Interim results for six months ended 31 March 2026

9 June 2026

Asia Strategic Holdings Ltd.

("Asia Strategic", the "Group" or the "Company")

Interim results for the six months ended 31 March 2026

The Board of Asia Strategic Holdings Ltd. (LSE: ASIA), an independent developer and operator of consumer businesses in Emerging Asia, is pleased to announce its unaudited interim results for the period ended 31 March 2026 ("6M26").

Financial Highlights

All data for the reporting period refer to the six-month financial period from 1 October 2025 to 31 March 2026 ("6M26") and the Group's financial year ended 30 September 2025 ("FY25"), unless otherwise stated. The comparative six-month financial period from 1 October 2024 to 31 March 2025 is referred to as "6M25".

The year-on-year ("YOY") growth or decline refers to any change that occurred between 6M26 and 6M25, or equivalent periods of one year, as applicable.

All figures are reported in United States Dollars ("$"), unless otherwise specified.

All data pertaining to the student numbers across the report, including tables and charts, are rounded to the nearest ten for clarity and presentation purposes.

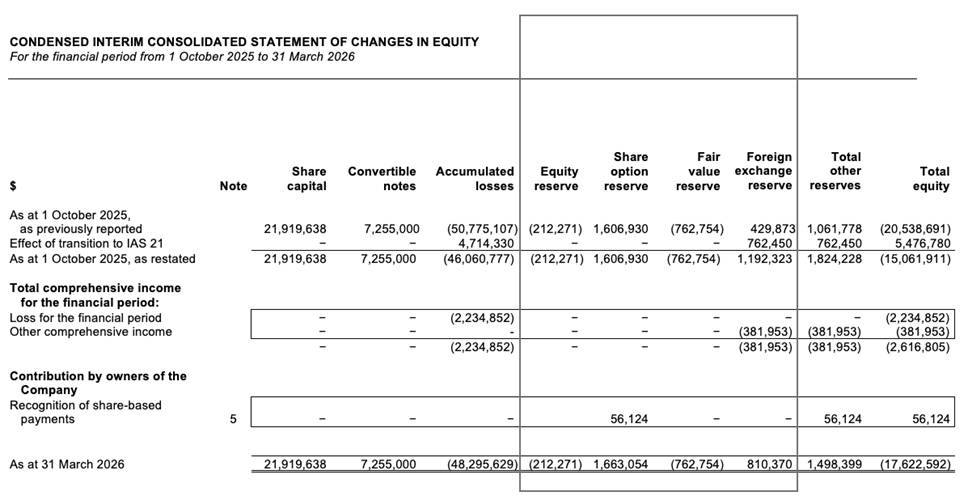

The Group adopted the amendments to "IAS 21: Lack of Exchangeability" from 1 October 2025, applying a market-based exchange rate for the Myanmar Kyat ("MMK") that more closely reflects prevailing conditions. The daily spot exchange rates applied during 6M26 ranged from MMK 3,600 to MMK 3,650 per USD with reference to the market trading rate published by the Central Bank of Myanmar ("MTR"), compared to the reference exchange rate ("RER") published by the Central Bank of Myanmar rate of MMK 2,100 (FY25: MMK 2,100). This change has materially reduced the MMK-denominated revenue, assets and liabilities reported in USD for the Myanmar operations of the Group, despite continued growth in local currency terms, while at the same time materially impacting the realised foreign exchange loss. In accordance with the transitional provisions, comparatives have not been restated. As at 1 October 2025, the cumulative effect of IAS 21 has been recognised in opening accumulated losses and in the foreign currency translation reserve (Refer to Note 2 of the financial statements for further details).

• Group revenue declined 18% YOY to $13.1 million in 6M26 (6M25: $16.0 million), primarily reflecting the IAS 21 translation of MMK-denominated revenues at the MTR. The Education division accounted for 77% of revenue (6M25: 79%), while Services contributed 23% (6M25: 21%). Key revenue movements included:

◦ A 24% decline (22% increase based on RER) in Myanmar's Education division (6M25: 27% increase), driven by contributions from newly launched brands and the continued scaling of existing operations;

◦ A 13% decline (24% increase based on RER) in the Services division (6M25: 2% decline), reflecting the replacement of large USD-denominated contracts by MMK-denominated ones, and the non-renewal of certain risk reporting contracts as the security situation gradually improved; and

◦ A 10% decline in Vietnam's Education division (6M25: 4% decline) driven by a weaker commercial performance at Wall Street English Vietnam. There was a partial offset due to 32% growth at Kids&Us Vietnam and 70% growth at Logiscool Vietnam, although off a smaller base.

• Group gross profit declined 17% YOY to $7.8 million in 6M26 (6M25: $9.4 million), with the Education division contributing 93% (6M25: 94%) and the Services division 7% (6M25: 6%). Gross profit margin remained consistent at 59% (6M25: 59%), supported by an improvement in the Education division's gross margin to 72% (6M25: 70%), reflecting efficiency gains from maturing schools and improved cost management, whilst being partially offset by a marginal decline in the Services division's gross margin to 17% (6M25: 18%) amid pricing pressure in Myanmar.

• The Group recorded a reduced net loss of $2.2 million in 6M26 (6M25: $3.7 million loss). The improvement was supported by a $0.4 million foreign exchange gain (6M25: $1.3 million loss) and a 13% reduction in administrative and other operating expenses to $9.6 million (6M25: $11.1 million), partially offset by a $0.9 million loss allowance on trade and other receivables relating to an affiliated entity (Refer to Note 12).

• Adjusted net losses, excluding the $0.9 million loss allowance on trade and other receivables, were $1.3 million (6M25: $3.2 million adjusted loss, excluding the plant and equipment write-off). The reduction of adjusted net losses reflects the evolution of the Group's new businesses and the ongoing cost optimisation at Wall Street English Vietnam.

• Group adjusted EBITDA was $1.3 million in 6M26 (6M25: $0.3 million LBITDA), a significant achievement in the Group's history, driven by improved operating performance across the Education division and cost reduction initiatives.

• At 31 March 2026, deferred revenue, representing cash received in advance of remaining performance obligations, was $14.5 million, of which $10.7 million was current (1 October 2025, as restated under IAS 21: $10.4 million), and $3.8 million was non-current (1 October 2025, as restated under IAS 21: $2.8 million). On a like-for-like basis against the restated comparatives, current and non-current deferred revenue grew 3% and 34% respectively, reflecting healthy advance bookings particularly across Auston and the franchised brands in Myanmar.

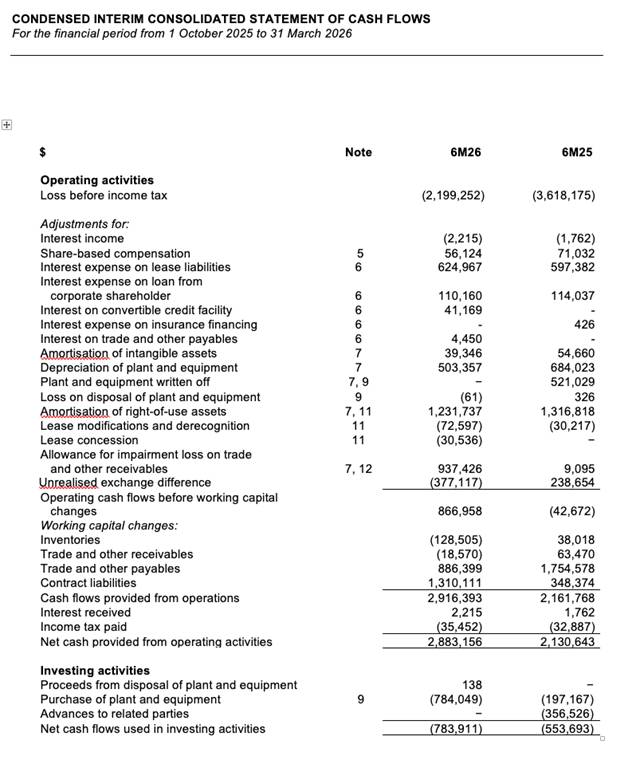

• The Group reported a positive operating cash flow of $2.9 million (6M25: $2.1 million), driven by increased advance payments in the Education division. If repayment of lease liabilities (including principal and interest) were considered, the Group would have recorded a positive adjusted cash flow of $1.0 million (6M25: positive $0.3 million). This improvement reflects a more efficient cash conversion cycle and disciplined working capital management. In parallel, the Group adopted a more strategic approach at Wall Street English Vietnam, implementing targeted cost reductions and commercial adjustments to support its pathway to profitability.

