Hello! Graham here with my annual round-up of investment ideas.

This is going to be split into two parts.

First, I’m going to do a review of the ten ideas mentioned in last year’s article (published on January 16th 2023, but using ideas from SCVRs in the latter half of 2022).

After that, I’ll do an article with my ten ideas for 2024.

I’m hoping that there will be plenty of overlap between the two articles!

But let’s start with a review of my ideas for 2023.

A G Barr (LON:BAG)

Total return for 2023 : -1.3%.

Market cap: £579m.

This Scottish soft drinks maker saw its share price drift lower at the start of the year, but it recovered in the second half with an upgrade to profit forecasts (in August) and then a robust “in line” trading outlook in September.

In October, it announced the £12m purchase of the soft drinks brand Rio. Barr already owned the exclusive licence to sell this brand.

So where do we go from here?

I’ve been positive on this share throughout 2023, pointing to its cash balance (last seen at £47m, July 2023, before the Rio acquisition), consistent performance during the Covid era, and strong revenue growth from price increases and acquisitions.

Barr does face an ongoing challenge to rebuild margins - its recent Boost acquisition instantly lowered company margins which were already under pressure.

The deposit retention scheme is also a concern - it will be implemented around the UK in c. 2025.

However, I remain stubbornly positive on this one.

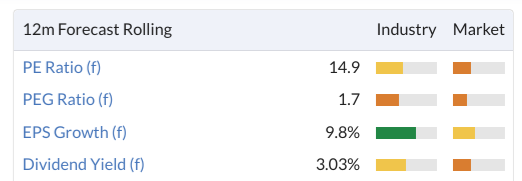

When I wrote last year’s article, Barr was trading on a P/S multiple of 2x, which I said was “not high in the context of the last ten years”.

The price to sales multiple is now only about 1.6x, and the other value metrics remain interesting:

Therefore while acknowledging that the company faces sector challenges, my positive stance here remains unchanged!

Nichols (LON:NICL)

Total return for 2023 : 8.9%.

Market cap: £431m.

Based in North-West England rather than Scotland, this is another old soft drinks company that seems to be consistently worth a look for small-cap investors. The flagship product is Vimto.

It faces many of the same issues as A.G. Barr. As with Barr, its operating margin has failed to recover back to where it was several years ago. Inflation is a major culprit, along with its offspring in the form of the cost-of-living crisis.

Here is the Nichols margin from 2017 to 2022:

We covered the interim results in July. Nichols reported a cash balance of £56m (more than 10% of the market cap), and a slight improvement in its pre-tax profit margin.

I’m remaining positive on this one - my thesis has been that inflation will progressively feed through to selling prices, allowing Nichols to improve its performance. On top of that, the cost-of-living crisis and its depressing effects on consumer spending must end, sooner or later. So for a patient investor who is willing to wait out the economy, this seems to be worth a second look.

With UK inflation now running at only 3.9% (above its long-term average but still much lower than it was a year ago), I’m optimistic that we can see normal profit performances at the drinks companies before too long. We have already seen inflation fall dramatically in the US and elsewhere.

The market shares my optimism, awarding Nichols a premium earnings multiple. I’m happy to keep my positive stance here unchanged:

Peel Hunt (LON:PEEL)

Total return for 2023: 34.1%.

Market cap: £127m

This boutique investment bank is currently loss-making, as it waits for better times in the equity markets.

We recently (December) covered its interims. It didn’t quite manage a breakeven result, which is what I look for from this sector. But it was close: the pre-tax loss was £0.8m. So a breakeven number for the full year remains just about possible.

Net assets are also holding steady, last seen around £93m, and providing plenty of asset backing to support the current market cap.

Peel Hunt’s research is highly regarded and in better times, I expect the company to be highly profitable.

Note that it cleverly IPO’d during the Covid boom, raising tens of millions of pounds at 228p.

Revenues were nearly £200m in FY March 2021, versus only c. £85m in the current year.

At less than half its IPO price, I think it continues to offer value investors a tempting way to bet on a recovery in small-cap and growth markets.

Numis (LON:NUM)

Total return for 2023 (until October): 79.6%.

Takeover value: £410m

This was a win as Deutsche Bank noticed the value on offer at Numis. A recommended cash offer was announced in April at 350p per share (including dividends). The deal was completed in October.

Cavendish Financial (LON:CAV)

Total return for 2023 year-to-date, including dividends: 2.5%.

Market cap: £39m

This was previously known as finnCap, but after the merger of equals with Cenkos, it trades under a new name.

Cavendish Financial is the #1 AIM broker with around 220 quoted clients.

Unfortunately, conditions on AIM have remained drought-like with few IPOs and few fundraisings as investor appetite remains extremely cautious. (After the calamitous series of IPOs that hit the market in 2021, I can hardly blame investors for not wishing to get burned again!)

We very recently covered interim results from Cavendish (December). The company reported having already unlocked £7m of cost synergies, along with an improved cash balance of £17m.

The market cap here has bounced in recent weeks but the enterprise value is still only c. £22m, or three times the cost synergies achieved by the merger! So if the AIM market ever achieves its prior popularity, the profit opportunity for Cavendish and its shareholders should be tremendous.

Mercia Asset Management (LON:MERC)

Total return for 2023 year-to-date, including dividends: minus 2.9%.

Market cap: £132m

This is a regional asset manager, investing in small and medium-sized enterprises.

