For many years, Domino’s Pizza was a prime example of a high flyer. It was a 14 bagger over an 11 year period (a 27% annualised capital return before dividends) and a standout performer in almost every two year period since it first bounced up from its lows back in 2001. And so, between the financial crisis and the stock's peak in 2017, Domino’s barely traded beneath a price to earnings ratio of 20. Which begs the question of when on earth could a value investor have ever bought this share? If value investors admit they couldn’t then isn’t there something that they are missing?

The problem with value investing

We human beings are genetically hard-wired to look for bargains. If you can pick something up for less than it’s worth you might just have a happy outcome and a few spare pennies in your pocket to boot. It’s a strategy that works in the flea market and it works just as well in the stock market. Buying cheap is the core tenet of value investing - the strategy that has minted thousands of stock market millionaires and quite a number of billionaires too.

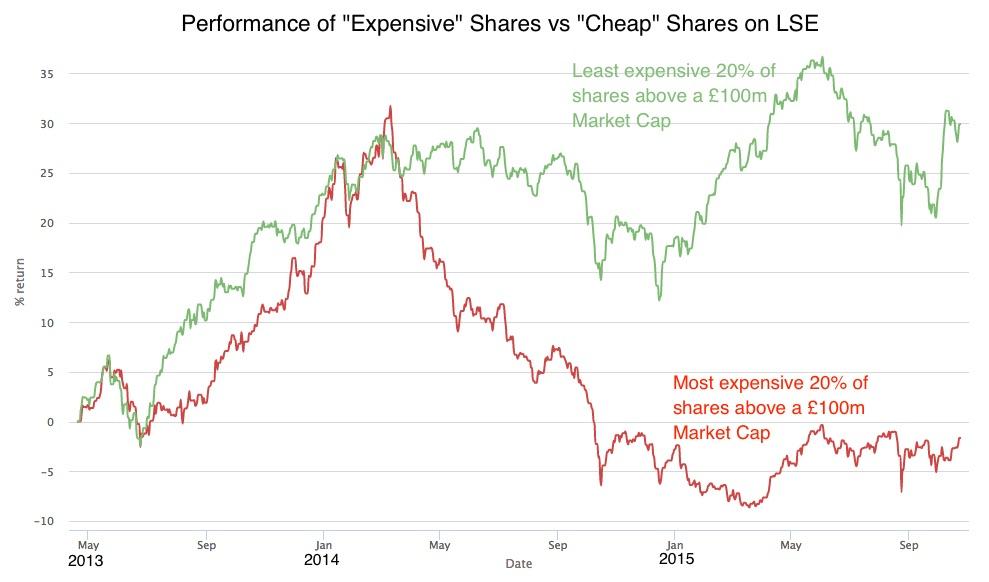

But there’s a problem at the heart of value investing which leads to a certain blindness. Value Investors have an inability to consider any stock that is even remotely pricey. Take a look at this chart and you’ll understand why.

The chart shows the performance of the cheapest 20% of the stock market (green line) vs the most expensive 20% of the stock market (red line) over the last 2 years according to the Stockopedia Value Rank. There’s about 200 stocks in each of those portfolios, but the cheap set of stocks has outperformed the expensive set by a massive 32%.

These results, from the last few years in the UK, are very typical for stock markets. Cheap shares tend to outperform expensive shares. So any rational investor, when asked to pick a winning portfolio of 50 stocks, would most likely go shopping amongst the higher probability set of shares… the cheap ones…. right ?

Lies, Damn Lies and Statistics

Well herein lies the blindness, and perhaps naivety of Value Investors. You see, nestled amongst that set of expensive shares lie some of the greatest companies listed on London Stock Exchange including Dominos’ Pizza, Betfair, Abcam, Next and Rightmove. These companies have trounced the market for years, and most likely some of them will continue to trounce the market in the coming years.

As I’ll be illustrating, there’s a set of 25 shares that could have been very easily selected using the tools at Stockopedia. This portfolio has managed a total return of about 60% over the same time period - a performance that has crushed the 30% average returns of the ‘cheap’ portfolio of value stocks and made a mockery of the -2% returns of the ‘expensive’ portfolio.

Averages, you see, can be highly deceptive - some expensive shares really are worth it. While I hope to show that it’s surprisingly easy to pick them, for Value Investors the process requires a bit of a mind shift. So let’s go a bit further down the rabbit hole to find out why.

The trick to pick’em - a brief interlude

There’s a trick to picking winners from the pool of expensive shares and it comes down to having a solid understanding of the key factors that drive stock returns. Academics bicker and fight over which factors are the most important, but in a nutshell we can simplify the most powerful to the following three which also make up the core triad behind the Stockopedia StockRanks:

Quality: good shares tend to outperform junk shares.

Value: cheap shares tend to outperform expensive shares.

Momentum: leading shares tend to outperform lagging shares.

If you imagine driving a go-kart, you can propel yourself in three different ways - with an engine, using gravity or just by continuing to free-wheel. These three forces are analogous to the quality, value and momentum forces that drive share prices in the stock market. Now in the perfect scenario one might like to find shares exposed to all three drivers but in fact all three aren’t necessary.

