Wynnstay Properties - Final Results and Notice of AGM

The information communicated within this announcement is deemed to constitute inside information for the purposes of the Market Abuse Regulation (EU) No. 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018. Upon the publication of this announcement, this information is considered to be in the public domain.

17 June 2026

WYNNSTAY PROPERTIES PLC

("Wynnstay" or the "Company")

AUDITED RESULTS FOR YEAR ENDED 25 MARCH 2026 AND NOTICE OF AGM

Wynnstay Properties PLC is pleased to announce the publication of its audited annual results for the year ended 25 March 2026. The financial and portfolio highlights reported in the annual results are set out below.

Financial Highlights

% Change

2026

2025

• Rental Income*

Annual

7.0 %

£2,866,000

£2,679,000

Underlying

3.5 %

£2,117,000

£2,045,000

• Net Property Income

7.5 %

£2,024,000

£1,883,000

• Operating Income

Before fair value adjustment

4.6%

£2,024,000

£1,935,000

After fair value adjustment

17.3%

£3,072,000

£2,618,000

• Earnings per share (weighted average)

23.6%

71.8p

58.1p

• Dividends per share, paid and proposed

5.6%

28.5p

27.0p

• Net asset value per share

3.8%

1,212p

1,168p

• Loan to value ratio

23.8%

23.3%

• Total Accounting Return for the year►

6.2%

5.1%

* Annual Rental Income is shown in note 2 of the Financial Statements and Underlying Rental Income is the like-for-like income in those years from properties held in the portfolio throughout the period 2022 - 2026

► Total accounting return is calculated by combining movements in net asset value and dividends for the period expressed as a percentage of the opening net asset value per share.

Portfolio highlights

· Portfolio valuation increased by 2.9%, on a like-for-like basis, to £44.17 million.

· Total portfolio value rose to £46.97 million, including the five industrial units at Cambridge acquired in-year and the unit at Weston-super-Mare held for sale.

· Weston-super-Mare property sold post year end for £665,000: an uplift of 35.7% over net book value in March 2025 valuation.

· 18 new leases completed: three open market lettings and 15 lease renewals, with aggregate annual rent reserved of c. £614,000 per annum, representing a 4.4% increase over the estimated rental value in March 2025 valuation.

· The 15 lease renewals, with 9 break options not exercised in the year, demonstrate strong tenant retention.

· Portfolio fully let at year-end, other than one unit under offer and open land marketed for open storage.

· 100% rent collection for the year.

· Continued focus on energy performance and refurbishment projects expected to deliver clear benefits in terms of both future rental income and capital value.

Commenting on the results, the Chairman Philip Collins, said:

"I am delighted to report on another good year for our shareholders. Wynnstay's portfolio continues to deliver growth in revenue and capital value which are reflected in our increased dividend payments and net asset value per share, and thus in total accounting return, for shareholders."

Managing Director, Chris Betts, added:

"We have delivered very satisfactory performance from our property investments and operations over the past year, reflecting disciplined asset management, strong tenant demand and continued focus on portfolio quality. The year saw a high level of leasing activity, with good outcomes in terms of increased rental income, high tenant retention and virtually full occupancy."

The Annual Report and Financial Statements is available on the Company's website www.wynnstayproperties.co.uk and will shortly be posted to those shareholders who have elected to receive documents by post, when a further announcement will be made.

Attached to this announcement are the following sections from the Annual Report and Financial Statements: Who We Are; Our Performance; Chairman's Statement; Managing Director's Review; the Financial Statements and the notes to those statements.

As stated in the note at the end of the attachment, the financial information set out therein does not constitute statutory accounts as defined in section 435 of the Companies Act 2006.

The Company's Annual General Meeting ("AGM") will be held on Wednesday 15 July 2026. Details of the arrangements for the meeting are set out in the notice of meeting in the Annual Report and Financial Statements.

This announcement was approved by the Board on 16 June 2026.

For further information please contact:

Wynnstay Properties PLC

Philip Collins (Chairman)

Chris Betts (Managing Director)

Ph: 07469 042389

Zeus (Nominated Adviser and Broker)

Darshan Patel, Mike Coe, Alex Slater

Ph: 020 3829 5000

LEI number is 2138006MASI24JYW5O76.

For more information on Wynnstay visit: www.wynnstayproperties.co.uk

WHO WE ARE

Company Profile

Wynnstay is a long-established, successful property company with a distinctive approach to commercial property investment and development. We aim to generate rising dividend income and achieve capital appreciation for shareholders over the medium to long-term. The Company is AIM quoted and our principal shareholders are private investors.

The portfolio is directly, rather than externally, managed and has been built incrementally, with opportunities being taken to dispose of assets as and when the time is appropriate and to reinvest in assets that offer better long-term returns. This is achieved gradually over time, without the need for deal-driven activity in pursuit of corporate or portfolio expansion.

Management is remunerated by salary and, where appropriate, with a cash bonus. The executive team and the Board are focused on Wynnstay's performance for the benefit of shareholders; operational costs are closely controlled; and dilution of shareholders' investment and potential conflicts of interest are minimised.

We adopt a prudent, pragmatic approach to finance. Investments are funded in part by retained profits and recycling capital receipts from disposals and in part from borrowings, the majority at a fixed rate and held at a modest loan-to-value level, from an experienced and supportive property lender.

Property Strategy

Wynnstay invests in a diversified and resilient commercial property portfolio in Southern and Central England. We recognise that commercial property is a cyclical market that can exhibit significant upward and downward movements. Steadiness and progression over the medium and long-term are most likely to be in the shareholders' interests.

The portfolio is currently focused on light industrial and trade-counter warehouses with diversity and resilience being reflected in the location, number and nature of the properties, and the mix of lease terms, tenants and uses.

We invest in locations where there is strong occupational demand and often limited supply to provide opportunities for further rental growth over time and maintain high levels of occupancy. We prefer rents to be based on market rates rather than indexation.

Our properties are generally flexible and adaptable, therefore appealing to a broad spread of occupiers. Uses include manufacturing and services; storage and distribution; and trade counter and out-of-town retail. As a result, our income is secured upon a wide range of occupiers across the private and public sectors, from large corporates to sole traders.

Most properties are multi-let, resulting in a number of individual tenancies in many locations, reducing exposure to any single tenant and risk of loss of rental income in the case of defaults and voids. Short-term agreements of two years or less are typically avoided.

Active direct management, close engagement and constructive business relationships with tenants, over time, underpin capital value and increase income. Flexibility in addressing tenant needs and requirements generally means that the terms agreed result in a mutually beneficial outcome for both parties, especially when many tenants have been in occupation for a considerable time.

As active owners with a long-term perspective, we explore opportunities to refurbish and improve properties and to carry out selective development.

