I remember the first stock that I recommended for purchase across all our client accounts in my private client group at Goldman Sachs. I was 22 years old and had to comply with the "process". That process meant that shares needed to have been recommended by one of our research analysts, who sat on a different floor to our investment team. I had been watching an Ed-Tech firm with the ticker symbol, CBTSY, and for no apparent reason, it had fallen about 30%. I applied the process, phoned the analyst who confirmed he had just spoken to the CFO very recently and that there was no change to the story. We bought it across all our client accounts.

The next day, the shares slumped dramatically on a profit warning. My boss, with more experience than I, immediately sold, and we took a £1 million loss across the accounts. There were many lessons that I took from this. I rarely trusted research analysts again, but more importantly, learnt the lesson of taking losses quickly. CBTSY continued to fall over the coming months.

As much of the stock market grinds lower, more and more shares are reaching bargain valuations. But markets can stay irrational longer than you can stay solvent. If you buy stocks, you are going to pick some losers, no matter how cheap they seem. This creates a quandary. What should you do with your losers?

In this article, I will illustrate the importance of keeping losses small with a few mental models and some practical guidance on loss management.

Fighting the inclination to hang onto losers

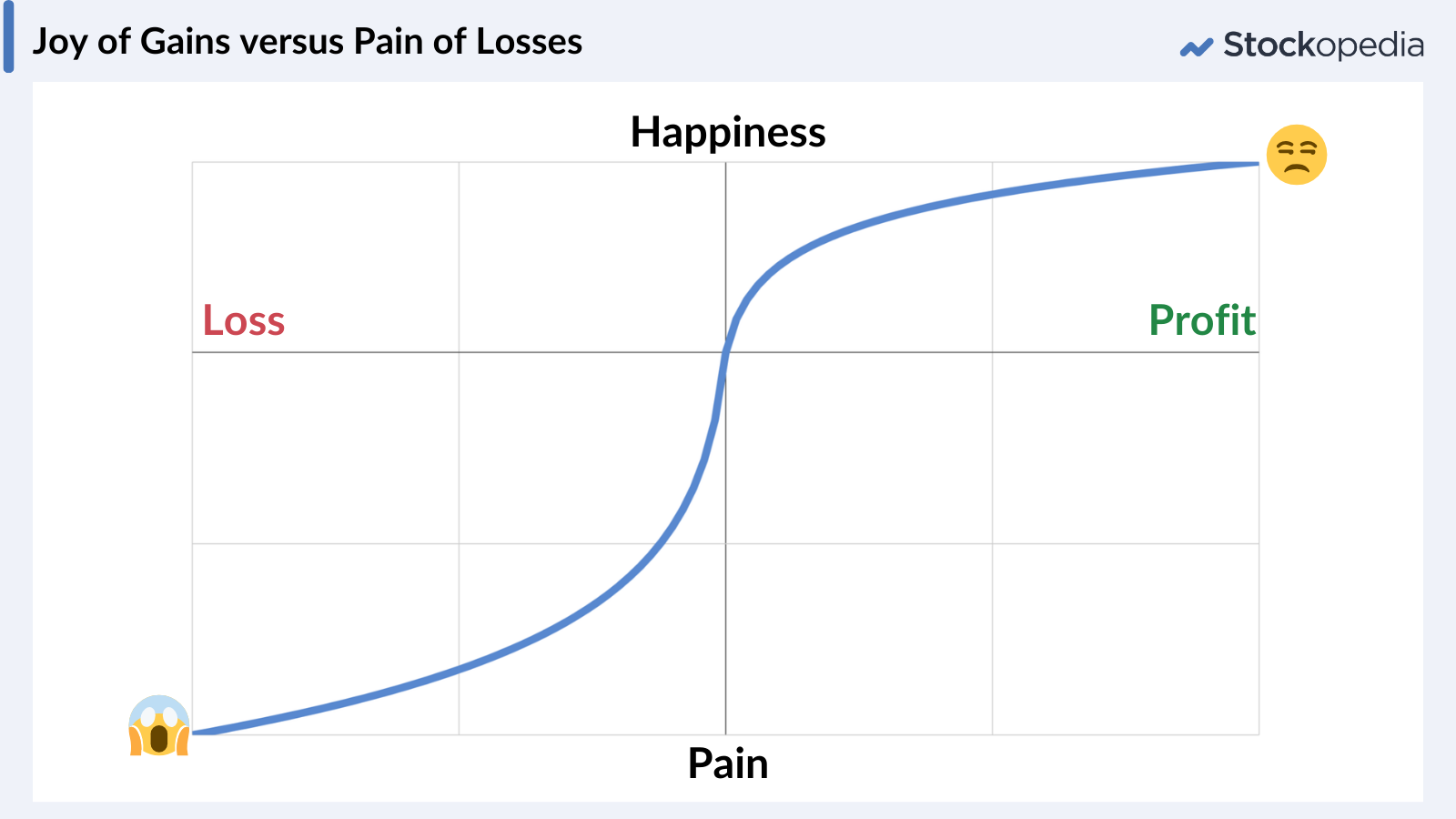

Daniel Kahneman and Amos Tversky extensively studied human behaviour towards differently framed opportunities in their famed “Prospect Theory”. What they found is that we have a tendency to be risk-seeking in our approach to holding losers, but risk-averse when it comes to holding winners. They found that we feel pain of losses more than twice as much as the joy of gains.