Take one of these drivers away and the other two work just fine without it. Value investors tend to solely focus on just two of the drivers quality and value. They can be thought of as Contrarians who look to buy good shares cheaply and don’t mind price action to be weak as it gives them a chance too buy shares when they are marked down. It’s a smart strategy and a profitable one, but it’s a strategy that will never allow them to own a stock like Domino’s Pizza. Contrarians may not realise it, but they are deliberately removing momentum from their model of the universe which may be a costly oversight.

In just the same way, there is a less popular, but just as profitable strategy that removes the concept of 'Value' from its model of the universe. By focusing on investing in the highest quality, highest momentum shares regardless of price it’s quite possible to trounce the market. We christened this set of shares High Flyers.

High flying investing greats

So who are among great investors who have had the instinct to invest in High Flyers? One of the first advocates was the wildly successful fund manager Richard Driehaus who was profiled in Jack Schwager’s excellent book The New Market Wizards[1] . Driehaus looked at the common attributes of spectacular stock market winners and realised he could never buy them on low P/E ratios:“Many of the best growth stocks have high multiples and are psychologically difficult to buy.” So he tore up the rule book and looked for high quality, high momentum shares. His anti-value strategy was summed up in this quote:

“One market paradigm that I take exception to is: Buy low and sell high. I believe that far more money is made buying high and selling at even higher prices. That means buying stocks that have already had good moves and have high relative strength - that is, stocks in demand by other investors.”

It worked very well for Driehaus who generated 30% annualised returns over a 12 year period.

Beyond Driehaus, one of my favourite authors is William J. O’Neil, who wrote How to Make Money in Stocks[2] which I thoroughly recommend to all investors. O’Neil spent years analysing what worked in stock markets, and bought a seat on the NYSE from his trading profits. He went on to found investors.com and publish Investors Business Daily - both excellent resources for US bound investors. O’Neil famously disregards the P/E ratio completely.

For years analysts have used P/E ratios as their basic measurement tool in deciding whether a stock is undervalued and should be bought… but our ongoing analysis of the most successful stocks from 1880 to the present shows that P/E ratios were not a relevant factor in price movement.

In his analysis of the greatest stock market winners of all time from 1953 through to 1995 he found that: the “beginning P/Es for most big winners ranged from 25 to 50, and the P/E expansions varied from 60 to 115”. In other words if you really wanted to find the great stocks you had to be willing to completely ignore traditional measures of value.

The nitty gritty - resources, ratios & metrics that can help hunt for High Flyers

In general terms - a Quality company is one that is highly profitable ( ROCE, ROE, GPA ) with high industry leading margins, stable, growing and ideally accelerating sales and earnings, with a strong and improving fundamental trend (F-Score), a good shareholder payout (Yield, Buybacks) without having any risky red flags (e.g. Bankruptcy risk, Earnings Manipulation Risk or Share price volatility).

A Momentum stock is one whose share price is up or above it’s 52 week highest price, is within the top 20% of share price percentage winners for the last 6 or 12 months (using Relative or Absolute Price Strength), is beating broker estimates (earnings surprise) and seeing estimate upgrades and recommendation changes.

Where high flyers go next

There are a few words of caution needing here. These kinds of shares tend to be more volatile than the market and as they have high price momentum they can suffer reversals more strongly than the overall market. This is clear to see in the performance chart above.

In my own experience few shares can stay a High Flyer for too long - especially in the UK as the market just isn’t as big as in the USA. Companies that do are the exception, rather than the rule. Most will spend a couple of years as a High Flyer before one of two things happens - either the stock or the company runs out of steam. So running a portfolio like this requires active management - regular portfolio rebalancing to keep jumping into the next set of High Flyers before the previous set runs out of steam.

Expensive shares are very fragile as the market has high expectations for them. If those expectations are not met then the market reaction can be brutal. Asos, the famous online fashion retailer, is a classic example. This stock soared, at times trading at beyond a P/E ratio of 100. But when the company finally disappointed the shares were decimated falling by something like 65% till they bottomed.

1. High Flyers can become Falling Stars

In ASOS’s case the broker expectations proved too high, so the share price ran out of steam (falling momentum). This left it as a high quality company on a very expensive valuation with sentiment turning against it. Finding a floor under a stock with this profile is hard as P/E ratios can contract dramatically. We call this profile of stock Falling Star and it’s one of the worst places to be as an investor.

2. High Flyers can become Momentum traps

The other, less usual, place for a High Flyer to end up is where the fundamentals deteriorate but the share price (momentum) keeps on trucking. These are known as Momentum traps and are most often seen in bubble periods where the market divorces itself from fundamental reality.

The final caution is that there are more stocks qualifying as “High Flyers” than I’ve seen in three years, so it may be that chasing these stocks is becoming a crowded trade.

Final Words

So my general rule of thumb with High Flyers is to watch them like a hawk, and sell as soon as price momentum or fundamentals turn. If you are really sure that the shares have a rock solid economic moat, and the valuation isn’t too stretched then it’s possible to continue to hold these shares through corrections. Your share may turn out to be a magical, multi-year compounder, the kind of share that comes along only a few times every decade that we’d all love to build our portfolios around.