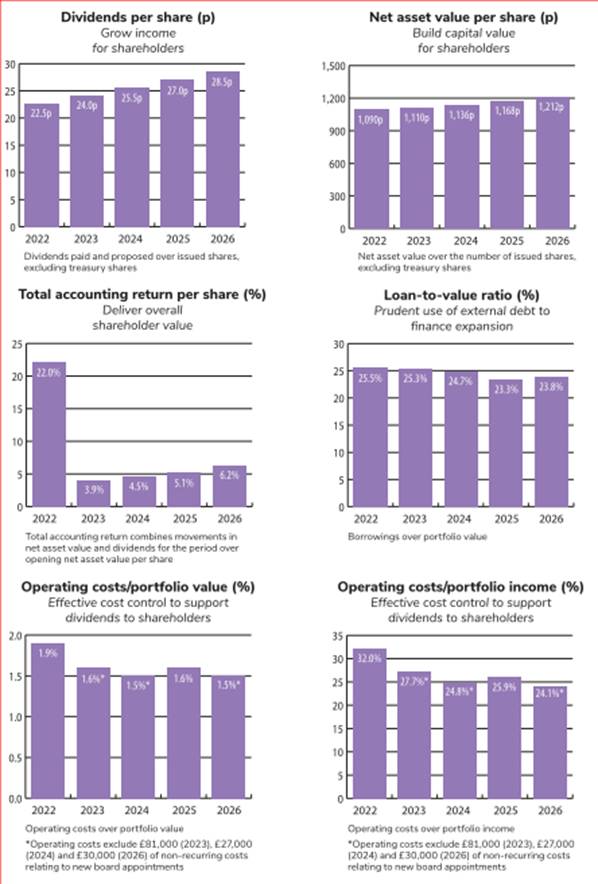

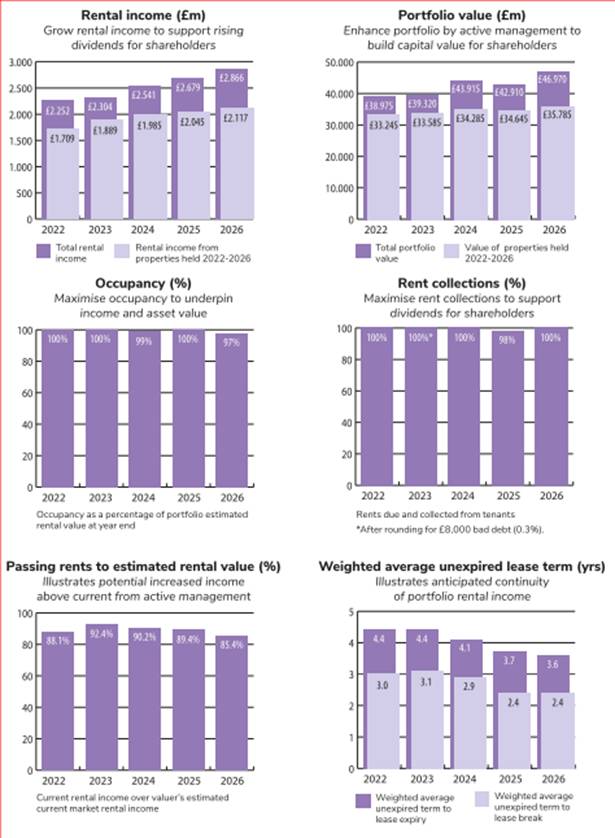

HOW WE HAVE PERFORMED

The charts below summarise how Wynnstay and its portfolio have performed over the past five years against the key performance indicators (KPI's) we have adopted in managing the business.

Our corporate performance

Our property performance

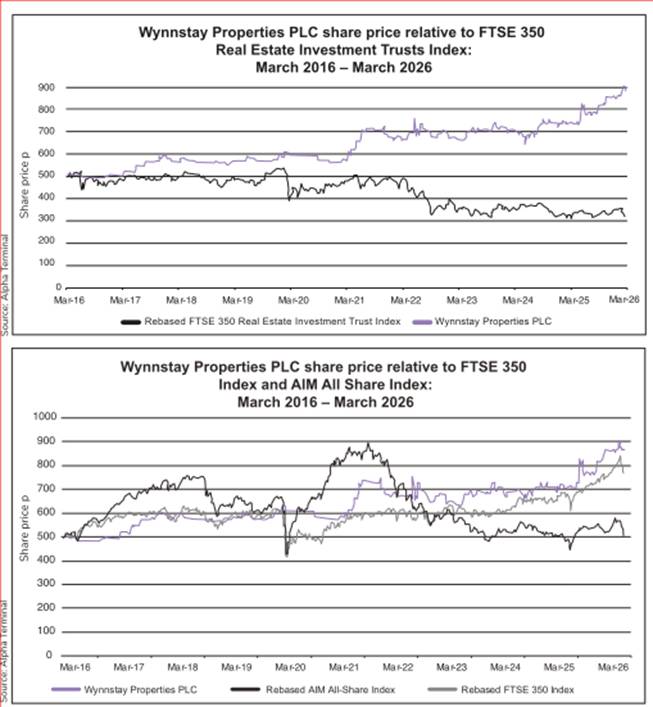

Our share performance

The charts below show that Wynnstay's share price has substantially outperformed the FTSE Real Estate Investment Trusts Index, the AIM All-Share Index and the FTSE 350 Index over the past ten years.

CHAIRMAN'S STATEMENT

I am delighted to report on another good year for our shareholders. Wynnstay's portfolio continues to deliver growth in revenue and capital value which are reflected in increased dividend payments and net asset value per share, and thus in total accounting return, for shareholders.

Wynnstay's overall financial performance in the financial year, compared to the prior year, is summarised in the overview table below. The table should be read in conjunction with the following commentary and the financial statements.

Overview of Financial Performance: 2026 vs. 2025

% Change

2026

2025

• Rental Income*

Annual

7.0 %

£2,866,000

£2,679,000

Underlying

3.5 %

£2,117,000

£2,045,000

• Net Property Income

7.5 %

£2,024,000

£1,883,000

• Operating Income

Before fair value adjustment

4.6 %

£2,024,000

£1,935,000

After fair value adjustment

17.3 %

£3,072,000

£2,618,000

• Earnings per share (weighted average)

23.6 %

71.8p

58.1p

• Dividends per share, paid and proposed

5.6 %

28.5p

27.0p

• Net asset value per share

3.8 %

1,212p

1,168p

• Loan to value ratio

23.8%

23.3%

• Total Accounting Return for the year►

6.2%

5.1%

* Annual Rental Income is shown in note 2 of the Financial Statements and Underlying Rental Income is the like-for-like income in those years from properties held in the portfolio throughout the period 2022 - 2026

► Total accounting return is calculated by combining movements in net asset value and dividends for the period expressed as a percentage

of the opening net asset value per share.

Commentary on Financial Performance in 2026

Rental income for the financial year increased by 7.0% compared to the previous year to £2,866,000 (2025: £2,679,000). This increase reflects previously reported changes in the portfolio, following disposal of the Cosham and Midhurst properties in the prior year and the acquisition of the industrial units in Waterbeach, Cambridge at the end of May 2025, and the benefit of a significant number of successful rent reviews and new lettings concluded during the year.

Other property income of £24,000 (2025: £14,000) comprised service charge related management fees.

Net property income rose to £2,024,000 (2025: £1,883,000) reflecting the higher property income noted above and property costs of £149,000 (2025: £113,000) and administrative costs of £717,000 (2025: £697,000) in the financial year compared to the prior year. Property costs were higher compared to the prior year as a result of the legal and agents' fees arising from the high level of leasing activity in the portfolio on which we report in the Managing Director's Review below.

As there were no disposals of assets in the year, no capital profits were realised (2025: £52,000). The fair value adjustment arising from the annual revaluation, was £1,048,000 (2025: £683,000). Earnings per share rose by 23.6% to 71.8p per share (2025: 58.1p per share).

As a result of the fair value adjustment arising from the valuation and the positive income generation in the business, net asset value per share rose by 3.8% to 1,212p per share (2025: 1,168p).

Valuation

Our Independent Valuers, BNP Paribas Real Estate, undertook the annual revaluation as at 25 March 2026 valuing the Company's portfolio at £46.970 million (2025: £42.910 million). This represents a 2.9% increase of £1.260 million on the like- for- like valuation of all properties held as at 25 March 2025 and primarily reflects the benefits of the active management of the portfolio reported in the Managing Director's Review.

Finance, Borrowings and Gearing

Wynnstay remains in a strong financial position, with a low loan-to-value ratio under our secured facilities of 23.8% (2025: 23.3%).

At the year-end, we held cash of £0.539 million (2025: £1.732 million) and our borrowings were £11.190 million (2025: £9.977 million). The reduction in cash held and the increase in our borrowing compared to the prior year resulted from our acquisition at Waterbeach, Cambridge. During the year, we repaid £400,000 initially borrowed under our revolving credit facility for this acquisition.

The interest rate under our Fixed Rate Facility is fixed at 3.61% until December 2026. In addition to our available cash balance and positive cash flow from our property activities, just under £4 million of our £5 million Revolving Credit Facility was undrawn at year-end.

