Growth has several facets.

Earnings growth is perhaps the most important factor for many stock pickers, although this must be considered alongside other elements, including cashflows, profitability, the company’s size and the price momentum. Investors should also ensure they are not overpaying for growth. Understanding these dynamics can significantly enhance investment decisions.

Earnings growth

Earnings growth has two key aspects.

The first is periodic growth, which refers to the percentage change in earnings over a specific period. Many investors consider the percentage change over a given year. For instance, William O'Neil’s CANSLIM approach to growth investing targets companies whose earnings have increased by at least 25% compared to the same quarter in the previous year.

Investors can also perform a longer-term analysis; O'Neil also examines earnings over the past three years, focusing on stocks that have grown by more than 25% during that period. This brings us on to the second aspect of earnings growth… consistency. Looking at growth over just one year may be insufficient. In The Zulu Principle, Jim Slater suggested that there should be at least two years of historical growth. To evaluate this, investors often analyse the growth streak, the number of consecutive years a company has increased its annual earnings.

Cashflows

Ideally company earnings would grow in tandem with cashflows. If earnings are growing but cashflows are not, then the company may struggle to finance growth initiatives without external financing. Moreover, growth without a corresponding increase in cashflow could signal accounting manipulations. Jim Slater warns investors that ‘too many companies seem to be doing well until you analyse their accounts and find that their earnings per share are not backed by cash. They are phantom profits.’

Profitability

Earnings growth is crucial, but it is equally important to understand what those earnings represent as a proportion of revenue. This is where profit margins come into play. Companies with higher margins have greater capacity to reinvest in future growth.

Profitability can also be indicative of a strong economic moat – a superior business model that enables it to generate above-average returns. These moats can deter competition, allowing the company to grow profits without facing significant rivals (we discuss economic moats in this article).

Profit margins: There are several types of profit margins. Gross margins represent the percentage of revenue that remains after subtracting the cost of goods sold (COGS). Operating margins deduct both COGS and operating expenses (e.g, salaries and marketing) from revenue. Net margins deduct all expenses from revenue.

Returns: We can also measure profitability by evaluating how efficiently a company turns its capital (equity or assets) into earnings. The most well-known are return on equity (ROE) and return on capital employed (ROCE). ROE measures how efficiently a company uses its equity to generate profits. It is calculated as Net Profit divided by Equity. ROCE measures how effectively a company uses its total capital to generate income. It is calculated as Operating Income divided by Capital Employed.

Size and market cap

Jim Slater's most famous saying was, "Elephants don't gallop." He was referring to the idea that smaller companies often have more room to grow compared to larger firms. Robbie Burns would most probably agree. In The Naked Trader, he said smaller stocks ‘often have better growth prospects than, say, FTSE 100 stocks’.

The smaller cap segment of the market is also less efficient. Smaller companies often get less attention from analysts and institutions. This often means that better bargains are available. Furthermore, small-caps generally outperform large-caps. Slater pointed out that ‘over the last fifty years [to 2008] micro-cap stocks have outperformed the market by more than eight times.’

The size of a company is typically measured using the market capitalisation (market cap).

Price momentum

Traditionally, there are two types of investors: those who focus on price movement and those who focus on financial statements. Jim Slater once poked fun at the former group, saying, ‘chartists usually have dirty raincoats and large overdrafts.’ He added, ‘I do not know many rich chartists.’ Over time, however, he softened his stance and recognised the importance of analysing price movement alongside financial statements. He said, ‘If the shares are not keeping up with the market, you should be on red alert.’ Other investors may be aware of problems that you have not yet identified.

You can assess price momentum in two ways: relative strength, which compares a stock's performance to the market, and absolute strength, which measures the percentage change over a given period.

Case study: Cairn Homes (LON:CRN)

Readers will know that as we go to print, many commentators predict that interest rates are peaking out and may well come down. This projection is positive for house builders. In theory, cheaper mortgages make it easier to buy property. Cairn Homes, a house builder, thus benefits from having that ‘new’ factor – i.e. an industry event which could drive the share price up.

Admittedly, the company has a market cap of £926.91m, so it is not quite a small-cap, although it is small enough to qualify for our implementation of the Jim Slater Zulu screen. Despite not fitting the small-cap criteria precisely, the StockReport indicates promising prospects for growth in other areas. For example, the Financial Summary shows a consistent trend in earnings growth, with just one bad year, i.e. 2020. It is also worth noting that earnings growth has been backed by cashflow growth. Operating cashflows and free cashflows were always above EPS figures (except for 2020).

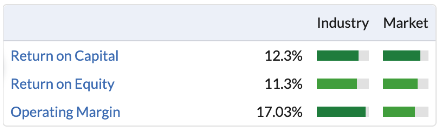

The company is cheap in terms of its P/E ratio, which stands at 13.4 on a TTM basis. The PEG ratio is also below 0.5 on a TTM basis (see above). The traffic light system shows green lights for the profitability metrics. Returns on both equity and capital are well above the industry and market averages; so too are operating margins.

Finally, we can see from the chart below that the company has outperformed the market over the last year or so, by a comfortable margin.

Integrating growth into your investing

Seeking companies based on growth metrics alone isn't widely advised by experts in the investment industry.

It's important to ensure the growth metrics mentioned above have some grounding in fundamental strength.

Investors seeking growth opportunities might also want to consider qualitative factors:

Competitive advantage: Warren Buffett once remarked that if given a billion dollars to compete with the Wall Street Journal, he would simply return the money. Some companies are so formidable that mere financial resources won't suffice to challenge them. These companies possess a robust competitive advantage, often stemming from a strong brand name, a dominant position in a specialised market, or patented products. A swift method to assess a company's competitive edge is to examine its returns, such as ROE or ROCE, along with profit margins. Strong brand names afford companies pricing power, leading to enhanced profitability.

Something new: Earnings can also be influenced by what Jim Slater terms as 'Something new'. These are typically factors such as new management, new products, significant industry events, or new acquisitions. For instance, when Polaroid introduced its instant developed photograph, the share price soared. Industry events, such as the collapse of a competitor or a major breakthrough like the discovery of North Sea oil, can also significantly impact earnings. William O'Neil’s CANSLIM approach also targeted companies with new products, new management, or positive events that can drive a company's stock to new highs. Indeed, the N in CANSLIM stands for new.

Scalable business model: Many growth investors prefer a repeatable business model, often referred to as cloneable, in the sense that the model can be replicated in different locations without modification. Think of a business that follows a standardised manufacturing process. Domino's Pizza comes to mind. They have a highly standardised process for making pizzas and grew rapidly, as the following annecode shows… The original company logo features three dots, where each dot represented one of the three stores in 1965. Domino's initially intended to add a new dot for each new store, but this plan was abandoned due to rapid expansion.

It is also worth considering the relationship between growth and value. Jim Slater, for example, sought out stocks that were forecasted to have strong earnings growth, but were also priced relatively low. The challenge lay in avoiding overpaying for growth. He stated, ‘I have always been attracted to growth shares, particularly those that can be purchased at what I perceive to be a discount to their proper value.’

One of Slater’s preferred metrics was the PEG Ratio, which evaluates a company's price against its earnings growth rate. It is calculated by dividing the PE ratio by EPS growth. A PEG ratio of 1 suggests the stock is fairly priced. A ratio below 0.75 or 0.5 is viewed as cheap. Investors can also use other metrics, like the simple PE ratio.