Contrarian stocks: How going against the crowd can put you ahead

Good quality companies don’t necessarily stop being good when their share prices fall. In fact, lower prices can be a blessing to a strategy that combines two of the most influential drivers of investment returns: Quality & Value.

It’s a strategy that has been executed with devastating success by some of the investing world’s best known names, ranging from David Dreman and Joel Greenblatt to Warren Buffett. The philosophy was best summed up by Greenblatt in The Little Book that Beats the Market[1] “buying good businesses at bargain prices is the secret to making lots of money.”

Why Quality plus Value is effective

In the taxonomy of stock market winners, Quality plus Value (QV) stocks are cast as the market’s Contrarians. These are the shares for value investors who don’t get hung up about positive momentum. Often they don't have an improving price trend, which turnaround investors use to find value stocks that are on the mend. But equally, Contrarian plays are less likely to be the deeply discounted shares with no quality and no momentum, that can end up being value traps.

Instead, Contrarian plays need investors to be sanguine about market sentiment and concentrate on buying quality at a reasonable price. As Warren Buffett termed it, “whether socks or stocks, I like buying quality merchandise when it is marked down.”

The appeal of this approach is that it introduces an important safety factor to value methods that simply focus on degrees of cheapness. One researcher that has looked closely at this is Robert Novy-Marx, an assistant professor of finance at the University of Rochester in New York. He has written that there is a strong philosophical connection between quality and value:

Quality can even be viewed as an alternative implementation of value — buying high quality assets without paying premium prices is just as much value investing as buying average quality assets at a discount.

Novy-Marx’s investigation into the effectiveness of Quality and Value found that trading on both signals achieved the double benefit of increasing expected returns while decreasing volatility and drawdowns. He noted, cheap, profitable firms tend to outperform firms that are just cheap or just profitable.”

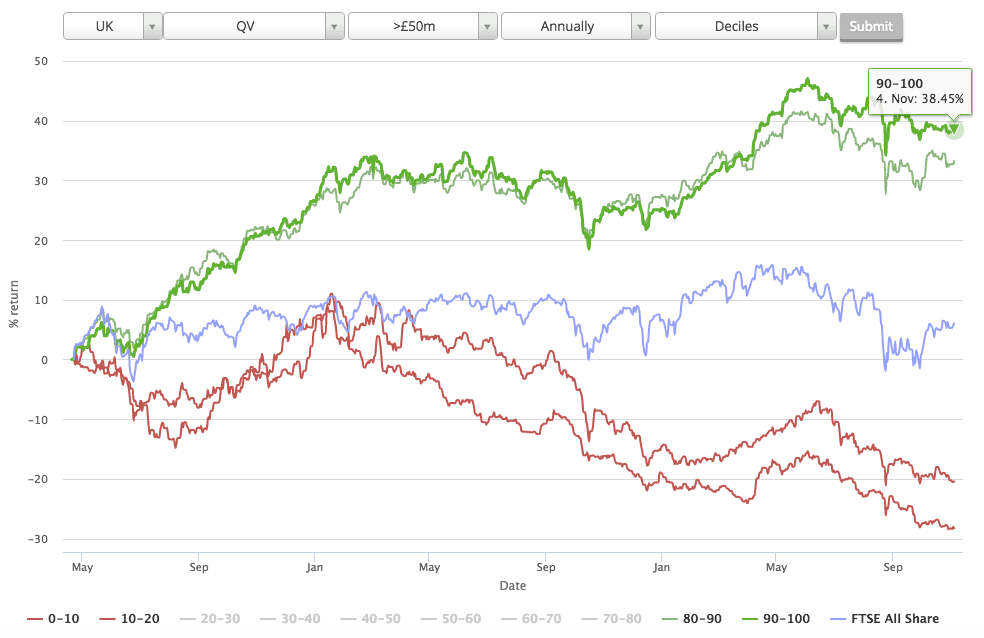

Indeed, the returns based on tracking by Stockopedia suggest that Quality & Value (QV) does produce superior payoffs to value alone. Stockopedia grades every stock in the market for the strength of its Quality, Value and Momentum in the StockRanks. Since April 2013, an annually rebalanced portfolio of stocks in the cheapest 10% of the market based on the ValueRank (using a composite of 6 value ratios) returned 26.5%. But introducing quality factors by ranking for combined Quality & Value (using the QV Rank) produced a much improved return of 38.5%.

How the experts combine Quality and Value

Introducing Quality to a Value strategy requires defining what Quality really means. It’s a question that’s been under the microscope of academics and professionals for decades and is still to be pinned down. Value is always defined relative to price, whether using relative measures like price-to-earnings and price-to-book or more complex intrinsic value measures like Discounted Cashflows, but Quality is much more amorphous to measure.

Quality measures often focus on profitability, earnings growth stability, cash generation, pricing power, efficiency and balance sheet health - and an absence of accounting red flags. These types of measures are often used to gauge the strength of what Buffett refers to as a company’s ‘economic moat’. These are the deeply embedded quality characteristics that can help a firm resist attacks from competitors and produce strong returns over the long-term.

As a result, a Buffett-like strategy would likely look for high industry leading operating margins and positive levels of free cash flow that can be reinvested by the company. Those investments themselves produce strong returns, which can be seen in measures like return on capital employed (ROCE) (search for > 12% ) and return on equity (ROE) (search for >15%).

Alternatively, it’s possible to take a checklist approach to measuring Quality. Back in 2000 American finance professor Joseph Piotroski introduced his nine-point F-Score of balance sheet health. It has since been adopted by finance professionals and banks like Societe Generale as a means of identifying improving fundamental trends in a business. Piotroski originally designed the F-Score as a way of picking potential winners from a basket of the very cheapest stocks in the market (where failure rates are high). He showed that over a 20 year test period, adding this quality factor to a bargain value strategy improved returns by at least 7.5% annually.

Another QV approach worth considering is American fund manager Joel Greenblatt’s technique of ranking the market using ratios that represent each factor. With his Magic Formula strategy, Greenblatt used two metrics: Earnings Yield (as a measure of cheapness) and Return on Capital (as a measure of quality). Every company is scored and ranked against each measure and the scores are added together to arrive at a Magic Formula score.

Greenblatt claimed 30%+ annual returns from this strategy in his backtests, although others have failed to recreate them. Even so, it remains an almost legendary example of how quality and value can be combined with great success.

Practical steps to finding Quality Value shares

There are lots of ways to screen for contrarian shares - an investor can hunt using some of the metrics mentioned above, but the Stockopedia StockRanks provide a shortcut. Subscribers can access our Contrarians Stock Screen here, which seeks to identify stocks based on:

QV Rank > 80 (ie. cheap and good)

MomentumRank < 40 (ie. muted price strength)

Market Cap > £50m (ie. excluding nano-caps)

There is no denying that the contrarian nature of these rules picks up stocks that have felt the wrath of the market. Some languish in depressed sectors like mining and energy, while others may have sprung bad news on investors - and are now paying the price. So it is important to DYOR.

I would argue that a Quality and Value approach captures the spirit of what investors should be looking for in the stock market. At the extreme, the strategy may help to find diamonds in the rough at the very cheapest end of the market. But it also echoes the quality-driven philosophies of fund managers like Terry Smith. For Smith, quality is a prerequisite, but he still resists overpaying for those assets. So I think the message is that quality can add a greater degree of comfort (and performance) for investors who love looking for a bargain.