The chart below is a handy illustration of this effect.

Psychologically, we don’t believe we’ve taken a loss until we’ve sold a share, so we avoid selling as we think “it might come back”, but we tend to sell gains too quickly, as we say to ourselves “we might lose our profit”. So we snatch at gains, and hold losers. This is the completely opposite behaviour to the age-old winning investment maxim to Run Winners and Cut Losers.

If you don’t fight the tendency to hold on to losers, and fight the tendency to sell winners, making any money in the stock market is an uphill battle. Just remember, our psychology is not well adapted to this behaviour, so we have to force ourselves to learn this habit through practice.

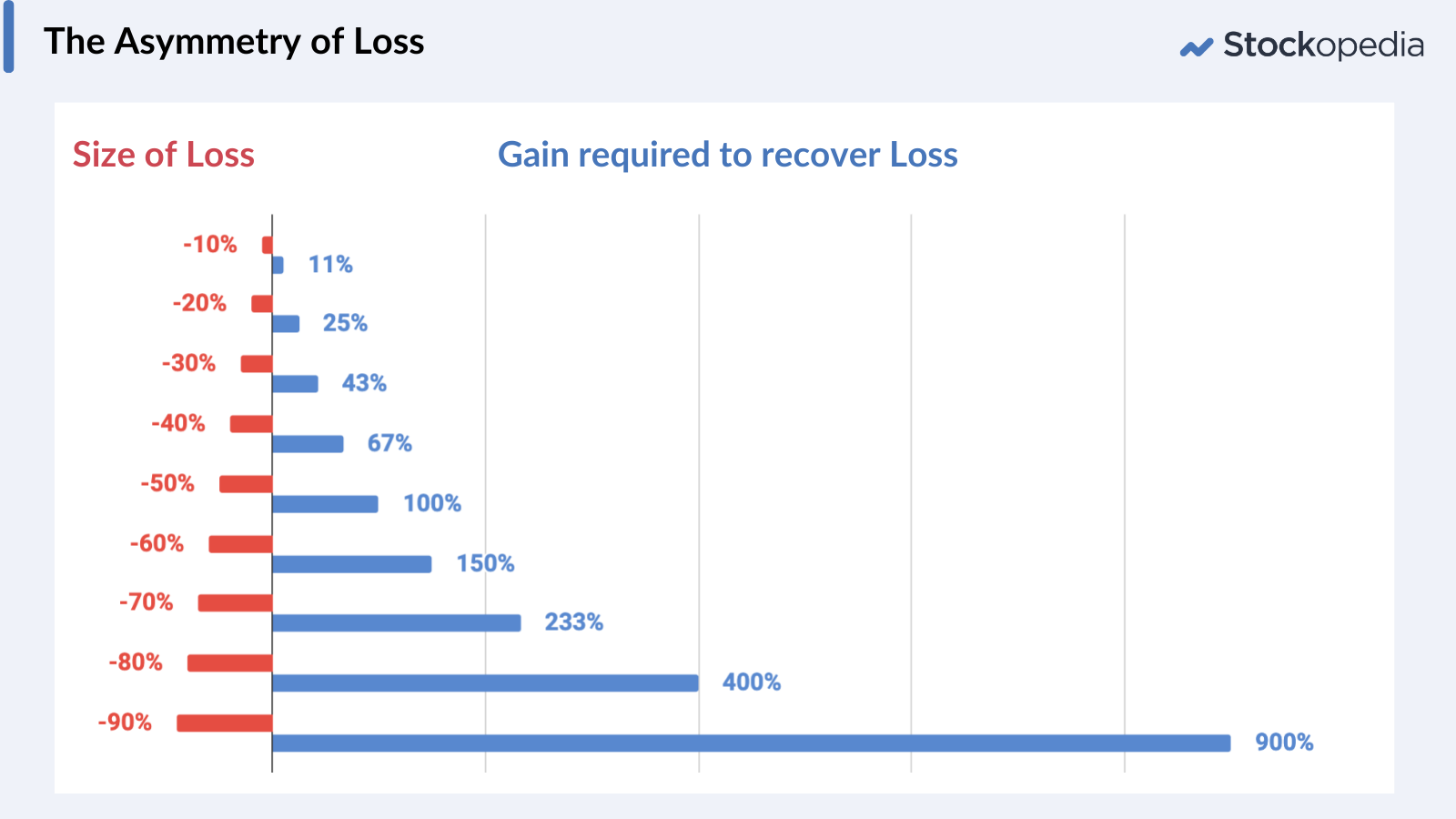

The larger the loss, the ever larger the recovery