• The Group invested $0.8 million in capital expenditure in 6M26 (6M25: $0.2 million), focusing on two new Kids&Us schools in Vietnam, the expansion of the Yangon American Bahan and Auston Yangon campuses, as well as the renovation of the Auston Mandalay campus post-earthquake in Myanmar in March 2025.

• The Group maintained a $4.5 million loan facility (the "Loan Facility") with MACAN, the Group's largest shareholder. No additional drawdowns were made during 6M26. As of the report date, $0.8 million of the facility remains available.

• Diversification of the Group's operations across multiple countries continues to play an important role in mitigating single-country risk. Management has determined that there are sufficient mitigating actions within the Group's control to ensure liquidity for at least the next twelve months from the date of this report.

Operational Highlights

Education

• Revenue from Education businesses declined 20% YOY to $10.1 million in 6M26 (6M25: $12.6 million), primarily reflecting the IAS 21 translation of MMK-denominated revenues. The Myanmar Education brands grew 22% YOY (excluding Yangon American) in local currency terms.

• At 31 March 2026, deferred revenue from Education businesses, representing cash received in advance of service delivery, comprised:

◦ Current: $10.4 million (1 October 2025: $10.1 million, as restated under IAS 21).

◦ Non-Current: $3.8 million (1 October 2025: $2.8 million, as restated under IAS 21).

• The Education division operates across Vietnam and Myanmar:

Brand

Type

Description

Vietnam

Myanmar

Wall Street English

Franchised

English language education for adults

✓

✓

Kids&Us

Franchised

English language education for children and teens

✓

✓

Logiscool

Franchised

Digital literacy, technology, and coding for children and teens

✓

✓

Yangon American

Owned

K-12 international school

-

✓

Auston

Owned

Tertiary education

-

✓

The number of schools and students at the end of each period were:

Number of Schools

Number of Students

31 Mar 2026

30 Sep 2025

31 Mar 2025

31 Mar 2026

30 Sep 2025

31 Mar 2025

Vietnam

17

16

15

4,860

4,610

4,530

Wall Street English

7

7

7

3,410

3,320

3,450

Kids&Us¹

7

6

6

1,290

1,130

970

Logiscool¹

3

3

2

160

160

110

Myanmar

20

19

17

6,110

5,800

5,380

Wall Street English

5

5

6

3,200

3,290

3,170

Kids&Us¹

4

4

3

780

610

490

Logiscool¹

6

6

4

1,100

850

620

Yangon American

3

2

2

200

190

180

Auston

2

2

2

830

860

920

Group

37

35

32

10,970

10,410

9,910

# of Students Studying Online

1,630

1,600

1,820

¹ New schools opened since 1 April 2026: 1 Kids&Us Vietnam. Schools in the pipeline (i.e., lease agreements signed and under construction) at the reporting date: 1 Logiscool Vietnam, 2 Kids&Us Myanmar, and 2 Logiscool Myanmar.

Vietnam

Total students increased by 5% compared to 30 September 2025, predominantly driven by the increase in Kids&Us.

• Wall Street English Vietnam: Total number of students increased slightly to ca. 3,410 at 31 March 2026, with commercial performance remaining subdued. One centre was relocated to a more cost-efficient location during the period. In response to a continued shift towards online preferences, the Group adjusted staffing, restructured service teams, and recalibrated its commercial strategy.

• Kids&Us Vietnam: Growth continued with financial and operational metrics largely meeting expectations. Student numbers grew 14% to ca. 1,290 at 31 March 2026, driven by stabilising retention rates and the opening of new schools. The Group advanced its growth agenda by refining its site selection strategy and focusing on smaller spaces, while maximising class sizes, optimising space utilisation, and improving margins. Further expansion is planned for 2026, including the potential entry into Hanoi.

• Logiscool Vietnam: Student numbers were broadly stable at ca. 160 at 31 March 2026, as growth was stagnant due to subdued sales at schools in secondary locations. With new leadership installed and planned co-location within existing Kids&Us sites in central areas, performance is expected to improve in the second half of FY26.

Myanmar

The number of students increased by 5% compared to 30 September 2025, driven by growth across all brands except Wall Street English Myanmar.

• Wall Street English Myanmar: Price increases, implemented to hedge against market risks, helped offset the modest decline in student numbers to ca. 3,200 at 31 March 2026. Affordability concerns and increased emigration remain key challenges.

• Kids&Us Myanmar: The business remained resilient, with student enrolment growing 28% to ca. 780 at 31 March 2026, supported by robust demand for early childhood English education. One school is currently under construction, and two additional schools are in the pipeline.

• Logiscool Myanmar: Student enrolment grew 29% from 30 September 2025 to ca. 1,100, representing the strongest student growth rate across the Group's franchised businesses. The commercial success was driven by an experienced commercial team, a strong product offering, and limited competition. One school is under construction and one more is in the pipeline.

• Yangon American: Student enrolment grew to ca. 200 at 31 March 2026. A key milestone in 6M26 was the opening of the new Bahan campus in central Yangon in January 2026, bringing secondary students to a dedicated campus in central Yangon. Yangon American also achieved IB Middle Years Programme ("MYP") authorisation during the period, making it the only IB Primary Years Programme ("PYP") and MYP authorised school in the Myanmar market.

• Auston: Student enrolment was ca. 830 at 31 March 2026, a decline from ca. 860 at 30 September 2025, driven by increased migration and conscription-related uncertainty. Auston signed academic partnership agreements with the University of Wolverhampton in December 2025 and University College Birmingham in February 2026, ensuring continuity and expanded pathways for students. Auston is pursuing an ambitious expansion of its Yangon campus facilities.

Services

• Revenue from Services businesses decreased 13% YOY to $3.0 million in 6M26 (6M25: $3.4 million), reflecting the replacement of certain USD-denominated contracts by MMK-denominated ones, and the non-renewal of certain risk reporting contracts as the security situation improved.

• At 31 March 2026, current deferred revenue from Services businesses, representing cash received in advance of service delivery, was $0.3 million (1 October 2025, as restated: $0.3 million).

• EXERA Vietnam: EXERA Vietnam was launched in FY24 to provide integrated facility management services and generated $29k revenue in 6M26 (6M25: $22k). The business remains an early-stage start-up and is exploring strategic partnerships to increase market penetration.

• EXERA Myanmar: Revenue declined 13% YOY in USD terms to $3.0 million in 6M26 (6M25: $3.4 million). EXERA Myanmar's contracts are denominated in multiple currencies; the decline was partially attributable to a growing proportion of MMK-denominated contracts and the related foreign exchange impact, as well as a net reduction of certain large accounts in a price-sensitive market. EXERA Myanmar employed ca. 2,280 service personnel (comprising primarily of security officers and FM staff) as of 31 March 2026 (30 September 2025: ca. 1,930) across ca. 280 sites in Myanmar (30 September 2025: ca. 250 sites).

SIGNIFICANT AND SUBSEQUENT EVENTS

1) Myanmar general election and political transition

Myanmar held a three-phase general election in December 2025 and January 2026, administered by the Union Election Commission. The Union Solidarity and Development Party secured an overwhelming majority across both chambers of the national legislature and was inaugurated in April 2026. While the completion of the electoral process has introduced a degree of political clarity that the Group cautiously views as a notable development for the operating environment, the transition does not in itself resolve the underlying structural challenges facing Myanmar's economy, including ongoing conflict in parts of the country, constrained FDI, and consumer price pressures. The Group continues to monitor the situation closely and will adjust its operational posture as circumstances evolve.

2) Impact of the Myanmar earthquake

One year after the devastating 7.7 magnitude earthquake that struck central Myanmar on 28 March 2025, recovery efforts have progressed meaningfully but remain fragile. According to the International Federation of Red Cross and Red Crescent Societies, more than 300,000 people have been assisted across earthquake-affected areas with shelter, essential items, and economic support, though thousands of families continue to face challenges accessing stable shelter, safe water, and sustainable livelihoods. Humanitarian organisations have transitioned from emergency relief to early recovery, including infrastructure restoration and livelihood support.

The Group is pleased to report that reinstatement works across its affected Mandalay premises, encompassing Wall Street English, Logiscool, and Auston, have been completed, and the Group has successfully resumed in-person operations at these sites.

