterday, as subscriber numbers fell. We have to watch out for subscription type businesses that are discretionary spending for their customers. Higher utility bills might make at least a few of WINE’s customers decide to cancel their subscriptions maybe?

Another point to beware of, is that it’s a lot more expensive to recruit new customers now, due to the internet giants grabbing the profits for themselves. Hence I would not be looking to buy into any online, subscription-based business right now.

.

Roland’s section

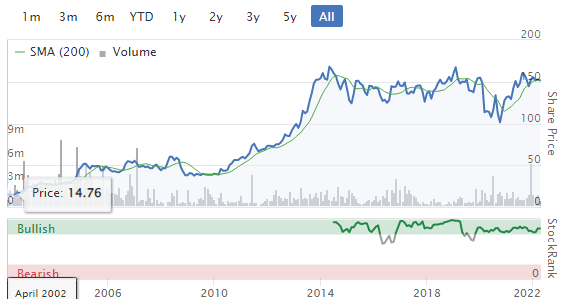

Carr's (LON:CARR)

Share price: 141p (-5% at 08.21)

Shares in issue: 94.0m

Market cap: £144m

“A robust performance in the period with full year expectations unchanged”

This agricultural supplies and engineering group has been a ten bagger over the last 20 years, outperforming the market by a country mile.

However, the stock has gone nowhere since 2014, while profits have also been fairly flat.

Carr’s has some attractive characteristics, in my view. But I see the lack of consistent growth as a potential risk. To consider buying the stock I’d want to see some signs of improvement. Do today’s half-year numbers provide fresh hope?

Note: Rather like Tate & Lyle (LON:TATE) - the former sugar producer - the supermarket bags of flour which bear Carr’s name are not produced by the company. The group sold its food division to Whitworths in 2016, “enabling Carr’s Group plc to focus on high value markets within Agriculture and Engineering”.

Financial highlights

Today’s half-year results cover the six months to 26 February 2022.

Carr’s numbers show strong revenue growth, but flat or falling profits, depending on your preferred measure of profits. This suggests to me that margins have come under pressure, presumably in the agricultural business.

- Revenue +10.6% to £222.7m

- Adjusted pre-tax profit -2.3% to £10.3m

- Statutory pre-tax profit -0.1% to £9.5m

- Adjusted earnings per share -8.4% to 7.6p

- Interim dividend unchanged at 1.175p per share

- Net debt up from £10.6m to £29.9m - a significant increase

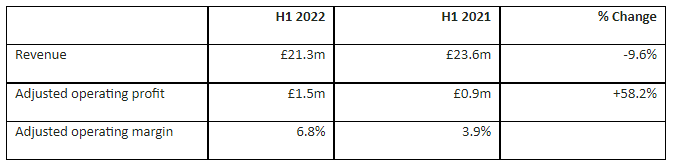

Specialty Agriculture: Sure enough, the commentary flags up a “strong performance in Agricultural supplies despite significant raw material cost increases” (my bold).

A combination of volatile market prices and forward sale agreements meant that increases to sale prices lagged behind rising input costs during the first half. However, “cost and prices have since been brought into line” and the situation has stabilised.

Higher raw material costs are also said to have accounted for the majority of the increase in net debt, as more cash was needed to fund inventory purchases. Carr’s expects this increase to unwind during the second half.

Profits and margins from this business were hit hard in H1, but if the situation does reverse in H2 then this might not be a big concern.

However, the company does warn that there’s some risk to volumes in H2 due to higher prices and drought in some parts of the USA (reducing livestock numbers).

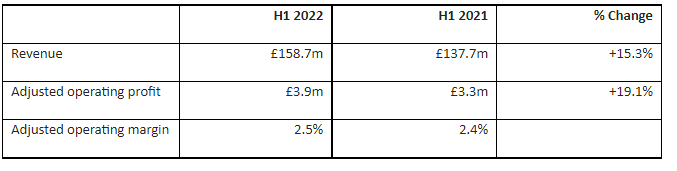

Agricultural supplies: This business generated 71% of revenue, but only 36% of profit during the first half of the year. It’s a low-margin operation, but appears to have traded well during the period

Like-for-like retail sales rose by 4.1%, with total revenue up 15% to £158.7m. This included a new machinery branch opening.

Solid, but unexciting. However, I can see opportunities for incremental growth through bolt-on acquisitions and new branch openings.

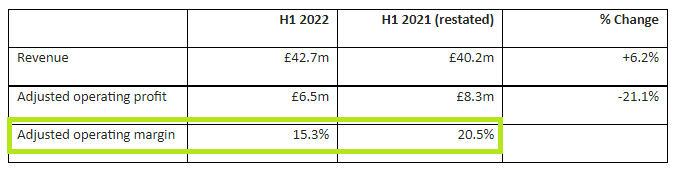

Engineering: Carr’s engineering businesses are focused on specialist steel fabrication, robotics and other engineering solutions for the oil, gas and nuclear energy sectors. They delivered an improved result compared to the pandemic-hit comparative period, but management say performance remained behind expectations.