Our current loan facilities expire in December 2026 and, as a result, our borrowings at the year-end are shown this year as current, rather than non-current, liabilities in our Statement of Financial Position. I am pleased to report that following discussions with our established lender, Handelsbanken PLC, it has confirmed that it has obtained credit approval and is willing in principle, subject to contract, satisfactory due diligence and agreement on documentation to increase the amount of our overall borrowing to a total of £20 million and accordingly has issued indicative term sheets for new facilities to us. The new facilities comprise two new Term Loan Facilities of £12 million and £3 million respectively and a new Revolving Credit Facility of £5 million. The new fixed term facilities will be available for drawdown for a period of six months from the signature of documentation and will be for a term of six years and one month, i.e. until January 2033. The Revolving Credit Facility is subject to market conditions on issue and will be available for drawdown for a period of five years from signature of documentation. We intend to drawdown under the new £12 million Term Loan Facility to refinance the existing £10 million facility and any drawings under the existing Revolving Credit Facility on or before their expiry on 17 December 2026. We will consider drawdowns under the £3 million Term Loan Facility and the Revolving Credit Facility as our future business needs require.

Dividend

Over many years we have sought to pursue a progressive dividend policy that aims to provide shareholders with a rising income commensurate with Wynnstay's underlying growth and finances.

In the light of the satisfactory results for the year, the Board recommends a final dividend of 18.0p per share (2025: 17.0p). An interim dividend of 10.5p per share (2025: 10.0p) was paid in December 2025. Hence, the total dividend for this year of 28.5p per share (2025: 27.0p) represents an increase of 5.6% on the prior year.

Subject to shareholder approval, the final dividend will be paid on 31 July 2026 to shareholders on the register at the close of business on 26 June 2026.

Wynnstay's Financial Performance in the longer-term

In the Annual Report four years ago, we introduced a new section, entitled Introduction to Wynnstay. This described Wynnstay's distinctive approach to commercial property investment primarily for private shareholders and provided information both on the Company's performance and its share price performance relative to market indices over time.

This year we have refreshed the front end of the Annual Report, dividing the former Introduction into two sections: "Who we are" and "How we have performed".

I encourage all shareholders to read this explanation of Wynnstay's rationale and performance in this report which highlights Wynnstay's continued strength over time, both in absolute terms and relative to the stock market, across a range of measures.

Key performance indicators to which I would draw shareholders attention are illustrated in the charts in the Annual Report. In managing the portfolio, we have achieved substantial underlying growth in rental income and portfolio value and maintained a consistent record of full occupancy and rent collections. Furthermore, as illustrated in the charts in the Annual Report, Wynnstay's share price has substantially outperformed established market indices for the quoted real estate sector over the past ten years.

Shareholder Communications

In my recent statements, I have reported that our annual Board self-evaluation had identified the importance of ensuring the effectiveness of the Company's communications with shareholders and potential investors and on various steps that we have taken in this regard, including the complete redesign of the website and our decision to use an online platform, Investor Meet Company, to supplement our regular reports and to provide an additional venue for questions to be put to us.

Two of these online presentations were made in July 2025 and November 2025. I am pleased to report that these presentations were well received: all but one of the attendees who offered comments provided positive responses. Shareholders were advised earlier this month that a further presentation will be made on the day of publication of this Annual Report. All the presentations are available on the Investor Meet Company platform (www. investormeetcompany.com) as well as through our website (www.wynnstayproperties.co.uk).

We also continue to encourage shareholders with individual enquiries to contact us, whether by letter to our registered office or by email (company.secretary@wynnstayproperties.co.uk).

This year we have made further changes to the Annual Report and enhanced the linkage between the printed report and the Company's website, for instance through the photographs of the portfolio on the inside covers of the report. Other changes to the content of this year's report follow the adoption of the revised Quoted Companies Alliance (QCA) Corporate Governance Code.

Our Share Register

As I have noted in previous statements, Wynnstay has a small, and rather unusual, share register on which there are around 240 accounts representing through nominee accounts around 300 shareholders, a significant number of which are connected through family relationships and are private investors rather than funds or institutions. In the main, they are long-term investors with some holdings having passed from generation to generation since the Company was founded in 1886. These long-term investors provide stability and continuity within the shareholder base.

As a result of this relatively small shareholder base the volume and proportion of Wynnstay shares traded in the market is less than for many quoted companies with larger share registers and more dispersed holdings. Fewer Wynnstay shares tend to be available to trade and then only usually in modest quantities and with a sizeable "spread" between the bid and offer prices. Shares are typically traded at a discount to the net asset value per share, although this discount has reduced significantly over the past year. This discount is also seen in other, much larger, quoted property companies.

Outlook

Economic growth has remained subdued, impacted by several geopolitical events and, in the UK, increased costs levied on business, higher cost of living for consumers and uncertainty about the direction and implementation of various important government policies. Until the end of February 2026, inflation was expected to fall to the Bank of England's target rate of 2% by the end of the year and the Bank's base rate was expected to fall in several steps to around 3-3.25%.

However, with the Middle East crisis starting in March, these expectations have been nullified, with inflation now forecast to increase over the remainder of the calendar year and leading to the prospect of rising, rather than falling, interest rates. Following the local election results in May, we have also entered a new period of domestic political turmoil in the UK. These economic and political uncertainties affect both business and consumer confidence.

Wynnstay's performance has proved to be resilient in past periods of economic uncertainty and the Board remains confident that our focused, stable and well-let portfolio can continue to deliver growth of capital and income for shareholders in the medium and long-term.

Board Succession

Succession planning is a current priority for the Board. With the anticipated retirement of several Directors, including the Chairman, the Board has, after consideration of the skills, experience and independence required for the next stage of the Company's development, commenced a process to appoint a new independent Chairman and, following that appointment, new independent Non-Executive Directors, using Forrester & Partners, a specialist external recruitment firm in the commercial property sector. The Board has delegated oversight of this process to an ad hoc committee of the Board, which reports with recommendations to the full Board. Announcements will be made as appointments are confirmed. The Board considers that this orderly process is consistent with the QCA Code's expectation that board membership be periodically refreshed.

Colleagues and Advisers

Our Managing Director, Chris Betts, and his team have continued to manage Wynnstay's business and the portfolio over the year and deliver value for shareholders. I would like to thank them, as well as my colleagues on the Board and our professional advisers, for their support over the year.

Annual General Meeting

There are two matters regarding the forthcoming Annual General Meeting to which I must draw shareholders' attention.

First, under the revised QCA Corporate Governance Code, Directors are expected to offer themselves for re-election to the Board each year rather than retiring and standing for re-election by rotation as has been the common practice under established company law and our articles of association. Accordingly, at the Annual General Meeting, resolutions are being proposed for the re-election of all the Directors.

Second, for many years resolutions have been proposed and passed by the requisite majority to grant authority for the Directors to issue a limited number of shares without first offering them to existing shareholders. These resolutions are intended to provide the Company with flexibility, for instance, to issue shares for small fundraisings which might support a larger acquisition or allow the issue of shares to vendors as part consideration on individual property acquisitions, where such vendors wish to retain an interest in a broader portfolio of assets in a quoted company. Bringing new investors to the share register with an interest in commercial property and in Wynnstay's distinctive approach would broaden the shareholder base and support its future development.

At the Annual General Meeting in July 2025, one of the two resolutions relating to the grant of such authority was not passed by a small margin. The Board had engaged with two significant shareholders at prior meetings on these resolutions and did so again at last year's Annual General Meeting. Their reasons for opposing the resolutions appear to relate to the liquidity in the market generally for purchase of the Company's shares and, if the authority were to be exercised, the potential dilution of their existing holdings resulting from any such issue of shares.

Liquidity in the market for the Company's shares is not a matter that is in Wynnstay's control, save where it may be possible to buy back shares in the market where there is an excess of sellers over buyers and it is in shareholders' interests to do so.

As regards potential dilution, it should be noted that resolutions of this nature are included as a matter of standard practice by most quoted companies in the UK. On 4 November 2022, the Financial Reporting Council issued the Statement of Principles on Disapplying Pre-Emption Rights on behalf of the Pre-Emption Group in relation to this subject. This Statement of Principles provides guidance on the factors to be considered by companies and investors when considering the case for disapplying pre-emption rights and sets out the circumstances where such disapplication might be appropriate.

It should be noted that the authority sought by the Company by resolution 12 is limited to either a new issue of shares for cash or transfer of shares out of treasury, in an amount, in aggregate, equal to five per cent. of the Company's entire issued share capital, such levels being significantly lower than those permitted by the Statement of Principles (being up to 10 per cent and, for an announced acquisition or specified capital investment, up to 20 per cent in aggregate).