3) Global macroeconomic and geopolitical uncertainty

The global macroeconomic and political environment has evolved considerably over the last few months. The escalation of the Iran conflict and the resulting tightening of global oil supply remain the most immediate sources of macroeconomic risk, with the disruption around the Strait of Hormuz elevating energy prices and weighing on import-dependent economies. Compounding this, political turmoil has resurfaced across multiple major economies, with contested elections, leadership transitions, and protectionist trade measures introducing renewed uncertainty into capital flows and consumer sentiment globally. The residual US tariff measures introduced in April 2025 have moderated through subsequent US-China de-escalation and the US-Vietnam Reciprocal Trade Framework, but the broader trade environment remains uneven, and tariffs are now considered a structural feature rather than a transitory shock. Spillover effects from higher energy prices, supply chain reconfiguration, and slowing growth in China and the EU are gradually filtering through to emerging markets, including via softer external demand and tighter financing conditions. In Vietnam, the trade outlook remains relatively constructive, anchored by stable bilateral arrangements with the US and continued FDI momentum, although exporter margins are likely to face pressure as the year progresses.

The broader Southeast Asian outlook is more moderate as the World Bank now expects regional growth to slow to 4.2% in 2026 from 5.0% in 2025; however, Vietnam continues to be among the better-positioned economies in the region. The Group has no direct exposure to the United States, and the direct impact of the residual tariff measures on its operations remains limited. It continues to exercise prudence in capital expenditure planning and to optimise its cost base in response to the evolving macroeconomic backdrop.

COUNTRY ECONOMIC UPDATES

The most recent forecast by the Asian Development Bank ("ADB") is for developing Southeast Asia's GDP growth of 4.7% in 2026. Inflation in developing Southeast Asia is expected to rise to 3.2% in 2026, up from 2.3% in 2025, driven by strengthening domestic demand and higher energy prices linked to the Middle East conflict.

Vietnam

The years stated below refer to the calendar year, which runs from 1 January to 31 December unless otherwise stated.

• According to the General Statistics Office of Vietnam ("GSO"), GDP growth for Q1 2026 was 7.8% YOY, the fastest Q1 growth since 2018, exhibiting strong economic fundamentals and a sustained long-term positive outlook. The full-year 2025 GDP growth was 8.0%, while the ADB forecasts 7.2% growth in 2026. Average CPI for March 2026 increased by 4.7% YOY, while education CPI rose by 3.3%, providing ca.135 basis points of defensible pricing room for education operators. Key inflation drivers included rising costs in education, transportation, food & beverage, and housing.

• Vietnam's exports in Q1 2026 are estimated at $126.6 billion, while imports reached $112.9 billion. The US implemented a 20% reciprocal tariff on Vietnamese imports, locked in through Executive Order 14257 of April 2025, and remains a structural H2 risk. However, the US-Vietnam Reciprocal Trade Framework signed in October 2025 has stabilised the picture, and the bilateral relationship continues to evolve constructively. The most disruptive scenarios have not materialised to date.

• Vietnam's industrial sector continued to strengthen in Q1 2026, with the Index of Industrial Production rising 9.0% YOY, according to the GSO. Meanwhile, Vietnam's S&P Global Manufacturing PMI stood at 51.2, remaining in expansion territory, though the trajectory has moderated from the highs of H2 2025. Manufacturing sub-sectors with relevance to the Group's services operations continued to perform strongly, including motor vehicles (+14.7%), chemicals (+18.2%), and iron and steel (+22.9%).

• Vietnam maintained strong foreign direct investment ("FDI") momentum. In Q1 2026, newly registered FDI was $17.9 billion, with Thai Nguyen alone attracting $5.4 billion through the Samsung ecosystem. Realised FDI of $5.0 billion continued at pace. Public investment disbursement reached VND 110.3 trillion, up 37% YOY, supporting infrastructure capacity and the Long Thanh Airport Phase 1 opening in June 2026. FDI is concentrating in the northern corridor, with Thai Nguyen ($5.4 billion), Nghe An ($2.3 billion), and Bac Ninh ($358 million) among the top recipients. Singapore ($5.3 billion) and South Korea ($3.7 billion) were the largest source countries of FDI.

• The Vietnamese Dong depreciated ca.1.5% YTD against the USD, with the spot rate at ca.VND 26,340 at 31 March 2026, managed within the State Bank of Vietnam's ±5% band. System credit growth of 3.2% in Q1 2026 is already on pace to overshoot the 15% annual target. Interbank rates have risen to ca.7.4%, up from a 4.5% trough in late 2025, signalling tightening conditions from the bottom up.

• New business registrations rose 58% YOY in Q1 2026, while education firm registrations declined 74%, suggesting a consolidation trend that favours established operators. The macro environment is supportive for the Group's education businesses, with education sector GDP growing 8.3%, the fastest rate since 2023. Key regulatory developments include the Personal Data Protection Law (effective January 2026), Decree 69 on fire safety (effective April 2026), the Social Insurance Law (effective July 2026), and the Law on Teachers (effective 2026). The Decree 293 minimum wage increase, effective from January 2026, is limited to workers without vocational certificates and has bounded impact on the Group's operations.

• Over the past two decades, Vietnam has evolved from a low-income to an upper-middle-income band (from $4,466 to $13,845) according to the World Bank, with 2024 GDP per capita estimated at $4,700. With a population of ca.102.2 million in 2025 and a median age of 33.4 years old, Vietnam is the third most populous country in Southeast Asia, after Indonesia and the Philippines. According to the EF English Proficiency Index in 2024, Vietnam was still classified as "Low proficiency".

Myanmar

The years stated below refer to the calendar year, which runs from 1 January to 31 December, and the financial year below refers to the Myanmar financial period, which runs from 1 April to 31 March.

• Myanmar's economy remains fragile, with the ADB forecasting GDP growth of 2.4% in 2026, recovering from a 2.2% contraction in 2025 that was exacerbated by the March 2025 earthquake. However, this growth is largely statistical, reflecting recovery off a depressed base, and does not indicate genuine rebuilding of investment, trade, or consumer demand. The ADB estimates per capita GDP contracted by 2.9% in 2025 and 1.5% in 2024, with a modest recovery to 1.7% growth forecast for 2026 - implying continued severe erosion of living standards through the forecast horizon.

• Inflationary pressures remain acute: headline CPI was 25.2% in 2025, the highest in Southeast Asia, and a March 2026 fuel spike added an estimated 2-3 percentage points to Q1 2026 CPI. The ADB projects inflation to ease to 24.0% in 2026 as a result of a stabilising currency and weakening domestic demand. Affordability continues to compress across consumer segments. The escalation of the Iran conflict and the resulting tightening of global oil supply have exacerbated fuel rationing in parts of Myanmar.

• Manufacturing PMI posted its strongest reading since Q3 2023 at 51.5 in March 2026, driven by stable electricity supply and local substitution amid import restrictions. However, surging input costs, now at an 18-month high, risk arresting the upturn. Employment contraction has returned, signalling a deeper structural constraint as outmigration erodes the skilled workforce. The People's Military Service Law continues to be actively enforced for ages 18-35 (men) and 18-27 (women), accelerating skilled labour outmigration and heightening staff retention risk.

• According to the World Bank, Myanmar recorded a trade surplus of ca.$1.0 billion (ca.1.3% of GDP) in FY25, driven mainly by import compression amid tighter licensing and border disruptions. The fiscal deficit widened to 4.1% of GDP in FY25 and is expected to increase further to 4.9% in FY26, reflecting rising reconstruction and humanitarian spending. The current account shifted to a surplus of 3.2% of GDP in FY25, supported by import compression and remittances, but is expected to narrow to 0.4% of GDP in FY26.

• The Central Bank of Myanmar's ("CBM") Notification 2/2026 reduced the mandatory export earnings conversion requirement from 25% to 15%, providing meaningful relief for export-oriented operations. The official CBM reference rate remains pegged at MMK 2,100 per USD, maintaining a multiple rates market with significant spreads.

• FDI remained at a fraction of pre-crisis levels, with Q1 2026 commitments of $62.9 million across 72 approvals generating ca.10,900 jobs. The new Union Government's FY2026-2027 budget of MMK 195 trillion targets 3.4% growth, with priority spending directed toward agriculture, MSMEs, and infrastructure. Key legislative developments include the Union Tax Law 2026, the Construction Development Law, and a signalled SEZ regulatory review.

• Myanmar faces persistent infrastructure and energy challenges, worsened by reduced FDI, limited external support, and widespread power shortages. Seasonal hydropower dependence and earthquake-related grid damage continue to drive frequent outages. Moreover, ca.80% of natural gas production is committed through long-term contracts to neighbouring nations.

• Political uncertainty and rising internal displacement continue to destabilise the labour market, hinder economic recovery, and shift consumer behaviour. Coupled with inflationary pressures, these factors have led to a significant rise in price sensitivity across the population. According to the World Bank, 3.7 million people were internally displaced and ca.16.0 million people required humanitarian assistance as of January 2026. Meanwhile, the World Bank's State of Education in Myanmar report noted a significant rise in household spending on private tutoring in 2023, as families sought to support their children's education amid uncertain times, a trend that is expected to remain stable.

