The relationship between risk and return

Most investors believe in the theory that risk and return are joined at the hip. The idea persists that to achieve higher returns you have to take on more risk.

While this may be true across different asset classes (for example, high volatility stocks do tend to outperform low volatility cash), the theory appears to fall apart within stocks. Research studies by famous academics and practitioners including Haugen & Baker[1], Blitz & van Vliet[2] and Frazzini & Pederson[3] have proven that historically low volatility (and low beta) shares outperform high volatility shares over the long run (on a risk adjusted basis).

The reason for this ‘anomaly’ is due to a few primary factors. Firstly, investors are often averse to borrowing money to invest in low volatility equities; secondly, the investment process at institutions is often biased towards risk-seeking by fund managers who seek to improve their bonuses in the short term; thirdly, private investors often aim for Lottery type rewards from high risk investments. All these factors, and more, ensure that higher risk assets are often systematically over-priced, reducing their eventual returns and inverting the risk-return relationship.

Whatever the reason, the fact remains that so many private investors chase high risk / speculative shares at precisely the wrong moment. As we’ll see, there are good times and areas of the market to invest in high risk shares, but over the long term, and in general, a conservative bias in the stock market does bring additional rewards.

For those inclined to investigate the academic research we recommend the research papers listed in the conclusion of this guide.

Understanding RiskRating Performance

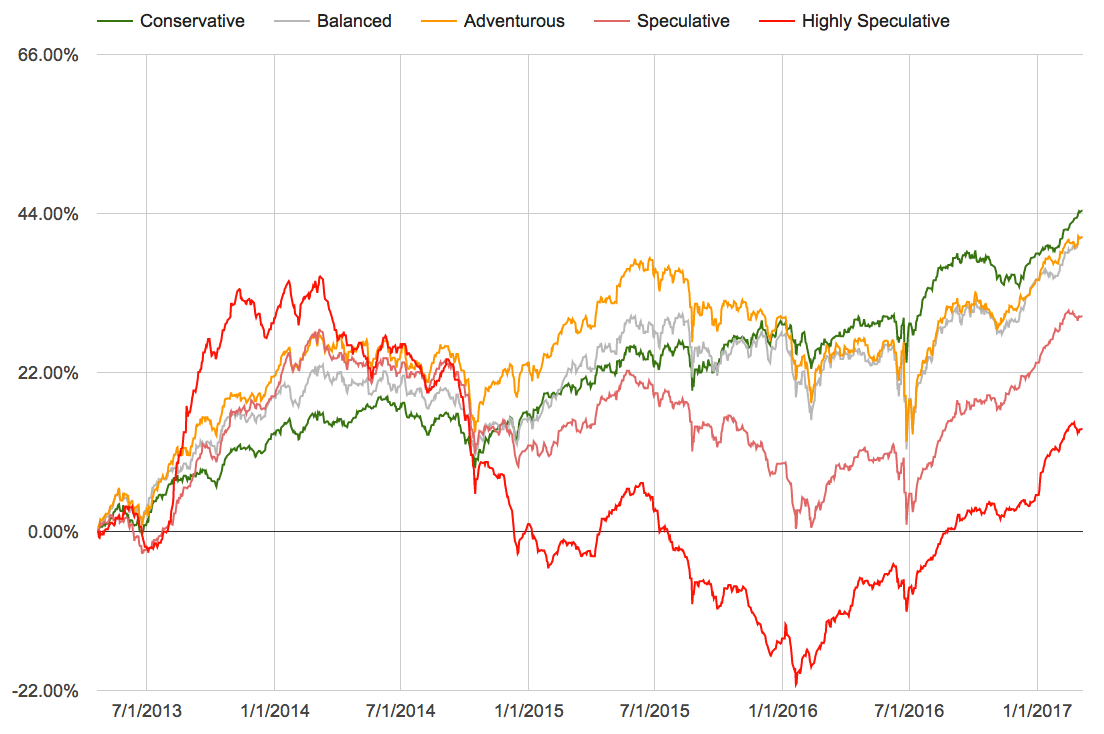

To prove the Low Volatility effect exists outside of the academic realm, we have conducted our own performance study using our own RiskRatings (you can read about our RiskRatings here) across UK securities back to April 2013. We calculated RiskRatings on 31 December each year and constructed equally weighted portfolios of all shares with a greater than £10m market cap at the time. The portfolio performances were tracked for the year and then the portfolios were rebalanced with new RiskRatings. The results are shown in the chart below.

We can draw the following insights:

The Conservative (lowest volatility) classification has tended to outperform the other segments over the longer term, falling less in negative markets, but rising more slowly in rising markets.

The higher volatility segments (from Adventurous to Highly Speculative) outperform considerably during ‘risk on’ market periods, but fall faster and harder in downswings and ‘risk off’ periods.

The Risk-Adjusted-Return (Sharpe Ratio) of each classification declines with increasing volatility.

These insights reflect the findings from the academic research literature into the Low Volatility Anomaly.

