Finding winners that keep on winning

Momentum is one of the most robust findings in academic finance. It is clear that, under certain conditions, winning stocks keep on winning and losing stocks keep on losing, but as always, the details matter.

What is Momentum?

In academia and amongst practitioners, 'Momentum' has a precise definition. It is based on the “serial auto-correlation” of stock prices. That sounds complex, but it really isn’t. “serial” means that the correlation is time-based, and “auto” means that stock prices are correlated to themselves and not to some third factor. If the serial autocorrelation is positive, positive share price moves are likely to be followed by positive moves and negative by negative. If the serial autocorrelation is negative, then stock prices are likely to experience what is known as mean reversion and move in the opposite direction.

It was already known by the late 1980s, from the work of Thaler and DeBondt[1], that stock prices tended to mean revert over very short periods, up to a month. Given the transaction costs, this anomaly is unlikely to be consistently tradable. The same authors also showed mean-reversion over much longer periods, three to five years. This effect is closely related to the value effect, where stocks that have become cheap subsequently outperform.

The first study to identify that stock prices were positively correlated with themselves over the medium term was by Jegadeesh and Titman in 1993, called Returns to Buying Winners and Selling Losers[2]. It is this effect that is known as "Momentum". They looked at various formation periods, from three to twelve months, i.e. how far back to look for historical outperformance, and various holding periods, again from three to twelve months. They realised it might be best to exclude the last week in the formation period due to the short-term mean reversion effect. Here’s what they found:

The most successful zero-cost strategy selects stocks based on their returns over the previous 12 months and then holds the portfolio for 3 months. This strategy yields 1.31% per month when there is no time lag between the portfolio formation period and the holding period and it yields 1.49% per month when there is a 1-week lag between the formation period and the holding period.

The Momentum anomaly has faced significant scrutiny from academics over the years. Those interested can read more about the battles over which factors should be included in this article by Wes Gray. So far, Momentum has stood up to the test. In terms of known anomalies based on price correlations, we have:

Overreaction: the strongest performers over 1 month tend to underperform the market.

Momentum: the strongest performers from 12 months to 2 months ago tend to outperform the market.

Value: the strongest performers over 3 years or more tend to underperform the market.

Why does Momentum work?

The big question is why isn’t this effect arbitraged away. If it is well known that winners keep on winning, why do investors sell? One option is that investors are being paid a risk premium. With all factor investing, there are two possible explanations for the outperformance. The first is that investors are bearing a greater risk, and to do so, they demand a higher return. This is the camp that academic pioneers of factor investing Eugene Fama and Ken French loosely fall into. The other explanation is a behavioural one, where investors consistently make errors in judgement, to which the likes of Richard Thaler and Robert Shiller would belong. I tend to head towards the behavioural side myself. It seems strange to me that extra risk would be associated with holding high-quality winners, but that’s the leap the risk-based camp must take.

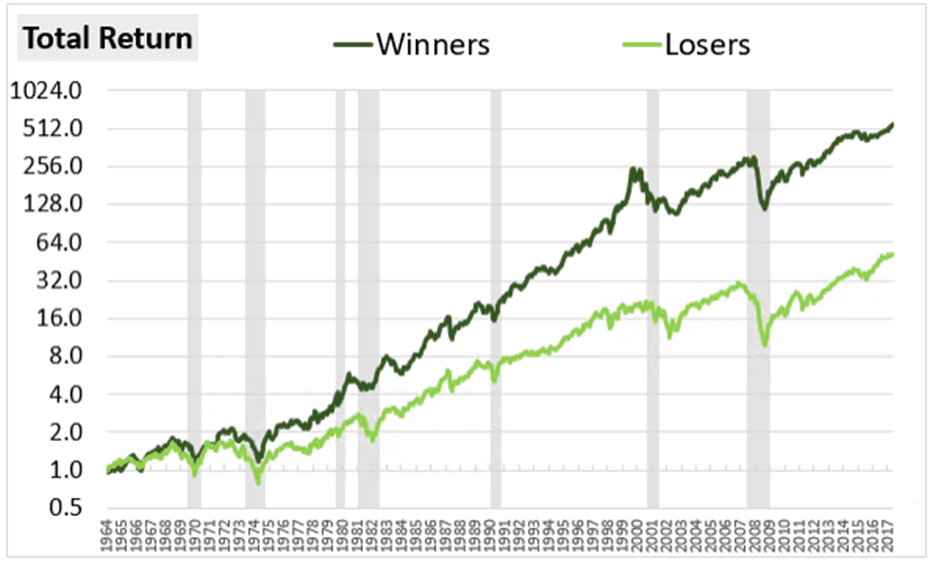

One of the most comprehensive analyses of the momentum strategy was done by O’Shaughnessy Asset Management in a paper called Factors from Scratch[3]. Their analysis focussed on buying the top quintile of large cap stocks on trailing six-month returns, which showed the expected outperformance over the long term:

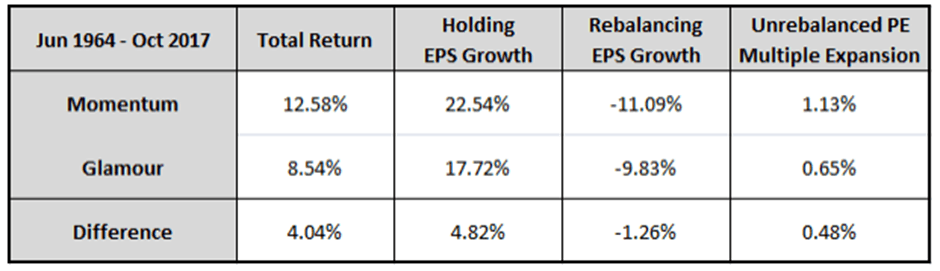

The most interesting part is that the returns to buying the winners came from very rapid EPS growth. In the following table, the authors compare Momentum to “Glamour”, the most expensive growth stocks:

It seems price momentum does a better job of predicting EPS growth than price alone, and Momentum investors are rewarded for that. Momentum investors see slightly greater multiple contraction, meaning the overall performance isn’t as good as the phenomenal EPS growth. However, the net effect is a clear win for Momentum with over a 4% CAGR outperformance.

Problems with Momentum: Rebalancing

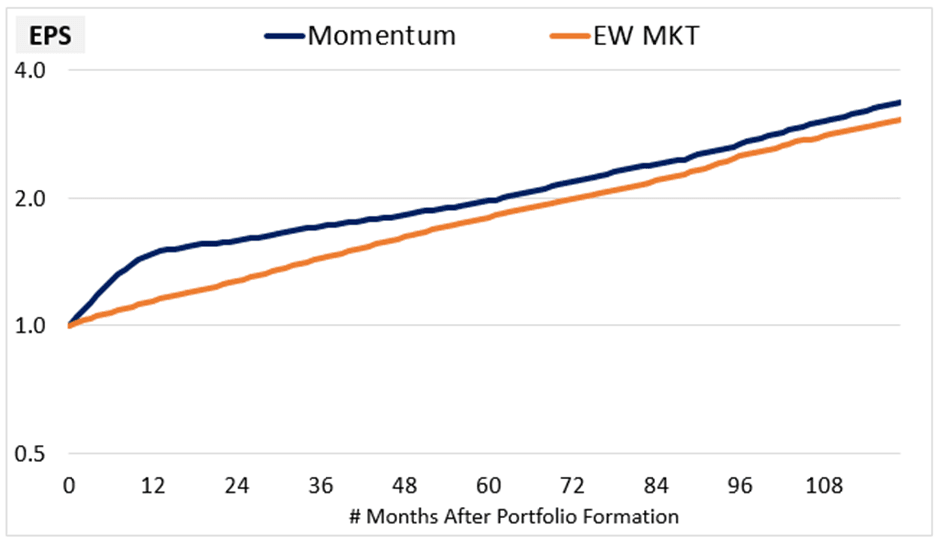

Jagadeesh and Titman were already aware that the momentum effect was relatively short-lived, and in their paper, they gave the example that...

…the portfolio formed on the basis of returns realised in the past 6 months generates an average cumulative return of 9.5% over the next 12 months but loses more than half of this return in the following 24 months.

This effect is visible in the following graph from Factors from Scratch:

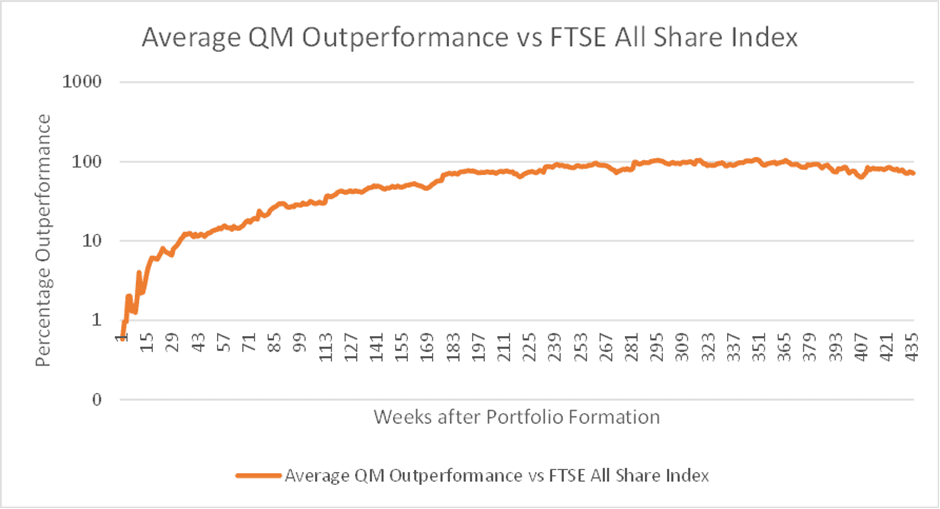

While my own research is not as exhaustive, when I looked at when to sell QM stocks, investors did best by selling after 9 months (excluding the impact of trading costs):

So, buying Momentum is a strategy for the nimble, but this leads to some problems. The first is that short-term trading may have tax implications for the investor. However, the major problem for all investors with a strategy that requires rapid rebalancing is high costs.

Problems with Momentum: Costs

It is well known that the Momentum strategy has not lived up to expectations. As Research Affiliates put it in a 2017 article:

Simulated portfolios based on Momentum add remarkable value, in most time periods and in most asset classes, all over the world; however, live results for mutual funds that take on a momentum factor loading are surprisingly weak.

A primary contributor to the performance gap between the standard momentum factor’s live and theoretical results is the price impact of trading costs associated with the strategy’s high turnover.

Or, as the great Yogi Berra once said:

In theory, theory and practice are the same. In practice, they are not.

The blame is squarely put on the high costs of rebalancing a strategy that may contain very small stocks.

Possible Solutions

Only invest when there are clear market trends

When I looked at when to sell QM stocks, I found that general market conditions significantly impacted the performance of Momentum strategies. Only investing when the general market has a clear trend or cutting the strategy holdings early if they underperform may well improve returns to Momentum investing.

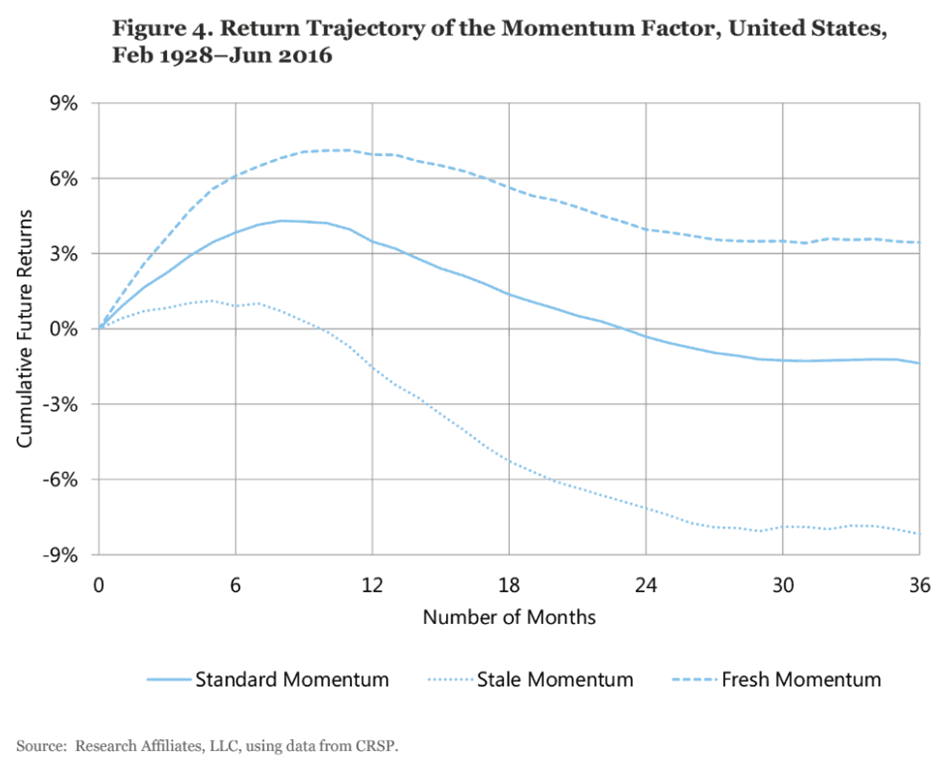

Avoid “Stale Momentum” stocks

While looking if Momentum can be saved, Research Affiliates found that:

Momentum can be divided into fresh and stale Momentum, with very different results. Stocks that have exhibited strong Momentum for two or more years are both very expensive and tired; this is stale Momentum. Momentum essentially fails, especially net of trading costs, for stale momentum companies.