The value of keeping losses small is no better illustrated than in the graphic below. If you lose money, the gain required just to recover the loss grows by a power-law. If you lose 50% on a position, that position will need to double just to return you to breakeven. If you lose 90%, it needs to gain 900%.

This is such an important mental model. Burning the below graphic into our minds helps considerably when thinking about what to do with losers.

Instead of thinking about cutting losses as an admission of a mistake, or as an unnecessary commission to your stockbroker, think about them as an insurance premium. There’s great comfort in paying car or home insurance, so why not consider small losses as a premium paid to preserve your capital?

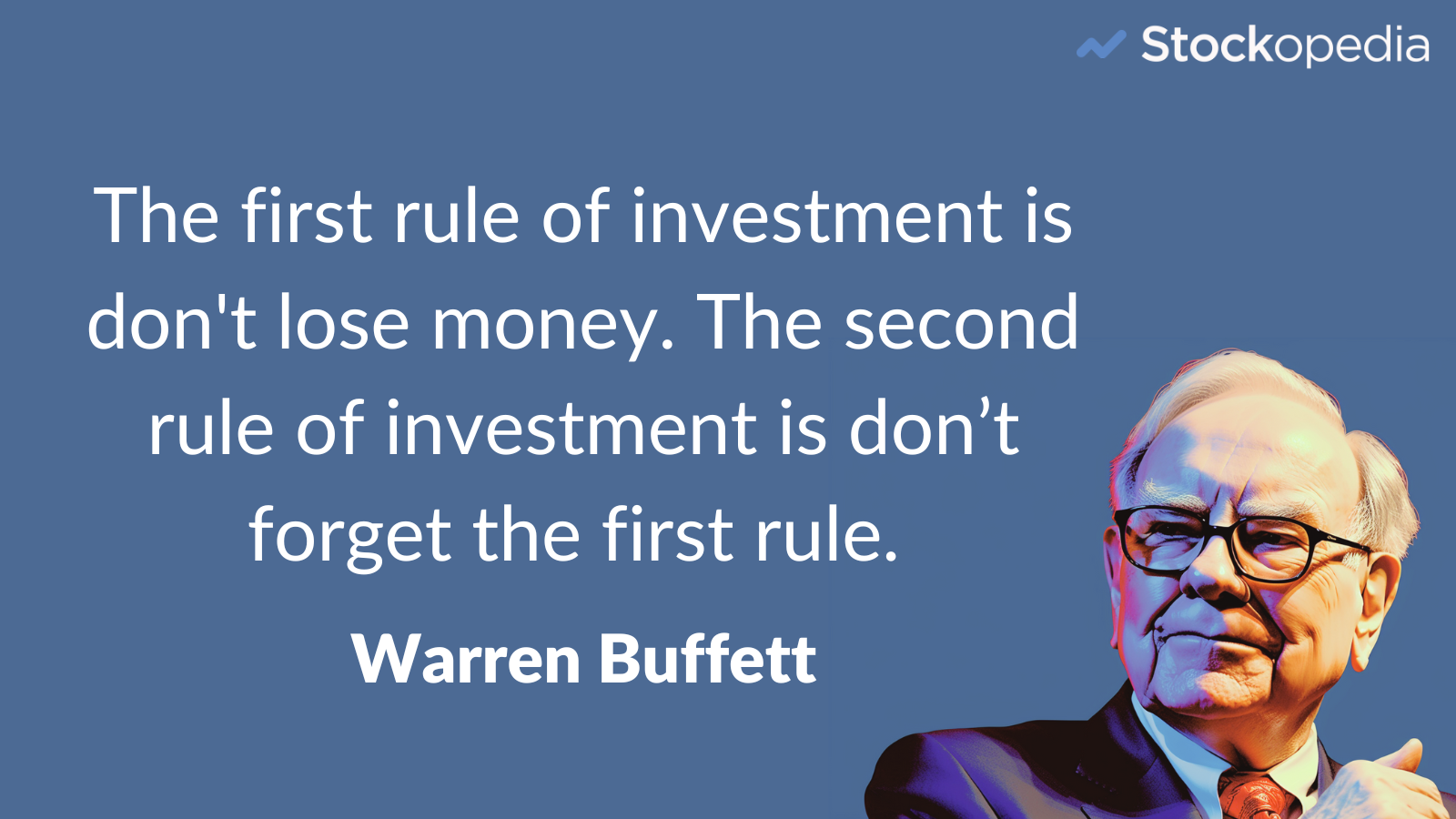

More than this, if you think “keeping losses small” is just a trader’s maxim, think again. None other than the great Warren Buffett has hammered home two rules of investment. Rule #1: don’t lose money. Rule #2: don’t forget the first rule.

