First Officer: “Captain - one of our engines is failing.” Captain: “Set throttle to maximum thrust on the failing engine.”

Even if you have never watched a sci-fi movie before, our captain’s response may sound a little odd to you, and for good reason. Engineering systems are designed to reallocate resources away from failing components and towards working components to ensure the system continues to work. Upon engine failure during flight, a pilot will redirect fuel away from the broken engine towards a working one, instead of doubling down efforts to the broken engine. This is synonymous to reducing capital from a losing stock market position and redirecting it to a working one.

“Run your winners and sell your losers” - Timeless advice endorsed by many successful investors including the Paul Tudor-Jones, ‘Naked Trader’ Robbie Burns and Mark Minervini and advice that you have probably heard hundreds of times before. And yet evidence shows many of us succumb to doing the very opposite. We persistently hold onto our losers as they continue to fall, vowing to sell them only once they return to their previous high. There is also a temptation to ‘average down’ in these stocks, which involves buying more of the losing stock, usually funded by selling our recent winners.

In ‘The Art of Execution’, one of the best books on selling strategy, Lee Freeman-Shor analyses the strategies adopted by 45 of the world’s top investors, summarising them into winning and losing styles. One of winning styles is an ‘Assassin’-like approach to losses - cutting them quickly, and a ‘Connoisseur’ approach to winners - being patient and allowing gains to compound over time.

Bill O’Neil had advocated a similar style several years before in his book ‘How to Make Money in Stocks’. Bill took this approach further, preferring to pyramid up position sizes. He suggested selling losers quickly and averaging up, buying more of a stock after it has risen in price.

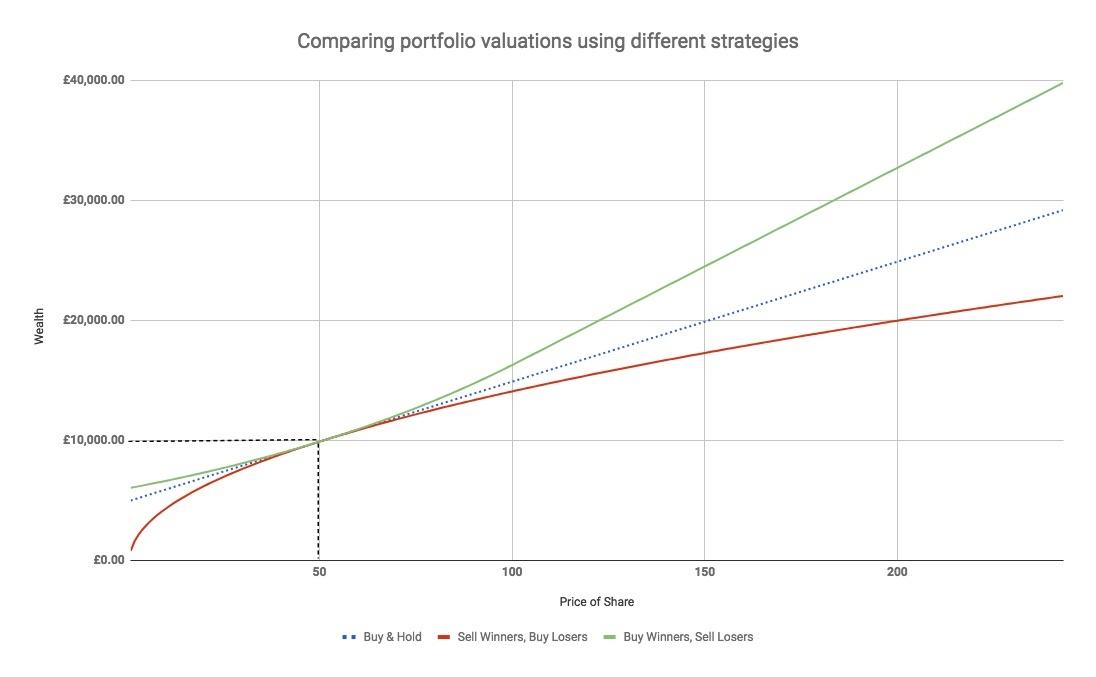

Why selling strategies matter

To outline the differences that these various strategies can have on your wealth, assume you have a portfolio which only holds two positions: an investment in Stock A and a Cash position. The starting value of the portfolio is £10,000 and it holds equal weight in Stock and Cash - 100 shares of Stock A at £50 per share and a £5000 cash position. For simplicity we assume cash has a constant return of 0%.

We then compare how the valuation of the portfolio changes for each of the strategies given a change in the price of Stock A.

Our ‘Buy and Hold’ investor does nothing in reaction to the price of Stock A - the ‘Rabbit’ as eluded by Lee Freeman-Shor.

Our “Sell Winners, Buy Losers” keeps topping up his losing position from the (relatively winning) cash allocation, ensuring that the portfolio keeps its initial equal weighted allocation.

Our “Buy Winners, Sell Losers” investor increases her allocation to Stock A funded from the cash position (the relative loser) as the price of Stock A rises, maxing out to 100% of the portfolio. As the price of Stock A falls she decreases her position, increasing her allocation to the relatively winning cash position.

The chart provides a visual representation of some of the troubles of selling winners to buy losers. Not only does this strategy start to truncate your upside as the price rises, it also exposes you to increasing losses as the price of Stock A falls. Reducing losers and topping up winners may be behaviourally difficult, but it both reduces your downside and increases your upside at an increasing rate as the stock rises in price.

“But wait,” I hear you say, “… Stock A might bounce back”.

Well this is certainly true. Lee Freeman-Shor also described another winning strategy of the “Hunter”, the expert analyst type who doubled down in losing shares and claimed a profit as they rebounded. Our very own Paul Scott claimed a big win when he invested in BooHoo soon after a profit warning and rode it up during its subsequent recovery.

But the question is, do you want to bet against the base rates? Lee Freeman-Shor found two-thirds of cut losing investments didn’t return to their purchase prices. Meanwhile, Stockopedia’s excellent Profit Warning Survival Guide showed that after a year had passed, only 13.2% of stocks ended with their share price back above the price before the warning. Finally, when you compare how high MomentumRank stocks (green) and low MomentumRank stocks (red) have performed over time, you can see the trend would not be your friend.

Now I am not suggesting that you should instantly sell all your holdings and move them all into your biggest winner - it’s important to be prudent with regards to risk management and position sizing. However, which business units to allocate capital to is a key part of any business. A study by strategy consultants McKinsey states:

“Companies that reallocated more resources—the top third of our sample, shifting an average of 56 percent of capital across business units over the entire 15-year period—earned, on average, 30 percent higher total returns to shareholders annually than companies in the bottom third of the sample. This result was surprisingly consistent across all sectors of the economy. It seems that when companies disproportionately invest in value-creating businesses, they generate a mutually reinforcing cycle of growth”

If good capital management - not chasing good money into bad projects - can add substantial shareholder value to billion dollar businesses, imagine the impact the same approach could have on your portfolio.