Enrico Cesenni (OSI), Chief Executive Officer of Asia Strategic, commented:

"The first half of FY26 has been a period of stabilisation and strategic repositioning for the Group. While reported revenue declined to $13.1 million, this primarily reflects the adoption of a market-based exchange rate for the Myanmar Kyat under IAS 21, which more accurately reflects the economic reality on the ground and the lack of exchangeability of the Myanmar Kyat. In local currency terms, our Myanmar operations continued to grow strongly, with the franchised Education brands collectively up 22% YOY in MMK terms, and I am particularly pleased that the Group achieved positive adjusted EBITDA of $1.3 million, the first time a positive adjusted EBITDA has been achieved, representing a significant milestone that demonstrates the underlying operational strength of our portfolio.

"In Vietnam, our priority has been to streamline operations and install the right leadership. Wall Street English Vietnam continues its restructuring, with one centre relocated to a more cost-efficient site. At Kids&Us Vietnam, we opened a new school and another in April, with further expansion planned nationwide. We have also installed new leadership at Logiscool Vietnam, and I am optimistic about the brand's trajectory.

"In Myanmar, the Group has moved decisively from post-earthquake recovery into expansion mode. All Mandalay premises impacted have been restored and reopened. Across our newer brands, we have two schools under construction and three more locations secured, in addition to the ambitious expansions underway at both Auston and Yangon American. Each campus is pursuing its own growth agendas: Auston through new UK university partnerships and campus development, and Yangon American through the opening of its Bahan campus in central Yangon. The Group has ambitious plans to expand the Bahan campus to include Early Years and Elementary from the academic year 2026/27.

"We remain committed to long-term value creation and believe strongly in the potential of Emerging Asia. On behalf of the Board, I thank our shareholders for their continued trust and extend heartfelt appreciation to the Asia Strategic team for their resilience and dedication."

For more information, please visit asia-strategic.com or contact:

Asia Strategic Holdings Ltd.

Richard Greer, Independent Non-Executive Chairman

Enrico Cesenni (OSI), Founder and CEO

richard@asia-strategic.com

enrico@asia-strategic.com

Allenby Capital Limited (Broker)

Nick Athanas / Nick Naylor (Corporate Finance)

Amrit Nahal / Lauren Wright (Sales and Corporate Broking)

+44 (0)20 3328 5656

Yellow Jersey PR (Financial PR)

Shivantha Thambirajah

+44 (0) 20 3004 9512

Notes to editors

Asia Strategic Holdings Ltd. (LSE: ASIA) is an independent developer and operator of consumer businesses focused on Education and Services in Emerging Asia, specifically Vietnam and Myanmar.

Education Division: The Group operates a diverse portfolio of education brands, encompassing English language learning, coding, K-12, and tertiary education. As of 31 March 2026, the Education division consisted of 37 schools, serving over 10,970 students.

Services Division: The Group operates two brands: (i) EXERA, an integrated risk and facilities management services provider in Myanmar and Vietnam; and (ii) Ostello Bello, a boutique hostel chain. As of 31 March 2026, EXERA employed ca. 2,280 service personnel (comprising primarily of security officers and IFM staff) across ca. 280 sites.

Asia Strategic Holdings utilises an asset-light strategy to scale its operations and capitalises on emerging opportunities in Vietnam and Myanmar.

OPERATIONAL REVIEW

Education

The Group's objective for its Education division is to become a leading operator and retailer of tech-enabled education services in Emerging Asia.

Revenue from Education businesses declined 20% YOY to $10.1 million in 6M26 (6M25: $12.6 million), primarily reflecting the IAS 21 translation of MMK-denominated revenues. The Myanmar Education brands (excluding Yangon American) grew 22% YOY in local currency terms.

At 31 March 2026, deferred revenue from Education businesses, representing cash received in advance of service delivery, was:

• Current: $10.4 million (1 October 2025: $10.1 million, as restated under IAS 21)

• Non-Current: $3.8 million (1 October 2025: $2.8 million, as restated under IAS 21)

Within its Education division, the Group provides educational products for children, teens, and adults through five brands across Vietnam and Myanmar.

Franchised Brands

Wall Street English is a leading English language education provider for adults with over 180,000 students enrolled in 29 countries. Its flexible and integrated blended learning solution is offered online or through a hybrid online/in-centre approach.

Kids&Us is a leading English language education provider for children and teens starting at age one and operates in ten countries with over 180,000 students enrolled across 600 schools. Its unique teaching method focuses on natural language acquisition, personalised for each student's age and experiences.

Logiscool is an enrichment programme that teaches children coding and digital literacy. Logiscool operates in 30 countries across more than 360 locations with over 320,000 students enrolled and graduated.

Own Brands

Yangon American offers an international K-12 education and is an authorised International Baccalaureate Primary Years Programme and Middle Years Programme school, the only PYP and MYP authorised school in Myanmar. It is also a candidate to be accredited as a Western Association of Schools and Colleges ("WASC") school.

Auston is a private higher education provider in Myanmar offering internationally recognised engineering and IT diplomas and degrees through (i) partnerships with the University of Wolverhampton (since December 2025), and University College Birmingham (since February 2026), and (ii) Pearson Edexcel and BTEC certifications.

Vietnam

Revenue from Education businesses in Vietnam decreased 10% YOY to $3.6 million in 6M26 (6M25: $4.0 million).

At 31 March 2026, deferred revenue from Education businesses in Vietnam, representing cash received in advance of service delivery, was:

• Current: $3.6 million (1 October 2025: $3.5 million)

• Non-Current: $0.6 million (1 October 2025: $0.7 million)

Wall Street English Vietnam

• Revenue from Wall Street English Vietnam decreased 16% YOY to $3.0 million in 6M26 (6M25: $3.5 million). The decline is attributable to the continued shift in product mix toward lower-priced online delivery.

• Student enrolment increased slightly to ca.3,410 at 31 March 2026.

• Cost reduction measures, including school rightsizing and staff restructuring, continue to be implemented to restore profitability. One centre was relocated to a more cost-efficient location during the period.

• At 31 March 2026, Wall Street English Vietnam operated seven schools, with six in Ho Chi Minh City and one in Binh Duong.

Kids&Us Vietnam

• Revenue from Kids&Us Vietnam increased 32% YOY to $0.6 million in 6M26 (6M25: $0.4 million), reflecting accelerating commercial traction as the brand continues to establish itself in the market.

• Student enrolment grew 14% from 30 September 2025 to ca.1,290 at 31 March 2026, driven by stabilising retention rates and new sales from the continued opening of new schools.

• The Group advanced its growth agenda by refining its site selection strategy, focusing on smaller, more efficient spaces, while enhancing service team efficiency. One new school opened in April 2026, with further expansion planned nationwide.

• At 31 March 2026, Kids&Us Vietnam operated seven schools in Ho Chi Minh City.

Logiscool Vietnam

• Revenue from Logiscool Vietnam increased 70% YOY to $77k in 6M26 (6M25: $45k), off a small base.

• Student enrolment was broadly stable at ca.160 at 31 March 2026. Growth was slower than expected in 6M26, driven by subdued sales at schools in secondary locations.

• With new leadership installed and planned co-location within existing Kids&Us sites in central areas, performance is expected to improve in the second half of FY26.

• At 31 March 2026, Logiscool Vietnam operated three schools, with two in Ho Chi Minh City and one in Binh Duong.

Myanmar

Revenue from Education businesses in Myanmar declined 24% YOY to $6.5 million in 6M26 (6M25: $8.6 million), primarily reflecting the IAS 21 translation of MMK-denominated revenues. The Myanmar Education brands (excluding Yangon American) grew 22% YOY in local currency terms, reflecting continued underlying expansion across the portfolio.

At 31 March 2026, deferred revenue from Education businesses in Myanmar, representing cash received in advance of service delivery, was:

• Current: $6.8 million (1 October 2025: $6.7 million, as restated under IAS 21)

• Non-Current: $3.2 million (1 October 2025: $2.2 million, as restated under IAS 21)

Wall Street English Myanmar

• Revenue from Wall Street English Myanmar grew 15% YOY in local currency, while declined 34% YOY in USD to $2.7 million in 6M26 (6M25: $4.1 million) due to the IAS 21 translation.

• Student enrolment declined 3% from 30 September 2025 to ca.3,200 at 31 March 2026. Price increases, implemented to hedge against market risks, helped offset affordability concerns and increased emigration.

• At 31 March 2026, Wall Street English Myanmar operated five schools with four in Yangon and one in Mandalay.