When finding Momentum stocks, some will be early in their journey of outperformance, whereas some will already have been stock market darlings for a couple of years. It seems that Momentum becomes stale early, and avoiding the stocks that have had Momentum for an extended period adds to returns. Avoiding stale Momentum improved expected returns and elongated the period of outperformance, hence reducing or mitigating switching costs:

Combine Momentum with Value

The reason that Research Affiliates found that some stocks exhibit “stale momentum” is that:

These stocks are mostly already very expensive (or, for the short side, very cheap) due to market participants’ overreaction; they are unlikely to present any positive surprises (negative surprises for the wrung-out short stocks) for investors.

This is why adding Value criteria, such as the Stockopedia Value Rank, into stock selection will likely make a positive difference to a Momentum strategy. The value criteria don’t have to be too strict, just enough to remove the most expensive stocks from consideration.

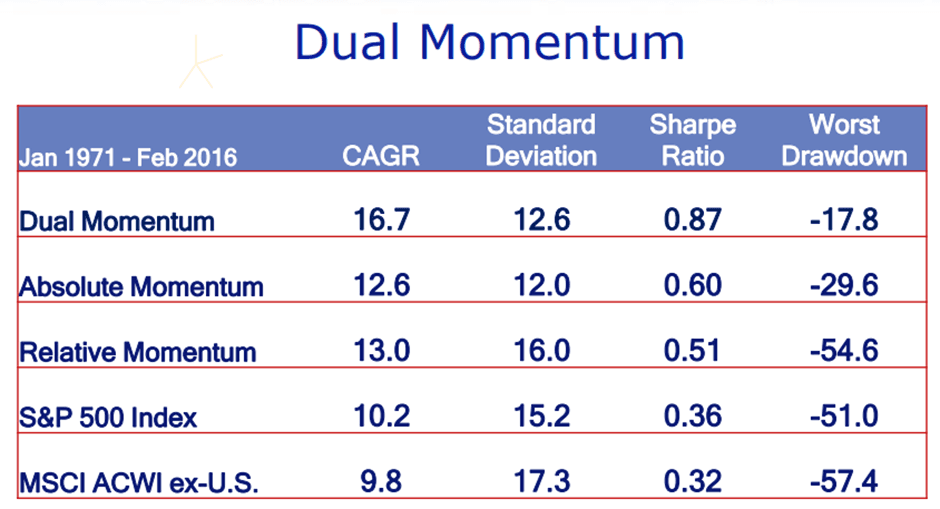

Dual Momentum

Gary Antonacci devised a momentum strategy that doesn’t involve stock picking, which he called “Dual Momentum”. Dual Momentum is constructed from just three highly liquid, and hence almost cost-free to transact, asset classes: US Stocks (S&P500), World Stocks Excluding the US (MSCI ACWI ex-US), and US Bonds (Barclays US Aggregate Bond index).

Antonacci constructed Dual Momentum from two components. He calls The first “Relative Momentum”, where the investor switches between the S&P 500 and the MSCI All Country World Index (ACWI) ex-US, with monthly rebalancing based on a 12-month formation period. The second is called Absolute Momentum, where the investor switches between the S&P 500 and the Barclays US Aggregate Bond index, again with monthly rebalancing and a 12-month formation period. He shows that this strategy produces some excellent results, at least based on back-testing, for such a simple set of rules:

He wrote a book about the strategy for those who want to know more.

Use Industry ETFs

The final idea for improving post-cost returns to Momentum is based on a paper called Do Industries Explain Momentum? by Tobias J. Moskowitz and Mark Grinblatt. The authors found:

…momentum investment strategies, which buy past winning stocks and sell past losing stocks, are significantly less profitable once we control for industry momentum. By contrast, industry momentum investment strategies, which buy stocks from past winning industries and sell stocks from past losing industries, appear highly profitable, even after controlling for size, book-to-market equity, individual stock momentum, the cross-sectional dispersion in mean returns, and potential microstructure influences.

So, it seems that investors could invest in the industries with the best Momentum cheaply via Industry-specific ETFs and get most of the returns to Momentum at very low costs.

Conclusion

Momentum remains one of the most robust market anomalies. However, its requirement for rapid rebalancing means that costs eat into the vast majority of the returns. Momentum funds have never lived up to their expectations. However, all is not lost for the Momentum investor. By making tweaks to the strategy to reduce costs or improve gross returns, investors can use the idea of investing in winners to enhance their portfolio performance.

- Werner De Bont and Richard Thaler . Does the Stock Market Overreact? .

- Narasimhan Jegadeesh and Sheridan Titman. Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. 1993

- Jess Livermore, Chris Meredith and Patrick O'Shauhnessy. Factors from Scratch: A look back, and forward, at how, when, and why factors work.