A note of caution

Markets tend to swing between what are known as “Risk on” and “Risk off” periods. While Conservative or Balanced stocks may outperform over the longer term, portfolios of these stocks will likely considerably underperform more speculative, adventurous shares in bullish market periods.

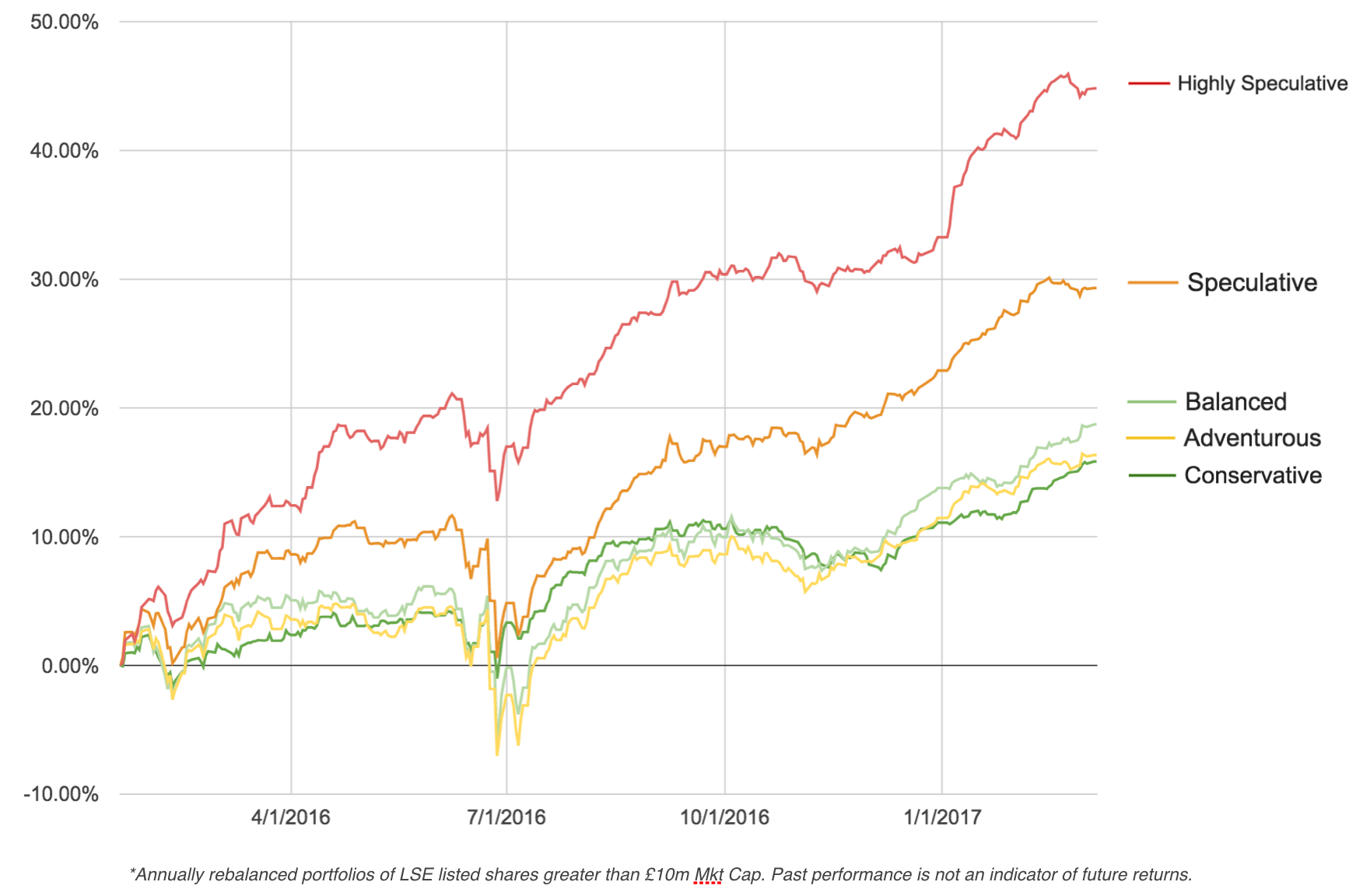

Most investors looking at the above performance chart think that conservative stocks win out so 'I’ll just buy conservative stocks'. While this may be a great long term strategy, one has to consider how such an investor would be feeling if they had bought a Conservative portfolio at the beginning of a ‘risk-on’ period (such as 2016 ) and held for 18 months. Have a look at this chart:

When all your friends are making a fortune in speculative shares it can be very hard to stick to your guns in a conservative strategy. Our experience suggests that many will throw in the towel right at the time that speculative shares hit the top of the cycle. Drastic underperformance of these segments in risk-off markets often leads to great financial pressure.

As markets are unpredictable, and temporary underperformance can feel unbearable to many, constructing an all-weather portfolio may minimise the risk of both long term and short term underperformance. The simplest way to do this is to build a portfolio diversified across the RiskRatings.

This may provide a portfolio with some conservative spine to steady the ship in downswings, and enough speculative thrust for meaningful participation in rallies.