The Company has also taken advice on the scope and drafting of resolution 12. As a result of that advice, the resolution proposed this year is shorter and simpler than last year. Although many quoted companies seek authority to provide for practical flexibility in fundraising from shareholders, our resolution no longer provides for a general disapplication of pre-emption to address various practical

issues that arise on a rights issue or pre-emptive offer of shares. It seems unlikely at the present time and in current market conditions that Wynnstay would seek to raise further funding in this way. If the Company wishes to do so in future, shareholders would be invited to grant the necessary authority at that time. Resolution 12 is thus now specifically limited to a single, simple disapplication of pre-emption capped at 5% of entire issued share capital.

The Directors have not used the authority when it has been granted previously and there is at present no transaction in contemplation where the authority might be used if granted now. However, the Directors consider that the proposed disapplication of pre-emption rights is desirable to give the Company the ability to issue a limited number of shares for cash to third parties, where to do so would be of benefit to the Company and in the best interests of shareholders generally at that time. In previous years there have been potential share-for-asset acquisitions where the use of the authority might have been considered for the reasons explained above. Although none are currently in contemplation, such potential transactions might well arise in the ordinary course of business in the future and it is therefore desirable for the Directors to be granted this authority. I would emphasise that the authority would only be exercised in circumstances that the Directors considered to be in the best interests of all shareholders.

The AGM provides an important and valued opportunity for the Board to engage with shareholders. Our AGM this year will be held at 2.00 pm on Wednesday 15 July 2026 at the Royal Automobile Club, 89 Pall Mall, London SW1Y 5HS. The Notice of Meeting is to be found at the end of this Annual Report.

The Board recommends all shareholders to vote in favour of all the resolutions to be proposed at the Annual General Meeting. Shareholders are urged to complete and return their proxy forms as soon as practicable so that their votes on the resolutions being put to the meeting can be counted.

Shareholders who have registered for Investor Centre online with our Registrars can also benefit from the ability to cast their proxy votes electronically, rather than by post. Shareholders not already registered for Investor Centre online will need their investor code, which can be found on their share certificate or dividend tax voucher, in order to register.

To maximise shareholder engagement, shareholders who are unable to attend the AGM are encouraged to submit in writing those questions that they might have wished to ask in person at the meeting. Questions should be emailed to company.secretary@wynnstayproperties.co.uk at least 48 hours in advance of the AGM. You will receive a written response and, if there are common themes raised by a number of shareholders, we aim to provide a summary for all shareholders, grouping themes and topics together where appropriate, on the Company's website following the AGM.

Finally, on behalf of the Board, I extend a warm welcome to shareholders who have recently acquired their Wynnstay shares; and express appreciation to the large body of shareholders who have held their shares often over many years for their continued investment in Wynnstay.

Philip Collins

Chairman

16 June 2026

MANAGING DIRECTOR'S REVIEW

We have delivered very satisfactory performance from our property investments and operations over the past year, reflecting disciplined asset management, strong tenant demand and continued focus on portfolio quality.

Portfolio Composition

As previously reported, a property was acquired in Waterbeach, Cambridge in May 2025 at a total cost of approximately £2.950 million, adding rental income of £183,000 per annum. No property sales were completed during the year.

Post Year‑End Property Disposal

We contracted to sell the Weston‑super‑Mare property at auction on 24 March 2026, completing the disposal on 24 April 2026. A five‑year lease renewal was agreed with Majestic Wine, the sole tenant of this stand‑alone unit, in February 2026, which materially enhanced the property's value. Given limited prospects for further rental growth, the Board considered that value was optimised by selling at this point. Competitive bidding resulted in a sale price of £665,000, representing a 35.7% uplift over the net book value of £490,000 as at 25 March 2025.

Portfolio Activity

The financial year saw a high level of leasing activity, with 18 new leases completed. Three were open‑market lettings to new tenants, while the remaining 15 were renewals with existing occupiers, demonstrating strong tenant retention across the portfolio. The aggregate annual rent reserved under these leases amounts to almost £614,000 per annum, representing a 4.4% increase over the estimated rental values used in the March 2025 valuation. In no instance was rent agreed below valuers' estimates.

One lease that expired during the year remains subject to negotiations with the occupier on revised terms. Nine leases were subject to tenant break options, none of which were exercised, resulting in rental income being maintained.

There were three vacancies during the year. One small unit in Hailsham was successfully re‑let in January. The unit and adjoining parcel of open storage land in Liphook, formerly let to Network Rail, have remained vacant following lease expiry at the end of February 2026. Together, these two elements represent 2.7% of the total portfolio estimated rental value used in the March 2026 valuation. The unit is under offer, and the land is being marketed for open storage use.

There was only one instance of rent arrears during the year, being £3,202 written off in respect of the small Hailsham unit prior to its re‑letting, as previously reported at the interim stage.

Portfolio Valuation

As in the prior year, property investment markets have remained focused on the timing and scale of interest‑rate reductions, expectations of which have been tempered by geopolitical developments, including the Middle East crisis. Yields have generally remained static, with valuation movements driven primarily by leasing activity, lease expiries, break options and rental growth.

On a like‑for‑like basis, excluding the Cambridge acquisition, the total estimated rental value adopted by the valuers increased by 2.2%. On the same basis, the market capital value increased by 2.9% to £44.170 million, underpinned by new leases secured during the year and the expiry of tenant break options.

Potential Infill Development

As outlined in the interim report, the Company has been exploring the development of six new units on surplus land in Liphook, Aylesford and Ipswich. Planning permission has now been secured at all three sites, providing for approximately 11,200 sq ft of new lettable space, broadly evenly distributed. However, updated advice indicates that construction costs have increased at a faster pace than projected rental growth, resulting in returns that are marginal relative to capital risk. While the Board does not currently consider progression of the schemes to be in shareholders' best interests, these opportunities will continue to be monitored.

Energy Performance Certificates

The industry continues to await clarity from government regarding the next phase of Minimum Energy Efficiency Standards. While a minimum EPC rating of C by the end of 2027 remains likely, it is not yet clear whether this will apply only to new transactions or also to existing leases.

Following a review of properties currently below this threshold, and taking account of improvements already completed by the Company and tenants, fresh EPCs are in the process of being lodged which would result in over 55% of units achieving a C rating or above.

The remaining units have been assessed and works identified to achieve a minimum C rating over the next 18 months. Typically, this involves the removal of gas‑fired heating in favour of air‑source heat pumps, together with upgraded LED lighting. A budget of £210,000 has been incorporated into our financial plans to deliver compliance by December 2027. In several cases, these improvements are expected to result in a B rating.

Refurbishment Expenditure

In addition to energy efficiency initiatives, planned capital expenditure includes refurbishment works at Liphook and Heathfield. Particular focus is being given to the replacement or over‑cladding of ageing asbestos cement sheet roofs, typically 40-50 years old, where repair is no longer viable.

Our energy performance and refurbishment projects are expected to deliver clear benefits in terms of both rental income and capital value in the future.

Chris Betts

Managing Director

16 June 2026

STATEMENT OF COMPREHENSIVE INCOME FOR YEAR ENDED 25 MARCH 2026

Notes

2026

2025

£'000

£'000

Property Income

2

2,890

2,693

Property Costs

3

(149)

(113)

Administrative Costs

4

(717)

(697)

Net Property Income

2,024

1,883

Movement in Fair Value of

Investment Properties

10

1,048

683

Profit on Sale of Investment Property

-

52

Operating Income

3,072

2,618

Investment Income

6

24

37

Finance Costs

6

(498)

(480)

Income before Taxation

2,598

2,175

Taxation

7

(662)

(608)

Profit after Taxation and Total Comprehensive Income

1,936

1,567

Basic and diluted earnings per share

9

71.8p

58.1p

The Company has no items of other comprehensive income.