I thought it was simply “too cheap” a year ago, but the market doesn’t agree with me yet.

A prestigious stock screen does agree with me, for whatever that’s worth:

Again, we have a recent report to which we can direct you: Mercia posted interim results in December.

Net assets on the balance sheet are still 50% above the current share price (45p vs 30p).

The company’s cash balance rose to £60m following the sale of one of its portfolio businesses, covering nearly half of its market cap and giving more certainty to NAV.

Given the excess cash balance, a £5m share buyback is now underway.

Mercia's strategic focus now is on 3rd party fund management, and it might sell more of its portfolio businesses to fund bolt-on fund management acquisitions.

Recent profitability has been unexciting but in these difficult conditions, I think that’s understandable (e.g. negative movements in the value of Mercia’s portfolio businesses flowing through its P&L). If you are willing to take the company’s adjustments at face value, then H1 operating profits were very encouraging at £5.5m.

The year has been a good one for Mercia and its shareholders, I think - a positive change in strategy, a big disposal boosting the cash balance, and a buyback. I’ll stay positive on this one.

S&U (LON:SUS)

Total return for 2023: 10.9%.

Market cap: £264m

I’m a long-term fan of this family-controlled hire purchase lender which also runs a property bridging business.

However, I recently (December) became spooked by the announcement that a Skilled Person Review was happening - a regulatory event that happens after a company comes to the attention of the FCA.

This type of review has been very problematic for another stock I’ve been positive on (Jarvis Securities (LON:JIM) ).

Not wishing to be stung twice by the same bee - even if I think that S&U should pass this review with flying colours - I’ve therefore switched to a neutral stance on this share. However, I acknowledge that this may be overly cautious and you can read counter-arguments in the comments section to the December 12th SCVR. I will probably turn bullish on this stock again, once there is a little more certainty in the outlook (both from an economic and a regulatory point of view),

For now, I note that while collections in hire purchase and repayments in property bridging are both said to be ahead of budget, there are signs of increased defaults and the Chairman seems to be even more bearish and exasperated than usual.

Mortgage Advice Bureau (Holdings) (LON:MAB1)

Total return for 2023 year-to-date, including dividends: 60%.

Market cap: £459m

The mortgage market was of course a hot topic during a year of rising interest rates and affordability issues for house buyers. Fortunately I stayed positive on this one in July despite a wobbly outlook statement. Shareholders have been rewarded in the latter half of the year with a surge in this company’s share price.

Interim results, published in September, confirmed that revenues were up 22% thanks to acquisitions, with organic growth of just 1%. Lower-margin refinancing deals became a majority of the loans arranged by MAB, and MAB outperformed the wider market, growing market share.

Statutory pre-tax profit for the six-month period was £7.6m, down from £10.1m in the prior year. Not bad considering the “extreme market conditions” (MAB’s words) seen in H1.

I continue to view this as a high-quality franchise business with good long-term potential. Acquisitions such as Fluent Money (75% stake bought for £73m) should provide a very helpful boost to profits when the mortgage market booms again.

While I am inclined to maintain my positive outlook on this stock - consistent with “letting my winners run” - I must conceded that it no longer offers the tremendous value that it did a year ago.

MS International (LON:MSI)

Total return for 2023 year-to-date, including dividends: 34%.

Market cap: £146m

Long-awaited confirmation of production order contracts for the US Navy have been announced by this engineering company - see our recent SCVR in December.

Net cash remains very strong and is still a significant chunk of the market cap at £50m.

It’s important to bear in mind that MSI has the culture and governance style of a private company. When I look at their homepage, I am strongly reminded of the Berkshire Hathaway page - these are not people who are interested in promoting their stock in the conventional way!

Given the strong momentum in profitability and the likelihood of continued improvements from the US Navy contracts, I’ve stayed positive on MSI, though it also does not offer the same value that it did a year ago.

Trustpilot (LON:TRST)

Total return for 2023 year-to-date, including dividends: 53.9%.

Market cap: £617m

The bull thesis has been playing out with this one as revenues continue to surge (up 18% in H1, as we reported here) and Trustpilot’s competitive position seems to be stronger than ever.

I’ve been positive on this one due to its fast growth, the apparent absence of significant competition (Google Reviews being a poor alternative), and a valuation that appeared to lag the multiples awarded to US software companies.

This is despite Trustpilot being, in my opinion, a better-than-average quality online platform.

The company hasn’t reported any statutory profitability yet, but is close to doing so (the net loss in H1 was only $2.5m).

Also, the net cash balance as of June 2023 was $83m, while annualised recurring revenues increased to $180m.

With a market cap equivalent to about $790m, that means we now have an EV/ARR multiple of about 4x. That’s significant progress from the 2.3x multiple I calculated in last year’s article, but still nothing to write home about - many US software companies trade at more aggressive multiples than this. So I’m still positive on Trustpilot.

Performance numbers

- AIM All-Share Index in 2023 year-to-date (excluding dividends): minus 8.1%

- FTSE All-Share Index in 2023 year-to-date (including dividends): 7.9%

- Average return of my 10 ideas for 2023 (including dividends): 28.0%*

*Numis was not held for the entire year, as the shares were suspended in October on completion of its takeover.

I hope you've found this interesting! I will shortly publish my 2024 list, which I expect to include several shares from the 2023 list.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.