Pearson: Three lessons in behavioural finance

I have written before about my strong dislike of Pearson (LON: PSON) the international textbook company and former owner of my old employer, the Financial Times. My dislike isn’t unfounded. Under the leadership of John Fallon (2013 to 2020), the company sold off its most profitable assets, leaving it with an education business which was unprepared for a digital world. That poor management resulted in a series of increasingly depressing financial results and moribund returns for investors.

I must admit that my inherent bias has, on occasion, been a source of pride. Between 2015 (when I started at the FT and joined the army of anti-Pearson journalists) and 2020 (when I left), the company’s share price fell 68%.

But this year, that bias has proved rather unfortunate. In 2022, Pearson has been the top performing stock in the FTSE 100, its share price is up 56%.

I am not alone in ruing a missed opportunity. Most people I know who have ever worked for a Pearson company (or former Pearson company) dislike the stock. As do many of the members of the teachers union, who like to disrupt Pearson AGMs with questions about price inflation and poor quality text books. And spare a thought for famed fund manager Nick Train who called time on is 18-year holding in April this year.

So why have so many of us got it wrong this year? The answer provides an interesting lesson in behavioural finance.

Lesson One: Confirmation Bias

Confirmation bias is a human tendency to seek out information which supports your belief and ignore information which contradicts it.

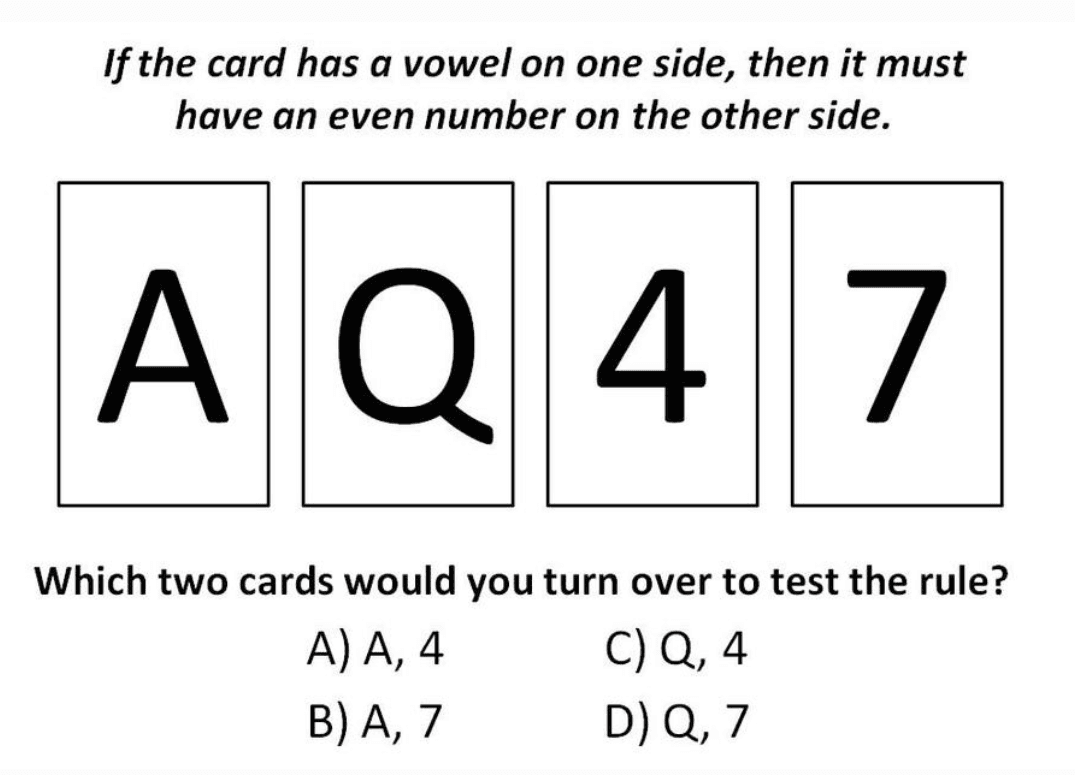

This can be explained by the following example of a Wasson Selection Test:

The correct answer to the question B) To test the rule you should turn over cards A and 7. Turning over A will help you confirm the rule, turning over 7 will allow you to disconfirm it if necessary (i.e. If a vowel is appears on the other side of the card, we will know that the rule is incorrect).

Did you select A and 4? If you did, you’re not alone. Psychologists have used iterations of this test since it was first constructed in 1966 and more than three quarters of respondents get it wrong. Human inherent bias is to seek out information that confirms what they already know (or think they know) rather than information that disproves their beliefs. For that reason, most of us will turn over card 4 looking for a vowel. But card 4 has no ability to invalidate the rule and therefore, in flipping it, we don’t learn anything new.

The Pearson Problem - confirmation bias in action

Like a politician scouring the dregs of the internet for a rival’s misdemeanours, I have used the internet’s unfailing memory for clear evidence of my own confirmation bias.