STATEMENT OF FINANCIAL POSITION 25 MARCH 2026

2026

2025

Notes

£'000

£'000

Non-Current Assets

Investment Properties

10

46,305

42,910

Investments

12

3

3

46,308

42,913

Current Assets

Trade and Other Receivables

14

300

344

Cash and Cash Equivalents

539

1,732

839

2,076

Non-current Assets held for Sale

15

665

-

1,504

2,076

Current Liabilities

Trade and Other Payables

16

(934)

(825)

Income Taxes Payable

(377)

(355)

Bank Loans Payable

17

(11,190)

-

(12,501)

(1,180)

Net Current (Liabilities) / Assets

(10,997)

896

Total Assets Less Current Liabilities

35,311

43,809

Non-Current Liabilities

Bank Loans Payable

17

-

(9,977)

Deferred Tax Payable

18

(2,623)

(2,339)

(2,623)

(12,316)

Net Assets

32,688

31,493

Capital and Reserves

Share Capital

19

789

789

Capital Redemption Reserve

205

205

Treasury Shares

(1,732)

(1,732)

Share Premium Account

1,135

1,135

Retained Earnings

32,291

31,096

32,688

31,493

Net Asset Value pence per share

1,212p

1,168p

Approved by the Board and authorised for issue on 16 June 2026

P.G.H. Collins C.G. Betts

Director Director

Registered number: 00022473

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 25 MARCH 2026

2026

2025

£'000

£'000

Cash flows from operating activities

Income before taxation

2,598

2,175

Adjusted for:

(Increase) in fair value of investment properties

(1,048)

(683)

Interest receivable

(24)

(37)

Interest and finance costs payable

498

480

Profit on sale of investment property

-

(52)

Amortised loan fees

-

34

Changes in:

Decrease in trade and other receivables

44

69

Increase/(decrease) in trade and other payables

109

(3)

Increase in income taxes payable

21

8

Cash generated from operations

2,198

1,991

Income taxes charged

(377)

(352)

Net cash generated from operating activities

1,821

1,639

Cash flows from investing activities

Interest and other income received

24

37

Purchase of investment properties

(3,012)

(42)

Sale of investment properties

-

1,782

Net cash (used in) / generated from activities

(2,988)

1,777

Cash flows from financing activities

Interest paid

(485)

(480)

Dividends paid

(741)

(701)

Drawdown of bank loans net of fees

1,600

-

(Repayment) of bank loans net of fees

- Note 1 below(400)

(900)

Net cash used in financing activities

(26)

(2,081)

(Decrease)/increase in cash and cash equivalents

(1,193)

1,335

Cash and cash equivalents at beginning of period

1,732

397

Cash and cash equivalents at end of period

539

1,732

Note 1: RECONCILIATION OF LIABILITIES ARISING FROM FINANCE ACTIVITIES

£'000

Balance at 26 March 2024

10,843

Cash flows

(900)

Other non-cash items

34

Balance at 25 March 2025 and 26 March 2025

9,977

Cash flows

1,200

Other non-cash items

13

Balance at 25 March 2026

11,190

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 25 MARCH 2026

YEAR ENDED 25 MARCH 2026

Share

Capital

Capital

Redemption

Reserve

Share

Premium

Account

Treasury

Shares

Retained

Earnings

Total

£'000

£'000

£'000

£'000

£'000

£'000

Balance at 26 March 2025

789

205

1,135

(1,732)

31,096

31,493

Total comprehensive

income for the year-

-

-

-

1,936

1,936

Dividends - note 8

-

-

-

-

(741)

(741)

Balance at 25 March 2026

789

205

1,135

(1,732)

32,291

32,688

YEAR ENDED 25 MARCH 2025

Share

Capital

Capital

Redemption

Reserve

Share

Premium

Account

Treasury

Shares

Retained

Earnings

Total

£'000

£'000

£'000

£'000

£'000

£'000

Balance at 26 March 2024

789

205

1,135

(1,732)

30,230

30,627

Total comprehensive

income for the year-

-

-

-

1,567

1,567

Dividends - note 8

-

-

-

-

(701)

(701)

Balance at 25 March 2025

789

205

1,135

(1,732)

31,096

31,493

Explanation of Capital and Reserves:

· Share Capital: This represents the subscription, at par value, of the Ordinary Shares of the Company.

· Capital Redemption Reserve: This represents money that the Company must retain when it has bought back shares, and which it cannot pay to shareholders as dividends: It is a non-distributable reserve and represents paid up share capital.

· Share Premium Account: This represents the subscription monies paid for Ordinary Shares of the Company in excess of their par value.

· Treasury Shares: This represents the total consideration and costs paid by the Company when purchasing the 458,650 shares as referred to in Note 19.

· Retained Earnings: This represents the profits after tax that can be used to pay dividends. However, dividends can only be paid from distributable reserves as detailed in the preceding table.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 25 MARCH 2026

1. BASIS OF PREPARATION, MATERIAL ACCOUNTING POLICIES AND ESTIMATES

Wynnstay Properties PLC is a public limited company incorporated and domiciled in England and Wales. The principal activity of the Company is property investment, development and management. The Company's ordinary shares are traded on the AIM, part of The London Stock Exchange. The Company's registered number is 00022473 and registered address is Riverbank House, 2 Swan Lane, London EC4R 3TT. The material accounting policies are summarised below.

1.1 Basis of Preparation

The financial statements have been prepared in accordance with UK adopted International Accounting Standards ("IAS"). The financial statements have been presented in Pounds Sterling being the functional currency of the Company and rounded to the nearest thousand. The financial statements have been prepared under the historical cost basis modified for the revaluation of investment properties and financial assets measured at fair value through Operating Income.

(a) New Interpretations and Revised Standards Effective for the year ended 25 March 2026

The Directors have adopted all new and revised IFRS Accounting Standards that are relevant to the Company and effective for accounting periods beginning on or after 26 March 2025. No new or amended standards effective in the year had a material impact on the disclosures or presentation of the financial statements.

(b) Standards and Interpretations in Issue but not yet Effective

The following IFRS Accounting Standard is effective for periods after 26 March 2026 and is considered potentially to have a material impact:

• IFRS 18 Presentation and Disclosure in Financial Statements

The Company does not expect any other new or amended standards not yet effective to have a material impact on the financial statements.

(c) Going concern

The financial statements have been prepared on a going concern basis. This requires the Directors to consider, as at the date of approving the financial statements, that there is reasonable expectation that the Company has adequate financial resources to continue to operate, and to meet its liabilities as they fall due for payment, for at least twelve months following the approval of the financial statements.

The Directors have reviewed cash balances and borrowing facilities to cover at least twelve months of operations, including the refinancing arrangements described in Note 17, financing costs and continuation of employment and advisory costs as currently contracted without any reduction for cost saving initiatives. The results of the review show that the Company will have cash and borrowing facilities to cover at least twelve months of operations, and that the Company will satisfy the financial covenant ratios in the borrowing facilities as described in Note 17. In addition, the Statement of Financial Position as at 25 March 2026 shows that the Company had a cash balance of £0.539 million (2025: £1.732 million), an undrawn Revolving Credit Facility of £3.800 million (2025: £5.000 million), net assets of £32.688 million (2025: £31.493 million), and a gearing ratio of 33% (2025: 26%). In the light of the foregoing considerations, the Directors consider that the adoption of the going concern basis is reasonable and appropriate.

1.2 Accounting Policies

Investment Properties

All the Company's investment properties are independently revalued annually and stated at fair value as at 25 March. The aggregate of any resulting increases or decreases are taken to Operating Income within the Statement of Comprehensive Income. The basis of independent valuation is described in Note 10.

Investment properties are recognised as acquisitions or disposals based on the date of contract completion.

Assets held for sale

Non-current assets are classified as held for sale if their carrying amount will be recovered through a sale transaction rather than through continuing use. This condition is regarded as met only when the sale is highly probable, and the asset is available for immediate sale in its present condition. Management must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year from the date of classification. Non-current assets classified as held for sale are measured at the lower of the assets' previous carrying amount or fair value less cost to sell.

Depreciation

In accordance with IAS 40 investment properties are included in the Statement of Financial Position at fair value and are not depreciated.

Disposal of Investments

The gains and losses on the disposal of investment properties and other investments are included in Operating Income in the year of disposal. Gains and losses are calculated on the net difference between the carrying value of the properties and the net proceeds from their disposal.

