High quality companies: It’s all in the numbers

There are three non-negotiable financial attributes I look for in a true quality stock.

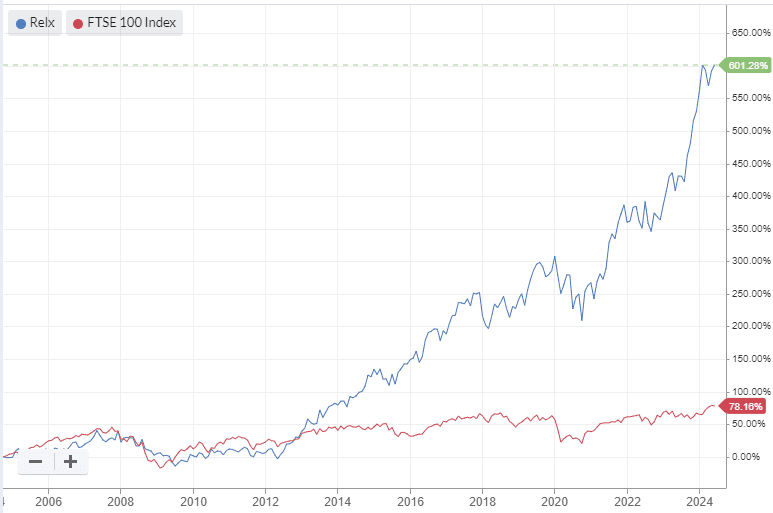

For 20 years, FTSE 100 publishing and data group Relx provided a good example of a quality compounding company. It provides a useful case study, which we’ll use throughout this article.

1. Profitability

Return on capital employed, or ROCE, is generally seen as the single most important profitability metric for quality investors (for non-financial stocks).

If you’re not familiar with ROCE, Ed has written a detailed explanation here explaining what return on capital means – and how a high ROCE can contribute to multibagger gains like those delivered by Relx.

As a rule of thumb, I’d expect a true quality stock to have a five-year average ROCE of at least 15%.

The other main profitability metric I use is operating margin. This expresses the difference between a company’s revenue and its operating costs, including cost of goods sold.

Businesses with a high operating margin generally benefit from pricing power and some competitive advantages. I’ll discuss what form these can take shortly.

I allow more flexibility with margins than ROCE, to allow for different business models. But as a rule of thumb, I expect a quality stock to have an operating margin of at least 10%, preferably much higher.

2. Cash generation

In itself, a profit is only an accounting entry. It does not necessarily mean that the corresponding amount of cash has flowed into the business.

A quality compounder (or almost any good business) also needs to be converting its profits into free cash flow. For those looking for more detail, we’ve explained this topic in depth here.

When I’m looking for quality stocks, I use free cash flow for two reasons:

To assess the company’s ability to convert profits into cash

To value the company

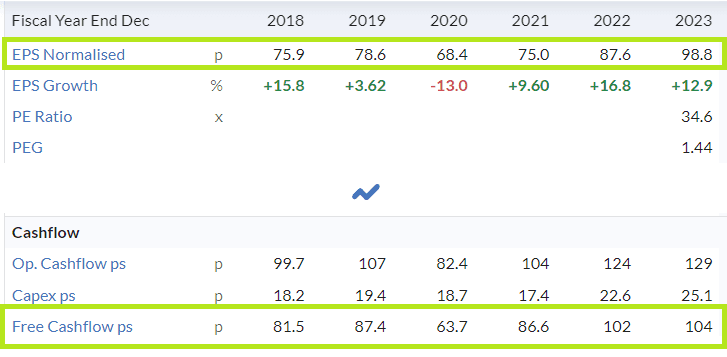

Cash conversion: free cash flow can be lumpier than profits from year to year. This is because cash generation includes one-off capex commitments that may not affect profits. For this reason I find it useful to look at free cash generation over the last five years, rather than just the last 12 months.

As a rule of thumb I look for at least 75% free cash conversion from earnings, on average, in a quality stock. Higher is better – good quality defensive businesses can sometimes achieve consistently above 90%.

Valuation: it would be nice to buy quality compounders when they’re cheap. But this rarely happens, except perhaps during major market crashes. Warren Buffett’s partner Charlie Munger gave us a clue as to how we might think about quality and valuation:

Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return—even if you originally buy it at a huge discount.

What Munger meant is that over long periods, valuation changes tend to average out and the returns investors receive reflect the underlying growth of the business. On that basis, it makes sense to pay a higher valuation multiple for a business that generates a 20% return on capital than one which only returns 10% on capital.

Even so, I think there has to be a bottom line somewhere in terms of valuation. I look for a free cash flow yield of at least 2%-3%, or alternatively, a free cash flow yield that’s greater than any dividend yield.

3. Is the company reinvesting for growth?

High returns on capital and good free cash flow generation are essential ingredients for compounding. Compounding refers to a company’s ability to reinvest a portion of its retained profit to fuel further growth.