Kids&Us Myanmar

• Revenue from Kids&Us Myanmar grew 64% YOY in local currency, while declined 5% YOY in USD to $0.4 million in 6M26 (6M25: $0.4 million) due to the IAS 21 translation.

• Student enrolment grew 28% from 30 September 2025 to ca.780 at 31 March 2026. With stabilised leadership in place, the business is on an upward trajectory, supported by robust demand for early childhood English education.

• At 31 March 2026, Kids&Us Myanmar operated four schools in Yangon. One school is currently under construction in Mandalay, and one additional school has been secured and shall open by August 2026.

Logiscool Myanmar

• Revenue from Logiscool Myanmar grew 141% YOY in local currency, the strongest among the Group's franchised businesses, while also grew 39% YOY in USD to $0.5 million in 6M26 (6M25: $0.4 million), as strong enrolment growth outpaced the translation impact under IAS 21.

• Student enrolment grew 29% from 30 September 2025 to ca.1,100 at 31 March 2026, representing the strongest student growth rate among the Group's franchised businesses.

• The commercial success was driven by an experienced commercial team, a strong product offering, and limited competition. One school is under construction, and one more is in the pipeline.

• At 31 March 2026, Logiscool Myanmar operated six schools, with five in Yangon and one in Mandalay. One school is under construction in Yangon, and one additional school has been secured and shall open by August 2026.

Yangon American International School

• Revenue from Yangon American increased 27% YOY to $1.1 million in 6M26 (6M25: $0.9 million), the strongest growth in USD terms across the Group's Myanmar Education businesses.

• Student enrolment grew to ca.200 at 31 March 2026. A key milestone in 6M26 was the opening of the new Bahan campus in January 2026, providing a dedicated Secondary campus in central Yangon.

• Yangon American also achieved IB Middle Years Programme ("MYP") authorisation during the period, making it the only IB Primary Years Programme ("PYP") and MYP authorised school in the Myanmar market. This reinforces its premium positioning and credentialling pathway for students progressing from elementary through to upper secondary.

• Looking ahead, the Group has ambitious plans to expand the Bahan campus to include Early Years and Elementary from the 2026/2027 academic year. Its central location near embassies, UN agencies, and city landmarks enhances accessibility and reinforces Yangon American's premium positioning.

• At 31 March 2026, Yangon American operated two campuses in Yangon: The Hlaing campus (Early Years and Elementary) and the Bahan campus (Secondary only for the 2025-2026 academic year).

Auston

• Revenue from Auston grew 10% YOY in local currency, while declined 37% YOY in USD to $1.8 million in 6M26 (6M25: $2.8 million) due to the translation under IAS 21.

• Student enrolment was ca.830 at 31 March 2026, with a small decline from 860 at 30 September 2025, driven by increased migration and conscription-related uncertainty.

• Auston signed new academic partnership agreements with the University of Wolverhampton in December 2025 and University College Birmingham in February 2026, ensuring continuity and expanded pathways for students.

• Auston is pursuing an ambitious expansion of its Yangon campus facilities. At 31 March 2026, Auston operated campuses in Mandalay and Yangon.

Services

The Group's objective is to become a leading risk management partner for organisations operating in Emerging Asia, focusing on integrated security and facility management services..

Revenue from Services businesses decreased 13% YOY to $3.0 million in 6M26 (6M25: $3.4 million).

At 31 March 2026, deferred revenue from Services businesses, representing cash received in advance of service delivery, was:

• Current: $0.3 million (1 October 2025: $0.3 million, as restated under IAS 21)

• Non-Current: $ Nil (1 October 2025: $ Nil, as restated under IAS 21)

Within its Services division, the Group operates two brands across Myanmar and Vietnam:

EXERA is a leading provider of risk management, consulting, integrated security, manned guarding, secure logistics, and integrated facility management services. It serves a wide range of international and local clients across Myanmar and holds ISO 18788, ISO 9001, ANSI/ASIS PSC.1 certifications, and ICoCA membership. In Vietnam, it is a start-up focused on integrated facility management services.

Ostello Bello is a boutique Italian hostel brand known for its vibrant social atmosphere and exceptional hospitality. Ostello Bello operates a boutique hostel in Bagan, Myanmar.

EXERA Vietnam

• EXERA Vietnam was launched in FY24 to provide integrated facility management ("IFM") services and generated $29k revenue in 6M26 (6M25: $22k). The business remains an early-stage start-up and is exploring strategic partnerships to increase market penetration.

EXERA Myanmar

• Revenue from EXERA Myanmar decreased 13% YOY to $3.0 million in 6M26 (6M25: $3.4 million), reflecting the non-recurrence of a large USD-denominated account, the non-renewal of certain risk reporting contracts as the security situation improved, and ongoing pricing pressure in the market, partially offset by new local client wins, particularly in financial services.

• EXERA Myanmar employed ca.2,280 service personnel as of 31 March 2026 (30 September 2025: ca.1,930) across ca.280 sites in Myanmar (30 September 2025: ca.250 sites).

FINANCIAL REVIEW

Results of Operations

Revenue declined 18% YOY to $13.1 million in 6M26 (6M25: $16.0 million), largely driven by the translation of MMK-denominated revenues at the Market Exchange Rate. Revenues would have increased by 3% if the Reference Exchange Rate had been applied.

$

6M26

6M25

6M24

FY25

FY24

Education - Vietnam

3,619,056

4,012,554

4,183,035

7,720,079

8,229,656

Wall Street English

2,980,763

3,543,518

3,929,484

6,686,568

7,631,372

Kids&Us

561,306

423,819

249,524

923,229

575,519

Logiscool

76,987

45,217

4,027

110,282

22,765

Education - Myanmar

6,511,410

8,572,051

6,741,082

17,250,190

14,441,789

Wall Street English

2,710,645

4,111,979

3,767,997

8,198,732

7,744,204

Kids&Us

367,636

388,733

142,739

854,603

416,064

Logiscool

546,741

394,277

15,922

1,003,583

148,726

Yangon American

1,124,850

884,802

600,891

1,795,032

1,230,966

Auston

1,761,538

2,792,260

2,213,533

5,398,240

4,901,829

Education

10,130,466

12,584,605

10,924,117

24,970,269

22,671,445

Services

EXERA Vietnam

28,940

22,477

-

60,787

3,576

EXERA Myanmar

2,955,152

3,410,225

3,496,937

7,071,011

6,988,643

Ostello Bello

-

-

10,351

-

10,351

Services

2,984,092

3,432,702

3,507,288

7,131,798

7,002,570

Total

13,114,558

16,017,307

14,431,405

32,102,067

29,674,015

Revenue from Education businesses in Myanmar declined 24% YOY to $6.5 million in 6M26 (6M25: $8.6 million), primarily reflecting the IAS 21 translation of MMK-denominated revenues. The Myanmar Education brands (excluding Yangon American) grew 22% YOY in local currency terms, reflecting continued underlying expansion across the portfolio. The reported revenue decline against last year's high base across these businesses reflects a one-off translation effect rather than underlying operational weakness.

The Services division declined in 6M26, reflecting the replacement of large USD-denominated accounts by local Myanmar Kyat-denominated clients and the non-renewal of certain risk reporting contracts as the security situation improved, resulting in a net reduction of contracts amid a price-sensitive market. EXERA Vietnam has begun generating revenue but remains an early-stage start-up.

Group gross profit declined 17% YOY to $7.8 million in 6M26 (6M25: $9.4 million), with the Education division contributing 93% (6M25: 94%) and the Services division 7% (6M25: 6%). The Group's gross profit margin remained stable at 59% (6M25: 59%), supported by an improvement in the Education division's gross margin to 72% (6M25: 70%), whilst being partially offset by a marginal decline in the Services division's gross margin to 17% (6M25: 18%) amid pricing pressure in Myanmar.

The Group's net loss narrowed to $2.2 million in 6M26 (6M25: $3.7 million loss). The improvement was primarily driven by a $0.4 million foreign exchange gain (6M25: $1.3 million loss) and a 13% reduction in administrative and other operating expenses to $9.6 million (6M25: $11.1 million), reflecting ongoing cost optimisation across the Group. These improvements were partially offset by a $0.9 million loss allowance on trade and other receivables relating to the affiliated entity (6M25: nil), following the consolidation and rationalisation of the Group's leased portfolio managed through that entity (see Note 12 of the financial statements).