Rental Income

Rental income is recognised on a straight-line basis over the period of the lease and is measured at the fair value of the consideration receivable. Lease deposits are held in separate designated deposit accounts and are thus not treated as assets of the Company in the financial statements. All income is derived in the United Kingdom. When there are changes to a tenancy agreement it is considered whether any lease incentives were given. Lease incentives are amortised on a straight line basis over the lease term.

Deferred Income

Deferred Income arises from rents received in advance of the period. See Note 16.

Taxation

Current and deferred tax are recognised and measured in accordance with IAS 12. The Company provides for deferred tax on investment properties by reference to the tax that would be due on the sale of the investment properties.

Trade and Other Accounts Receivable

All receivables do not carry any interest and are short term in nature.

Cash and Cash Equivalents

Cash and cash equivalents comprise cash at bank and on demand deposits.

Trade and Other Accounts Payable

All trade and other accounts payable are non-interest bearing.

Pensions

Defined pension scheme contributions are charged to the Statement of Comprehensive Income as incurred.

Borrowings

Borrowings are classified as current liabilities unless the Company has a right to defer settlement of the liability at the end of the reporting period for at least 12 months and are measured at amortised cost.

Dilapidations

Dilapidations receipts are recognised in the Statement of Comprehensive Income when the right to receive them arises. They are recorded in revenue as other property income unless a property has been agreed to be sold whereby the receipt is treated as part of the proceeds of sale of the property. See Note 2.

1.3 Key Sources of Estimation Uncertainty and Judgements

The preparation of the financial statements requires management to make judgements, estimates and assumptions that may affect the application of accounting policies and the reported amounts of assets and liabilities, income and expenses.

Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period. The key sources of estimation uncertainty that have a significant risk of causing material adjustment to the carrying amounts of assets and liabilities within the next financial year are those relating to the fair value of investment properties which are revalued annually by the Directors having taken advice from the Company's independent external valuers, on the basis described in Note 10. A key judgement taken by the Directors is as to whether a property is being held for sale.

There are no other judgemental areas identified by management that could have a material effect on the financial statements at the reporting date.

2. PROPERTY INCOME

2026

2025

£'000

£'000

Rental income

2,866

2,679

Other property income

24

14

2,890

2,693

Rental income comprises rents earned and apportioned over the lease period taking into account rent free periods and rents received during the period. Other property income comprises dilapidations payments received and miscellaneous income arising from the letting of properties.

3. PROPERTY COSTS

2026

2025

£'000

£'000

Property management

17

27

Legal fees

87

66

Agent fees

45

20

149

113

4. ADMINISTRATIVE COSTS

2026

2025

£'000

£'000

Rents payable - short term lease

-

1

General administration, including staff costs

635

651

Auditors' remuneration - audit fees

47

44

Tax services - Saffery LLP

5

1

Non-Recurring costs - costs relating to new Board appointments

30

-

717

697

5. STAFF COSTS

2026

2025

£'000

£'000

Staff costs, including Directors' fees, during the year were as follows:

Wages and salaries

316

303

Social security costs

42

34

Other pension costs

33

35

391

372

Further details of Directors' emoluments, totalling £320,000 (2025: £305,000), are shown under Directors' Emoluments in the Directors' Report and form part of these Financial Statements. There are no other key management personnel.

2026

2025

No.

No.

The average number of employees, including Non-Executive Directors, engaged wholly in management and administration

6

6

The number of Directors for whom the Company paid pension benefits

during the year was:

1

1

6. FINANCE COSTS (NET)

2026

2025

£'000

£'000

Interest payable and finance costs on bank loans

498

480

Less: Bank interest receivable

(24)

(37)

474

443

7. TAXATION

2026

2025

£'000

£'000

(a) Analysis of the tax charge for the year:

UK Corporation tax at 25% (2025: 25%)

Total current tax charge

377

352

Deferred tax - temporary differences

285

256

Tax charge for the year

662

608

(b) Factors affecting the tax charge for the year:

Income before taxation

2,598

2,175

Current Year:

Corporation tax thereon at 25% (2025: 25%)

649

544

Fixed asset differences

13

77

Capital gains net tax movement on disposals

-

-

Corporation tax adjustment for profit on disposals

-

(13)

Total tax charge for the year

662

608

8. DIVIDENDS

2026

2025

£'000

£'000

Final dividend for 2025 of 17.0p per share

(2025: Final dividend for 2024 of 16.0p per share)

457

431

Interim dividend paid in year of 10.5p per share

284

270

(2025: Interim dividend paid in year of 10.0p per share)

741

701

On 16 June 2026 the Board resolved to pay a final dividend of 18.0p per share which will be recorded in the Financial Statements for the year ending 25 March 2027.

9. EARNINGS PER SHARE

Basic and diluted earnings per share are calculated by dividing Income after Taxation and Total Comprehensive Income attributable to Ordinary Shareholders of £1,936,000 (2025: £1,567,000) by 2,696,617 shares which is the weighted average number of 2,696,617 (2025: 2,696,617) ordinary shares in issue during the period excluding shares held as treasury. There are no instruments in issue that would have the effect of diluting earnings per share.

10. INVESTMENT PROPERTIES

2026

2025

£'000

£'000

Properties

Balance at beginning of financial year

42,910

43,915

Additions

3,012

42

Disposals

-

(1,712)

Revaluation surplus

1,048

665

46,970

42,910

Transfer to Assets held for sale

(665)

-

Balance at end of financial year

46,305

42,910

Assets held for sale in 2026 represented a property which was contracted to be sold at an auction held on 24 March 2026 and the sale was completed on 24 April 2026: See Note 24.

The Company's freehold and one long-leasehold properties were valued as at 25 March 2026 by BNP Paribas Real Estate Advisory & Property Management UK Limited, RICS Registered Valuers, acting in the capacity of external valuers, and adopted by the Directors. The valuations were undertaken in accordance with the requirements of the RICS Valuation - Global Standards 2024, effective 31 January 2025, the International Valuation Standards and the UK National Supplement 2023, effective 1 May 2024 reissued January 2025.

The valuation of each property was on the basis of Fair Value. The valuers reported that the total aggregate Fair Value of the properties held by the Company was £46,970,000 (2025: £42,910,000).

The valuer's opinions were primarily derived from comparable recent market transactions on arms-length terms.

In the financial year ended 25 March 2026, the total fees earned by the valuer from Wynnstay Properties PLC and connected parties were less than 5% of the valuer's company turnover.

The valuation complies with International Financial Reporting Standards. The definition adopted by the International Accounting Standards Board (IASB) in IFRS 13 is Fair Value, defined as: 'The price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date.'

These recurring fair value measurements for non-financial assets use inputs that are not based on observable market data, and therefore, fall within level 3 of the fair value hierarchy.

The most pertinent market data observed reflected net initial yields which ranged from broadly 4.9% to 6.6% with equivalent yields estimated to range between broadly 5.3% and 7.1 % for the core industrial properties. The portfolio as a whole exhibits a net initial yield of 5.57 % (2025: 5.86%) and a nominal equivalent yield of 6.44% (2025: 6.40%).

There have been no transfers between levels of the fair value hierarchy. Movements in the fair value are recognised in profit or loss.

A 0.5% decrease in the weighted equivalent yield would result in a corresponding increase of £3.980 million (2025: £3.930 million) in the fair value movement through profit or loss. A 0.5% increase in the same yield would result in a corresponding decrease of £3.420 million (2025: £3.350 million) in the fair value movement through profit or loss.

11. OPERATING LEASES RECEIVABLE

2026

2025

The following are the future minimum lease payments receivable under non-cancellable operating leases which expire:

£'000

£'000

Not later than one year

295

440

Between 1 and 5 years

3,744

3,891

Over 5 years

5,172

2,507

9,211

6,838

Rental income under operating leases recognised through profit or loss amounted to £2,866,000 (2025: £2,679,000).

Typically, the properties were let for a term of between 5 and 10 years at a market rent with rent reviews every 5 years. The above maturity analysis reflects future minimum lease payments receivable to the next break clause in the operating lease. The properties are generally leased on terms where the tenant has the responsibility for repairs and running costs for each individual unit with a service charge payable to cover common services provided by the landlord on certain properties. The Company manages the services provided for a management fee and the service charges are not recognised as income in the accounts of the Company as any receipts are netted off against the associated expenditures with any residual balance being shown as a liability.