Note the improved margins:

Checking back to H1 2020, revenue was £24.9m and adjusted operating profit was £1.2m. So the H1 2022 profit performance seems to be an improvement on pre-pandemic levels, too.

Stronger conditions in the oil and gas market are benefiting Carr’s and the company also won a new robotics contract in the USA.

The problem area seems to be the engineering solutions business, which is suffering delays and cost overruns on a defence project.

The order book rose to £44.2m at the end of February, an increase of 13.8% from the year end.

The numbers seem reasonably positive to me, albeit with limited visibility.

Strategic review: In January, Carr’s announced a strategic review of its three divisions to evaluate their growth potential. This is said to be nearing completion.

Balance sheet & profitability: As Paul has noted previously, this is quite a complex and capital-intensive business. Profitability varies widely between the group’s divisions and the balance sheet shows net tangible assets of £104m.

At a statutory level, profitability is low:

- TTM operating margin: 3.0%

- TTM ROCE: 7.3%

The sharp increase in net debt is also a risk, although I think the explanation (working capital linked to higher input prices) is reasonable.

These numbers don’t look too exciting to me. But as a long-term investment, Carr’s has proved a safe home for shareholders’ cash.

There’s also a useful forecast yield of 3.6%, backed by a very solid dividend record:

Valuation: Carr’s has left full-year guidance unchanged today. Based on Stockopedia’s consensus forecasts for earnings of 13.2p per share, that prices the stock on a modest 10.7x forecast earnings.

My view: Carr’s valuation looks very undemanding to me. The shares also offer a useful dividend yield.

Today’s results do flag up some risk factors relating to commodity market conditions and perhaps climate change.

However, Carr’s has been in business for over a century and has been listed on the London market for more than 50 years. It’s survived a variety of difficult conditions and appears to have some attractive operations in engineering and agriculture.

The ongoing strategic review could see the group reshaped to focus on higher growth/more profitable lines of business.

I’d consider Carr’s as a potential long-term value play, for a true buy-and-hold portfolio.

Severfield (LON:SFR)

Share price: 67p (+5% at 09.13)

Shares in issue: 309.5m

Market cap: £199m

“The group expects to deliver a full year result in line with management’s previous expectations.”

Today’s update from this structural steel group covers the year to 31 March and strikes a confident note. I’d guess it should be reassuring for shareholders, who’ve seen the stock fall by more than 15% over the last year.

Severfield’s operations are divided into two geographic divisions, UK/Europe and a joint venture in India. Conditions appear to remain positive in both the group’s main markets, despite some cost pressures relating to Russia’s invasion of Ukraine.

Full-year results are expected to be in line with expectations. According to Stockopedia’s consensus forecasts, this leaves Severfield shares looking potentially good value:

Let’s take a brief look at the commentary from each division.

UK/Europe: Back in November, Jack noted “some signs of customers delaying projects”. There’s no mention of delays in today’s update.

Severfield says that the company secured “a significant value of new work” in H2, resulting in a record UK/Europe order book of £479m at 1 April 2022 (1 November 2021: £393m). £382m is due for delivery over the next 12 months.

The order book is said to be well diversified across the group’s markets, with 96% for projects within the UK.

Management say they’re encouraged by levels of tending activity and are well positioned to take advantage of “some significant opportunities” in markets such as data centres, industrial and distribution.

Cost inflation and higher steel prices are said to be being managed effectively, with steel remaining “largely a pass-through cost for the group”. Although this statement is reassuring, it also makes me wonder whether Severfield’s increased order book may be due in part to higher steel prices, rather than organic growth.

India: Severfield’s Indian joint venture reports big order book numbers, but has not been very profitable historically (2021 share of loss £0.7m, 2020 share of profit £2.2m).

However, today’s update says that the JV is performing profitably and in line with expectations, after a difficult start to the year.

The order book has risen to £166m, from £140m at the start of November. 40% of this total is said to represent higher margin commercial work, with the remainder representing industrial projects.

Balance sheet: Severfield expects to report year-end net debt of £19m, excluding lease liabilities. The group recently refinanced its revolving credit facility, increasing it from £25m to £50m.

My view: Severfield shares look decent value on around eight times rolling forecast earnings, and the forecast yield of c.5% seems safe enough to me at present.

The main risk, in my view, is that we’ll see a cyclical slowdown in some construction markets as rising inflation and higher interest rates dampen growth. However, by targeting a diverse range of projects Severfield may be able to mitigate this risk.

Severfield is still a fairly capital-intensive business, but the long-term average ROCE of 10% seems reasonable to me and the balance sheet looks fine, following a refinancing a few years ago. If market conditions remain stable, then I think Severfield shares could offer decent value at current levels.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.