Buffett is of course the greatest investor of all time and has an incredibly high hit rate for identifying long-term, compounding winners, but if he makes a mistake he gets out. It’s not exactly easy when you invest at the scale he does, but his Tesco investment is a good example. Bought in 2006, the business deteriorated through 2013. He was mostly out in 2014. While Tesco hasn’t slumped more since, the opportunity cost of having his capital in an underperforming stock was significant. He had better uses of the funds. Don’t hold losers.

Of course, Warren Buffett’s approach to avoiding losses is to ensure that all purchases are made with a significant Margin of Safety between the price paid and the true intrinsic value of the investment. This lesson was taught by his tutor Benjamin Graham, the “Father of Value Investing” as the most important principle of investment. If you buy with a high Margin of Safety the likelihood of significant losses is reduced. He also espoused broad diversification across undervalued stocks to ensure the risk of losses on a single investment could not impair capital to a significant degree.

Whatever your style of investing, not losing money is the most important principle for ensuring strong gains. If you keep your losses small, the gains take care of themselves.

What to do with losses

The book The Art of Execution by Lee Freeman-Shor[1] has a useful model for what to do with losers. He studied the results of many fund managers over a multi year period. He identified the habits of fund managers handling losing positions and classified them as assassins, hunters and rabbits.

Assassins - those that act quickly and cut their losses on losing positions.

Hunters - those that bought more, averaging down when prices fell.

Rabbits - those that did nothing on losers. Stuck in the headlights.

He found that out-performing fund managers were decisive - either Assassins or Hunters - whereas Rabbits were consistent under-performers. So you only really have two options when you are present with a loss. Cut losses or average down. Doing nothing is not an option.

As an amateur investor, your ability to identify the right stocks to average down on may be more limited. If a share really does have a strong Margin of Safety, then purchasing more can make sense, but it's easy to become extremely overconfident on even a limited amount of research. You may well be wrong. Not only this, but if a share price falls, it has negative momentum and many investors will have regretted their purchase at higher prices. These present headwinds to share price recovery. This is why I personally believe taking an assassin approach is quite a sensible approach for many investors.

Using stop losses to keep losses small

Much of the professional investment community rejects stop losses, mostly because they are hard to use when deploying large scale funds, but individual investors, deploying smaller capital, have no such constraint.

The mistake that most investors make with stop losses is to use the same stop loss level for all positions. They pick something arbitrary like 10% and wonder why they get whipsawed out of their small cap positions regularly. There’s nothing worse than selling your position on a 10% loss only to see the stock bounce back above your purchase price the next day.

The key is to set stop loss levels in relation to a share’s price volatility. More volatile shares are more likely to hit tight stop loss levels. So use wider stop levels for more volatile shares.

A reasonable shortcut is to use Stockopedia’s RiskRating Classifications or the “6 month Volatility” metric which is available to add to tables. I find that using the 6 month share price volatility (or less) to be a reasonably effective stop loss level for many shares.

In terms of coupling stop loss levels to the RiskRatings, I’ve found the following rules of thumb quite useful. We applied these in our Staff Investment Club to good effect, one example being LoopUp which we were stopped out of at 192p for a 22% loss. LoopUp’s shares hit a low of 2p.

The RiskRatings are published at the top of all StockReports in the Classifications section.

If you can’t stomach stop losses…

And just to finish off this piece, if you don't use stop losses then there is one final rule. It was first promoted by Peter Lynch in his essential One Up On Wall Street[2] and reiterated by Jim Slater in his excellent Zulu Principle[3] pair of books.

Sell when the story has materially changed.

As a stock picker, whenever you buy a share, it's imperative to have a strong grasp of the "story". Peter Lynch will try to write a two-minute monologue about a share’s narrative, which he would use to clarify his thinking, and refer back to through time. Keeping a journal, or record, of the reasons why you bought a share can help you reassess the continued investment case when things change.

Things do change. Profit warnings. Management mistakes. Di-worseifications. Competition. Limits to growth. External disasters.

The great lesson I learned very early on with CBTSY, was that you should cut your losses as soon as the story has changed. Even if it’s the very next day.

I am sure that many in the community have their own rules for keeping losses small. Ultimately, the best is to buy with a good margin of safety and time the buy well - arts in themselves.

Please let me know your own thoughts and principles, and I'll try and reply when I can.