If the tenant does not carry out its responsibility for repairs and the Company receives a dilapidations payment, the resulting cash is recorded in revenue as other property income unless the payment is deployed on repairs to the premises or a property has been agreed to be sold where the receipt is treated as part of the proceeds of sale of the property. See Note 2.

12. INVESTMENTS

2026

2025

£'000

£'000

Quoted investments

3

3

13. SUBSIDIARY COMPANY

The Company has the following dormant subsidiary which the Directors consider immaterial to, and thus has not been consolidated into, the financial statements. The subsidiary holds the legal title to an access road to an investment property, the use of which is shared between the Company, its tenants at the property and neighbouring premises.

Scanreach Limited 80% owned Dormant Net Assets: £4,447 (2025: £4,447)

14. ACCOUNTS RECEIVABLE

2026

2025

£'000

£'000

Trade receivables

209

266

Other receivables

91

78

300

344

Trade receivables include an adjustment for credit losses of £3,000 (2025: £17,000). Any provision for impairment of trade receivables has been set against a specific tenant.

Trade receivables, which are the only financial assets at amortised cost, are non-interest bearing and generally have a 15-day term. Due to their short maturities, the carrying amount of trade and other receivables is a reasonable approximation of their fair value.

Of the trade receivables balance at the end of the year £28,643 (2025: £32,468) is due from the Company's largest tenant. There are seven other tenants who represent more than 5% of the total balance of trade receivables.

15. ASSETS HELD FOR SALE

2026

2025

Property held for sale

665

-

16. ACCOUNTS PAYABLE

2026

2025

£'000

£'000

Trade payables

65

120

Other creditors

168

4

Deferred income

605

590

Amount due to subsidiary

4

4

Accruals

92

107

934

825

The average credit period taken for trade purchases is 19 days (2025: 14 days). No interest is charged on the outstanding balances. The Directors consider that the carrying amounts of trade and other payables is a reasonable approximation of their fair value.

17. BANK LOANS PAYABLE

2026

2025

£'000

£'000

Current loans

11,190

-

Non current loans

-

9,977

In December 2021, a five-year Fixed Rate Facility of £10 million and a Revolving Credit Facility of £5 million were entered into providing a total committed credit facility of £15 million. Interest on loan amounts drawn down under the Fixed Rate Facility of £10 million (2025: £10 million) is charged at 3.61% per annum (2025: 3.61%) for the year ended 25 March 2026. Loan arrangement fees amortised over the loan period amounted to £13,000 (2025: £34,000). Loan amounts drawn down under the Revolving Credit Facility during the year amounted to £1,600,000 (2025: £nil). Interest on loan amounts drawn down under the Revolving Credit Facility is charged at variable rates. Loan amounts repaid under the Revolving Credit Facility during the year amounted to £400,000 (2025: £nil). Prior period net drawdowns of £nil were repaid in the current period (2025: £900,000) and the amortised balance drawn as at 25 March 2026 is £1,200,000 (2025: £nil).

Both facilities are repayable in one instalment on 17 December 2026. The facilities include the following financial covenants which were complied with during the year:

• Rental income shall not be less than 2.25 times the interest costs.

• The drawn balance shall at no time exceed 50% of the market value of the properties secured.

The facilities are secured by fixed charges over freehold land and buildings owned by the Company, which at the year-end had a combined value of £35,560,000 (2025: £34,645,000). The undrawn element of the facilities available at 25 March 2026 was £3,800,000 (2025: £5,000,000).

Interest charged under the Revolving Credit Facility is linked to Bank of England Base Rate as the reference rate.

As at 16 June 2026 the Company had received confirmation from its lender that it had obtained credit approval and is willing in principle, subject to contract, satisfactory due diligence and agreement on documentation to increase the amount of its overall borrowing to a total of £20 million and accordingly had issued indicative term sheets for new facilities to the Company. The new facilities comprise two new Term Loan Facilities of £12 million and £3 million respectively and a new Revolving Credit Facility of £5 million. The new fixed term facilities will be available for drawdown for a period of six months from the signature of documentation and will be for a term of six years and one month, i.e. until January 2033. The Revolving Credit Facility is subject to market conditions on issue and will be available for drawdown for a period of five years from signature of documentation. The Company intends to drawdown under the new £12 million Term Loan Facility to refinance the existing £10 million facility and any drawings under the existing Revolving Credit Facility on or before their expiry on 17 December 2026.

18. DEFERRED TAX

2026

2025

£'000

£'000

Deferred Tax brought forward

2,338

2,083

Charged for the year

285

255

Deferred Tax carried forward

2,623

2,338

A deferred tax liability of £2,623,000 (2025: £2,338,000) is recognised in respect of the unrealised gains in investment properties and has been calculated at a tax rate of 25% (2025: 25%).

19. SHARE CAPITAL

2026

2025

£'000

£'000

Authorised

8,000,000 Ordinary Shares of 25p each:

2,000

2,000

Allotted, Called Up and Fully Paid

3,155,267 Ordinary shares of 25p each:

789

789

All shares rank equally in respect of shareholder rights.

In March 2010, the Company acquired 443,650 Ordinary Shares of Wynnstay Properties PLC from Channel Hotels and Properties Ltd at a price of £3.50 per share. On 19 July 2022, shareholders granted authority to make market purchases of its shares for a period of five years from that date. Pursuant to this share buyback authority, in September 2022, the Company acquired 15,000 Ordinary Shares of Wynnstay Properties PLC at a price of £7.10 per share, representing less than 0.005 % of the issued share capital, with the aggregate consideration paid for the shares being £106,500. The total cost of establishing the share buyback authority, together with this acquisition, was £164,000. The total of 458,650 shares acquired, representing 14.5% of the total shares in issue, are held in treasury. As a result, the total number of shares with voting rights is 2,696,617.

20. FINANCIAL INSTRUMENTS

The objective of the Company's policies is to manage the Company's financial risk, secure cost-effective funding for the Company's operations and minimise the adverse effects of fluctuations in the financial markets on the value of the Company's financial assets and liabilities, on reported profitability and on the cash flows of the Company.

As at 25 March 2026 the Company's financial instruments comprised borrowings, cash and cash equivalents, quoted investments, short term receivables and short-term payables. The main purpose of these financial instruments was to raise finance for the Company's operations. Throughout the period under review, the Company has not traded in any other financial instruments. The Board reviews and agrees policies for managing each of the associated risks and they are summarised below:

Credit Risk

The risk of financial loss due to a counterparty's failure to honour its obligations arises principally in connection with property leases and the investment of surplus cash.

Tenant rent payments are monitored regularly, and appropriate action is taken to recover monies owed or, if necessary, to terminate the lease. The Company carefully vets prospective new tenants from a credit risk perspective. Bad debts are mitigated by close engagement with tenant businesses within a well-diversified mix of some 93 units across the portfolio and close monitoring of rental income receipts. The Company regularly reviews the portfolio, including feedback from engagement with tenants, in order to assess the risk of tenant failures. In addition, the Company obtains credit reports on significant tenants on a regular basis. Credit reports can be seen on all tenants upon request, but the focus of the Board is on the top 10 tenants by amount and any tenants showing delayed rent payments.

The Company has no significant concentration of credit risk associated with trading counterparties (considered to be over 5% of net assets) with exposure spread over a large number of tenancies. In terms of concentration of individual tenant's rents versus total gross annual passing rents the Company has 3 tenants whose rent, on an individual basis, is between 5.1% and 7.1% of total gross annual passing rents.

Funds are invested and loan transactions contracted only with banks and financial institutions with a high credit rating. Concentration of credit risk exists to the extent that as at 25 March 2026 and 2025 current account and short-term deposits were held with two financial institutions, Handelsbanken PLC and C Hoare & Co. The combined exposure to credit risk on cash and cash equivalents at 25 March 2026 was £539,000 (2025: £1,732,000).

Currency Risk

As all of the Company's assets and liabilities are denominated in Pounds Sterling, there is no exposure to currency risk.