$

6M26

6M25

6M24

FY25

FY24

Revenue

13,114,558

16,017,307

14,431,405

32,102,067

29,674,015

Cost of services

(5,335,787)

(6,601,338)

(6,107,945)

(13,207,615)

(12,689,487)

Gross profit

7,778,771

9,415,969

8,323,460

18,894,452

16,984,528

Gross profit margin

59%

59%

58%

59%

57%

Other income

40,141

8,708

37,549

57,951

16,495

Foreign exchange gain/(loss)

379,023

(1,267,015)

(584,505)

(2,794,062)

(1,455,135)

Loss allowance on receivables

(937,426)

(9,095)

-

(3,008)

-

Impairment on intangible assets

-

-

-

-

(4,561,645)

Plant & equipment write-off

-

(521,029)

-

(522,237)

-

Administrative & other operating expenses

(8,679,015)

(10,533,868)

(9,722,868)

(20,496,642)

(20,350,864)

Loss from operations

(1,418,506)

(2,906,330)

(1,946,364)

(4,863,546)

(9,366,621)

Finance cost

(780,746)

(711,845)

(617,946)

(1,493,155)

(1,341,391)

Loss before income tax

(2,199,252)

(3,618,175)

(2,564,310)

(6,356,701)

(10,708,012)

Income tax

(35,600)

(62,591)

-

79,821

(245,674)

Loss after income tax

(2,234,852)

(3,680,766)

(2,564,310)

(6,276,880)

(10,953,686)

Selected non-cash items:

Depreciation of P&E

503,357

684,023

580,733

1,301,998

1,207,028

Amortisation of ROU assets

1,231,737

1,316,818

1,402,364

2,683,325

2,786,093

Amortisation of intangibles

39,346

54,660

49,522

102,741

100,718

Plant & equipment write-off

-

521,029

-

522,237

-

Impairment on intangible assets

-

-

-

-

4,561,645

Loss allowance on receivables

937,426

9,095

-

3,008

-

Finance costs (excl lease)

155,779

114,463

94,550

224,802

220,416

Interest on lease liabilities

624,967

597,382

523,396

1,268,353

1,120,975

Total non-cash items

3,492,612

3,297,470

2,650,565

6,106,464

9,996,875

Adjusted EBITDA*

1,293,360

(320,705)

86,255

(250,237)

(711,137)

Adjusted EBITDA after impact of ROUs*

(563,344)

(2,234,905)

(1,839,505)

(4,201,915)

(4,618,205)

* Key performance indicators for the Group, based on earnings before interest, income tax, depreciation and amortisation ("EBITDA"), are (i) Adjusted EBITDA (as presented above) and (ii) Adjusted EBITDA less amortisation of right-of-use assets and interest on lease liabilities ("Adjusted EBITDA after impact of ROUs").

Group adjusted EBITDA turned positive at $1.3 million in 6M26 (6M25: $0.3 million loss), a significant milestone for the Group, driven by improved operating performance across the Education division and cost reduction initiatives. Marketing expenses, which consist predominantly of USD-denominated digital spend, decreased 18% YOY to $1.4 million (6M25: $1.7 million), reflecting improved spending discipline and more targeted campaigns.

Adjusted net losses, excluding the $0.9 million loss allowance on trade and other receivables relating to the affiliated entity, were $1.3 million in 6M26 (6M25: $3.2 million adjusted loss, excluding the plant and equipment write-off). The narrowing of adjusted net losses reflects the increasing maturity of the Group's new businesses and ongoing cost optimisation at Wall Street English Vietnam.

Cash Flow Evolution

At 31 March 2026, the Group's cash and cash equivalents position was $1.2 million (1 October 2025: $1.2 million, as restated under the IAS 21). The position resulted from the combination of (i) a $2.9 million inflow from operating activities, (ii) a $0.8 million outflow from investing activities, and (iii) a $2.1 million outflow from financing activities.

The Group generated cash inflow from operating activities of $2.9 million in 6M26 (6M25: inflow $2.1 million). Operating cash flow before working capital changes in 6M26 was positive $0.9 million (6M25: negative $43,000). If repayment of lease liabilities of $1.9 million (6M25: $1.8 million) were considered, adjusted cash inflow from operating activities would be positive $1.0 million (6M25: positive $0.3 million).

The Group incurred cash outflow from investing activities of $0.8 million in 6M26 (6M25: $0.6 million), of which $0.8 million (6M25: $0.2 million) was spent on capital expenditure in plant and equipment, primarily directed towards the opening of new Kids&Us schools in Vietnam and the expansion of the Yangon American Bahan Secondary Campus and Auston Yangon campus in Myanmar.

Cash outflow from financing activities amounted to $2.1 million in 6M26 (6M25: $1.0 million) for the repayments of (i) lease liabilities, totalled $1.9 million (6M25: $1.8 million) and convertible credit facility $0.2 million (6M25: $ Nil). There were no new shareholder loan drawdowns or convertible note proceeds in 6M26 (6M25: $45,000 shareholder loan and $0.7 million convertible notes).

Dividends

The Board of Directors does not recommend paying dividends for 6M26 as the Group needs to conserve cash for working capital and future expansion.

Liquidity Management And Going Concern

The Board of Directors has carried out a detailed review of the Group's cash flow forecast and specifically considered a going concern review period of twelve months from the date of this report.

The Board of Directors determined management has control over sufficient mitigating actions to manage cash outflow, including:

• Monitoring and adjusting any Myanmar business expansion against the political and economic environment. The Myanmar businesses have been expanding and are self-sustaining since FY23, with any capital expenditures funded through excess capital earned locally;

• Leveraging the negative cash conversion cycle, as tuition fees and certain risk management services are generally collected up to twelve months in advance of service delivery;

• Support by franchise partners through flexible payment plans in relation to franchise fees and didactic materials;

• Accessing the unutilised Loan Facility as disclosed in the financial statements.

At the date of this report, the Directors have concluded that the Group has adequate financial resources to cover its working capital needs for at least the next twelve months.

OUTLOOK

Asia Strategic Holdings is committed to leveraging its integrated operating model and in-house shared service functions to deliver sustainable returns to shareholders.

Capital Allocation and Strategic Focus

The Group maintains a disciplined asset-light approach to capital, with the existing businesses financing growth through organic cash flow generation. Expansionary capital expenditures are approached carefully, ensuring that multi-brand locations are privileged to maximise the economies of scale. Any expansion into new geographies and/or sectors would leverage the strength of the Group's shared service function.

Continued Development of Existing Brands

Turning around Wall Street English Vietnam remains a top priority, with efforts focused on operational maturity, cost rightsizing, and commercial recalibration. In Myanmar, the Group's newer brands (e.g. Kids&Us and Logiscool) have already established market-leading positions and are well positioned for continued expansion, with two schools under construction and three more in the pipeline.

The Group is also actively enhancing the programmes at Auston and Yangon American, ensuring students receive the best-in-class education. Auston's new university partnerships with the University of Wolverhampton and University College Birmingham, and Yangon American's new Bahan campus, strengthen both institutions' competitive edge.

Navigating Macroeconomic Conditions

The Group expects the operating environment to remain complex but manageable. In Myanmar, the completion of the general election and the formation of a new government provide a degree of political clarity, though structural economic challenges persist. The Group continues to actively manage its cost base to protect margins. In Vietnam, the macroeconomic fundamentals remain supportive, with strong GDP growth, rising education demand, and a consolidating competitive landscape that favours established operators. The Group is well-positioned to capitalise on these dynamics.

NOTES TO THE CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTSFor the financial period from 1 October 2025 to 31 March 2026

1 CORPORATE INFORMATION

Asia Strategic Holdings Limited (the "Company" or "Asia Strategic") (Registration Number 201302159D) is a public company limited by shares incorporated and domiciled in Singapore with its principal place of business and registered office at 80 Raffles Place #32-01, UOB Plaza, Singapore 048624. The Company's ordinary shares are traded on the Main Market of the London Stock Exchange under the equity ticker ASIA.

The consolidated financial statements of the Group and the statement of financial position of the Company are presented in United States dollar ("US$" or "$") which is the functional currency of the Company and the presentation currency for the consolidated financial statements.

The condensed interim consolidated financial statements as at and for the six-month financial period ended 31 March 2026 comprise the Company and its subsidiaries (collectively, the "Group").

For management purposes, the Group is organised into business units based on its services, and has three reportable operating segments as follows:

a) Education - Operation of education businesses ranging from early years to tertiary education and including vocational training, consultancy, advisory and project management services in the education sector in Vietnam and Myanmar;

b) Services - Provision of integrated services, consultancy, advisory and project management services in the security, facility management and hospitality sectors in Vietnam and Myanmar. This reportable segment has been formed by aggregating the relevant operating entities, which are regarded by management to exhibit similar economic characteristics; and

c) Corporate - Corporate services, management support and certain shared services to subsidiaries of the Group.

These operating segments are reported in a manner consistent with internal reporting provided to the chief operating decision-maker responsible for allocating resources and assessing the performance of the operating segments.