Between January and May 2018 I wrote about three Pearson trading updates for the Investors Chronicle. Here are short extracts:

January: “The earnings beat has been caused by a better-than-expected tax rate. On an underlying basis, the company is struggling just as much as ever.”

February: “Debts are down, cash flows are up and profits came in at the upper end of guidance. The problem is that guidance was slashed this time last year, meaning numbers aren’t truly impressive when compared with 2016.”

May: “The first-quarter contributes so little to Pearson’s annual profits that we think it would be foolish to change our opinion.”

None of these trading updates was particularly strong and the company was using annoyingly flowery language to paper over its problems, but in all three cases I was hunting out the bad news. I had my narrative (Pearson is a terrible company) and I was sticking to it, with all the evidence I could find.

The Cure

Our underlying beliefs shouldn’t be ignored, but we should seek to disprove them with evidence wherever we can. Investment research shouldn’t focus only on things that we believe we know, but also things that we know we don’t.

Lesson Two: Outcome Bias

In all walks of life we tend to judge decisions by their eventual outcome, rather than by the quality of the decisions when they were made.

Nobel prize winning economist and psychologist Daniel Kahneman puts this down to our perception of the two systems in our brain - what he calls system one and system two. System one is the fast thinker, it is responsible for immediate and automatic decisions. System two is more measured, considered and deliberate. Biases occur when we associate decisions (good or bad) with our system two brain, when they have really been made by our system one brain - we believe we have made rational decisions, but in reality it is our initial hunch or unconscious bias which has sparked an action.

The outcome of that decision can cause problems. If a decision leads to a positive outcome we are more likely to think of it as a measured skilled decision (made by system two) than an irrational, automatic decision (made by system one).

This is a particularly pervasive problem in investing because the stock markets are so bad at giving feedback. For example, if your portfolio is performing well right now it may be because of good decisions made by your system two brain, but it could equally have been caused by irrational system one thinking: luck in the stock market has the same results as good judgement.

The Pearson Problem - outcome bias in action

The decline in Pearson’s share price throughout John Fallon’s tenure was caused by bad management. He took the decision to sell off assets and focus on the education business without fully preparing that business for the demands of the future. The poor shareholder returns were a fair reflection of the inherent problems at the company.

But was it really my system two thinking that lead me to decide that Pearson was a poor investment time after time? I certainly believed it was. I had done my research, found that Pearson was performing badly and then watched with pleasure as the share price fell and I was proven correct. The outcome was what I expected - it must have been down to my research.

But if I am honest, it was my system one brain that drove that research and lead me to make the decisions which ended up being good ones. In 2022, I have been proved wrong, and it is clear that I haven’t allowed by system two brain the space to make its own decisions.

The Cure

Stephen Yui, the lead manager at the Blue Whale Growth fund, overcomes this problem with what he calls ‘blank paper investing’. Every time he comes to make a decision on whether or not to buy or sell a stock he begins with a blank sheet of paper. This means that any past decisions (and the outcomes caused by them) don’t impact his decision making.

Lesson Three: Loss Aversion Bias and the Endowment Effect

People tend to feel the pain of a loss twice as acutely as they feel a win of the same magnitude - a psychological factor that English football fans will no doubt attest.

In 1984 - before he started investigating the system one and two brain - Daniel Kahneman wrote a paper on this alongside his friend and distinguished psychologist Amos Tversky. They found that the asymmetry between pain and pleasure manifests in a phenomenon they termed loss aversion: humans require greater evidence of disutility to give up an object than evidence of utility to acquire it.

In stock markets, this loss aversion makes investors hold onto their stocks longer than they perhaps should. In order to sell, they require significantly more evidence than the evidence they needed to add the stock to their portfolio in the first place.

The work of Kahneman and Tversky links closely to a study by Richard Thaler (1980) on what he called the ‘endowment effect’: people demand much more to give up an object than they would have been willing to pay to acquire it. In investment circles that often means that they attach much higher value to stocks that they own than stocks that they don’t.

The Pearson Problem - Loss aversion and the endowment effect in action

I have never been a Pearson shareholder and have therefore shown no symptoms of the endowment effect (except perhaps in the lack of attention I gave the share when new management set in place a turnaround strategy which seems to finally be paying dividends.) But Nick Train has almost certainly been a vicim.

Train arguably attributed more value than he should have done as the share price was crashing under John Fallon’s tenure. In 2015, when the company first began to focus on the poorly performing education business, shares were trading at more than 1500p a share. By the time he had sold his entire stake in April 2022, they were worth just 760p.

The Cure

Systematic investing. Rules are a major help to sentimental investors who get too attached to stocks they own or fail to see the good in stocks that they don’t own. For example, investors should seek to only look at their portfolio performance when they really need to and limit trading times to avoid emotional or irrational decision making.

Rules for buying can also help investors overcome their unconscious (or indeed their conscious bias). In February this year Pearson had a StockRank of 86 and a share price of 640p. If I had added it to my portfolio then, I’d have made a 43% return on my investment this year, not including dividends.