Interest Rate Risk

The Company is exposed to interest rate risk that could affect cash flow as it currently borrows at both floating and fixed interest rates. The Company monitors and manages its interest rate exposure on a periodic basis but does not take out financial instruments to mitigate the risk. The Company finances its operations through a combination of retained profits and bank borrowings.

Liquidity Risk

The Company seeks to manage liquidity risk to ensure sufficient funds are available to meet the requirements of the business and to invest cash assets safely and profitably. The Board regularly reviews available cash balances and cash forecasts to ensure there are sufficient resources for working capital requirements and to maintain an adequate cash margin.

Interest Rate Sensitivity

Financial instruments affected by interest rate risk include loan borrowings and cash deposits. The analysis below shows the sensitivity of the statement of comprehensive income and equity to a 0.5% change in interest rates:

0.5% decrease

in interest rates

0.5% increase

in interest rates

2026

2025

2026

2025

£'000

£'000

£'000

£'000

Impact on interest payable - gain/(loss)

6

-

(6)

-

Impact on interest receivable - (loss)/gain

(3)

(9)

3

9

Total impact on pre-tax profit and equity

3

(9)

(3)

9

The calculation of the net exposure to interest rate fluctuations was based on the following as at 25 March:

2026

2025

£'000

£'000

Floating rate borrowings (bank loans)

1,200

-

Less: cash and cash equivalents

(539)

(1,732)

661

(1,732)

Carrying Amounts of Financial Instruments

Management believes the carrying amounts of most financial assets and financial liabilities on the balance sheet represent a reasonable approximation of their value. The classification and measurement of financial instruments are performed in accordance with IFRS 9 'Financial Instruments'. Exceptions to this approach, if any, are detailed below.

Fixed-Rate Borrowings

It is important to note that the carrying amounts of fixed-rate borrowings might not always reflect their fair value due to changes in market interest rates.

Financial assets

2026

2025

£'000

£'000

Quoted investments measured at fair value

3

3

Loans and receivables measured at amortised cost

209

264

Cash and cash equivalents measured at amortised cost

539

1,732

Total financial assets

751

1,999

Financial liabilities at amortised cost

11,190

9,977

Total liabilities

11,200

10,000

The only financial instruments measured subsequent to initial recognition at fair value as at 25 March are quoted investments. These are included in level 1 in the IFRS 13 fair value hierarchy as they are based on quoted prices in active markets.

Capital Management

The primary objectives of the Company's capital management are:

• to safeguard the Company's ability to continue as a going concern, so that it can continue to provide returns for shareholders; and

• to enable the Company to respond quickly to changes in market conditions and to take advantage of opportunities.

Capital comprises shareholders' equity plus net borrowings. The Company monitors capital using loan to value and gearing ratios. The former is calculated by reference to total debt as a percentage of the year end valuation of the investment property portfolio. Gearing ratio is the percentage of net borrowings divided by shareholders' equity. Net borrowings comprise total borrowings less cash and cash equivalents. The Company's policy is that the net loan to value ratio should not exceed 50% and the gearing ratio should not exceed 100%.

2026

2025

£'000

£'000

Loans and overdraft

11,190

9,977

Cash and cash equivalents

(539)

(1,732)

Net borrowings

10,651

8,245

Shareholders' equity

32,688

31,493

Investment properties and Assets held for resale

46,970

42,910

Loan to value ratio

23.8%

23.3%

Net borrowings to value ratio

22.7%

19.2%

Gearing ratio

32.6%

26.2%

21. RELATED PARTY TRANSACTIONS

Related Party Transactions with the Directors have been disclosed under Directors' Emoluments in the Directors' Report. There were no other Related Party Transactions during the year (2025: £nil). At year end there was £37,666 (2025: £nil) of Directors Emoluments accrued for payment.

22. SEGMENTAL REPORTING

The Chief Operating Decision Maker ('CODM'), who is responsible for the allocation of resources and assessing performance of the operating segments, has been identified as the Board. IFRS 8 requires operating segments to be identified on the basis of internal reports that are regularly reviewed by the Board. The Board has reviewed the segmental information and concluded that there are three operating segments.

Industrial

Retail

Office

Total

2026

2025

2026

2025

2026

2025

2026

2025

£'000

£'000

£'000

£'000

£'000

£'000

£'000

£'000

Rental Income

2,824

2,569

42

47

-

63

2,866

2,679

Other Property Income

24

14

-

-

-

-

24

14

Profit /(Loss) on investment property at fair value

873

693

175

(10)

-

-

1,048

683

Total income and gain

3,721

3,276

217

37

-

63

3,938

3,376

Property expenses

(142)

(92)

(7)

-

-

(21)

(149)

(113)

Segment profit

3,579

3,184

210

37

-

42

3,789

3,263

Unallocated corporate expenses

(717)

(697)

Profit on sale of

investment property

-

52

Operating income

3,072

2,618

Interest expense (all relating to property loans)

(498)

(480)

Interest income and

other income

24

37

Income before taxation

2,598

2,175

Other information

Industrial

Retail

Office

Total

2026

2025

2026

2025

2026

2025

2026

2025

£'000

£'000

£'000

£'000

£'000

£'000

£'000

£'000

Segment assets

46,305

42,420

665

490

-

-

46,970

42,910

Segment assets held

as security

34,895

34,155

665

490

-

-

35,560

34,645

23. CAPITAL COMMITMENTS

Significant capital expenditure contracted for at the end of the financial year and not recognised as liabilities in the financial statements is: £nil (2025: £nil).

24. SUBSEQUENT EVENTS

On 24 March 2026 the Company contracted to sell its Weston-super-Mare property for a total consideration of £665,000 before costs. The net proceeds of the sale after deducting auction and legal fees is anticipated to be approximately £653,000. The sale was completed on 24 April 2026.

The Company has received confirmation from its lender that it had obtained credit approval and is willing in principle, subject to contract, satisfactory due diligence and agreement on documentation to increase the amount of its overall borrowing to a total of £20 million and accordingly had issued indicative term sheets for new facilities to the Company. The new facilities comprise two new Term Loan Facilities of £12 million and £3 million respectively and a new Revolving Credit Facility of £5 million. The new fixed term Facilities will be available for drawdown for a period of six months from the signature of documentation and will be for a term of six years and one month, i.e. until January 2033. The Revolving Credit Facility is subject to market conditions on issue and will be available for drawdown for a period of five years from signature of documentation. The Company intends to drawdown under the new £12 million Term Loan Facility to refinance the existing £10 million facility and any drawings under the existing Revolving Credit Facility on or before their expiry on 17 December 2026.

.

NOTE

The financial information set out in this announcement does not constitute statutory accounts as defined in section 435 of the Companies Act 2006. Accordingly pursuant to section 435(2), this announcement does not include the auditor's report on the statutory accounts.

However, the financial information for the year ended 25 March 2026 contained in the announcement is taken directly from the statutory accounts for that year. The auditors reported on those accounts; their report was unqualified and did not contain a statement under either Section 498 (2) or Section 498 (3) of the Companies Act 2006 and did not include references to any matters to which the auditor drew attention by way of emphasis.

The statutory accounts for the year ended 25 March 2026 have not yet been delivered to the Registrar of Companies. The 2026 accounts will be delivered to the Registrar of Companies following the Company's Annual General Meeting.

The statutory accounts for the year ended 25 March 2025 and for the prior years referred to in this announcement have been delivered to the Registrar of Companies. The auditors reported on those accounts; their reports were unqualified and did not contain a statement under either Section 498 (2) or Section 498 (3) of the Companies Act 2006 and did not include references to any matters to which the auditor drew attention by way of emphasis.

This information is provided by RNS, the news service of the London Stock Exchange. RNS is approved by the Financial Conduct Authority to act as a Primary Information Provider in the United Kingdom. Terms and conditions relating to the use and distribution of this information may apply. For further information, please contact rns@lseg.com or visit www.rns.com.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.ENDFR FFMPTMTBBBIF

Recent news on Wynnstay Properties

See all newsBrief: Wynnstay Properties Recommends Final Dividend Of 18.0p; Total Dividend For Year 28.5p