1.1 BASIS OF PREPARATION

The condensed interim consolidated statement of financial position as at 31 March 2026 and the related condensed interim consolidated statement of other comprehensive income, condensed interim consolidated statement of changes in equity and condensed interim consolidated statement of cash flows for the six-month financial period ended 31 March 2026 and the explanatory notes have not been audited or reviewed by the Group's Independent Auditors. The condensed interim consolidated financial statements for the financial period ended 31 March 2026 have been prepared in accordance with International Accounting Standards ("IAS") 34 Interim Financial Reporting as adopted by the European Union.

The condensed consolidated interim financial statements do not include all disclosures that would otherwise be required in a complete set of financial statements and should be read in conjunction with the annual report for the financial year ended 30 September 2025. However, selected explanatory notes are included to explain events and transactions that are significant to understanding the changes in the Group's financial position and performance since the last annual financial statements for the financial year ended 30 September 2025, which can be found on the Company's website at www.asia-strategic.com.

The consolidated financial statements of the Group are presented in United States dollars ("$"), which is the presentation currency for the consolidated financial statements.

2 MATERIAL ACCOUNTING POLICIES

The accounting policies adopted are consistent with those of the previous financial year which were prepared in accordance with International Financial Reporting Standards ("IFRS") as adopted by the European Union, except for the adoption of new and amended standards as set out below.

Changes in accounting policy

On 1 October 2025, the Group adopted the new or amended IFRS and interpretations to IFRS that are mandatory for application for the financial year. The adoption of these standards did not result in significant changes to the Group's accounting policies and had no material impact to the Group's financial statements, except as detailed below:

Amendments to IAS 21: Lack of Exchangeability

The amendments to IAS 21, effective for the Group from 1 October 2025, set out how an entity assesses whether a currency is exchangeable and how it estimates a spot exchange rate when it is not, and requires disclosure of the nature and financial effects of the exchangeability issue, the spot rate applied, the estimation approach, and the carrying amount of items exposed.

Since its inception, the Group has developed significant operations in Myanmar. Since February 2021, the Central Bank of Myanmar ("CBM") has maintained administrative controls over foreign currency transactions, including restrictions on the conversion of the Myanmar Kyat ("MMK") and on the transfer of funds. The Group has therefore concluded that the MMK is not freely exchangeable into USD, its presentation currency, within a reasonable time frame at the reporting date.

Exposure arises from (i) monetary items held in a non-functional currency within Myanmar subsidiaries, whose remeasurement affects profit or loss, and (ii) the translation of MMK functional subsidiaries into the Group's USD presentation currency, whose effect is recognised in the foreign currency translation reserve.

As the CBM reference rate is not reasonably accessible, the Group has estimated the spot rates using the Market Trading Rate ("MTR"), applied without adjustment. The MTR, is a weighted average of interbank and bank-customer trades executed by authorised dealers, and is published daily by the CBM. The MTR is considered an appropriate basis because it is market-driven, reflects prevailing supply and demand, and is accessible to market participants, and represents the rate at which an orderly exchange transaction would take place at the measurement date between market participants under prevailing economic conditions.

Estimation of the spot rate involves significant judgement. In reaching this conclusion, the Group also considered rates observable in active cross-border markets, rates on the Group's own recent arm's length transactions, and published indices and observable data. The daily spot rates applied during 6M26 ranged from MMK 3,600 to MMK 3,650 per USD. Changes in the underlying assumptions could materially affect the translation of monetary items and the results of the Myanmar operations.

Effect of Transition

In accordance with the transitional provisions, comparatives have not been restated. The cumulative effect of applying the amendments has been recognised at 1 October 2025 as adjustments to:

(a) opening accumulated losses: exchange differences arising on the remeasurement of foreign currency monetary items in the underlying records of the Myanmar subsidiaries; and

(b) foreign currency translation reserve: exchange differences arising from the translation of financial performance and financial position of foreign operations whose functional currency is MMK into the Group's USD presentation currency.

The carrying amount of items exposed and the transition effect are summarised below.

Group

$

1 Oct 2025,

as previously reported

Effect of

IAS 21 transition

1 Oct 2025,

as restated

under IAS 21

Assets

Plant and equipment

2,910,672

(594,232)

2,316,440

Intangible assets

1,974,736

(57,859)

1,916,877

Right-of-use assets

16,040,875

(3,719,383)

12,321,492

Trade and other receivables

3,310,080

(1,363,362)

1,946,718

Non-current assets

24,236,363

(5,734,836)

18,501,527

Inventories

437,715

(57,214)

380,501

Tax recoverable

47,809

(20,215)

27,594

Trade and other receivables

2,401,956

(520,672)

1,881,284

Cash and cash equivalents

1,548,372

(396,884)

1,151,488

Current assets

4,435,852

(994,985)

3,440,867

Total assets

28,672,215

(6,729,821)

21,942,394

Liabilities

Contract liabilities

4,399,689

(1,561,200)

2,838,489

Lease liabilities

15,422,395

(4,894,041)

10,528,354

Borrowings

4,225,975

-

4,225,975

Non-current liabilities

24,048,059

(6,455,241)

17,592,818

Contract liabilities

14,480,878

(4,069,461)

10,411,417

Trade and other payables

8,158,155

(1,246,919)

6,911,236

Lease liabilities

2,523,814

(434,980)

2,088,834

Current liabilities

25,162,847

(5,751,360)

19,411,487

Share capital

21,919,638

-

21,919,638

Accumulated losses

(50,775,107)

4,714,330

(46,060,777)

Reserve

8,316,778

762,450

9,079,228

Equity

(20,538,691)

5,476,780

(15,061,911)

28,672,215

6,729,821

21,942,394

The foreign exchange regime in Myanmar remains fluid. The Group will reassess exchangeability and the estimated spot rate at each reporting date. Changes in regulations, approval processes or market conditions may have a material impact on the Group's financial statements in future periods.

Foreign currency risks and sensitivity analysis

Foreign exchange risk arises when individual entities within the Group enters into transactions denominated in a currency other than their functional currency. The currency that gives rise to material risk for the Group is primarily the MMK. The Group has not entered into any currency forward exchange contracts as at the end of the reporting period.

The following table sets out the Group's sensitivity to a 20 per cent (30 Sep 2025: 20 per cent) change in the MMK against the USD, reflecting the limited observable liquidity in the MMK/USD market and the potential divergence between the MTR applied by the Group and alternative rate sources available to market participants. The analysis assumes an instantaneous change in the exchange rate at the reporting date, with all other variables held constant.

Gain/(Loss)

before tax

$

31 Mar 2026

30 Sep 2025

$

Myanmar Kyat

Strengthen against United States Dollar

382,000

293,000

Weaken against United States Dollar

(382,000)

(293,000)

IFRSs issued but not yet effective

Certain new accounting standards and interpretations have been issued but are not yet effective for the current financial year ending 30 September 2026 and have not been adopted early by the Group. The Group expects that the adoption of these IFRSs, if applicable, will have no material impact on the financial statements in the period of initial application except for the IFRS 18 Presentation and Disclosure in Financial Statements as disclosed in the last annual report for the financial year ended 30 September 2025.

3 USE OF JUDGEMENTS AND ESTIMATES

In preparing the condensed interim financial statements, management has made judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, income and expenses. These estimates are based on management's best knowledge of current events and market environment in the respective countries the Group operates as at the reporting date. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimates are revised and in any future periods affected.

The significant judgments made by management in applying the Group's accounting policies and the key sources for estimating uncertainty were the same as those that applied to the consolidated financial statements as at and for the financial year ended 30 September 2025, except as disclosed in Note 2 to the financial statements.

3.1 SEASONAL OPERATIONS

The Group's businesses were not affected significantly by seasonal or cyclical factors during the financial period ended 31 March 2026.

The timing of revenue recognition would affect the amount of revenue and deferred revenue recognised as at the reporting date in the condensed consolidated statement of financial position.

$

31 Mar 2026

30 Sep 2025

Contract liabilities

Current

10,746,043

14,480,878

Non-current

3,813,974

4,399,689

14,560,017

18,880,567

Significant changes in contract liabilities are as detailed below:

$

6M26

FY25

At 1 October 2025, as previously reported

18,880,567

14,424,989

Effect of transition to IAS 21

(5,630,661)

-

As at 1 October 2025, as restated

13,249,906

14,424,989

Cash received in advance of performance

and not recognised as revenue

11,787,645

30,357,376

Revenue recognised during the financial

period/year:

- On contract liabilities at beginning of financial period/year

(7,290,450)

(11,643,390)

- On cash received in advance during financial period/year

(3,165,563)

(13,957,360)

(10,456,013)

(25,600,750)

Foreign exchange difference

(21,521)

(301,048)

At end of financial period/year

14,560,017

18,880,567

Remaining performance obligations

Deferred revenue is in respect of cash received in advance of performance, which will be recognised based on the following:

(i) Tuition fees: collected 1 to 12 months (30 Sep 2025: same), and more than 12 months for certain students who prepaid in advance of course period with reference to the individual terms of the student contracts.