Being able to reinvest surplus profits at consistently high returns on capital is what defines the best quality stocks. It’s this characteristic that allows some companies to outperform the market for many years.

How can we measure whether a company is compounding its retained profit?

Ultimately, returns on capital represent the earnings generated from a company’s assets, or capital employed.

To look for evidence of compounding I compare a company’s net asset value, or book value, with its historical ROCE.

What I want to see is a rising book value per share and stable ROCE. This will tell me that a company is retaining profit (rising book value) and reinvesting it successfully (stable ROCE).

If this requirement is met, then I can usually be confident that the company is also generating sustainable profit growth from its growing asset base.

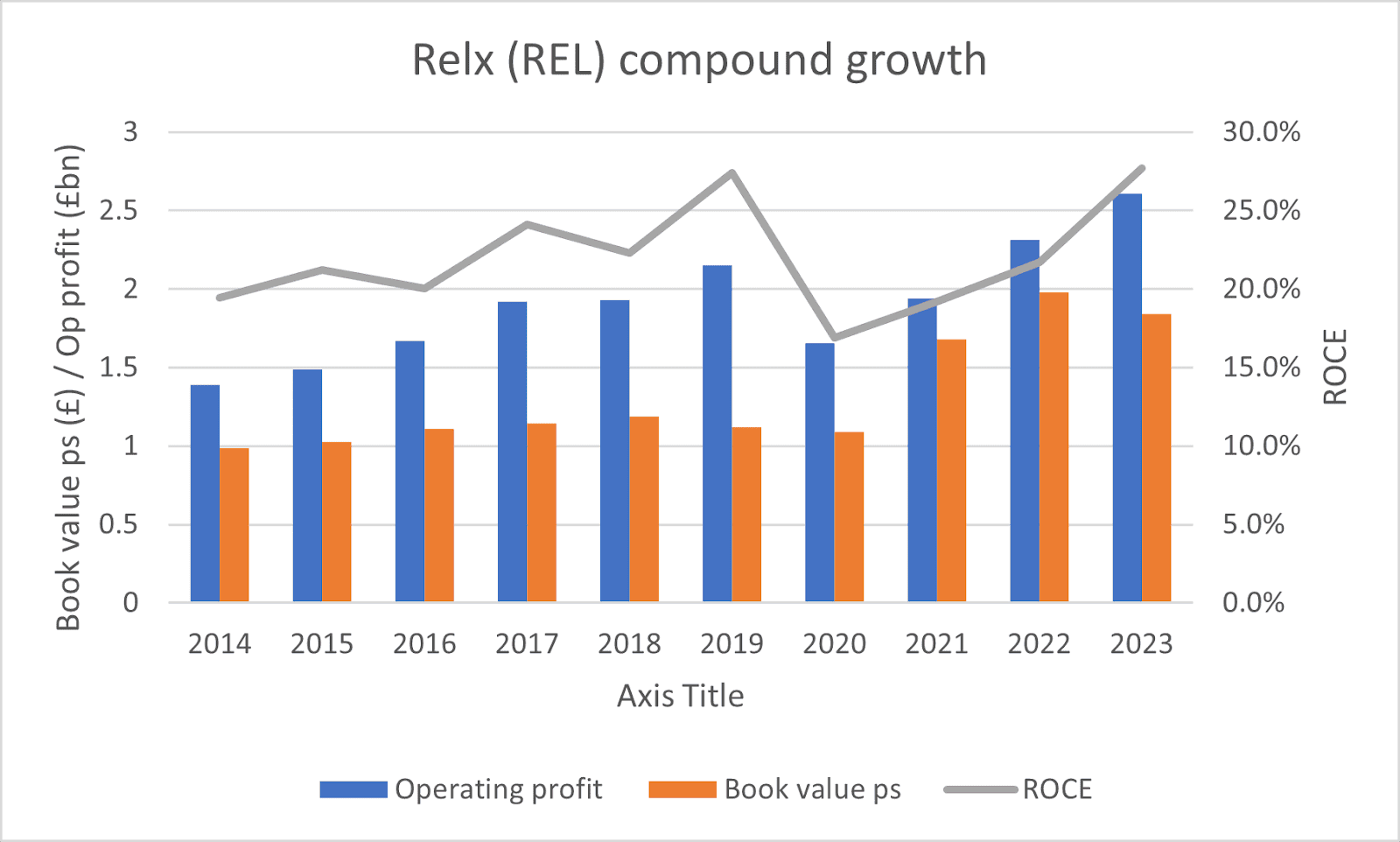

We can see evidence of the type of metrics I like to see by taking a long-term view of Relx.

Working through this in stages, we can see:

Operating profit has risen by 87% since 2014

Book value per share has risen by an almost identical 86%

ROCE has remained in a stable range, averaging 22%

Note how profit and book value have grown in direct proportion. This tells me the company has been able to deploy additional capital at stable rates of return - exactly what I'm looking for.