Good morning from Paul & Graham! Firing on all cylinders again, so let's hope we have some interesting news to cover.

Today's report is now finished.

Agenda

Paul’s Section:

Sanderson Design (LON:SDG) [Quick comment] - 113p (£81m mkt cap) - this is a “reach” (non-regulatory) announcement, of a new licensing agreement with Ruggable (two-piece rugs, with the upper piece being washable - clever idea!) SDG’s William Morris fabric designs will be used. It says this is the “second major” licensing deal in the USA - a key market that SDG wants to aggressively grow into, seeing a big market opportunity there. I reviewed the in line interim results here. As I noted at the time, strong licensing performance is offsetting weaker trading in the main business, which if it continues, could help SDG get through this recession.

My view remains positive on SDG shares - it’s easy to imagine this share being double the current valuation once the economy has returned to normal. Between now and then, there’s obviously the risk of a profit warning, and the company has previously indicated a wide range of outcomes is possible, shorter term. Balance sheet is bulletproof, so no risk of dilution or insolvency, hence it's a good long-term hold I think, if a potential dip shorter term doesn't worry you. Maybe one to take a small position in, and keep some cash on the side to top up on a warning (which may or may not happen), I was thinking.

WANdisco (LON:WAND) [Quick comment] - 900p (£621m mkt cap) - here’s an interesting share, that has soared in the last 6 months. We flagged here on 28 June that a big contract win was starting to look interesting, although the results announced on 15 June were dreadful. The key “tell” that something interesting was afoot (with hindsight) was that it got away another fundraise in June, at a premium, despite reporting terrible numbers. Afterwards, a series of big contract wins were announced. That was the turning point, it's tripled in price since then. So we’ll have to take a closer look at any more companies that look basket cases, but successfully raise fresh equity without having to offer a discount, as that suggests instis are being privately told that there’s a very positive outlook, and believe it to be real. Yesterday saw another deal announced, $31m, with half paid up-front. This reinforces my view that something very interesting seems to be happening at WAND.

Tremor International (LON:TRMR) [Quick comment] - Up 9% to 300p - mkt cap £433m - Sky News says that TRMR has appointed Goldman Sachs, to try to sell the company. That could make sense, as it’s become obvious that stock market investors don’t trust the company and its figures - otherwise it wouldn’t be trading on a forward PER of 4. I’ve never understood the business model, so generally avoid trying to write anything about it. Graham reviewed it here in August, flagging up various issues. The Director dealings page doesn’t suggest they’re bullish about the company with their own money. Major shareholders look interesting, including a Saudi family office owning 24%, Toscafund on 15.5%, and News Corp at 5.9%. Interesting that its excessive share options scheme has been challenged by shareholders recently. My view - no idea, I can’t determine if it’s good or bad, so I’ll steer clear.

Xeros Technology (LON:XSG) [Quick comment] - one of many dismal, jam tomorrow companies on AIM. Mkt cap is now only £6m, but you can now buy at 3.8p, below the 5.0p price of a recent fundraising, which replenished the coffers (for now). An update today says its Indian partner is shortly to launch domestic washing machines using XSG’s technology. Trials of larger washing machines are also underway. “Financial guidance remains unchanged” - it’s previously said targeting breakeven by 2024. Cash burn this year has been high, and revenues so far negligible. So this is high risk, but could be a speculative multibagger if sales take off - chances of that happening? Slim, I would say! If it needs to raise cash again, we could be looking at a wipeout like at TWD. So it looks very high risk, but very occasionally something like this does pay off. Looks like Canaccord (very shrewd small cap investors) like it, with a 14.3% recently bought stake. Might be worth a flutter, with money we can afford to lose?

Purplebricks (LON:PURP) [Quick comment] - here’s an interesting development, on a slow news day. Shareholder Lecram Holdings requisitioned an EGM, to attempt removal of the Chairman, Paul Pindar. The result came out 2 days ago, and was 28.3% in favour of Pindar’s removal, and 71.7% against. So it failed, but a 28.3% yes vote is significant, which the company acknowledges in its comments. The new CEO says she recognises that “past performance has not been good enough”, and reckons that FY 4/2023 results “will be clear for all to see… substantially improved cash and profit performance”. Cost base has been reduced by £17m. My view - PURP still has cash in the bank, and the latest CEO’s comments today do suggest that it has made some progress. The £29m mkt cap is well supported by £31m net cash at Oct 2022. Positive cash generation guided in early FY 4/2024. Worth a speculative dabble possibly at 9.2p per share?

Graham's Section:

Insig Ai (LON:INSG) (£17m) - looking at this share for the first time, it has applied so-called “machine learning” techniques to improve and automate the ESG process for fund managers. They have enjoyed success with at least one asset management company agreeing to pay a long-term revenue stream to Insig AI. This deal, it is thought, combined with other sales opportunities, will lead to Insig AI being cash flow positive from next summer. However, the stock remains extremely high risk and is surviving now only thanks to convertible loans provided by two individuals (including the Chairman) and shares that have been gifted to it by a pair of directors. (More detail below)

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Graham’s Section:

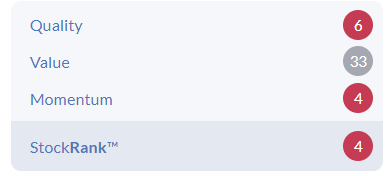

Insig Ai (LON:INSG)

Share price: 16.5p (unch.)

Market cap: £17m

This describes itself as “the data science and machine learning solutions company serving the asset management industry”.

It is yet to achieve much from a financial point of view:

Let’s quickly look over Monday’s interim results to September 2022, to see if there are any green shoots.

- Revenue: £950k (last year: £900k)

- Operating loss: £2.6m (last year: £500k)

Unfortunately, there are good reasons why this one is categorised as a Sucker Stock:

The Chairman’s statement is crammed with jargon and buzzwords. The main achievement of the company, it seems, has been to build:

…a repository of machine learning ESG company disclosures on more than 2,500 global businesses. Our database now encompasses all constituents of the S&P 500, the STOXX 600 and the FTSE 100/250/350 together with hundreds of non-listed corporates.”

These “ESG diagnostics”, it is thought, will enable fund managers to demonstrate objective compliance with their ESG mandates.

Funding - the company is expecting to be cash flow positive from Q2 2023, as it has a long-term revenue agreement with a customer that is tied to that customer’s AUM.

For now, it is surviving on convertible loans from the Chairman and another shareholder.

In addition, the company has today been gifted shares worth £1.1m by two of its founding Directors. This is a very rare event, in my experience! If you want to interpret it positively, you can see it as a reflection of the commitment of the Directors to see this company through to success.

Alternatively, you can see it as a sign that the convertible loans aren’t enough, and the company is living on fumes.

Outlook

Last month, we set out that we had prioritised and accelerated the timeline to expected profitability of the Group. This was underpinned by our expectations for the receipt of recurring revenues from sharing of management fees. Substantial investment over the last 18 months should result in payback with these revenues expected to commence next summer. Over subsequent quarters, these should grow substantially.

My view

I must admit I’m intrigued by the company’s claims that it will be cash flow positive from next summer. Watch this space, maybe?

If it’s true that they can automate the ESG process for fund managers, then in principle that is something I can see the value in.

Objectively speaking, however, this stock is clearly very high up on the risk spectrum and is not a “value” share. It will be a tremendous achievement if they can avoid diluting shareholders.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.