(ii) Security risk management services: generally collected 6 to 24 months (30 Sep 2025: same) in advance of risk management services to the customer.

6M26

$

Education

Services

Corporate

Total

Revenue

10,130,466

2,984,092

-

13,114,558

Cost of services

(2,864,630)

(2,471,157)

-

(5,335,787)

Gross profit

7,265,836

512,935

-

7,778,771

Other income

4,363

744

35,034

40,141

Foreign exchange gain, net

349,030

27,643

2,350

379,023

Administrative and other operating expenses

(7,227,438)

(856,395)

(1,532,608)

(9,616,441)

Loss from operations

391,791

(315,073)

(1,495,224)

(1,418,506)

Finance cost

(667,162)

(3,424)

(110,160)

(780,746)

Segment loss

(275,371)

(318,497)

(1,605,384)

(2,199,252)

Income tax expense

(35,600)

-

-

(35,600)

Loss after income tax

(310,971)

(318,497)

(1,605,384)

(2,234,852)

Other non-cash items:

Total depreciation of plant and equipment

461,556

41,618

183

503,357

Total amortisation of right-of-use asset

1,203,242

28,495

-

1,231,737

Total amortisation of intangible assets

39,346

-

-

39,346

Loss allowance on trade and other receivables

883,379

54,047

-

937,426

Finance costs (excluding interest on lease liabilities)

45,619

-

110,160

155,779

Total interest on lease liabilities

621,543

3,424

-

624,967

3,254,685

127,584

110,343

3,492,612

Adjusted EBITDA

2,979,314

(190,913)

(1,495,041)

1,293,360

Adjusted EBITDA after

impact of ROU

1,154,529

(222,832)

(1,495,041)

(563,344)

Reportable segment assets

as at 31 March 2026

17,008,807

3,223,134

245,233

20,477,174

Total Group's assets

Included in the segment assets:

Additions:

Plant and equipment

773,320

10,729

-

784,049

Right-of-use assets

608,384

-

-

608,384

Reportable segment liabilities as at 31 March 2026

(32,043,607)

(1,023,737)

(5,032,422)

(38,099,766)

6M25

$

Education

Services

Corporate

Total

Revenue

12,584,605

3,432,702

-

16,017,307

Cost of services

(3,777,289)

(2,824,049)

-

(6,601,338)

Gross profit

8,807,316

608,653

-

9,415,969

Other income

7,532

565

611

8,708

Foreign exchange loss, net

(1,190,361)

(67,847)

(8,807)

(1,267,015)

Administrative and other operating expenses

(8,756,407)

(938,967)

(1,368,618)

(11,063,992)

Loss from operations

(1,131,920)

(397,596)

(1,376,814)

(2,906,330)

Finance cost

(588,468)

(8,920)

(114,457)

(711,845)

Segment loss

(1,720,388)

(406,516)

(1,491,271)

(3,618,175)

Income tax expense

(76,802)

14,211

-

(62,591)

Loss after income tax

(1,797,190)

(392,305)

(1,491,271)

(3,680,766)

Other non-cash items:

Total depreciation of plant and equipment

639,805

44,127

91

684,023

Plant and equipment

written off

521,029

-

-

521,029

Total amortisation of right-of-use asset

1,270,855

45,963

-

1,316,818

Total amortisation of intangible assets

54,660

-

-

54,660

Impairment loss on other receivables

9,095

-

-

9,095

Finance costs (excluding interest on lease liabilities)

-

-

114,463

114,463

Total interest on lease liabilities

588,462

8,920

-

597,382

3,083,906

99,010

114,554

3,297,470

Adjusted EBITDA

1,363,518

(307,506)

(1,376,717)

(320,705)

Adjusted EBITDA after

impact of ROU

(495,799)

(362,389)

(1,376,717)

(2,234,905)

Reportable segment assets

as at 31 March 2025

Total Group's assets

18,122,741

4,168,955

85,130

22,376,826

Included in the segment assets:

Additions:

Plant and equipment

186,819

9,253

1,095

197,167

Right-of-use assets

92,132

-

-

92,132

Reportable segment liabilities as at

31 March 2025

(34,631,683)

(1,202,378)

(4,641,031)

(40,475,092)

Geographic information

The Group operates in three main geographical areas. Revenue is based on the country in which the customers are located and services were delivered. Segment non-current assets consist primarily of non-current assets other than financial instruments and deferred tax assets. Segment non-current assets are shown by geographic area in which the assets are located.

Revenue

Non-current assets

$

6M26

6M25

31 Mar

2026

30 Sep 2025

Singapore

11,194

19,352

14,139

15,821

Vietnam

3,647,996

4,035,031

4,266,524

4,781,647

Myanmar

9,455,368

11,962,924

11,562,290

16,128,815

13,114,558

16,017,307

15,842,953

20,926,283

Non-current assets consist of plant and equipment, intangible assets and right-of-use assets in the Group's condensed consolidated statement of financial position.

5 EMPLOYEE BENEFIT EXPENSES

$

6M26

6M25

Wages, salaries and allowances*

6,710,282

8,483,424

Share-based compensation*

56,124

71,032

Staff insurance and medical expenses

146,258

124,866

Staff accommodation and welfare

256,742

210,257

Termination benefits

13,164

23,846

Others

54,537

130,590

7,237,107

9,044,015

Total employee benefit expenses:

- Cost of services

3,318,397

4,240,883

- Administrative and other operating expenses

3,918,710

4,803,132

7,237,107

9,044,015

* Included in these expenses are Director fees and remuneration.

6 FINANCE COST

$

6M26

6M25

Interest expenses:

- Shareholder loan (Note 14)

110,160

114,037

- Lease liabilities

624,967

597,382

- Interest on convertible credit facility

41,169

-

- Others

4,450

426

780,746

711,845

7 LOSS BEFORE INCOME TAX

Depreciation and amortisation expenses relating to plant and equipment, right-of-use assets and intangible assets directly attributable to provision of services and for operating activities are included in the "cost of services" and "administrative and other operating expenses", respectively in the condensed consolidated statement of comprehensive income.

In addition to the charges and credits disclosed elsewhere in the financial statements, the loss before income tax includes the following charges/(credits):

$

6M26

6M25

Cost of services

Academic expenses

700,054

1,141,580

Student enrolment and support fees

670,205

696,717

Expenses relating to student instalment plans

111,080

66,396

Security service expenses

269,232

281,443

Hotel related operating expenses

142,749

-

Depreciation expense

41,653

69,702

Amortisation of intangible assets

-

1,573

Administrative and other operating expenses:

Selling and marketing expenses

1,356,686

1,651,448

Professional fees

500,545

380,230

Travelling and transportation expenses

184,449

185,147

Amortisation of right-of-use assets

1,231,737

1,316,818

Amortisation of intangible assets

39,346

53,087

Depreciation expense

461,704

614,321

Impairment loss on trade and other

receivables (Note 12)

937,426

-

Plant and equipment written off (Note 9)

-

521,029

8 INCOME TAX EXPENSE

The corporate income tax rate applicable to the Company and its subsidiaries in Singapore is 17% (6M25: 17%). The Group has significant operations in Myanmar and Vietnam, for which the applicable corporate income tax rates are 22% (6M25: 22%) and 20% (6M25: 20%), respectively.

Income tax expense of $35,600 (6M25: $62,591) are mainly from profitable Education businesses. Other subsidiaries of the Group with operating losses have no chargeable income and/or unutilised tax losses for set-off.

9. PLANT AND EQUIPMENT

$

Leasehold improvements

Furniture

and fittings

Computers

and books

Motor

vehicles

Construction-

in-progress

Total

Cost

At 1 October 2025, as previously reported

3,958,846

1,427,265

1,390,494

61,769

35,328

6,873,702

Effect of transition to IAS 21

(635,473)

(239,496)

(252,689)

(17,026)

(1,001)

(1,145,685)

As at 1 October 2025, as restated

3,323,373

1,187,769

1,137,805

44,743

34,327

5,728,017

Additions

466,451

119,330

64,859

-

133,409

784,049

Transfers

37,573

1,887

-

-

(39,460)

-

Write-off

-

(2,578)

-

-

-

(2,578)

Foreign exchange difference

400

(217)

(628)

(42)

(74)